Online Grocery Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

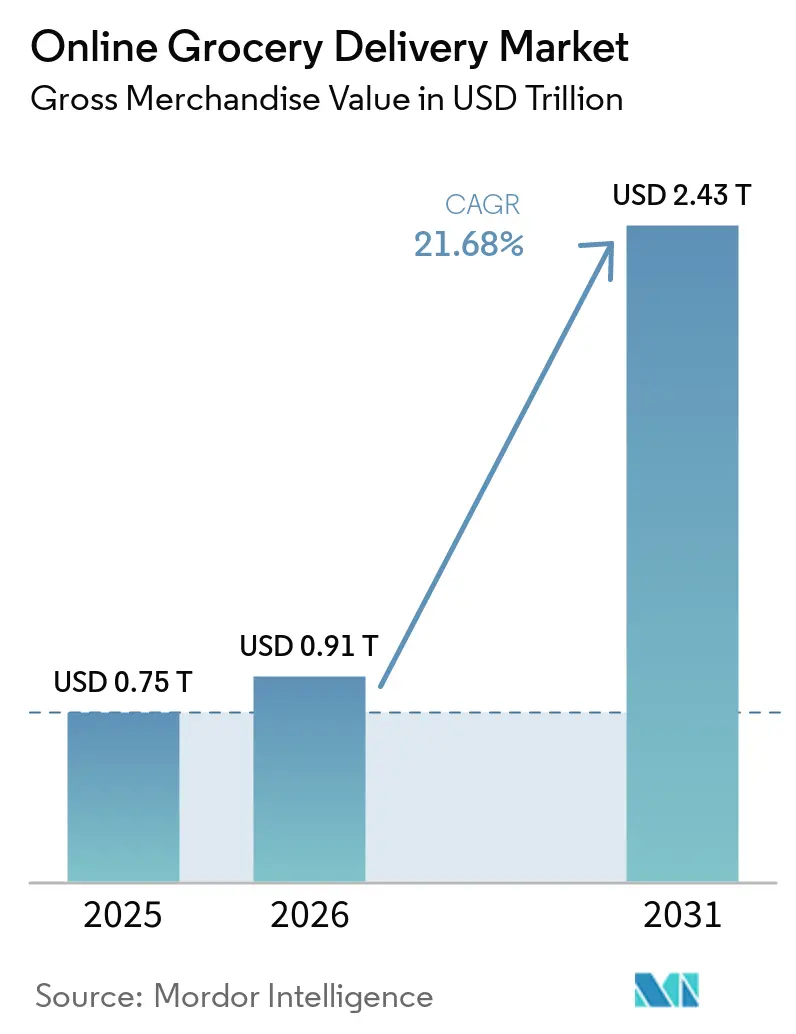

| Market Size (2026) | USD 0.91 Trillion |

| Market Size (2031) | USD 2.43 Trillion |

| Growth Rate (2026 - 2031) | 21.68% CAGR |

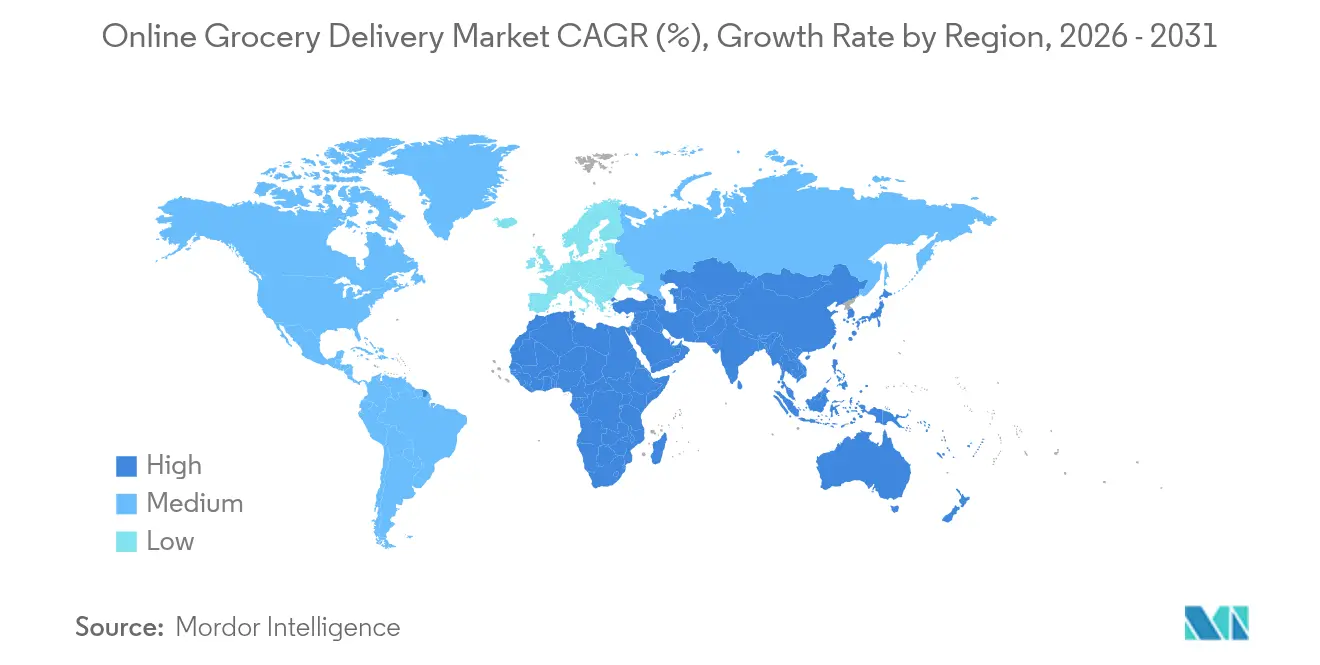

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Grocery Delivery Market Analysis by Mordor Intelligence

The online grocery delivery market size was valued at USD 0.75 trillion in 2025 and estimated to grow from USD 0.91 trillion in 2026 to reach USD 2.43 trillion by 2031, at a CAGR of 21.68% during the forecast period (2026-2031). The acceleration is underpinned by rising digital adoption, faster fulfilment models, and data-driven merchandising that strengthens profitability across formats. Asia-Pacific contributes the strongest incremental demand as dark-store build-outs compress delivery windows, while North America preserves scale leadership through established logistics networks. Competitive intensity is sharpening as omni-channel retailers monetize first-party data, quick commerce operators court impulse missions, and pure-play specialists refine last-mile technology. Strategic alliances between platforms and FMCG manufacturers improve forecasting accuracy and shelf availability, even as labour activism, antitrust rulings, and cold-chain bottlenecks challenge margins. Capital continues to rotate toward ESG-linked fleets, retail-media assets, and AI-based order orchestration, indicating sustained investment appetite despite macro volatility.

Key Report Takeaways

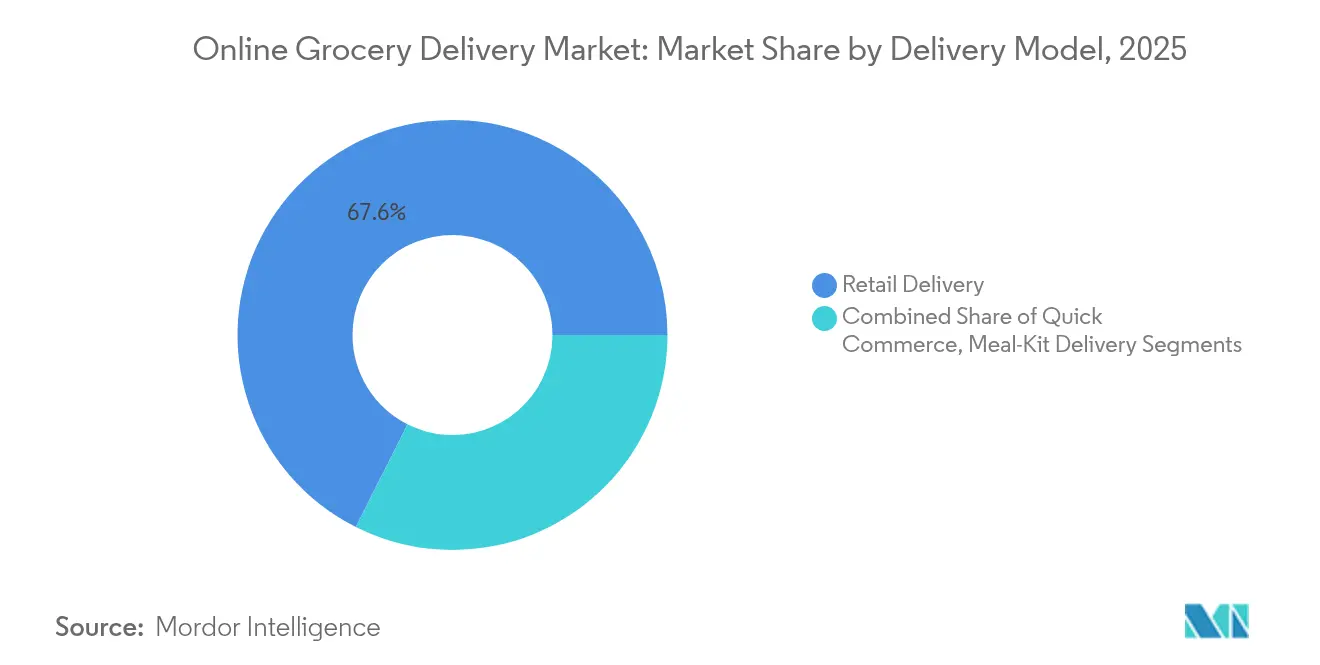

- By delivery model, retail delivery held 67.58% of the online grocery delivery market share in 2025, while quick commerce is projected to post a 28.45% CAGR through 2031.

- By platform type, omni-channel retailers commanded 45.78% revenue share in 2025; pure-play e-grocery platforms are forecast to register the highest CAGR at 23.95% over 2026-2031.

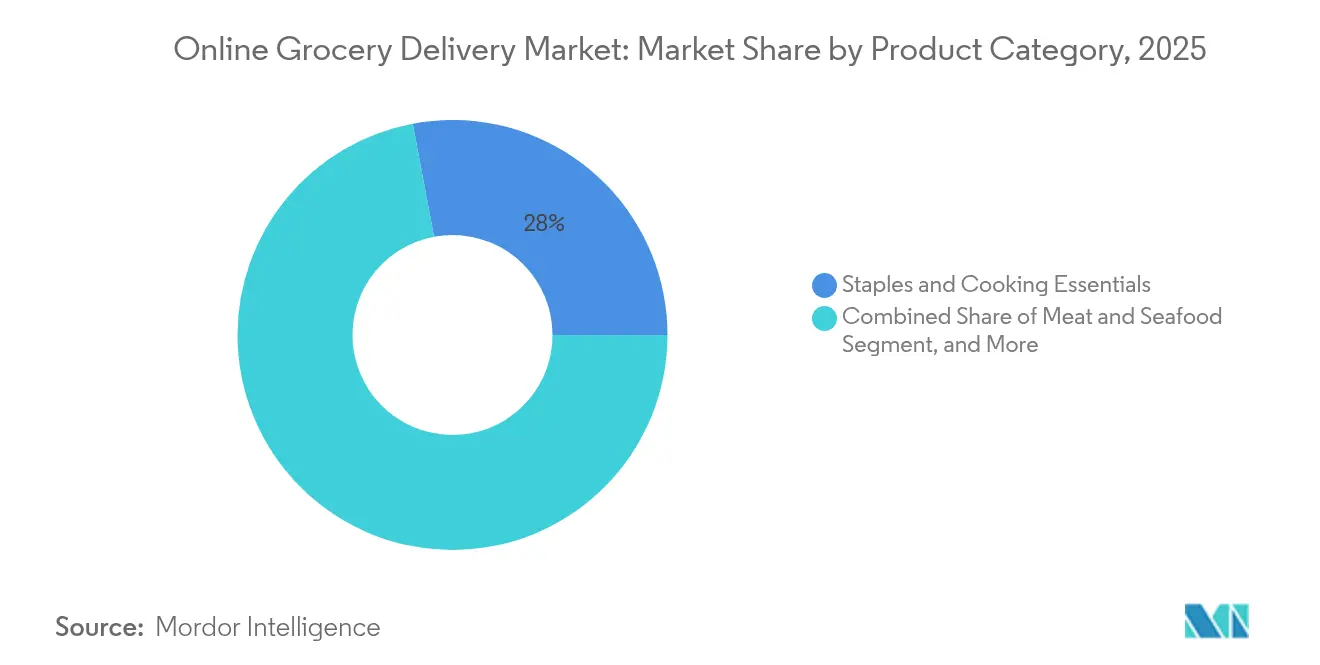

- By product category, staples and cooking essentials accounted for 27.96% of the online grocery delivery market size in 2025; fresh produce is advancing at a 24.6% CAGR to 2031.

- By delivery type, scheduled services captured 59.72% of the online grocery delivery market share in 2025, whereas instant/on-demand services are growing at more than 30% year-over-year in leading urban centres.

- Regionally, Asia-Pacific is poised for a 26.95% CAGR, outpacing all other regions, while North America remained the largest geography with 40.85% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperlocal Dark-Store Penetration in Asian Metros | +3.5% | Asia-Pacific, with spillover to Middle East | Medium term (~ 3-4 yrs) |

| Expansion of Real-Time Government Payment Rails | +2.8% | North America & Europe | Long term (≥ 5 yrs) |

| Data-Sharing Partnerships with FMCG Majors in Europe | +2.4% | Europe, with spillover to North America | Medium term (~ 3-4 yrs) |

| Growth of Single-Person Households in North America | +1.9% | North America, with spillover to Europe | Long term (≥ 5 yrs) |

| Retail-Media Monetization as Profit Catalyst | +1.6% | Global, with early adoption in North America | Medium term (~ 3-4 yrs) |

| ESG-Linked Capital for Carbon-Neutral Last-Mile | +1.2% | Europe & North America | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Hyperlocal Dark-Store Penetration in Asian Metros

Rapid dark-store roll-outs are redefining service-level benchmarks. In India, operators target 5,000–5,500 facilities by FY 2026, supporting 15- to 30-minute fulfilment that accelerates repeat purchase frequency [1]Bureau staff, “Dark store count may touch 5,500 by FY26 as competition heats up in quick commerce,” The Economic Times, economictimes.com. Blinkit intends to double its network to 2,000 sites by December 2025 despite near-term EBITDA deficits. High-density clustering improves inventory turns and slashes rider kilometres per order, strengthening unit economics. The competitive race is triggering parallel investments in micro-fulfilment automation and temperature-controlled picking zones to widen assortment without sacrificing speed. Spillover effects are emerging in Gulf cities where similar demographics favour micro-fulfilment solutions.

Expansion of Real-Time Government Payment Rails

Government payment modernisation is broadening addressable demand. The United States now permits SNAP and WIC redemptions on platforms such as Instacart, supported by a USD 153.9 billion SNAP budget for FY 2025 [2]USDA authors, “United States Department of Agriculture FY 2025 Budget Summary,” USDA, usda.gov. Real-time rails reduce checkout friction, lifting basket conversion among previously cash-reliant shoppers. European regulators are likewise upgrading instant-payment directives, which will allow grocers to settle cross-border transactions in seconds. These frameworks bolster inclusion while lowering acquirer fees, indirectly funding deeper promotional activity.

Data-Sharing Partnerships with FMCG Majors in Europe

Retailers and CPG suppliers are codifying data-exchange protocols to enhance shelf planning and campaign attribution. The YouGov–RetailZoom alliance in Hungary melds attitudinal and sell-out data, unlocking sharper segmentation for promotion calendars [3]Staff writer, “YouGov partners with RetailZoom to launch a new groundbreaking service for the Hungarian FMCG community,” YouGov, business.yougov.com. A post-Brexit trade reset reduces customs friction, further enabling collaborative inventory pooling across the Channel. Purchasing alliances such as Intermarché-Auchan-Casino aggregate volumes and harmonise data standards, consolidating negotiating power with multinationals.

Growth of Single-Person Households in North America

Solo-resident households now exceed 38 million in the United States, catalysing smaller-basket, higher-frequency missions. Meal-kit providers report USD 11.6 billion revenue for 2024 and are introducing single-portion SKUs to cut food waste. Academic research confirms that convenience and pricing strongly influence adoption, whereas perceived performance risks deter older cohorts. Grocers respond with curated “one-pot” bundles and smaller pack sizes that travel well through delivery networks.

Restraints Impact Analysis*

| Online Grocery Delivery: Restraints Impact Summary | Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Labor-Union Pushback Raising Courier Costs | -2.1% | North America & Europe | Short term (≤ 2 yrs) |

| Cold-Chain Gaps in Tier-2 Asian Cities | -1.8% | Asia-Pacific | Medium term (~ 3-4 yrs) |

| Margin Pressure & Antitrust Scrutiny | -1.5% | Global, with focus on North America | Medium term (~ 3-4 yrs) |

| Produce-Quality Trust Deficit in Latin America | -1.2% | Latin America | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Labor-Union Pushback Raising Courier Costs

Heightened labour activism is trimming operating leverage. A U.S. federal judge halted the Kroger–Albertsons merger citing wage concerns. Meanwhile, Woolworths warehouse staff in Australia demanded hourly pay of USD 38, disrupting stock flows [4]Holly Hales, “Noticing fewer groceries on the shelves at Woolworths?,” The Guardian, theguardian.com. Operators confront a 21% labour hours deficit versus 2019 levels, forcing wage hikes or automation investment that pressures contribution margins. Contract renegotiations also raise the probability of service interruptions during peak demand periods.

Cold-Chain Gaps in Tier-2 Asian Cities

Quality-consistent fresh delivery outside tier-1 metros remains difficult. Zepto’s partnership with Transport Corporation of India expands temperature-controlled capacity yet underlines systemic shortfalls. India’s cold-chain market is expected to quintuple by 2032, but many municipalities still lack high-throughput cross-docks. AI-enabled demand forecasting can improve lane utilisation, but capital intensity and power-supply instability slow roll-out, particularly for protein categories prone to spoilage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Model: Quick Commerce Reshapes Service Norms

Retail delivery retained the largest share in 2025, controlling 67.58% of the online grocery delivery market. Its scale leverages nationwide distribution centres and scheduled routes that optimise drop densities, securing predictable margins even as competitive promotions intensify. The online grocery delivery market size for retail delivery segments is projected to advance steadily, supported by loyalty integration and basket-building initiatives. Demand-driven replenishment systems reduce shrink and enhance turnaround of non-perishables, preserving profitability.

Quick commerce, although smaller, is redefining consumer expectations with sub-30-minute fulfilment. The model posts a 28.45% forecast CAGR through 2031, propelled by micro-warehouses, AI-powered picking, and rider network densification. Its share of the online grocery delivery market is rising fastest in Asian and European capitals where population density underpins high order velocity. Efficiency gains from dark-store automation and delivery batching are narrowing cost gaps with scheduled formats, accelerating wallet share migration from convenience stores.

By Platform Type: Omni-Channel Scale vs. Pure-Play Agility

Omni-channel retailers dominated 2025 with 45.78% of market revenue, underpinned by store-based fulfilment that amortises inventory across physical and digital channels. Many deploy AI engines for demand sensing, cutting out-of-stocks and enabling precise markdown optimisation. Their extensive SKU breadth deepens shopper loyalty, which in turn supports higher attachment rates for private-label lines. The online grocery delivery market size for omni-channel operators benefits from loyalty-app penetration that locks in recurring baskets.

Pure-play online grocery platforms, unburdened by legacy real estate, are scaling rapidly at a projected 23.95% CAGR. They harness cloud micro-services and proprietary routing algorithms to refresh features faster than traditional peers. Strategic alliances with ride-hailing firms extend courier capacity during peak windows, and embedded fintech modules streamline checkout. As venture funding prioritises sustainable unit economics, many pure-plays pursue profitability through retail-media monetisation and subscription tiers offering reduced service fees and carbon-neutral delivery.

By Product Category: Fresh Produce Accelerates on Trust Gains

Staples and cooking essentials formed the core basket in 2025, securing 27.96% share and anchoring the online grocery delivery market. Their non-perishable nature permits longer fulfilment windows and higher warehouse density. Retailers capitalise on stable turns to negotiate favourable supplier terms and reduce holding costs.

Fresh produce, historically hindered by quality scepticism, is now the fastest-growing segment at a 24.6% CAGR. Improved cold-chain nodes and AI-based ripeness prediction tools enhance appearance consistency upon arrival. When fresh items arrive in optimal condition, basket value increases and churn declines. These gains lift the online grocery delivery market share for fresh categories, compelling platforms to integrate produce-specific quality guarantees and near-real-time geotagged traceability.

By Delivery Type: Scheduled Dominance with On-Demand Momentum

Scheduled services controlled 59.72% of volumes in 2025, enabling route consolidation that cuts per-order costs by double-digit percentages relative to ad-hoc dispatch. Most households align replenishment cycles with weekly routines, and subscription discounts further stabilise demand. The online grocery delivery market size attributable to scheduled drop-offs is therefore insulated from courier surge pricing.

On-demand deliveries register robust growth, driven by urban professionals valuing immediacy for forgotten items and fresh meals. Order frequency spikes during evenings and weekends, stressing rider availability, yet rising autonomous-vehicle pilots hint at cost curve inflection. Full-self-driving fleets could unlock lower variable costs and higher safety, positioning on-demand to capture incremental wallet share within the overall online grocery delivery market.

Geography Analysis

North America retains primacy with 40.85% of global revenue in 2025. High broadband penetration, sophisticated payment infrastructure, and entrenched big-box retailers sustain leadership. Walmart alone posted USD 276 billion in U.S. grocery sales for FY 2025. The region’s online grocery delivery market size grows steadily as single-person households expand and labour activism drives partial automation of last-mile tasks. Regulatory scrutiny, exemplified by the blocked Kroger–Albertsons merger, constrains consolidation yet spurs service innovation.

Asia-Pacific is the fastest-growing geography with a projected 26.95% CAGR. Urbanisation and smartphone proliferation underpin demand, while dark-store roll-outs compress delivery lead times. India exemplifies momentum with a targeted 5,500 dark stores by FY 2026. Investment flows into cold-chain upgrades and AI-based inventory placement to bridge tier-2 city gaps. Platform competition is intense, yet rising disposable incomes and optionality around payment wallets drive sustained order growth across demographics.

Europe exhibits mature yet evolving dynamics. Data-sharing ecosystems facilitate hyper-personalised offers, and the UK-EU customs reset lowers frictions for cross-border sourcing (wdhn.com). Sustainability consciousness is high, with consumers willing to pay a 9.7% premium for low-carbon goods (pwc.com). Grocery alliances pool purchasing power to negotiate energy-efficient packaging and lower inbound transport emissions. The online grocery delivery market share in fresh categories therefore inches upward as trust in quality, traceability, and ESG credentials solidifies purchasing intent.

Mordor Intelligence provides coverage of the online grocery delivery market across other key regional markets, including Middle East and Africa, Asia, and South America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition spans legacy retailers, e-commerce majors, and regional specialists, yielding a moderately concentrated structure. Omni-channel giants leverage store estates for efficient click-and-collect and ship-from-store models, while pure-plays differentiate through user-experience velocity and AI-led curation. Recent strategic moves illustrate directional bets:

Walmart and Uber are piloting drones and autonomous vans to compress delivery costs and extend reach into lower-density suburbs. Instacart deepens platform stickiness by integrating restaurant delivery via Uber Eats, blurring boundaries between grocery and foodservice. Zepto expands temperature-controlled distribution to underpin a private-label meat portfolio targeting USD 120 million revenue by March 2026.

Retail-media monetisation is the most lucrative adjacency, generating 70-90% gross margins and creating a new battleground for data-rich incumbents. Simultaneously, ESG-linked loan structures reward emissions abatement, influencing fleet electrification timelines. Operators able to balance efficiency, societal expectations, and innovation pipelines will consolidate leadership as the online grocery delivery market scales.

Online Grocery Delivery Industry Leaders

Walmart Inc.

Amazon.com, Inc.

Uber Technologies Inc. (Uber Eats)

Just Eat Takeaway.com N.V.

Instacart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Loop Capital raised Instacart’s price target to USD 58, citing upward gross transaction value revisions that strengthen acquisition attractiveness to mobility platforms.

- May 2025: Maersk’s Latin America update highlighted harvest-season bottlenecks, prompting grocery platforms to diversify third-party logistics partners for produce reliability.

- April 2025: Flipkart limited quick-commerce expansion to eight metros to curb a USD 40 million monthly cash burn, tightening capital allocation discipline.

- April 2025: Walmart and Uber unveiled joint drone and AV pilots, signalling commitment to automation as a hedge against rising labour costs.

Global Online Grocery Delivery Market Report Scope

The study is structured to track the gross merchandise value of grocery items delivered once the order is placed through an online channel. Retail Delivery refers to delivery of grocery items from physical retail stores (supermarkets, brick-and-mortar shops, or grocery stores) when the order is placed through an online shop run by the retailer themselves. Quick Commerce refers to delivery services that support with last-mile delivery or operate ghost stores wherein the platform through which the order is placed are responsible for the deliverable. Meal Kit Delivery refers to the delivery of recipe boxes through subscription services are delivered from preparation by the customer.

The online grocery delivery market is segmented by delivery model (retail delivery, quick commerce, meal kit delivery), by geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Rest of Europe], Asia-Pacific [China, Japan, India, Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, Chile, Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Retail Delivery |

| Quick Commerce |

| Meal-Kit Delivery |

| Pure-Play E-grocery Platforms |

| Multi-Category Marketplaces |

| Omni-Channel Retailers |

| Meat and Seafood |

| Breakfast and Dairy Products |

| Snacks and Beverages |

| Fresh Produce |

| Staples and Cooking Essentials |

| Scheduled Deliveries |

| Instant/On-demand Deliveries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| SouthAmerica | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Delivery Model | Retail Delivery | |

| Quick Commerce | ||

| Meal-Kit Delivery | ||

| By Platform Type | Pure-Play E-grocery Platforms | |

| Multi-Category Marketplaces | ||

| Omni-Channel Retailers | ||

| By Product Category | Meat and Seafood | |

| Breakfast and Dairy Products | ||

| Snacks and Beverages | ||

| Fresh Produce | ||

| Staples and Cooking Essentials | ||

| By Delivery Type | Scheduled Deliveries | |

| Instant/On-demand Deliveries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| SouthAmerica | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the online grocery delivery market?

The online grocery delivery market stands at USD 0.91 trillion in 2026 and is forecast to reach USD 2.43 trillion by 2031.

Which region is growing fastest in online grocery delivery?

Asia-Pacific leads growth with a projected 26.95% CAGR through 2031, driven by rapid dark-store expansion and rising smartphone penetration.

How big is the quick commerce segment within online grocery?

Quick commerce is smaller than traditional retail delivery today but is expected to post a 28.45% CAGR between 2026 and 2031, making it the fastest-growing delivery model.

Why are retail media networks important for grocery platforms?

Retail media generates 70-90% gross margins and delivers an USD 8.5 billion revenue opportunity in 2025, helping offset thin grocery margins.

What are the main challenges facing online grocery delivery operators?

Key challenges include labour-union wage pressures, cold-chain infrastructure gaps in emerging markets, and rising regulatory scrutiny over market concentration and sustainability.

How are sustainability goals influencing last-mile operations?

Grocers are securing ESG-linked financing and piloting electric or autonomous vehicles, aiming to meet emissions targets and capture consumers willing to pay nearly 10% more for sustainable delivery options.

Page last updated on: