Photographic Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.21 Billion |

| Market Size (2031) | USD 48.91 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photographic Services Market Analysis by Mordor Intelligence

The photography services market size is expected to grow from USD 37.51 billion in 2025 to USD 39.21 billion in 2026 and is forecast to reach USD 48.91 billion by 2031 at 4.52% CAGR over 2026-2031. Healthy growth reflects steady global demand for compelling visual content, underpinned by rapid adoption of subscription-based platforms, increasing corporate spending on brand storytelling, and a widening technology stack that now includes generative AI for editing and asset creation. Consolidation among leading stock libraries is reshaping competitive dynamics, while professional service providers differentiate through specialization, workflow automation, and environmental credentials. Digital channels, particularly online marketplaces, remain the primary revenue engine, yet physical studios retain relevance for high-touch corporate portraiture and premium print output. Regionally, North America retains scale advantages, but Asia-Pacific’s accelerated corporate digitalization positions the region as the long-term volume driver.

Key Report Takeaways

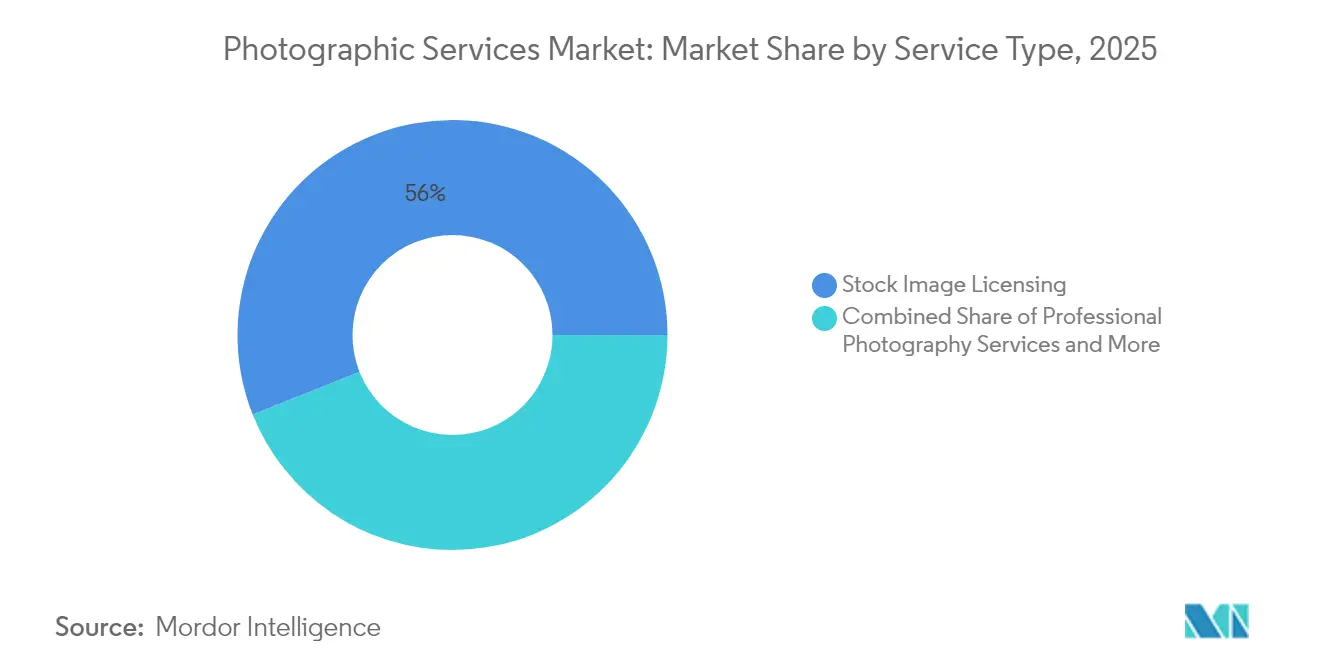

- By service type, Stock Image Licensing led with 56.02% of the photography services market in 2025, while Professional Photography Services is projected to expand at a 6.64% CAGR through 2031.

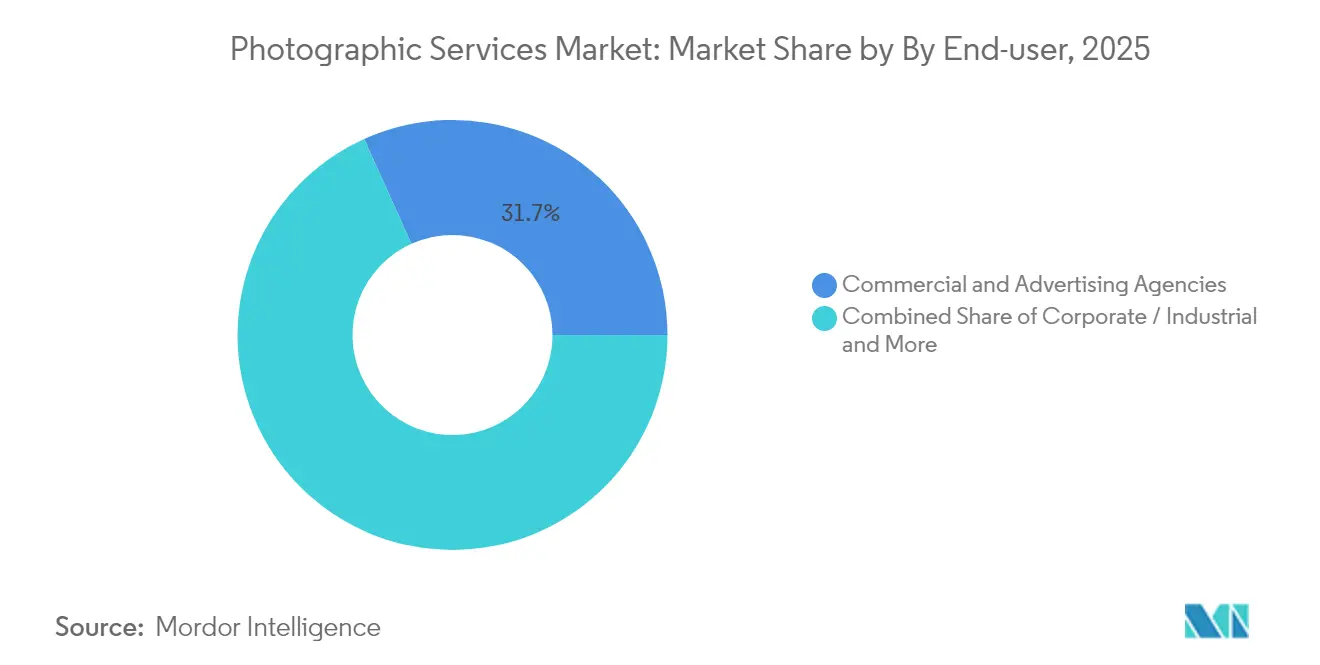

- By end-user, Commercial & Advertising Agencies commanded 31.74% revenue share in 2025; Corporate & Industrial applications are growing fastest at 7.1% CAGR to 2031 in the photography services market.

- By distribution channel, Online Platforms & Marketplaces accounted for 63.67% of the photography services market size in 2025 and are advancing at a 6.47% CAGR.

- By geography, North America contributed 36.18% of revenue in 2025, whereas Asia-Pacific is forecast to grow at 6.19% CAGR through 2031 in the photography services market.

- Top 5 players, such as Getty Images, Shutterstock, Adobe Stock, Alamy, and Shutterfly, hold major market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photographic Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in digital-first brand campaigns | +1.2% | Global, with early gains in North America & Europe | Short term (≤ 2 years) |

| E-commerce boom driving product imagery demand | +1.8% | Global, strongest in Asia-Pacific & North America | Medium term (2-4 years) |

| Smartphone proliferation & pro-grade enhancement add-ons | +0.9% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Expansion of subscription-based stock platforms | +1.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Generative-AI training needs for curated photo datasets | +1.3% | Global, concentrated in tech hubs | Short term (≤ 2 years) |

| NFT & Web3 monetization of photo assets | +0.4% | North America & Europe, selective adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Digital-First Brand Campaigns

Corporate marketing strategies increasingly prioritize visual storytelling across digital channels, creating sustained demand for professional photography services. It allocates 23% more budget to visual content than in 2023, and corporate buyers increasingly commission bespoke photography to differentiate brand narratives[1]Source: Zenfolio, “2024 Photography Industry Report,” zenfolio.com. Custom shoots for product launches, executive portraits, and omnichannel ads have driven many studios to add viewing-appointment workflows that lift average order value by up to 20%. The persistent shift toward always-on content strategies underlies recurring demand that benefits both stock platforms and professional providers across the photography services market.

E-commerce Boom Driving Product Imagery Demand

Online sellers attribute 90% of purchase intent to image quality, prompting retailers to invest in studio-grade hero shots that lift click-through rates well above standard pack images[2]Source: Studio Pod, “E-commerce Image Quality Survey,” studiopod.com. High-volume e-commerce photography has spawned specialized micro-studios optimized for rapid turnaround, and their scaled operations support the broader photography services market as global e-retail grows.

Smartphone Proliferation & Pro-Grade Enhancement Add-ons

Professional photographers embrace smartphone technology, with 13% using mobile devices for half or more of their professional work, while 64% incorporate smartphones into personal photography workflows. Sensor upgrades, AI-enabled lenses and improved computational imaging sharpen output quality, allowing hybrid shoots and expanding the client pool for on-location corporate briefs.

Expansion of Subscription-Based Stock Platforms

Annual Subscription plans deliver 57% of Getty Images’ revenue, validating a model that grants predictable income for contributors and lower marginal cost for buyers. Shutterstock’s Q1 2025 report confirmed 17% content revenue growth on similar plans, cementing the recurring revenue shift that underpins the scaling of the photography services market. This model provides photographers with more stable income while offering customers cost-effective access to extensive image libraries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundance of free UGC compressing price points | -1.4% | Global, particularly social media-driven markets | Short term (≤ 2 years) |

| Complex IP & licensing disputes | -0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Sustainability scrutiny curbing on-location shoots | -0.6% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Verification costs vs. deepfakes & synthetic media | -0.5% | Global, critical in journalism & commercial sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Abundance of Free UGC Compressing Price Points

Smartphones now capture 92.5% of all photos, saturating social platforms with no-cost visuals that reset client expectations[3]Source: Stock Photo Secrets, “Dreamstime Clarifies AI-Generated Image Policy,” stockphotosecrets.com. Professional photographers report declining rates for basic services as clients increasingly accept lower-quality alternatives, forcing specialization toward high-value applications requiring technical expertise and creative vision that cannot be replicated through amateur photography.

Complex IP & Licensing Disputes

The flood of AI-generated art blurs ownership lines, prompting agencies to revise submission guidelines and heightening legal spending for usage vetting. Dreamstime’s selective acceptance of AI imagery illustrates the operational friction small vendors face, and lingering uncertainty restrains market velocity. These disputes create operational uncertainty and increase legal compliance costs, particularly affecting smaller photography service providers lacking resources for comprehensive IP management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Stock Licensing Dominates as Professional Services Accelerate

Stock Image Licensing held 56.02% of the photography services market share in 2025, benefiting from long-established distribution channels and scalable subscription revenue. Demand from marketing teams for quick, cost-effective visuals sustains volume, while large libraries monetize legacy archives through AI data agreements. In value terms, the segment anchors the current photography services market size with recurring revenue streams that stabilize cash flow even during economic soft patches.

Professional Photography Services, although smaller in revenue, grows at a forecast 6.64% CAGR through 2031 on increased corporate demand for unique brand content and technical shoots that free stock cannot supply. Studio investments in automated editing, AI-curated proofing, and live collaboration workflows raise throughput, enabling higher job volume without commensurate labor expansion. The dual-track dynamic, where licensing brings a breadth, and bespoke services deliver depth, underscores the evolving balance inside the photography services market.

By End-User: Corporate Sector Becomes the Prime Growth Engine

Commercial & Advertising Agencies commanded 31.74% of 2025 revenue, leveraging multi-year contracts for campaign assets that require diverse shoot lists and rapid iteration. Agencies prize usage-cleared stock bundles and agile photographers capable of mixed-media deliverables. Even as budgets fragment across channels, agency spending remains the foundation of current photography services market size, sustaining established studios and global stock houses alike.

Corporate & Industrial clients exhibit the fastest expansion, growing at 7.1% CAGR as businesses integrate professional imagery into investor reports, manufacturing documentation, and employer-branding portals. Safety-compliant industrial shoots, factory VR walkthroughs, and executive portraits now often bundle with video components, increasing average project value. Media & Entertainment participants adopt drone rigs for cinematic shots and leverage 3D capture for streaming platforms, while Individual/Consumer demand concentrates in high-emotion events such as weddings, a segment still willing to pay for on-site crews and premium post-production. Together, varied use cases deepen the photography services market penetration across economic sectors.

By Distribution Channel: Digital Platforms Drive Revenue While Offline Studios Refocus

Online Platforms & Marketplaces generated 63.67% of 2025 revenue and are set to expand at a 6.47% CAGR as clients favor frictionless search, subscription access, and instant downloads. The post-merger scale of Getty Images and Shutterstock, with combined revenue nearing USD 2 billion, reinforces network effects through algorithmic discovery and diverse content tiers. Integrated editing APIs embed stock selection into design software, further anchoring customer loyalty within the photography services market.

Offline Studios & Retail Labs now prioritize premium portraiture, large-format archival printing,g and experiential services that digital channels cannot replicate. Sustainability initiatives, such as solar-powered labs and eco-certified substrates, resonate with environmentally conscious clients and provide differentiation. Hybrid storefront-plus-web models offer remote proofing with in-store pickup, maintaining foot traffic while maximizing operational reach. As a result, the balanced channel mix sustains overall photography services market resilience even amid digital predominance.

Geography Analysis

North America benefits from corporate marketing budgets, early subscription adoption, and advanced infrastructure for content distribution. The region's mature client base values indemnified licensing, pushing agencies to premium providers that guarantee rights clarity. At the same time, widespread AI experimentation introduces competitive tension, prompting professional studios to invest in proprietary workflows that protect margins across the photography services market.

Asia-Pacific represents the fastest-growing territory, with a projected 6.19% CAGR through 2031. Rapid digital commerce expansion fuels product imagery demand, while government incentives for creative-industry development spur local studio formation. China drives absolute volume, whereas Japan and South Korea set quality benchmarks, together enriching the regional photography services market.

Europe balances mature consumption with emergent sustainability mandates. EU environmental directives encourage low-carbon print operations and recycling of consumables, nudging service providers toward greener workflows. Equipment supply chains experienced Brexit-related import frictions, pushing European studios to build local maintenance capacity and diversify suppliers. Despite regulatory overhead, the continent's diverse cultural heritage and high art-market activity secure a stable premium segment of the photography services market. In the Middle East & Africa, improving connectivity and smartphone adoption unlock digital distribution, though infrastructure gaps outside major hubs temper near-term scale.

Mordor Intelligence provides coverage of the photographic services market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The January 2025 agreement for Getty Images to acquire Shutterstock for USD 3.7 billion creates a visual-content powerhouse with expected USD 150–200 million in annual cost synergies by year three. Post-deal, the enlarged entity commands unmatched contributor reach, proprietary AI assets and cross-selling potential spanning enterprise, SMB and media verticals, reinforcing high-end dominance in the photography services market.

Beyond stock, competition remains fragmented. Thousands of boutique studios and regional event specialists compete on proximity, niche style and personalized service. Adobe Stock, Alamy and Shutterfly round out the top-five digital libraries, each leveraging distinctive contributor incentives and brand equity. Equipment makers now encroach on services: Nikon’s purchase of cinema-camera firm RED.com positions the company to bundle hardware, support and production expertise for professional clientele. AI developers also partner with content owners—Clarifai integrates Getty assets to power enterprise ML applications—blurring the line between technology vendor and creative supplier.

Strategic alliances center on workflow efficiency. Imagen’s “Edit to Delivery” integration with Pic-Time slashes editing time by up to 96%, freeing photographers to handle greater project volume. Lensrentals’ acquisition of BorrowLenses consolidates rental capacity and broadens geographic coverage for specialist gear. While M&A accelerates among top players, most national markets still feature a long tail of independents, keeping customer choice vibrant and sustaining innovation across the photography services market.

Photographic Services Industry Leaders

Getty Images

Shutterstock

Adobe Stock

Alamy

Shutterfly

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Getty Images agreed to acquire Shutterstock for USD 3.7 billion, targeting USD 150–200 million in cost synergies while maintaining distinct brand identities.

- January 2025: Axcel acquired medium-format camera producer Phase One for USD 230 million, expanding its imaging technology portfolio.

- December 2024: Imagen partnered with Pic-Time to launch an automated “Edit to Delivery” workflow that cuts photographer editing time by up to 96%.

- June 2024: Shutterstock signed a multi-year agreement with Reka to license visual datasets for AI model training.

Global Photographic Services Market Report Scope

Photography is the art or process of producing images by the action of radiant energy, especially light, on a sensitive surface (such as film or an optical sensor). The Photographic Services Market is Segmented By Type Outlook (Shooting Service and After-Sales Service), By Application (Consumer and Commercial), And By Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America). The report offers market size and forecasts for the Photographic Services Market in value (USD billion) for all the above segments.

| Professional Photography Services |

| Stock Image Licensing |

| Photofinishing & Printing |

| Photo Booth & Event Imaging |

| Others (Restoration, Digitization) |

| Commercial & Advertising Agencies |

| Media & Entertainment |

| Individual / Consumer |

| Corporate / Industrial |

| Offline Studios & Retail Labs |

| Online Platforms & Marketplaces |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service Type | Professional Photography Services | |

| Stock Image Licensing | ||

| Photofinishing & Printing | ||

| Photo Booth & Event Imaging | ||

| Others (Restoration, Digitization) | ||

| By End-user | Commercial & Advertising Agencies | |

| Media & Entertainment | ||

| Individual / Consumer | ||

| Corporate / Industrial | ||

| By Distribution Channel | Offline Studios & Retail Labs | |

| Online Platforms & Marketplaces | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How large is the photography services market in 2026 and what is its growth outlook?

The market is valued at USD 39.21 billion in 2026 and is projected to reach USD 48.91 billion by 2031, advancing at a 4.52% CAGR.

Which service type currently holds the largest share of industry revenue?

Stock Image Licensing leads with 56.02% of photography services market share in 2025, supported by mature subscription models and global distribution networks.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to expand at a 6.19% CAGR, driven by rapid e-commerce adoption and rising corporate demand for professional visuals.

How is generative AI influencing business spending on photography services?

Enterprises license curated image libraries for AI training and adopt text-to-image tools, creating new revenue streams while accelerating content production workflows.

What effect does free user-generated content have on professional pricing?

The prevalence of smartphone photos now 92.5% of all images compresses prices for commodity shoots, pushing professionals toward high-value specialty offerings.

Page last updated on: