Ophthalmic Knives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Knives Market Analysis by Mordor Intelligence

The Ophthalmic Knives Market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 1.89 billion in 2026 to reach USD 2.32 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031).

Demand holds steady because cataract surgery volumes keep rising, even as femtosecond laser platforms sharply reduce effective phacoemulsification time and begin to displace manual blades. Growth also reflects greater procedure throughput at outpatient facilities, ongoing material innovations such as diamond-like carbon coatings, and the push for infection-free single-use kits. At the same time, sustainability mandates complicate disposable adoption, and price pressure from declining reimbursement nudges many facilities toward reuse schemes. Consolidation among suppliers accelerates, with leading players pairing blade portfolios with laser technology and digital workflow tools to protect share in an environment of rapid technology substitution.

Key Report Takeaways

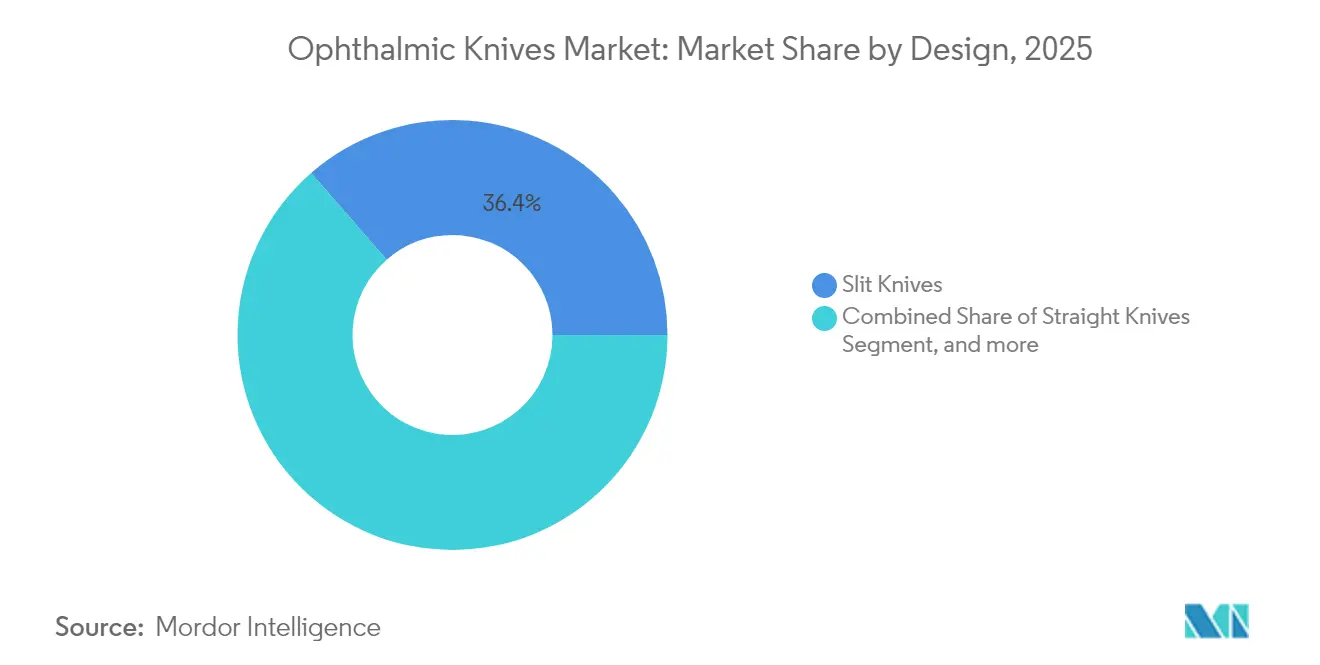

- By design, slit knives held 36.42% of ophthalmic knives market share in 2025, while MVR knives are projected to expand at a 5.71% CAGR to 2031.

- By product, reusable blades accounted for 63.38% of the ophthalmic knives market size in 2025, whereas single-use options are growing at a 7.26% CAGR.

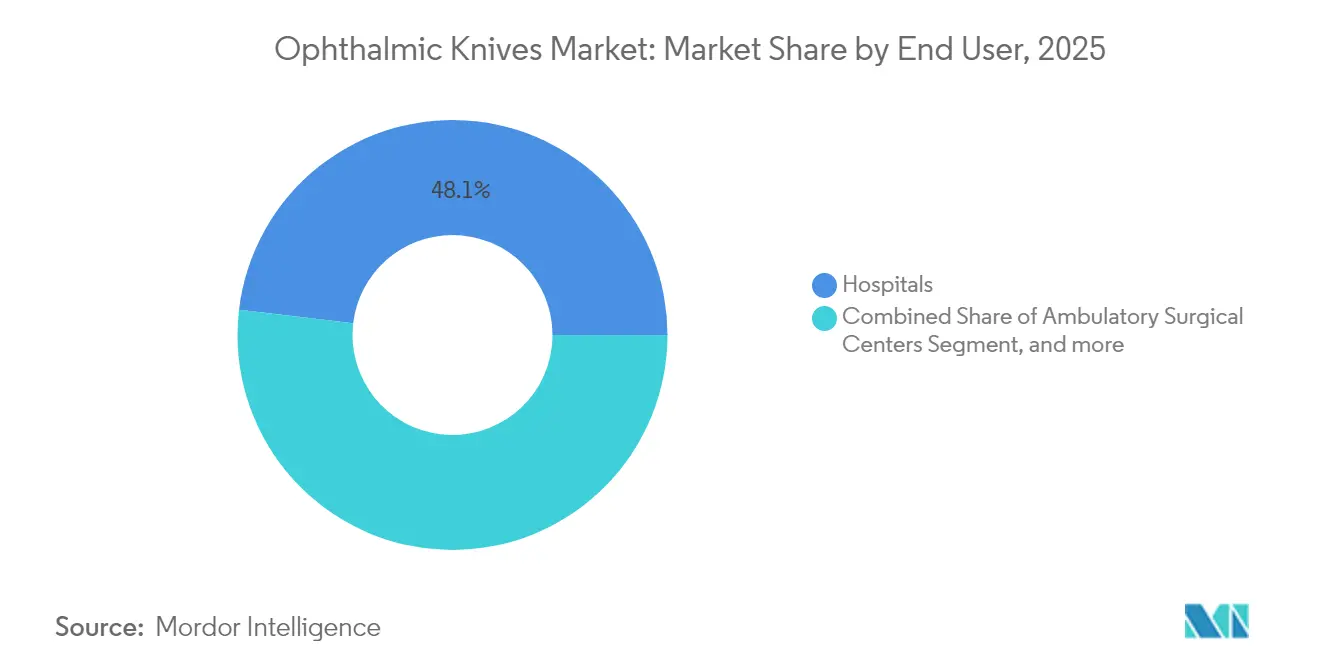

- By end-user, hospitals led with 48.12% revenue share in 2025; ambulatory surgical centers (ASCs) post the fastest growth at 8.21% through 2031.

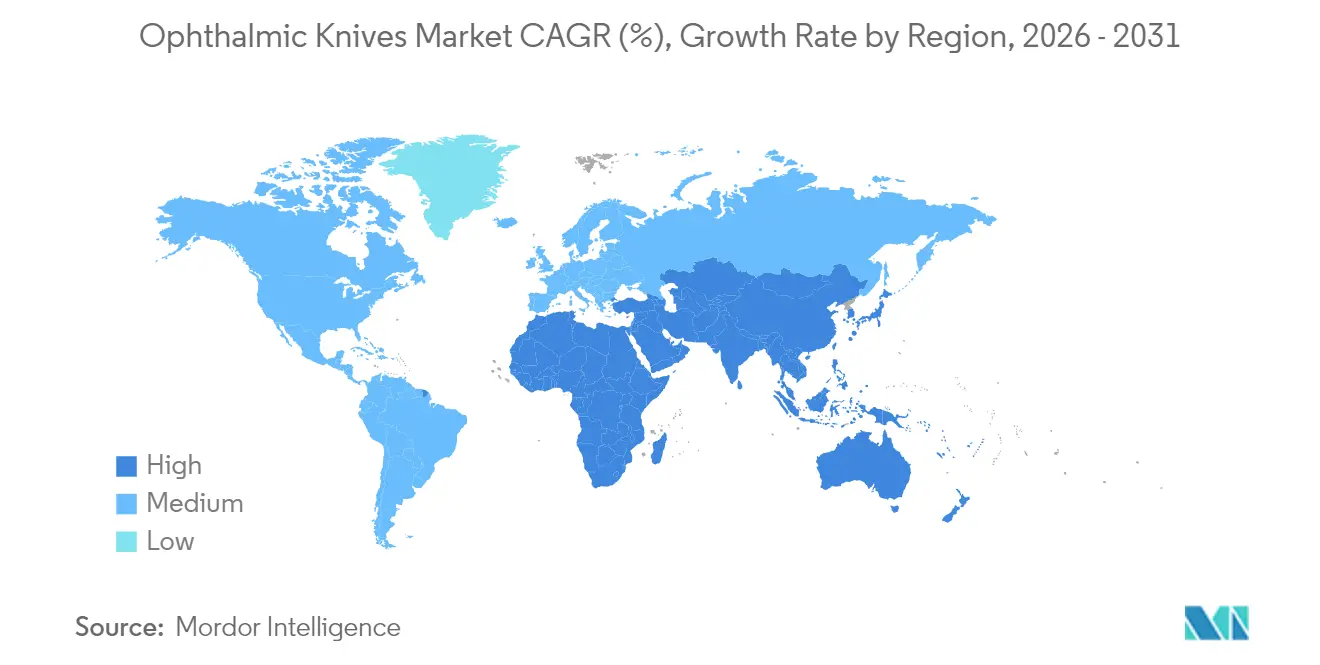

- By geography, North America captured 36.02% of 2025 revenue, while Asia-Pacific is advancing at a 5.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmic Knives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence of Ophthalmic Diseases | +1.2% | Global, with higher impact in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Aging Population & Cataract Prevalence | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Technological Advances in Blade Materials | +0.7% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Shift Toward Day-Care / Minimally-Invasive Cataract Surgery | +1.1% | North America & EU, spillover to emerging markets | Medium term (2-4 years) |

| Rise of Mobile Eye-Care Camps in Emerging Markets | +0.4% | APAC core, expansion to MEA and Latin America | Short term (≤ 2 years) |

| Additive-Manufactured Custom Geometries Enabling Niche Procedures | +0.3% | North America & EU, selective adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Ophthalmic Diseases

Cataract remains the principal cause of avoidable blindness, and disability-adjusted life years linked to lens opacity continue to rise in low-sociodemographic regions. Mobile surgical camps in India now deliver more than 10 000 cataract procedures annually, achieving 79.3% rates of 6/9 visual acuity or better.[1]Indian Journal of Ophthalmology, “Performance Metrics of Mobile Eye Surgical Units,” ijo.in China’s registry shows phacoemulsification in 94.93% of cataract operations, underscoring the continuing need for high-precision incision tools. This sustained disease burden anchors baseline demand for every major blade design even as femtosecond systems gain ground.

Aging Population & Cataract Prevalence

Global demographic shifts add millions of procedures each year; by 2050 annual cataract surgeries are projected to reach 50 million. Office-based centers in the United States now exceed 150 locations and help alleviate hospital capacity constraints without compromising safety standards. Although Medicare payments have fallen 51% in real terms since 1982, procedure volumes tied to an older patient pool keep overall blade consumption trending upward.

Technological Advances in Blade Materials

Researchers have produced diamond knife tips below 60 nanometers using low-energy oxygen ion beam machining, enabling cleaner corneal entry and faster wound sealing.[2]Journal of the European Optical Society, “Nanometric Diamond Knife Tip Fabrication,” jeos.org Ultra-thin 100-micrometer crescent blades improve control in glaucoma flap creation. Disposable silicon blades tested ex-vivo now deliver cutting performance similar to diamond, adding options for cost-sensitive markets.

Shift Toward Day-Care / Minimally-Invasive Cataract Surgery

ASCs gain share because they match hospital quality while lowering overhead for payers and providers. Disposable kits that remove sterilization steps dovetail with fast-turnover schedules, reinforcing the 7.72% growth trajectory for single-use blades. Microincisional techniques rely on sub-2 mm trapezoidal designs to maintain wound integrity, further stimulating demand for specialty geometries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost of Premium Knives | -0.8% | Global, acute impact in emerging markets | Medium term (2-4 years) |

| Reimbursement Pressure on Ambulatory Surgery Centers | -1.2% | North America & EU, expanding globally | Short term (≤ 2 years) |

| Regulatory Sustainability Rules Restricting Single-Use Plastics | -0.6% | EU leading, adoption in other regions | Medium term (2-4 years) |

| Rapid Adoption of Femtosecond Lasers Displacing Manual Knives | -1.4% | North America & EU, selective APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost of Premium Knives

Multi-layer diamond coatings push individual blade prices well above stainless-steel alternatives, straining budgets in markets where reimbursement is flat or declining. Facilities in Latin America and parts of Southeast Asia often reuse premium knives beyond manufacturer guidance to amortize costs, a practice that heightens sterilization risk and tempers replacement demand.

Rapid Adoption of Femtosecond Lasers

More than 950 LenSx systems are installed worldwide, and surgeons report capsulotomy satisfaction scores above 9 on a 10-point scale. In controlled studies effective phaco time drops by 83.6% when lasers replace manual incisions.[3]American Academy of Ophthalmology, “Femtosecond Laser–Assisted Cataract Surgery Outcomes,” aao.org Alcon’s USD 430 million LENSAR acquisition signals deeper integration of laser workstations into the mainstream surgical suite. As capital costs fall and throughput rises, manual blade volumes risk erosion, particularly in high-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: MVR Knives Lead Specialty Growth

MVR knives posted the fastest 5.71% CAGR and benefit from surging vitreoretinal procedure complexity linked to diabetes and age-related macular degeneration. Slit knives still command the largest slice of ophthalmic knives market share at 36.42% in 2025, reflecting their utility in both primary and secondary cataract incisions. Crescent and straight blades serve niche anterior applications, but additive manufacturing is beginning to deliver bespoke angles and shaft lengths that broaden surgeon choice. Diamond-like carbon coatings lengthen edge life and improve tissue glide, encouraging uptake for multi-procedure packs in teaching hospitals. Yet femtosecond adoption tempers volume expectations beyond 2028 as laser capsulotomy reduces reliance on manual entry for routine cataract surgery. To offset the shift, suppliers emphasize ultra-high-precision MVR variants and hybrid packages that bundle vitreoretinal blades with disposable cannulas.

The design segment shows resilience because not all health systems can finance lasers, and because certain glaucoma, pediatric, and trauma cases still demand tactile feedback unavailable in robotic or laser platforms. Furthermore, custom 3D-printed trial blades let innovators explore asymmetric bevels suited to irregular corneas, opening incremental revenue channels. Slit knife suppliers are integrating radio-frequency identification tags to track sterile reprocessing cycles, a move that aligns with hospital quality metrics while locking customers into proprietary asset-management software, thereby stabilizing their foothold in the ophthalmic knives market.

By Product: Single-Use Gains Despite Reusable Dominance

Reusable instruments accounted for 63.38% of the ophthalmic knives market size in 2025 because budget-pressed centers spread acquisition cost across dozens of cycles. High-volume Indian and Brazilian state programs commonly sterilize stainless blades more than 40 times, underscoring this economic logic. Disposable kits, however, are growing 7.26% annually, propelled by more stringent infection control rules after widely publicized endophthalmitis clusters in 2024. The FDA’s revised Quality Management System Regulation, effective February 2026, requires documented risk mitigation, making single-use pathways attractive for facilities unwilling to invest in automated tracking of reprocessing.

Sustainability rules complicate this trajectory. The EU Packaging and Packaging Waste Regulation, active from August 2026, caps landfill waste and restricts virgin plastics, spurring research into bio-based handles and recyclable blister packs. Manufacturers now pilot mechanical recycling loops in Germany, where ground polymer from single-use handles reenters non-clinical products. While surgeons favor the sharpness consistency of disposables, survey data show 79% perceive operating-room waste as excessive, foreshadowing a gradual migration toward hybrid portfolios that mix reusable shafts with modular, minimally-wasteful cutting tips.

By End-User: ASCs Drive Market Evolution

Hospitals retained 48.12% revenue in 2025 owing to complex case referral patterns and embedded procurement agreements. Nonetheless, ambulatory surgical centers exhibit an 8.21% CAGR through 2031, boosted by same-day discharge convenience, tighter case scheduling, and the elimination of overnight nursing costs. Medicare’s site-neutral reimbursement framework pays ASCs roughly USD 1 329 for cataract surgery in 2025, making outpatient settings financially compelling despite a concurrent 2.8% physician fee cut. Specialty eye clinics lie between the two extremes, thriving on patient-centric branding but facing higher per-unit supply costs due to lower throughput.

Mobile surgical units expand reach in densely populated developing regions. India’s flagship program now fields buses equipped with laminar-flow theatres, completing cataract rounds in under 20 minutes and generating fresh demand for portable single-use blade packs. In the United States, office-based suites inside group practices perform more than 50 000 cataract cases annually, an evolution that favors compact disposable kits to simplify logistics and comply with state sterilization statutes. Together, these patterns reshape procurement priorities and keep the ophthalmic knives market firmly oriented toward highly efficient, procedure-ready solutions.

Geography Analysis

North America commanded 36.02% of 2025 revenue thanks to roughly 4 million cataract procedures, fast adoption of premium coatings, and widespread use of ASCs. Femtosecond penetration exceeds 40% of cataract theaters, yet manual blades remain indispensable for backup and for surgeons who favor tactile feedback. Ongoing cuts to the Medicare conversion factor exert margin pressure, pushing providers toward blended reusable–disposable models that safeguard cash flow while meeting Centers for Medicare & Medicaid Services infection benchmarks.

Asia-Pacific is the fastest-growing territory at a 5.28% CAGR. China alone anticipates a 223.54% jump in cataract prevalence through 2030, and national surgical registries confirm that phacoemulsification dominates 94.93% of cases, anchoring demand for compatible incision blades. India’s mobile eye camps demonstrate cost-effective outreach, with favorable visual outcomes sustaining steady inventory turnover for single-use packs. Mature markets such as Japan and Australia pursue premium diamond blades for microincisional glaucoma surgery, while Indonesia and Vietnam purchase cost-optimized steel sets to fit public-sector budgets.

Europe follows closely, driven by Germany, United Kingdom, France, and Italy. The EU Medical Device Regulation 2017/745 imposes rigorous post-market surveillance, favoring suppliers with strong quality systems. Simultaneously, the bloc’s waste-reduction law compels design shifts toward recyclable or reusable components, reinforcing innovation in low-waste blade handles. Eastern European modernization programs attract vendors with mid-price stainless products, keeping growth momentum intact despite reimbursement ceilings. Overall, environmental compliance and high clinical standards give Europe an outsized influence on the next generation of blade technology in the ophthalmic knives market.

Competitive Landscape

Competition remains moderately fragmented. Alcon leads after reporting USD 9.8 billion in surgical revenue for 2024 and deepening its vertical stack with the USD 430 million LENSAR laser deal. Bausch + Lomb, Mani, and Microsurgical Technology follow, each refining proprietary edge geometries and launching mobile-friendly disposable lines to address outreach programs in Asia and Africa. Large players emphasize closed-loop supply, bundling blades with viscoelastics, drapes, and in-theatre analytics to secure multi-year tenders.

Material innovation fuels differentiation. One supplier now coats stainless blades with a 7.8 GPa soft diamond-like carbon layer that preserves biocompatibility yet withstands 40 autoclave cycles without edge rounding. Another is trialing nitinol shafts that flex to accommodate deep-set orbits, lowering incision stress in paediatric cases. Additive manufacturing lets small entrants carve niche positions by offering surgeon-specific bevels delivered within days, a capability that integrated multinationals are beginning to replicate through on-demand printing hubs.

Regulation shapes the field. The FDA’s enhanced Quality Management System Regulation arriving in 2026 rewards companies with real-time complaint handling and unique device identification pathways embedded in enterprise resource planning platforms fda.gov. Firms unable to absorb compliance costs may exit or sell portfolios, setting the stage for further consolidation. Conversely, sustainability mandates open white space for newcomers marketing recyclable handles or take-back schemes. As strategic alliances form between laser platform owners and blade makers, competition tilts toward ecosystem control rather than stand-alone instrument excellence, a trend expected to accelerate through 2030 in the ophthalmic knives market.

Ophthalmic Knives Industry Leaders

Optiedge, India

Paramount Surgimed Ltd

Surgistar

Alcon

Ophtechnics Unlimited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The All India Institute of Medical Sciences (AIIMS) has achieved a significant milestone by performing its first-ever gamma knife radiation treatment for retinoblastoma, a rare eye cancer primarily affecting children under five years old. This marks a major advancement in ophthalmic oncology, as AIIMS expands the application of this highly precise radiation therapy beyond its previous use for choroidal melanoma cases in adults.

- April 2025: Microsurgical Technology (MST) has entered into a strategic partnership with Mani Inc. to enhance the distribution of ophthalmic surgical blades in the United States. Under this agreement, MST will serve as the exclusive distributor of Mani’s specialized surgical blade portfolio, strengthening its market presence and expanding access to high-quality ophthalmic surgical tools for healthcare professionals. This collaboration is further bolstered by the establishment of Mani Medical America, a newly formed U.S. subsidiary of Mani Inc., which will provide additional support for operations and customer engagement in the region.

- February 2025: McKesson Corporation announced agreement to acquire 80% controlling interest in PRISM Vision Holdings for approximately USD 850 million, expanding its ophthalmology market presence across 91 locations and seven ambulatory surgery centers.

- June 2024: HumanOptics introduced a fresh brand image and expanded product offerings at the DOC Congress 2024 in Nuremberg. As part of this transformation, the company is launching the EXTRA IN VISION campaign, reflecting its commitment to cutting-edge ophthalmic solutions. Alongside this initiative, HumanOptics is unveiling a revamped company logo, reinforcing its new corporate identity.In addition to these branding updates, the German manufacturer of premium implants for eye surgery is expanding its portfolio with new disposable surgical knives. These include phaco knives (slit knives) featuring the optimized Smart Shape design and other specialized instruments that extend beyond standard cataract procedures. This strategic move enhances HumanOptics' product range and reinforces its position as a leading innovator in ophthalmic surgery.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global ophthalmic knives market as the value of all reusable and single-use blades engineered to cut corneal or scleral tissue during cataract, refractive, vitreo-retinal, and glaucoma surgeries. According to Mordor Intelligence, the market will reach USD 1.82 billion in 2025.

The sizing deliberately omits femtosecond laser equipment, handheld forceps, and non-surgical diagnostic blades.

Segmentation Overview

- By Design

- Straight Knives

- Crescent Knives

- Slit Knives

- MVR Knives

- Others

- By Product

- Reusable Ophthalmic Knives

- Single-Use Ophthalmic Knives

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cataract surgeons, ASC procurement heads, and specialty-blade distributors across North America, Europe, China, India, and Brazil. Dialogues clarified average knives used per case, reusable turnover cycles, and regional preferences for diamond versus stainless steel tips, which sharpened model assumptions picked from desk work.

Desk Research

We first mapped supply using open datasets such as WHO Vision Atlas, FDA 510(k) device clearances, Eurostat trade code 9018.90 export flows, and OECD Health Statistics, which reveal procedure volumes and import trends. Company 10-Ks, investor decks, and specialty-surgery journals provided price corridors and material splits. Paid resources, including D&B Hoovers for manufacturer revenue, Dow Jones Factiva for tender notices, and Questel for patent intensity, helped us size competitive footprints. These examples illustrate, but do not exhaust, the secondary sources consulted.

Market-Sizing & Forecasting

We reconstruct demand top-down. Age-adjusted cataract, refractive, and retinal procedure counts are multiplied by average knives consumed per surgery, then valued with regional ASP bands. Bottom-up cross-checks, sampled OEM revenue splits and distributor channel checks, backstop totals before adjustments. Key variables include (1) annual cataract surgery growth, (2) disposable-to-reusable shift ratio, (3) average selling price erosion, (4) ASC share of eye procedures, and (5) regulatory uptick tied to FDA and EU MDR sterilization rules. A multivariate regression anchored on those drivers projects figures through 2030, while scenario analysis captures policy or technology shocks.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated anomaly flags, peer comparison, and senior analyst sign-off. We refresh models each year and issue interim tweaks when recalls, reimbursement changes, or currency swings materially move the baseline.

Credibility Corner: Why Mordor's Ophthalmic Knives Baseline Stands Firm

Published estimates often diverge because firms pick dissimilar device baskets, price anchors, and refresh cadences. Our scope sticks to knives only, values them at ex-factory ASPs, and updates annually, so clients see a stable yet current reference point.

Principal gap drivers versus external figures involve inclusion of handheld scissors, hospital transfer pricing, or a static 2023 currency set, which we avoid by triangulating both procedure data and supplier revenue before inflation-adjusted conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.82 B (2025) | Mordor Intelligence | - |

| USD 2.16 B (2023) | Global Consultancy A | Bundles other handheld instruments and applies list-price ASPs |

| USD 0.39 B (2023) | Trade Journal B | Counts only diamond blades sold through hospital pharmacies |

| USD 2.24 B (2024) | Industry Tracker C | Uses distributor invoice values, no adjustment for multi-knife usage per case |

These contrasts show that our disciplined scope selection, dual-path modelling, and yearly refresh deliver a balanced, transparent baseline buyers can reproduce with clear inputs, even when other sources swing widely.

Key Questions Answered in the Report

What is the current size of the ophthalmic knives market?

The Ophthalmic Knives Market is valued at USD 1.89 billion in 2026 and is forecast to grow to USD 2.32 billion by 2031.

Which end-user segment is expanding the fastest?

Ambulatory surgical centers are growing at an 8.21% CAGR through 2031, outpacing hospitals and specialty clinics.

How are femtosecond lasers influencing demand for manual blades?

Laser systems reduce effective phacoemulsification time by up to 83.6%, gradually displacing manual knives in high-income regions while leaving a large residual need in cost-sensitive markets.

Why are single-use ophthalmic knives gaining ground despite higher waste?

Infection-control protocols and the FDA’s 2026 Quality Management System Regulation favor disposables, driving a 7.26% CAGR even as EU waste rules prompt recyclable designs.

Which geographic region shows the strongest growth through 2031?

Asia-Pacific leads with a 5.28% CAGR, boosted by China’s expanding cataract caseload and India’s mobile surgical programs.

What materials innovations are improving blade performance?

Diamond-like carbon coatings and sub-60 nm diamond tips deliver cleaner cuts and longer edge life, enhancing surgical precision and supporting premium pricing.

Page last updated on: