Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

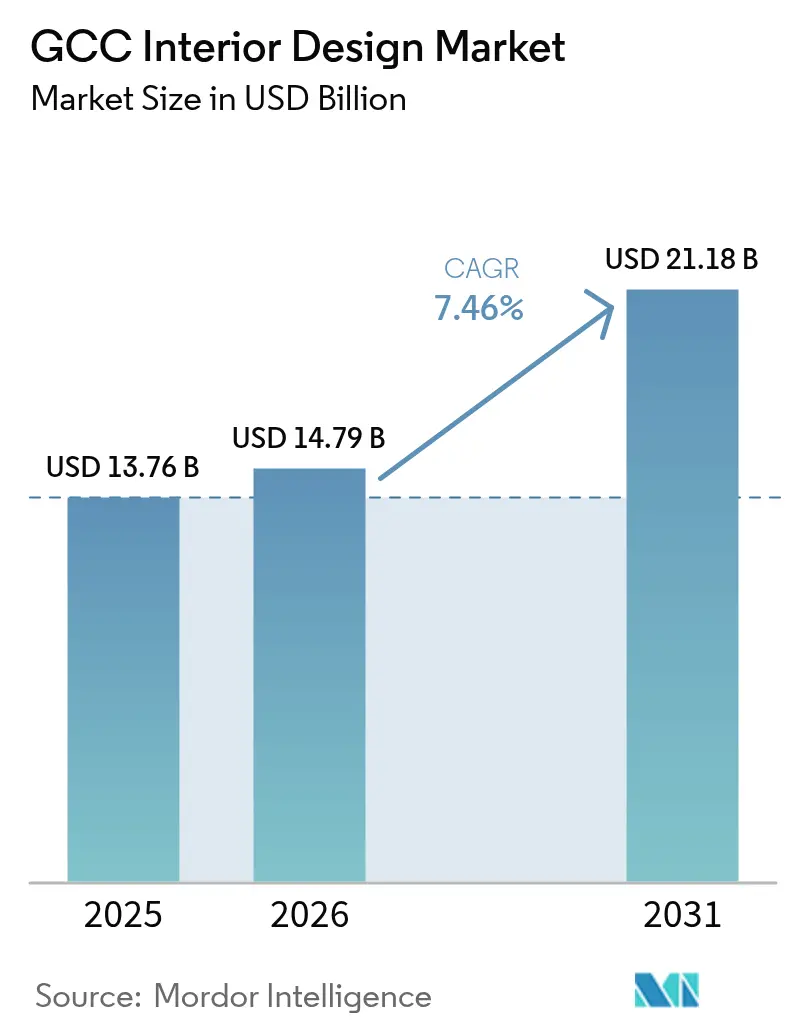

| Base Year Market Size (2025) | USD 13.76 Billion |

| Market Size (2026) | USD 14.79 Billion |

| Market Size (2031) | USD 21.18 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Interior Design Market Analysis by Mordor Intelligence

The GCC interior design market size in 2026 is estimated at USD 14.79 billion, growing from 2025 value of USD 13.76 billion with 2031 projections showing USD 21.18 billion, growing at 7.46% CAGR over 2026-2031. The robust growth trajectory stems from the region’s sweeping Vision 2030 programs, an accelerating hospitality pipeline, and sustained migration of high-net-worth individuals into tax-advantaged Gulf jurisdictions[1]Source: Vision 2030, “AlWadi,” vision2030.gov.sa.. Strong renovation activity, which holds 51.36% of current revenues, signals a mature ecosystem in which upgrade cycles cushion the industry from new-build volatility. Mega-projects such as Saudi Arabia’s Mukaab, NEOM, and Diriyah generate long-tail demand for specialized residential, commercial, and hospitality fit-outs that combine advanced digital workflows with culturally resonant aesthetics. ESG mandates and green-building incentives in the United Arab Emirates (UAE) and Saudi Arabia compel firms to integrate low-carbon materials, LEED and ILFI benchmarks, while BIM and VR adoption compresses design iterations and drives down rework costs. Talent shortages persist across skilled trades, yet companies that invest in upskilling and robotics gain a decisive execution edge. Price volatility in imported finishes remains the principal near-term headwind; however, ongoing localization initiatives across Gulf states aim to reduce supply-chain risk and stabilize input costs.

Key Report Takeaways

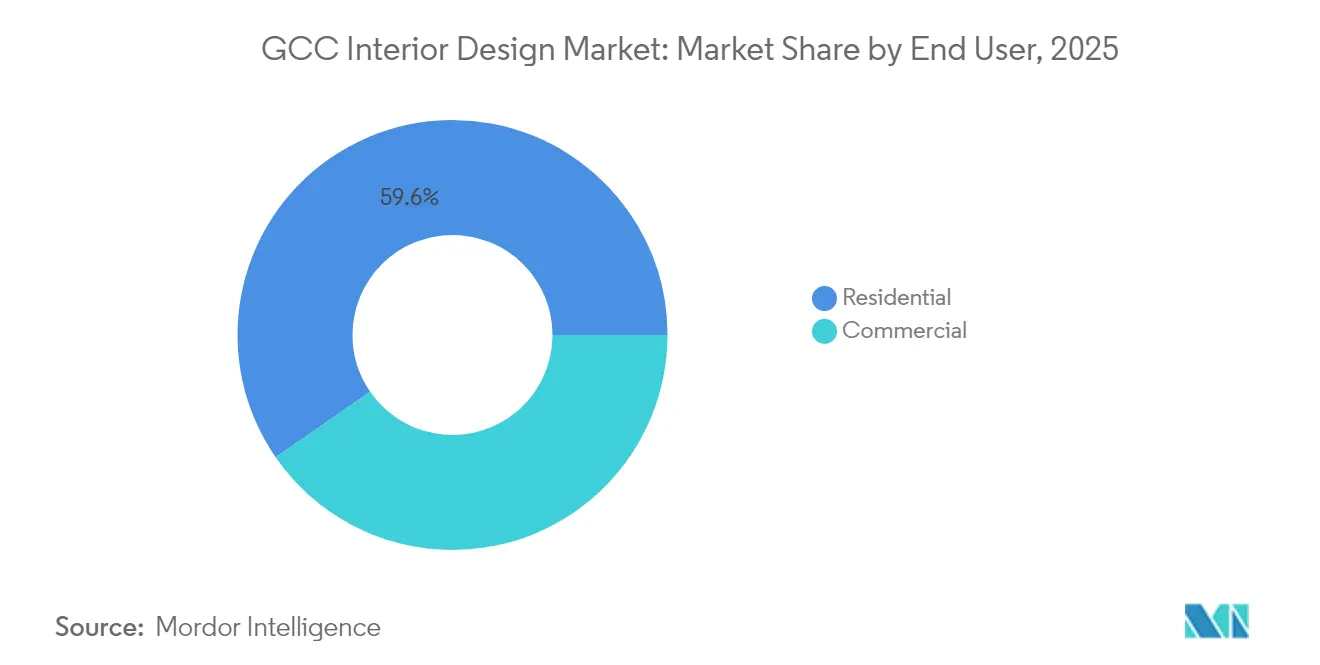

- By end-user, residential interior design captured 59.62% of the GCC interior design market share in 2025, whereas commercial applications are set to record the fastest 9.05% CAGR through 2031.

- By service type, renovation and remodeling commanded a 50.88% share of the GCC interior design market size in 2025 and is projected to deliver a 8.74% CAGR between 2026-2031.

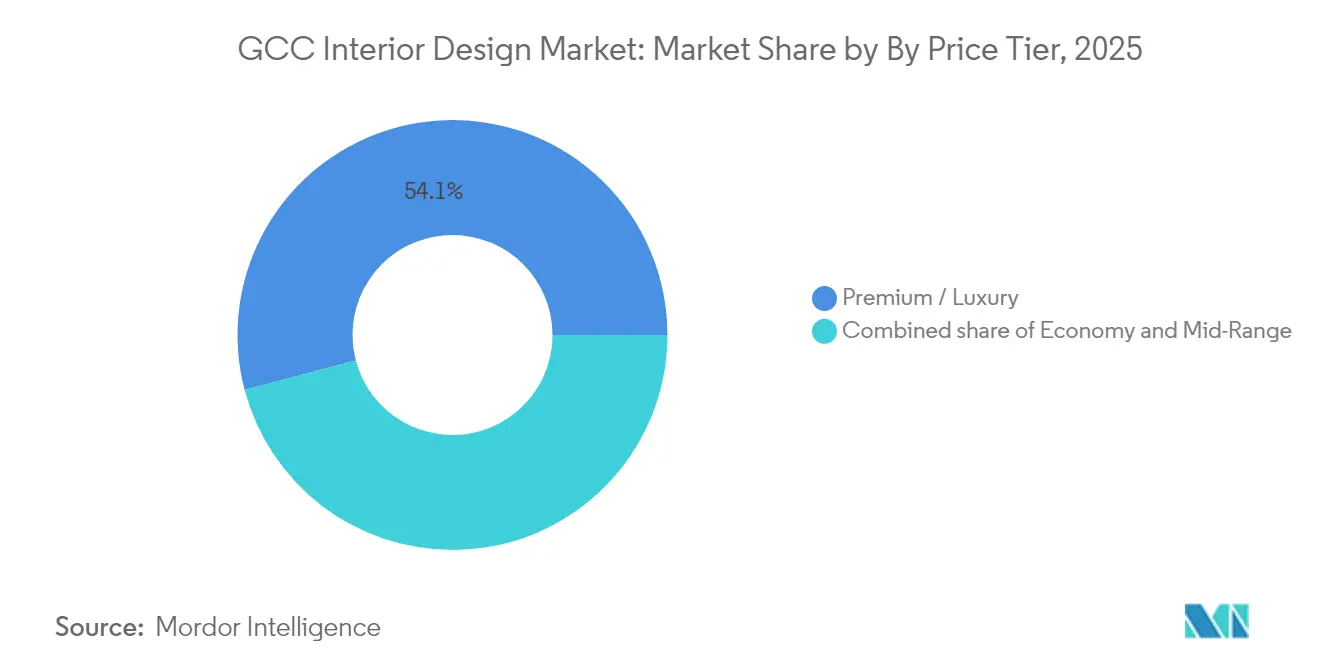

- By price tier, the mid-range/economy bracket contributed 45.88% of the 2025 GCC interior design market share, while premium and luxury offerings are forecast to expand at an 10.85% CAGR to 2031.

- By geography, Saudi Arabia held 39.05% o the GCC interior design market share for 2025, yet Qatar and the UAE are poised to advance at a 9.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Interior Design Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Residential Real-estate Investments | +1.2% | Saudi Arabia, UAE core with spillover to Qatar | Medium term (2-4 years) |

| Expanding Hospitality & Tourism Pipeline | +1.5% | UAE, Qatar, Saudi Arabia with Bahrain emergence | Long term (≥ 4 years) |

| Government-led Affordable-Housing Schemes | +0.8% | Saudi Arabia dominant, Kuwait secondary | Medium term (2-4 years) |

| High Net-worth Migration to GCC | +0.9% | UAE, Qatar primary with Saudi Arabia growth | Long term (≥ 4 years) |

| Digitized Fit-Out Platforms (BIM/VR-based) | +0.6% | UAE leading, Saudi Arabia rapid adoption | Short term (≤ 2 years) |

| Green-Building Incentives & ESG Mandates | +0.7% | UAE mature market, Saudi Arabia accelerating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Residential Real-estate Investments

Riyadh-based ROSHN Group has committed SAR 350 billion (USD 93.3 billion) to master-planned communities that will eventually house more than 1.5 million residents, unleashing continuous demand for turnkey interiors across villas, apartments, and mixed-use amenities [2]Source: U.S. International Trade Administration, “Saudi Arabia Design and Construction ROSHN Project Opportunities,” trade.gov. Mixed-use formats require designers to orchestrate hospitality, retail, and office schemes alongside core housing units, elevating complexity and revenue potential in a single development. Luxury builders such as Dar Global are blending high-jewelry branding with interior packages at projects valued at SAR 880 million (USD 234 million), illustrating how design now anchors the marketing narrative rather than remaining an after-sales consideration. Off-plan sales in Dubai already exceed 60% of transactions, driving early-stage design engagement and long-run stickiness for specialist consultancies. Saudi Arabia’s Architecture Characters Map program requires heritage-aligned interiors in public projects, creating niche opportunities for culturally informed suppliers. As a real-estate pre-sales fund working capital, interior firms gain earlier payment schedules, improving cash flow and lowering project-completion risk.

Expanding Hospitality & Tourism Pipeline

Roughly 600,000 hotel rooms are under development across the Gulf, representing a USD 110 billion fit-out backlog that spans guest rooms, branded residences and adjacent F&B venues. Saudi Arabia aims to host 100 million visitors by 2030, and projects such as NEOM’s Trojena will introduce innovative ring-shaped hotels requiring bespoke interiors that integrate sustainability and luxury. UAE visitor spending is forecast to reach AED 228.5 billion (USD 62.26 billion) in 2025, prompting legacy properties to refurbish in order to remain competitive with next-generation assets[3]Source: HospitalityNet, “International Traveller Spend in UAE to Reach Record,” hospitalitynet.org. High-profile openings like Waldorf Astoria Residences Dubai underscore convergence between hospitality and high-end residential design, amplifying cross-segment competencies for leading studios. Qatar’s Art Mill Museum and Design Doha biennale enlarge the cultural tourism footprint, driving demand for museum-grade interior specialists. Besides pure revenue, marquee hospitality interiors elevate a firm’s portfolio branding, translating into pricing power in adjacent categories.

Digitized Fit-Out Platforms (BIM/VR-based)

Dubai Municipality now mandates BIM for large projects, accelerating adoption across the GCC interior design market and helping firms cut rework by double-digit percentages. VR walk-throughs shorten client approval cycles and unlock remote decision-making, a boon when stakeholders are dispersed across multiple countries. KEO International attributes 23% revenue growth partly to robotics-enabled manufacturing of bespoke joinery that syncs directly with BIM models. Oman’s construction sector, which contributes 9.20% of GDP, views BIM as central to quality assurance despite skills gaps, offering consultancies a chance to supply training and turnkey digital-delivery services. 4D-BIM platforms integrated with VR safety modules decrease job-site incidents and support multilingual crews in the UAE, enhancing compliance with OSHAD regulations. As more developers demand digital twins for lifecycle asset management, firms with mature data ecosystems capture larger scopes including facilities-management handover.

Green-Building Incentives & ESG Mandates

The UAE mobilized AED 1 trillion (USD 272.48 billion) in sustainable finance that directly channels capital toward low-carbon interiors and renewable-ready MEP systems. Dubai alone counts more than 1,100 LEED-certified buildings, compelling even mainstream residential towers to include reclaimed-wood cabinetry, low-VOC paints and smart water fixtures. Forbes International Tower in Riyadh will source 100% clean energy, 75% from hydrogen, setting a high bar for specification of interior materials with embedded-carbon disclosure requirements. Saudi Arabia’s Green Initiative pursues net-zero by 2060, tightening codes on thermal performance and indoor air quality, which increases demand for data-driven design services that quantify sustainability ROI. GCC adherence to International Green Construction Code Chapter 8 places indoor environmental quality front-and-center, weaving air-monitoring sensors and daylight-optimization into interior briefs.[4]Source: International Code Council, “Chapter 8 Indoor Environmental Quality,” iccsafe.org. Developers now list ESG credentials alongside floor-area ratios in marketing brochures, indicating a structural shift from optional to mandatory sustainability features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Imported Furnishing Materials | -1.1% | GCC-wide with Saudi Arabia most exposed | Short term (≤ 2 years) |

| Cyclical Oil-Price Volatility | -0.8% | Kuwait, Saudi Arabia primary impact | Medium term (2-4 years) |

| Fragmented Regulatory Codes Across GCC | -0.4% | Regional coordination challenges | Long term (≥ 4 years) |

| Talent Shortage in Specialized Trades | -0.6% | Saudi Arabia, Qatar acute shortage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Furnishing Materials

Saudi Arabia’s Vision 2030 pipeline exceeds USD 850 billion, straining global supply chains for premium fixtures, stone and specialty lighting while exposing budgets to freight spikes and currency swings. A Qatar pricing study found economic and regulatory forces drive 47.30% of cost volatility in construction materials, with logistics adding another 22%, numbers that cascade directly into interior fit-out risk margins. The GCC paints and coatings market is forecast to hit USD 4.5 billion by 2027, yet resin costs track petrochemical indexes, subjecting project P&Ls to oil-derived feedstock variability. Local manufacturers focus on bulk ceramic tiles and gypsum boards, leaving gaps in high-end decorative metals and acoustic solutions. Designers increasingly write contingency clauses into contracts or recommend material alternates, but client acceptance varies with brand positioning.

Cyclical Oil-Price Volatility

Although GCC contract awards remained resilient at USD 167 billion during prior oil slumps, discretionary upgrade budgets for premium interiors contract when hydrocarbon revenues dip, extending sales-cycle duration. Econometric analysis confirms oil-price uncertainty negatively influences Saudi stock returns, indirectly dampening real-estate and fit-out investment appetites. While IMF data underscore Gulf progress in diversifying GDP composition, government outlays on mega-projects can slow if fiscal buffers erode, squeezing pipeline visibility. Kuwait’s real-estate macro score of 3.5 for H2 2024 signals resiliency yet also flags dependency on stable crude receipts for continued capex. Design firms hedge exposure by diversifying into public-sector education and healthcare interiors, which show counter-cyclical funding patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Commercial Acceleration Outpaces Residential Dominance

In 2025, the residential segment generated 59.62% of the overall revenue of the GCC interior design market as government-backed housing schemes and developer-led luxury towers dominated handovers, illustrating the consumer pull that still anchors the GCC interior design market. Yet the commercial category is forecast to clock a 9.05% CAGR to 2031, eclipsing residential growth and reshaping the demand profile toward office, retail, and hospitality packages. Landmark projects such as Dubai’s AED 10 billion (USD 2.72 billion) exhibition-center expansion add 180,000 sqm of leasable interiors, exemplifying scale advantages commercial specialists can harness. The GCC interior design market size for commercial jobs is therefore set to widen steadily, fueled by continued government diversification into finance, tourism, logistics, and events. Within commercial, the hospitality sub-set sees unprecedented order books as 600,000 new keys translate into standardized guest-room modules, back-of-house kitchens, and branded lobby concepts. Healthcare interiors offer an additional frontier; Bahrain’s King Hamad American Mission Hospital integrates 14,000 sqm of greenery that calls for biophilic and infection-control design expertise, opening a lucrative vertical for specialized firms.

The residential arena maintains absolute volume leadership, yet its growth moderates because high base effects and tightening mortgage rules in some markets slow new-sale velocity. Nevertheless, retrofit cycles, especially in Dubai’s first-generation freehold communities, sustain a healthy funnel of kitchen, bath, and smart-home replacements. Developers such as ROSHN increasingly integrate retail promenades within housing districts, blurring segmentation lines and allowing residential-focused studios to extend into adjacent commercial scopes. Premium villas surrounding Riyadh’s World Expo 2030 site adopt curated interiors that blend global luxury cues with Saudi heritage motifs, demanding cross-cultural storytelling skills from design teams. Renovation work tied to post-handover warranty periods further stabilizes revenue for firms with maintenance divisions. Cumulatively, the GCC interior design market will continue to see end-user cross-pollination, reinforcing the need for diversified service portfolios.

By Service Type: Renovation Dominance Signals Market Maturity

Renovation and remodeling earned 50.88% the GCC interior design market share in 2025 and will deliver a 8.74% CAGR through 2031, confirming that the GCC interior design market has reached a phase where asset-refresh cycles rival new-build projects in size and strategic relevance. Many first-wave malls, hotels, and residential towers commissioned during the 2005-2015 boom now require modernization to meet ESG codes and shifting consumer behaviors, driving sustained demand for rapid-turnaround interior refits. Digital scanners and BIM facilitate precise as-built modeling that minimizes demolition and accelerates re-installation, particularly in occupied commercial spaces where downtime carries hefty penalties. New construction interiors account for the remaining 49.12% of the GCC interior design market size, yet exhibit slightly lower growth because mega-project pipelines now span longer delivery horizons. Dubai’s target that 35% of new offices achieve LEED certification by 2025 forces legacy stock to retrofit, creating incremental pathways for renovation-centric suppliers.

Despite lower headline growth, new-build interiors remain indispensable for brand-new economic clusters like Saudi Arabia’s Mukaab, which alone offers 1.4 million sqm of office space that will come online after 2028 and require avant-garde design narratives. Renovation leaders leverage specialization in live-environment protocols, acoustic isolation, and phased scheduling, attributes less relevant in greenfield assemblies but pivotal in retrofit jobs. Material-recovery schemes, where contractors salvage and upcycle fit-out elements, create additional revenue streams and align with Gulf sustainability agendas. Growing preference for flexible layouts in co-working hubs and hybrid offices encourages interior designers to specify demountable partitions and plug-and-play furniture systems, sustaining after-market modification contracts. Taken together, the GCC interior design market benefits from a dual-engine model in which renovations yield recurring cash flows while marquee new-builds amplify prestige credentials.

By Price Tier: Premium-Luxury Surge Reflects Wealth Migration

The mid-range and economy brackets collectively contributed 45.88% to 2025 turnover, propelled by standardized interiors for affordable housing and institutional projects that require tight cost control without sacrificing durability. Yet premium and luxury interiors are forecast to expand at an 10.85% CAGR through 2031, handily outperforming the overall GCC interior design market. Ultra-prime schemes such as Waldorf Astoria Residences and Raffles Trojena validate how luxury operators integrate interior design at the concept stage, ensuring bespoke millwork, art integration, and smart-glass facades are intrinsic rather than add-on features. High-net-worth inflows to Dubai, Abu Dhabi, and Doha elevate the appetite for branded residences where unit prices exceed USD 3 million, enabling interior consultants to charge premium design-management fees and orchestrate cross-border sourcing of rare materials.

Economy-tier interiors, while less glamorous, represent critical volume that stabilizes factory-line joinery suppliers and feeds ancillary segments such as low-cost furnishings and lighting. Governments stipulate locally sensitive aesthetics even in mass-market schemes, encouraging designers to incorporate regional motifs using cost-effective laminates or digitally printed wall panels. Mid-range offices that cater to SMEs in free zones require ergonomic, technology-ready layouts delivered under compressed budgets, fostering innovation in modular fit-out packages. Meanwhile, luxury developers embrace ESG as a prestige differentiator; Forbes International Tower’s ILFI Zero-Carbon certification converts sustainable materials into a status symbol, compelling interior teams to master advanced material-passport documentation. Consequently, the GCC interior design market enjoys a barbell structure where both cost-efficient standardization and high-margin bespoke deliveries coexist and cross-pollinate best practices.

Geography Analysis

Saudi Arabia, holding 39.05% of the GCC interior design market revenues in 2025, is the epicenter of the GCC interior design market and benefits from an estimated USD 850 billion project pipeline anchored by Vision 2030 flagships like NEOM, Diriyah, and the Mukaab. The Saudi Architecture Characters Map program alone targets an SAR 8 billion (USD 2.13 billion) GDP contribution by 2030 through heritage-driven design mandates, creating recurring opportunities for firms versed in Islamic geometric and Najdi motifs. ROSHN Group’s SAR 350 billion (USD 93 billion) spend across integrated communities underlines residential scale, while the Kingdom’s push toward 100% renewable-powered luxury enclaves elevates demand for eco-intelligent interiors.

Qatar and the UAE jointly represent the fastest-growing geographies with a projected 9.51% CAGR through 2031, each pursuing complementary yet distinct trajectory drivers. Qatar capitalizes on post-World-Cup legacy assets and heavy cultural investments such as Lusail’s Art Mill Museum, galvanizing museum-grade interior design requirements and furnishing Doha with a cultural gravity that pulls regional talent. The UAE’s pipeline is hospitality-centric; Dubai Exhibition Centre’s expansion to 180,000 sqm and Abu Dhabi’s projected 39.9 million annual visitors by 2030 demand elevated guest experiences, pushing supply chains toward high-spec FF&E programs.

Kuwait, Oman and Bahrain represent high-potential niches where interior firms can tailor specialized offers. Kuwait’s Vision 2035 smart-city agenda supports tech-infused interiors that accommodate advanced AV and IoT devices, while its H2 2024 real-estate macro index score of 3.5 reflects a stable launchpad for new residential fitouts. Oman’s tender for 12 new schools’ signals education as a growing pipeline and underscores the need for acoustically optimized durable classroom interiors. Bahrain pioneers’ wellness-centric healthcare design at King Hamad American Mission Hospital, opening an avenue for designers proficient in biophilic and therapeutic environments. Collectively, these secondary markets offer comparatively less competition and higher margin potential for first movers, thereby enriching the GCC interior design market landscape.

Regulatory Landscape

Interior design services in the GCC operate within building, fire-life-safety, and occupational safety frameworks that govern interior materials, egress, and site practices. In the UAE, the UAE Fire and Life Safety Code and emirate-level building codes shape requirements for partitions, finishes, and interior fit-out execution, while Abu Dhabi projects commonly align with OSHAD for workplace safety controls relevant to fit-out and renovation activities. In Saudi Arabia, the Saudi Building Code provides baseline compliance thresholds that influence specification, approvals, and inspection workflows for interior works.

Sustainability compliance is increasingly codified through regional and national programs that influence interior material selection and documentation. GSAS adoption as Gulf Standard GSO 3000:2025 formalizes sustainable building requirements across parts of the region, and the GCC Green Building Certification Center issued an inaugural Green Building Materials Whitelist on March 31, 2026, supporting more consistent screening of sustainable materials used in interiors. These shifts elevate compliance-led specification, product submittal management, and traceability needs for LEED/GSAS-aligned projects, particularly in hospitality and Grade-A commercial developments.

Value Chain Analysis

The GCC interior design services value chain typically begins with client briefing, concept design, and space planning, then moves into detailed design development (drawings, BIM deliverables, specifications, and bill of quantities) and coordination with MEP and structural stakeholders. From there, procurement and FF&E selection follow, with firms relying on strategic sourcing, trade discounts, and controlled scope definition (often through moodboards and alternates) to protect margins amid imported-material volatility. Execution includes tendering and contractor appointment, fit-out delivery (joinery, finishes, lighting, and furniture installation), commissioning and snagging, and then handover with as-built documentation.

Large projects increasingly use design-build and other integrated delivery frameworks that consolidate design coordination and procurement under single-point responsibility, tightening the interface between designers, contractors, and suppliers. Differentiation for leading consultancies comes through BIM and immersive-technology integration (including VR walk-throughs and digital coordination), compliance navigation across varying GCC codes, and talent management for specialized trades and project controls. After-handover services such as maintenance support and renovation cycle planning feed recurring demand, which supports the market structure where renovation and remodeling represents a large share of activity.

Competitive Landscape

The GCC interior design market exhibits a fragmented structure, with most established players having less than three decades of operational history in the region. Local and regional players dominate the market landscape, with Dubai serving as a primary hub for many leading firms. The market is characterized by the presence of both specialized interior design studios and larger conglomerates offering integrated design and fit-out services. Many firms have developed strong regional networks and established their presence across multiple GCC countries, though their primary operations remain concentrated in their home markets. The competitive dynamics are shaped by firms' ability to understand local design preferences while incorporating international trends and standards.

The market shows limited consolidation activity, with most growth happening through organic expansion rather than mergers and acquisitions. Companies are primarily focused on building their individual brand identities and service capabilities rather than pursuing aggressive acquisition strategies. The competitive landscape is further characterized by the presence of numerous boutique design firms catering to specific market segments or client preferences. The industry structure allows for considerable market entry opportunities, though establishing a strong reputation and securing high-profile projects remains challenging for newer entrants.

For new entrants and growing firms, focusing on niche markets or specialized design services can provide opportunities for market penetration. The ability to offer unique design solutions while maintaining cost competitiveness is crucial for gaining market share. Companies need to carefully navigate regulatory requirements across different GCC countries while building strong local networks and partnerships. The risk of substitution remains relatively low due to the specialized nature of professional interior design services, though firms must continuously evolve their service offerings to maintain relevance. Building strong client relationships and establishing a reputation for reliable project delivery are essential factors for long-term success in this market. Additionally, firms offering interior consultancy and interior remodeling services are finding new avenues for growth by addressing specific client needs.

GCC Interior Design Industry Leaders

Depa

KEO International Consultants

Atkins

Gensler

Dewan Architects + Engineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Net-zero-ready and code-compliant retrofit and fit-out packages remain a clear whitespace across offices, hospitality, and mixed-use assets as owners align interior specifications with green-building requirements and material traceability. Evidence of active demand shows up in the pace of regulatory and standards work, including GSAS as Gulf Standard GSO 3000:2025 and the March 31, 2026 Green Building Materials Whitelist issued by the GCC Green Building Certification Center. This direction pushes projects toward documented low-VOC finishes, compliant fire-rated assemblies, and sustainability-aligned procurement. Firms that can package BIM-enabled coordination, compliant material submittals, and lifecycle documentation tend to gain traction in renovation-heavy portfolios where speed-to-reopen is commercially important.

Two additional opportunity pockets are visible around Grade-A workplace programs and large-format destination projects. In Riyadh, Grade-A office occupancy was cited at 98% as of June 2026, supporting higher-value workplace design programs focused on user experience, flexibility, and technology integration rather than commodity fit-outs. In the UAE, the Sphere Abu Dhabi project on Yas Island (with AtkinsRealis and ALEC named for lead design and delivery roles in 2026, and an opening timeline communicated for 2029) points to demand for integrated design, immersive technology, and complex interior delivery capabilities beyond conventional commercial interiors. Together, these signals point to growth in multidisciplinary scopes spanning interior architecture, digital experience design, specialist finishes, and coordinated procurement across long-lead items.

Recent Industry Developments

- July 2026: AtkinsRealis joined forces with ALEC Engineering and Contracting LLC as lead design and supervision consultant for the Sphere Abu Dhabi project on Yas Island. The collaboration expands multidisciplinary design and interior-delivery footprint in GCC mega-projects.

- July 2026: AtkinsRealis secured a major contract from the Royal Commission for Riyadh City (RCRC) for engineering and supervision services on the Riyadh Metro network and road infrastructure. The contract underscores sustained GCC megaproject activity with integrated design-delivery opportunities for interiors players.

- June 2026: AtkinsRealis appointed by ORA Developers to deliver master planning, infrastructure, and public realm design services for BAYN, a waterfront community in Ghantoot, UAE. The project highlights expansion of interior-design-adjacent services into urban-scale developments and Gulf waterfront communities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid interior design services delivered for residential and commercial spaces across GCC countries, starting from concept and space planning through detailed design and project coordination that supports a finished interior.

Scope exclusions: Excludes pure construction contracting and MEP engineering work when they are sold as standalone services without an interior design engagement.

Segmentation Overview

- By End-User

- Residential

- Commercial

- By Service Type

- New Construction

- Renovation / Remodeling

- By Price Tier

- Economy

- Mid Range

- Premium / Luxury

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public building blocks that explain demand and activity levels in the GCC built environment. We relied on sources such as national statistics offices in GCC countries, central bank and government budget publications, municipal building permit dashboards where available, and customs and trade statistics for major interior-related material flows.

To keep the numbers tied to what firms can actually deliver, we also reviewed company annual reports and investor presentations for design-led groups, plus project announcements, tender portals, and reputable regional press coverage. Where needed, we used paid subscriptions for company financials and intelligence, and for contract and tender tracking, so revenue ranges and project pipelines could be sense-checked. The desk sources named here are illustrative, and other public references were also used for data collection, validation, and clarifying assumptions.

Primary Interviews and Surveys

Primary work focused on cross-checking service scope, typical fee structures, and how design work converts into billed revenue across new build and renovation activity. We spoke with design firms, fit-out ecosystem participants, and buyer-side stakeholders such as developers and facility operators across the GCC, so the demand picture stayed realistic by country and by end-use. Respondent input was used to tighten utilization assumptions, project size distributions, and near-term pipeline risk before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | |

| Mid tier: 49% | Functional/Unit leaders: 29% | |

| Smaller Players: 18% | Managers: 54% |

Market-Sizing & Forecasting

The sizing model used a top-down and bottom-up approach, where construction and renovation spending indicators in GCC countries were first converted into an addressable interior design services demand pool. We corroborated totals using selective bottom-up checks, including sampled project fee ranges by building type and an output-based view of what an average design team can bill in a year. If gaps appeared, we handled them by using conservative midpoints until they were validated in follow-up calls.

A few practical inputs shaped the model, including the new construction versus renovation mix, hospitality and retail project starts, premium versus mid-range fit-out intensity, average design fee as a share of project value, and delivery lead times that shift revenue recognition across years. For forecasting, we leaned on scenario analysis supported by country-level project pipeline views and expert expectations on how fast major programs and private developments convert into awarded and executed work. When the forecast was extended, we kept assumptions consistent with visible project backlogs and macro signals, then adjusted for likely normalization in pricing and capacity utilization.

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals, including large project award activity, developer capex commentary, and the implied revenue capacity of the active supplier base. Outliers were flagged and reworked, then the full file was reviewed by a second analyst so country splits, growth rates, and fee assumptions stayed internally consistent.

The report is refreshed annually, with interim updates when material events change demand or pricing, such as major project reprioritization or new regulation affecting construction activity. Before delivery, we do a final pass on recent news and macro releases, and any meaningful variance triggers a quick re-contact with sources to confirm the direction and magnitude.

Mordor Intelligence's Gcc Interior Design Services Market Size Versus Other Published Estimates

Published values for GCC interior design services can differ even when they sound like the same market, because the service boundary is not always kept consistent and the base year may shift. Differences also come from how firms treat renovation cycles, price tier weighting, and the timing used for currency conversion when local contracts are billed over long periods.

Fit-out contracting revenues are often blended into the headline number in some publications, but that activity sits outside Mordor Intelligence's scope for this study when it is not tied to an interior design services engagement, which can pull totals upward. Gaps also show up when a forecast assumes aggressive mega-project conversion without validating award-to-execution slippage, or when fee-rate progressions are applied evenly across countries despite different procurement patterns and cost inflation paths.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.76 B (2025) | |

| Global Consultancy A | USD 13.41 B (2024) | Uses a different base year and can blend broader delivery work into services, which shifts the addressable pool and changes how project value converts into design fees. |

| Industry Data Platform B | USD 12.26 B (2024) | Leans on a shorter forecast window and may include adjacent fit-out activity and event-related interiors in places, which can compress the pure design-only definition and change the implied service take-rate. |

The spread across the table is mainly explained by what is counted as a service and when the base year is set, and both points matter in a project-led market. By keeping the demand pool tied to observable construction and renovation signals, and then checking fee and capacity assumptions through interviews, our estimate stays easier to trace and repeat when clients update scenarios.

Key Questions Answered in the Report

How large is the GCC interior design market in 2026?

The GCC interior design market size stands at USD 14.79 billion in 2026 and is forecast to reach USD 21.18 billion by 2031.

What is the projected growth rate for interior design services across the Gulf?

The market is expected to post a 7.46% CAGR from 2026-2031, aided by Vision 2030 mega-projects and a booming hospitality pipeline.

Which end-user segment is expanding the fastest?

Commercial interiors, encompassing office, retail and hospitality spaces, are projected to grow at 9.05% CAGR through 2031.

Which price tier offers the highest growth opportunity?

Premium and luxury interiors show the strongest upside with an 10.85% CAGR, fueled by high-net-worth migration and branded residences.

How does renovation compare with new construction in revenue terms?

Renovation and remodeling commands 50.88% of current revenue and slightly outpaces new-build growth due to asset-refresh cycles and sustainability retrofits.

Page last updated on: