Recruiting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

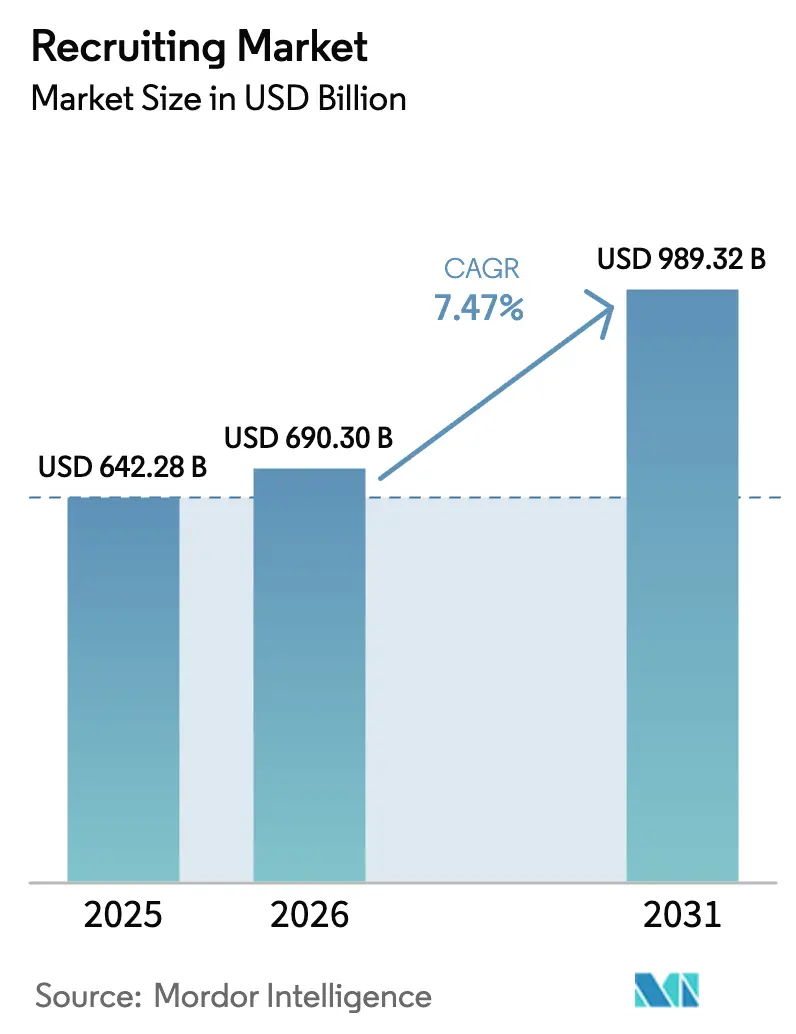

| Market Size (2026) | USD 690.3 Billion |

| Market Size (2031) | USD 989.32 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

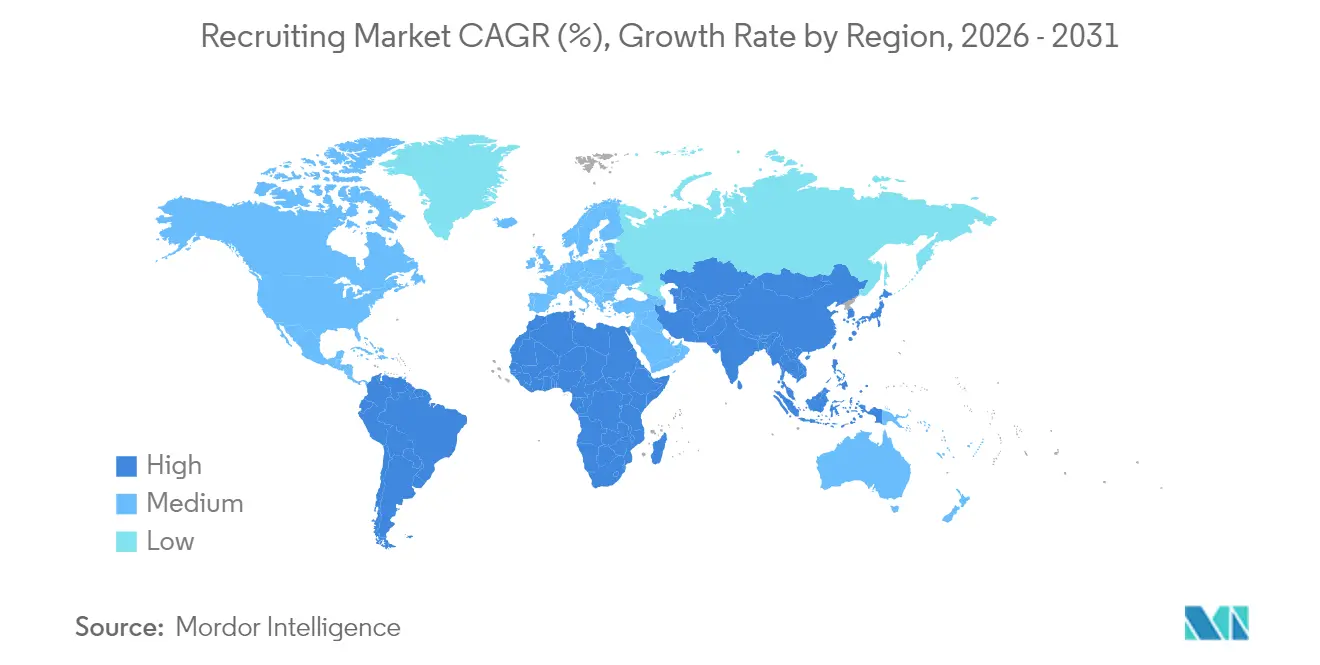

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

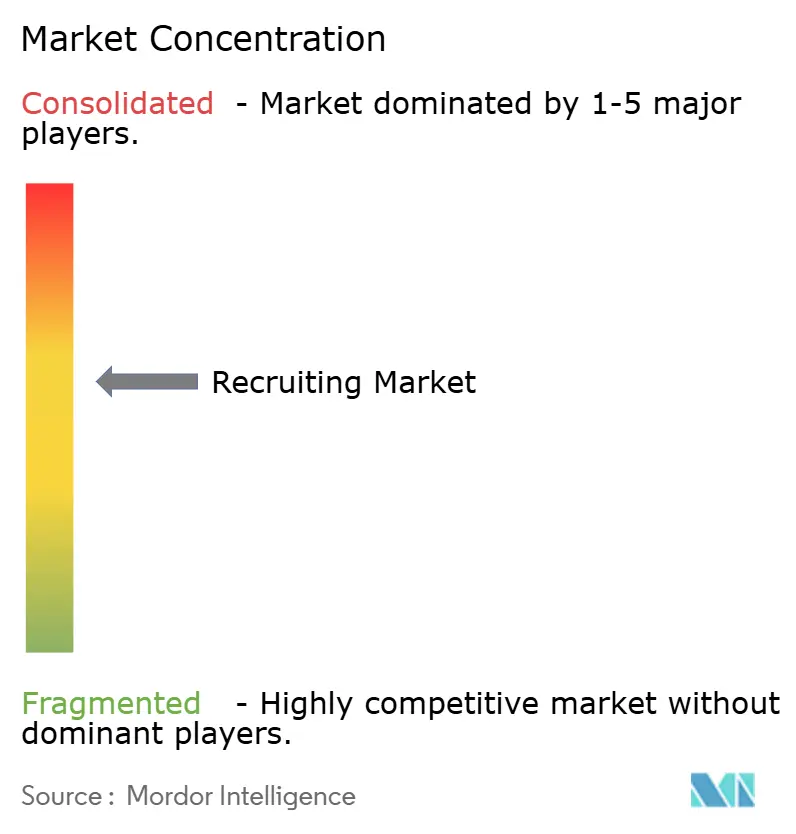

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recruiting Market Analysis by Mordor Intelligence

The recruiting market size is expected to grow from USD 642.28 billion in 2025 to USD 690.3 billion in 2026 and is forecast to reach USD 989.32 billion by 2031 at 7.47% CAGR over 2026-2031. The headline figures underscore how strongly talent-acquisition spend rebounds once employers regain budget confidence after cyclical dips, especially when labor shortages threaten project delivery and revenue targets. Demand is now anchored in three structural forces: pervasive AI adoption that automates sourcing and screening, the gig-economy shift that normalizes contingent staffing, and the mainstreaming of skills-based hiring that broadens candidate pools beyond traditional credentials. Each force amplifies the others: AI lets staffing firms parse vast freelance databases in seconds, while skills taxonomies standardize how platforms match short-term experts to client needs, thereby compressing time-to-hire from weeks to hours. Because labor scarcity persists in software, cybersecurity, and advanced manufacturing, even temporary macroeconomic slowdowns only delay—not destroy—recruitment demand, prompting vendors to invest in predictive analytics that identify early demand signals.

Key Report Takeaways

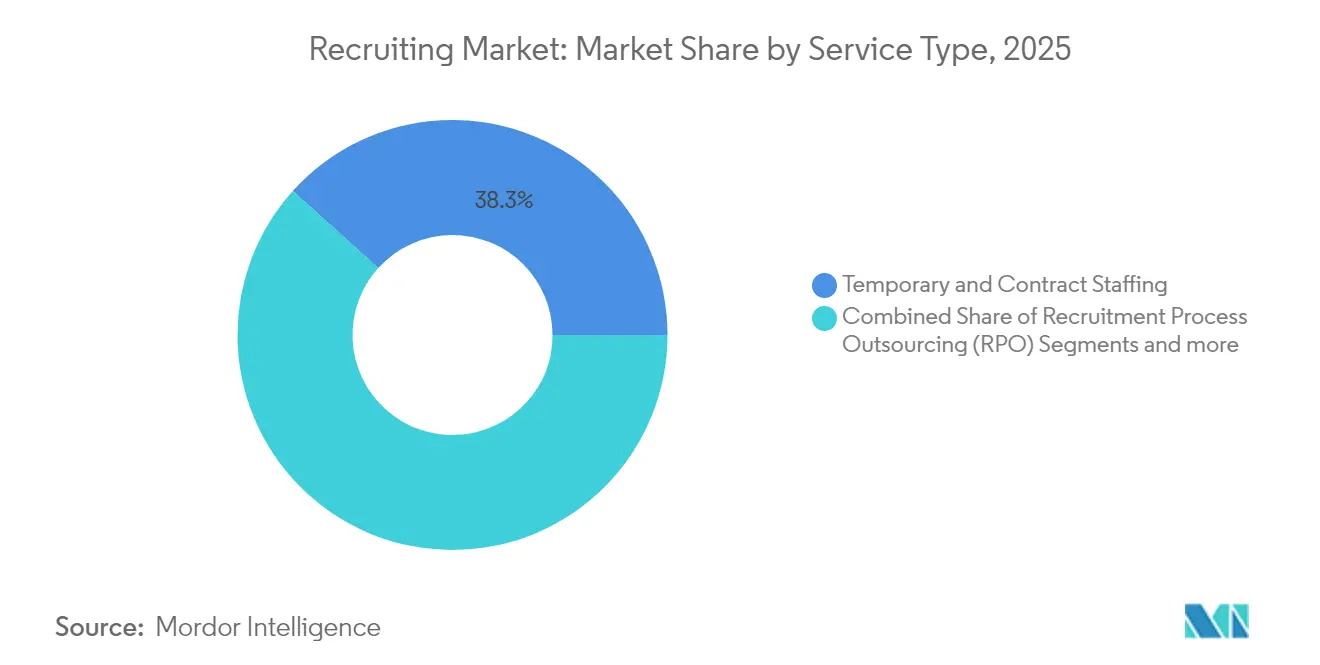

- By service type, temporary and contract staffing led with 38.32% of recruiting market share in 2025, whereas recruitment process outsourcing is projected to climb at a 9.23% CAGR through 2031.

- By recruitment channel, online platforms and job boards accounted for 40.76% of the recruiting market size in 2025; hybrid and managed service providers are poised for the fastest 10.05% CAGR to 2031.

- By client size, large enterprises held 46.02% share of the recruiting market in 2025, while small and medium-sized enterprises represent the quickest-growing segment at an 8.49% CAGR.

- By industry vertical, IT and telecom captured 29.15% of the recruiting market share in 2025; healthcare and life sciences are forecast to expand at a 9.04% CAGR between 2026-2031.

- By geography, North America commanded 36.55% of the recruiting market in 2025, yet Asia-Pacific leads growth with an 8.12% CAGR expected over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recruiting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation and AI-driven tools | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Gig-economy expansion | +1.5% | Global, highest in Asia-Pacific and North America | Long term (≥4 years) |

| Persistent talent shortages | +1.2% | Global, most acute in developed economies | Long term (≥4 years) |

| Skills-based hiring frameworks | +0.9% | North America and the EU, spreading to Asia-Pacific | Medium term (2-4 years) |

| Employer-of-record uptake in emerging markets | +0.7% | Asia-Pacific core; spill-over to the Middle East and Latin America. | Short term (≤2 years) |

| Blockchain credential verification | +0.4% | Early adoption in North America and the EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and AI-Driven Recruitment Tools Adoption

More than half of enterprises worldwide now embed AI somewhere in their hiring workflows, a milestone that quietly shifts the sector’s center of gravity from manual résumé screening to data-driven decision engines. Early adopters report time-to-hire reductions of nearly half and simultaneously widen candidate reach, because algorithms scrape passive-talent forums, alumni networks, and freelance exchanges that recruiters once ignored for lack of bandwidth. Productivity gains amplify over time: every requisition teaches the model to rank future applicants more precisely, creating feedback loops that compound accuracy advantages. In parallel, AI-augmented video interviewing analyzes vocal sentiment and body language to flag potential biases and prompt interviewers with follow-up probes, enhancing fairness and compliance [1]Aneel Bhusri, “Reinventing Hiring for the AI Era,” workday.com . The fusion of AI with applicant-tracking systems produces sticky ecosystems because data portability hurdles deter clients from switching vendors, thereby raising competitive barriers. Vendors that marry AI innovation with robust governance frameworks will capture disproportionate wallet share as regulators scrutinize algorithmic transparency.

Gig-Economy Expansion Increasing Contingent Staffing Demand

Corporate workforce strategies have evolved from binary full-time versus temporary thinking toward elastic talent architectures that blend permanent cores with project-based specialists accessible on demand. Remote-work normalization accelerated this evolution because geographic boundaries no longer constrain where clients source expertise, and platforms now mediate payments, compliance, and language localization at scale. Flexible engagement terms appeal to finance leaders seeking variable-cost models that mirror revenue volatility, while knowledge workers appreciate autonomy and premium rates. As marketplaces mature, they transition from commodity job listings to curated communities where ratings, verified credentials, and outcome histories de-risk hiring decisions for employers. Staffing firms that once competed on Rolodex depth must now compete on API integrations, platform analytics, and speed of matching, which pushes traditional agencies to adopt SaaS front ends or partner with digital natives. Over time, contingent staffing’s share of the recruiting market could climb further because companies facing digital-transformation roadmaps increasingly favour specialized gig talent over long onboarding cycles.

Persistent Global Talent Shortages

Forecast scenarios show an 85.2 million developer deficit by 2030, and similar gaps loom in cybersecurity, advanced analytics, and semiconductor engineering, forcing employers to bid aggressively for scarce skills [2]Grid Dynamics, “Global Developer Shortage: Quantifying the Gap,” griddynamics.com . Wage inflation, however, is only one manifestation of scarcity; companies also amplify non-cash incentives such as remote-first policies, continuous-learning budgets, and social-impact commitments to stand out. Recruitment agencies respond by establishing verticalized practice groups—AI/ML, biotech, clean energy—staffed with subject-matter experts who speak the candidate’s technical language and can vet competency beyond résumé keywords. To widen supply, providers finance bootcamps, scholarship programs, and return-to-work pathways that convert career-break professionals into qualified candidates, effectively expanding their own inventory. International hiring, facilitated by employer-of-record services, further eases chokepoints by allowing companies to tap talent in secondary markets where supply exceeds local demand. Until education systems scale output of high-demand skills, the recruiting market should enjoy structural tailwinds rooted in chronic shortages.

Skills-Based Hiring Frameworks: Accelerating Competency-Matching Platforms

Skills-based hiring reframes talent evaluation around demonstrable capabilities instead of pedigree, thereby opening doors for self-taught coders, bootcamp graduates, and career switchers who were previously filtered out by degree requirements. Leading organizations deploying competency rubrics observe faster ramp-up times because new hires already demonstrate proficiency in role-critical tasks, reducing costly onboarding. Data also show stronger retention when candidates understand job expectations through objective skill matrices rather than vague role descriptions. AI-driven platforms parse job taxonomies, assign weightings to key competencies, and score applicants via coding challenges, work-sample projects, or scenario assessments, producing match rankings that outperform keyword-based résumé parsing. Staffing firms commercialize this capability by offering white-label assessments and bias-audited scoring algorithms to clients lacking internal analytics resources. As governments emphasize inclusive growth, skills-based frameworks align with public policy goals, garnering support that should entrench the approach long term.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic slowdowns | -1.4% | Global, deepest in developed markets | Short term (≤2 years) |

| Growing in-house talent-acquisition teams | -0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising data-privacy compliance costs | -0.6% | EU leading; North America and Asia-Pacific catching up | Long term (≥4 years) |

| Liability risks from algorithmic bias | -0.4% | North America and the EU focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Slowdowns Curbing Hiring Budgets

When GDP growth decelerates, finance chiefs prime cost-containment levers, and discretionary external-recruiting spend is often among the first to be trimmed. Yet demand for niche specialists remains comparatively resilient, because projects tied to risk mitigation, digital transformation, or regulatory mandates continue even in downturns. Internal mobility surges as a hedge: talent-management teams redeploy employees whose roles sunset, thereby saving severance payouts and onboarding costs. Recruitment agencies that pivot to advisory services—workforce planning, skills audits, redeployment frameworks—position themselves as cost-avoidance partners rather than pure expense. Once leading indicators such as job-posting volumes and purchasing-manager indices turn positive, hiring budgets rebound quickly, rewarding firms that maintained talent pipelines through the trough.

Intensifying Competition from In-House Teams

Corporations with large hiring volumes increasingly build internal recruitment centers of excellence, licensing best-in-class ATS platforms and poaching agency consultants to run them. The wave of tech-sector layoffs in 2024 released thousands of seasoned recruiters into the labor market, giving non-tech employers a unique opportunity to insource expertise at attractive compensation levels. Transactional requisitions—such as call-center hires or back-office clerks—are most vulnerable to internalization because process workflows are standardized and easily automated. External partners, therefore, double down on high-complexity searches, executive mandates, and surge hiring where speed and niche networks justify fees. Some agencies counter by offering embedded-recruiter programs, placing consultants on-site while retaining them on the agency payroll, thus blending internal control with external scale. Hybrid models blur boundaries but ensure agencies remain integral to talent strategies even as corporate functions mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology-Enabled Outsourcing Gains Momentum

Temporary and contract staffing generated the largest portion of the recruiting market in 2025, testament to employers’ preference for operational flexibility when forecasting uncertainty remains elevated. Despite its scale, growth moderates relative to recruitment process outsourcing (RPO), which is projected to expand at a 9.23% CAGR because clients seek turnkey models that bundle sourcing, screening, and onboarding into outcome-based contracts. RPO vendors leverage AI pipelines, offshore delivery centers, and fixed-price agreements that promise both cost visibility and faster fill rates, sometimes slashing recruiting expenses by 70% after process re-engineering . Because RPO relationships often span three to five years, providers gain annuity-like revenue streams that fund continuous technology investment, further differentiating them from traditional placement competitors. Compliance burdens, especially around data privacy and algorithmic transparency, are increasingly baked into RPO statements of work, giving established providers with robust legal frameworks a defensible barrier. Consequently, the recruiting market size attached to comprehensive outsourcing models will likely outpace legacy staffing formats as clients elevate recruitment from transactional necessity to strategic cornerstone.

The widening gap between transactional staffing and strategic RPO mirrors a broader shift in HR priorities from cost containment to value creation. Clients measure RPO success not just by vacancy fill time but by candidate quality, retention at 12 months, and diversity benchmarks, pushing vendors to integrate sophisticated assessment science and continuous-learning content into the solution. AI-driven talent intelligence dashboards let HR leaders forecast skills gaps years in advance, inviting RPO partners to design proactive sourcing campaigns rather than react to short-term requisitions. Vendors embedding such predictive analytics into service-level agreements differentiate on insight, not merely price, making it harder for low-cost entrants to win on rate cards alone. As RPO adoption deepens across mid-market companies seeking enterprise-grade capabilities, temporary staffing firms face strategic crossroads: invest in technology and consultative talent analytics or risk revenue erosion. The winners will be those who reinvest margin gains from automation into upskilling recruiters who can interpret data and advise executives on workforce architecture.

By Recruitment Channel: Blended Delivery Models Dominate

Digital platforms captured the largest 40.76% slice of the recruiting market because self-service job postings and automated résumé parsing align with modern candidate behaviour, where applications are often submitted via mobile within minutes of listing. Network effects reinforce platform dominance: each additional employer attracts more talent, and each additional résumé refines search algorithms, boosting relevance and engagement rates. Yet the fastest 10.05% CAGR belongs to hybrid and managed service providers (MSPs) that integrate digital reach with human judgment, reflecting employers’ appetite for scale without sacrificing cultural fit. These providers run omnichannel campaigns—programmatic ads, targeted social outreach, talent-community nurturing—and then layer consultant expertise to curate shortlists and coach hiring teams. Analytics dashboards visualize funnel conversion at each stage, enabling data-driven tweaks that lift offer-acceptance rates and reduce reneges. As employers confront DEI commitments, hybrid partners deploy bias-audited AI that ranks competencies blind to demographic variables, while consultants ensure hiring panels interpret data responsibly.

MSPs also centralize vendor management, aggregating dozens of niche agencies under one governance framework that standardizes rate cards, compliance, and performance metrics. This orchestration yields economies of scale similar to procurement BPO arrangements, freeing HR leaders to focus on strategic initiatives. Pure-play job boards, recognizing the limits of self-service models, now launch talent-matching subscriptions, virtual career fairs, and AI interview coaches to capture value upstream in the hiring cycle. Conversely, traditional agencies integrate chatbots, scheduling automation, and candidate relationship management tools to defend against digital disruption, illustrating how channel boundaries blur. Over time, clients may not distinguish between platform and agency; instead, they will judge partners by their ability to deliver qualified hires at the right cost, speed, and compliance standard. The recruiting market therefore converges toward blended delivery, with differentiation anchored in analytics sophistication, sector expertise, and candidate experience quality.

By Client Size: SMEs Unlock Enterprise-Grade Capabilities

Large enterprises commanded 46.02% of recruiting market revenue in 2025, leveraging buying power to negotiate multi-country MSP contracts that bundle volume discounts with advanced analytics, compliance coverage, and on-site recruiter pods. Their scale demands robust governance, multilingual candidate care, and real-time dashboards that feed executive scorecards, which only a handful of global providers can deliver. Mid-market organizations often serve as innovation test beds, piloting technology features such as AI-augmented sourcing or blockchain credentials before those tools roll out enterprise-wide. Small and medium-sized enterprises, however, represent the swiftest 8.49% CAGR segment because cloud-based SaaS platforms democratize recruiting functionality previously unaffordable outside Fortune 500 budgets. Subscription tiers scale with headcount, letting a 150-person fintech access automated job-posting distribution, programmatic advertising, and offer-letter e-signatures for a fraction of historic costs.

SMEs also rely on employer-of-record services to circumvent the legal and tax complexities of hiring abroad, enabling global expansion from day one. Because internal HR teams are lean, owners value consultative input on salary benchmarking, equity structuring, and employment-brand storytelling—areas where external agencies offer turnkey expertise. Vendors respond with modular service menus: sourcing-only packages, interview-panel training, or fractional recruiter engagements that flex up during funding rounds and down afterward. As these smaller clients mature, they often evolve into mid-market accounts, creating lifetime-value upside for agencies that onboard them early. Consequently, serving SMEs is not merely a volume play but a strategic investment in future enterprise pipelines, cementing their role in the broader recruiting market.

By Industry Vertical: Healthcare Surges on Demographic Tailwinds

IT and telecom maintained a 29.15% recruiting market share in 2025 as every sector digitizes, requiring full-stack developers, cloud architects, and security analysts at scale. Tech recruiters with deep community ties to Github, Stack Overflow, and hackathon circuits remain indispensable because passive talent rarely browses generic job boards. Meanwhile, healthcare and life sciences race ahead with a 9.04% CAGR through 2031, propelled by aging populations, post-pandemic capacity expansion, and a pipeline of novel therapies that intensify clinical-trial staffing needs. Credential verification, shift scheduling, and license tracking add compliance layers that generalist agencies struggle to navigate, making specialized healthcare staffing firms valuable partners. Telehealth adoption further diversifies demand, requiring hybrid skillsets that blend clinical knowledge with digital fluency, which few internal HR teams can source efficiently.

Banking, financial services, and insurance confront digitization and regulatory mandates such as Basel III and IFRS 17, driving demand for risk analysts, reg-tech developers, and model-validation specialists. Manufacturing and industrial sectors benefit from reshoring and Industry 4.0 investments, which create vacancies in robotics maintenance and advanced metrology. Energy transition projects generate new hiring spikes for renewable engineers, grid-integration planners, and carbon-accounting auditors. Agencies that structure vertical practice groups with tailored assessment batteries, salary-intel databases, and compliance playbooks will outperform peers reliant on horizontal service models. Sector specialization thus remains a critical lens through which recruiting market participants secure differentiation and margin resilience.

Geography Analysis

North America led the recruiting market with a 36.55% share in 2025, buoyed by the United States’ tight labor conditions, vibrant start-up ecosystem, and early AI-tool adoption that accelerates sourcing scalability. Venture-capital funding has flowed into HR tech, spawning innovations ranging from conversational bots that prescreen candidates to blockchain wallets that store portable credentials. Canadian employers capitalize on immigration-friendly policies that funnel STEM graduates into the workforce, yet they lean on agencies for credential recognition, relocation logistics, and bilingual onboarding to ensure smooth integration. Mexico’s nearshoring boom drives demand for bilingual production managers and supply-chain planners able to coordinate with US headquarters, creating cross-border recruiting assignments that reward firms fluent in both regulatory regimes. Compliance expertise—covering I-9 verification, H-1B visa processing, and emerging pay-transparency rules—acts as a differentiation lever for providers working in this region. Consequently, North America remains the epicenter of both revenue and innovation within the recruiting market.

Asia-Pacific posts an 8.12% CAGR that eclipses all other regions, driven by double-digit vacancy growth in India’s global capability centers and Japan’s structural worker shortages that spur proactive mid-career reskilling programs. Employers increasingly adopt employer-of-record models to hire software engineers in tier-2 Indian cities or data analysts in Vietnam without establishing subsidiaries, expanding the addressable talent pool. China’s recovery in manufacturing and e-commerce promotes multilingual recruiter demand capable of navigating evolving labor regulations and data-localization requirements. Singapore and Australia serve as regional hubs for fintech and cybersecurity, attracting expatriate expertise but also tightening scrutiny on fair hiring and DEI compliance, which raises the bar for agency governance. As generative AI adoption accelerates, demand for prompt engineers and AI ethics specialists surges, providing new revenue streams for forward-thinking recruiters. Taken together, Asia-Pacific’s demographic breadth and economic dynamism guarantee its long-term status as the fastest-growing slice of the recruiting market.

Europe maintains steady, if uneven, momentum; while headline GDP slows, specialized talent demand in renewable energy, semiconductors, and advanced automotive keeps recruitment activity robust. The EU AI Act imposes strict transparency obligations on algorithmic hiring tools, compelling vendors to audit models for bias and document decision logic, thereby elevating compliance as a competitive differentiator. Southern Europe’s rebound—illustrated by 3% growth in Italy and 8% in Spain—reinvigorates hospitality and logistics hiring, while Northern markets focus on green-tech roles tied to offshore wind and hydrogen initiatives. Germany and France anchor continental industrial demand, especially as automakers electrify product lines and require battery-supply-chain expertise. Collectively, Europe’s complex mosaic of languages, labor laws, and data-privacy statutes ensures sustained demand for cross-border recruiting specialists.

Competitive Landscape

The global recruiting market exhibits moderate concentration, with the top five agencies accounting for a significant share of revenue. This balance enables economies of scale while creating opportunities for niche players to disrupt the market. Scale players such as Adecco, Randstad, and ManpowerGroup funnel multi-billion-dollar technology budgets into AI sourcing engines, omnichannel candidate engagement, and predictive workforce analytics that clients cannot easily replicate internally. Mid-tier specialists thrive by targeting high-barrier niches—cybersecurity, clinical research, clean energy—where deep domain expertise outweighs sheer delivery volume. Strategic partnerships with cloud providers, exemplified by Adecco’s collaboration with Salesforce, integrate recruiting data into enterprise workflow platforms, embedding agencies deeper into client operating models. Acquisitions remain a preferred route to capability expansion: TrueBlue buying Healthcare Staffing Professionals added regulated-sector depth, while Monster’s merger with CareerBuilder pooled job-board traffic and advertising tech to fend off platform competitors.

Innovation pressure intensifies as start-ups commercialize blockchain credential wallets, bias-auditing SaaS, and AI interview simulators that challenge incumbents’ value propositions. Yet compliance expectations rise in parallel; corporate customers now demand third-party attestations that recruiting algorithms meet fairness thresholds, that candidate data is encrypted at rest, and that pay-equity analytics accompany offer recommendations. Agencies meeting these standards secure multi-year master service agreements that stabilize revenue cycles. Geographic expansion remains another battleground: Groupe Adéquat’s purchase of Italy’s AxL Group signals appetite for market share in Southern Europe, while US-based GEE Group’s acquisition of Hornet Staffing boosts managed-service provider capacity at Fortune 1000 clients. In sum, competitive advantage resides at the intersection of technology maturity, sector specialization, and regulatory credibility within the recruiting market.

Recruiting Industry Leaders

Adecco Group AG

Randstad NV

ManpowerGroup Inc.

Recruit Holdings Co., Ltd.

Allegis Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Randstad announced plans to extend its Talent Platform to most markets within two years, targeting EUR 2 billion in digital-marketplace revenue and opening specialized talent centers to enhance service delivery.

- March 2025: Adecco Group unveiled an AI-powered workforce-management venture with Salesforce that orchestrates collaboration between human employees and AI agents, reflecting the industry’s pivot toward integrated human-machine staffing models.

- February 2025: Workday and Randstad formalized a partnership that leverages Workday Recruiting Agent, which processed more than 700,000 requisitions in 2024 and boosted recruiting capacity by 54%.

- February 2025: TrueBlue acquired Healthcare Staffing Professionals to accelerate its entry into healthcare recruitment, citing demographic trends that elevate demand for licensed clinicians.

Global Recruiting Market Report Scope

Recruitment involves actively seeking, identifying, and hiring candidates for specific positions. This process encompasses everything from the initial search to the successful integration of the new hire into the company. This report provides a comprehensive analysis of the recruiting market. It explores market dynamics, underscores emerging trends across various segments and regions, and offers insights into various product and application types. Furthermore, the report examines key players and the competitive landscape. The recruiting market is segmented by industry, which includes technology, healthcare, finance, manufacturing, and retail and hospitality; by experience level, including entry-level, mid-level, and senior-level; by employment, including full-time, part-time, and contract/freelance; by demographic including age, education level, and gender and diversity; and by geography including North America, South America, Europe, Asia-pacific, and Middle-East & Africa). The report offers market size and forecasts for the recruiting market in value (USD) for all the above segments.

| Permanent Staffing |

| Temporary & Contract Staffing |

| Recruitment Process Outsourcing (RPO) |

| Executive Search |

| Other Niche Services |

| Offline / Agency-Led |

| Online Platforms & Job Boards |

| Hybrid / Managed Service Providers |

| Small & Medium-sized Enterprises (SMEs) |

| Mid-Sized Enterprises |

| Large Enterprises |

| IT & Telecom |

| Healthcare & Life Sciences |

| Banking, Financial Services & Insurance (BFSI) |

| Manufacturing & Industrial |

| Retail & Consumer Goods |

| Other Verticals |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Permanent Staffing | |

| Temporary & Contract Staffing | ||

| Recruitment Process Outsourcing (RPO) | ||

| Executive Search | ||

| Other Niche Services | ||

| By Recruitment Channel | Offline / Agency-Led | |

| Online Platforms & Job Boards | ||

| Hybrid / Managed Service Providers | ||

| By Client Size | Small & Medium-sized Enterprises (SMEs) | |

| Mid-Sized Enterprises | ||

| Large Enterprises | ||

| By Industry Vertical | IT & Telecom | |

| Healthcare & Life Sciences | ||

| Banking, Financial Services & Insurance (BFSI) | ||

| Manufacturing & Industrial | ||

| Retail & Consumer Goods | ||

| Other Verticals | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global recruiting market in 2026?

The recruiting market stands at USD 690.3 billion in 2026, reflecting strong demand for digital and skills-based hiring solutions.

How fast is the recruiting market expected to grow through 2031?

It is forecast to expand at a 7.47% CAGR, reaching USD 989.32 billion by 2031 as AI tools, gig work and RPO contracts gain traction.

Which recruiting service segment is projected to grow the quickest?

Recruitment process outsourcing (RPO) shows the fastest momentum with a 9.23% CAGR forecast for 2026-2031, outpacing traditional staffing.

What region will see the highest recruiting market growth?

Asia-Pacific is set for the strongest rise, advancing at an 8.12% CAGR on the back of rapid digital-economy expansion and employer-of-record uptake.

Why are skills-based hiring frameworks becoming popular?

They deliver faster ramp-up and better retention by matching candidates on proven competencies rather than academic pedigree, broadening the talent pool for hard-to-fill roles.

How concentrated is the competitive landscape in recruiting?

The top five providers capture a significant share of market revenue, resulting in a moderate concentration score of 6, which underscores opportunities for niche players to strategically position themselves in the market.

Page last updated on: