Self-checkout System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.97 Billion |

| Market Size (2031) | USD 9.03 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-checkout System Market Analysis by Mordor Intelligence

The self-checkout system market size is projected to be USD 5.44 billion in 2025, USD 5.97 billion in 2026, and reach USD 9.03 billion by 2031, growing at a CAGR of 8.63% from 2026 to 2031. These gains stem from tightening labor pools, surging digital-wallet adoption, and retailers’ need for faster front-end throughput. Hardware still anchors deployments, but margin now migrates to software, analytics, and managed services that curb fraud and integrate loyalty data. Computer-vision startups have compressed scanning time to under 10 seconds, giving retailers a path to reclaim floor space and redeploy staff. At the same time, advertising sold on kiosk screens is converting what was once a pure cost center into a blended labor-savings and media-revenue asset.

Key Report Takeaways

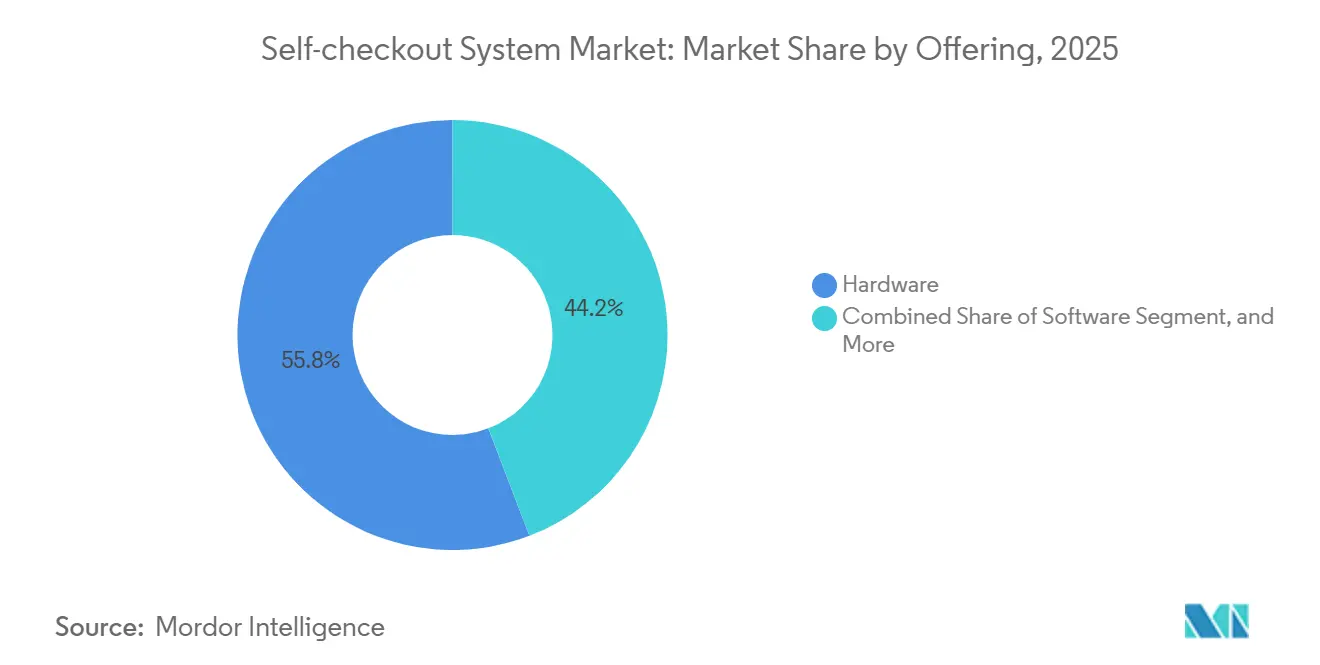

- By offering, hardware led with 55.83% of self-checkout system market share in 2025, while services are set to grow at an 11.31% CAGR through 2031.

- By transaction type, cash-based lanes held 61.79% share of the self-checkout system market size in 2025, whereas cashless lanes are projected to expand at a 12.02% CAGR.

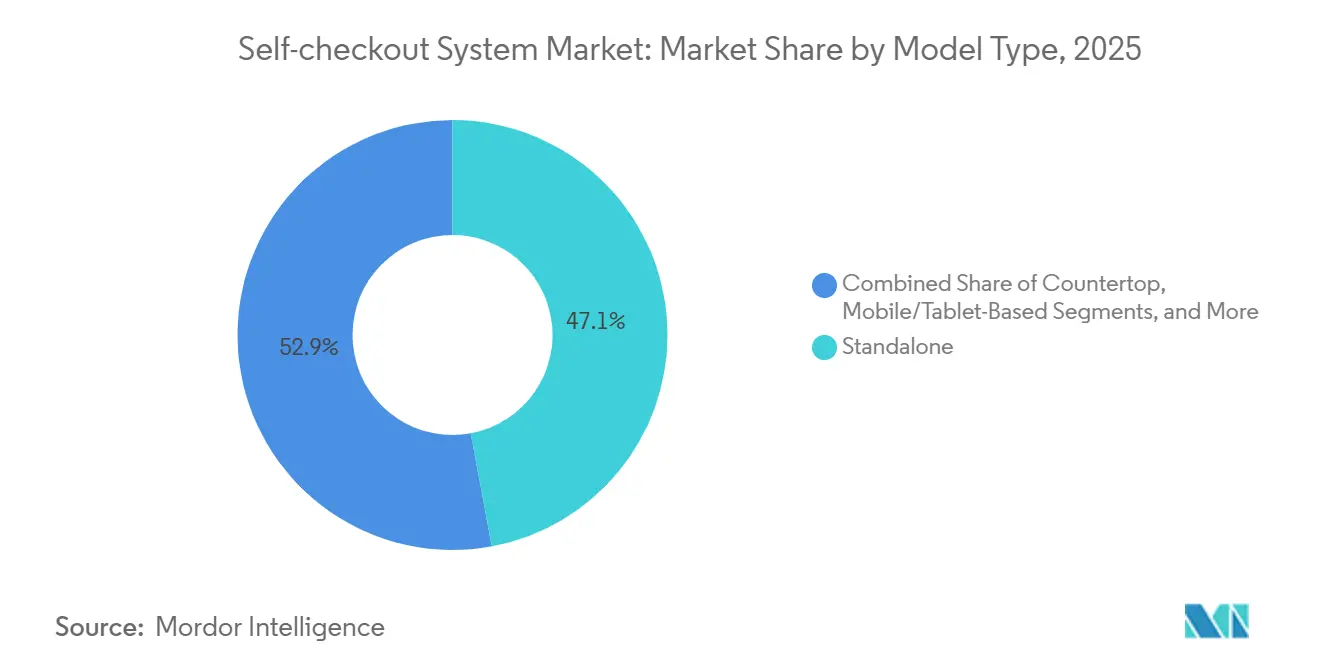

- By model type, standalone kiosks accounted for 47.07% of 2025 revenue and mobile or tablet systems are advancing at a 9.87% CAGR.

- By end-user industry, retail captured 59.68% of 2025 deployments, but travel venues are pacing the field at a 10.27% CAGR.

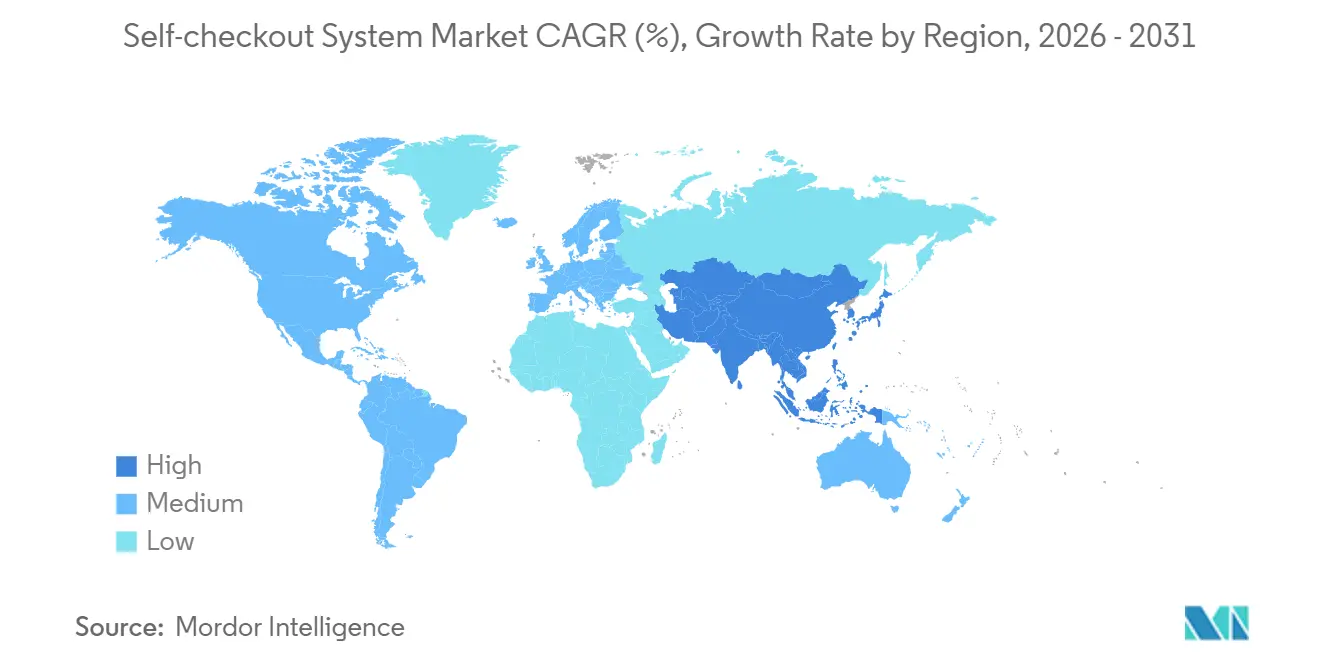

- By geography, North America controlled 58.47% share in 2025 and Asia Pacific is forecast to register the fastest 11.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Self-checkout System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption by Supermarkets and Hypermarkets | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Labor Shortages and Increasing Labor Costs | +2.3% | North America, Europe, Japan, Australia | Short term (≤ 2 years) |

| Growing Preference for Cashless and Contactless Payments | +1.8% | Global, led by Asia Pacific and Europe | Medium term (2-4 years) |

| Technological Advances in AI and Computer-Vision | +1.5% | North America, Europe, China | Long term (≥ 4 years) |

| Store-as-Media Monetization Through SCO Screens | +0.6% | North America and Europe | Long term (≥ 4 years) |

| App-Driven Personalized Promotions and Analytics | +0.7% | North America, Europe, urban Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption by Supermarkets and Hypermarkets

Large-format grocers now view the self-checkout system market as a strategic lever to free staff for click-and-collect picking and shelf-stocking tasks. An NCR Voyix survey of 1,000 U.S. shoppers in 2024 found that 43% prefer self-service, with the figure climbing to 60% among adults aged 18-44.[1]NCR Voyix, “Consumer Preferences and Self-Checkout Trends,” NCRVOYIX.COM Kroger reported that baskets rung through its 2,700 self-checkout lanes match the value of baskets at manned registers, calming earlier fears of trade-down. Tesco’s hybrid service model routes simple baskets to kiosks while reserving staffed lanes for age-restricted items, preserving compliance and customer choice. Carrefour’s 2025 pilot of scan-and-go apps in 150 French stores suggests European hypermarkets see mobile checkout as the next evolution. Together, these moves underscore a structural commitment from grocers to self-service formats that will sustain double-digit deployment growth.

Labor Shortages and Increasing Labor Costs

Retail quit rates sat at 3.2% per month in 2024, topping the economy-wide average and forcing operators to automate front-end roles. Japan projects a 6.4 million-worker shortfall by 2030, accelerating kiosk adoption in convenience stores.[2]Ministry of Health, Labour and Welfare, Japan, “Labor Force Projections 2030,” MHLW.GO.JP Walmart disclosed that self-checkout has trimmed labor hours per transaction by 35%, unlocking 740,000 associate hours for e-commerce fulfillment. Australia’s 5.75% minimum-wage increase in mid-2024 pushed Woolworths and Coles to widen self-service footprints. As wage inflation grows faster than kiosk amortization rates, the self-checkout system market gains a compelling cost-avoidance narrative that resonates with finance chiefs.

Growing Preference for Cashless and Contactless Payments

India’s Unified Payments Interface clocked 13.4 billion transactions in December 2024, up 58% year over year. Cashless terminals remove the cost of cash handling, armored transport, and counterfeit detection. Target calculated that cashless lanes cost 40% less to operate than cash-accepting kiosks. Regulators also back the shift: India’s 2024 National Retail Policy promotes digital payment in organized retail. As smartphone penetration climbs, cashless checkout becomes table stakes for convenience and hygiene, propelling further penetration of the self-checkout system market.

Technological Advances in AI and Computer-Vision

Computer-vision accuracy for produce now tops 95%, letting kiosks identify items in under 0.5 seconds. Mashgin processed 440 million transactions across 4,000 U.S. sites in 2024, showcasing sub-second recognition without barcodes. Toshiba’s MxP Vision Kiosk, unveiled at NRF 2025, combines Intel RealSense cameras with edge inference for real-time fraud alerts.[3]Toshiba Global Commerce Solutions, “MxP Vision Kiosk Launch,” COMMERCE.TOSHIBA.COM Standard AI and Zippin deploy ceiling-mounted cameras to offer just-walk-out baskets, broadening use cases beyond fixed kiosks. As algorithms mature, retailers gain shrinkage control while providing frictionless experiences, making AI the central differentiator in the self-checkout system industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for SMB Retailers | -1.2% | Global, acute in South America, Africa, South Asia | Short term (≤ 2 years) |

| Theft and Shrinkage Concerns at Unattended Lanes | -0.9% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Consumer Demand for Human Interaction in Premium Retail | -0.4% | Europe, North America, Middle East | Long term (≥ 4 years) |

| Data-Privacy Legislation Limiting Biometric Scanning | -0.6% | Europe, North America, select Asia Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for SMB Retailers

Independent grocers face kiosk price tags of USD 15,000-40,000, a steep hurdle when EBITDA margins hover near 3%.[4]IT Retail, “Self-Checkout Capital Expenditure Study,” ITRETAIL.COM Entry models under USD 3,000 often exclude payment modules, forcing trade-offs that raise shrinkage. Zippin’s subscription option converts capex into opex, but annual fees can exceed USD 48,000 if stores run modest traffic. Import duties of up to 35% in South America plus double-digit lending rates further stretch payback periods. Until hardware costs fall or financing improves, small formats will adopt cautiously, dampening near-term self-checkout system market growth.

Theft and Shrinkage Concerns at Unattended Lanes

Shrinkage at self-service lanes runs 2-4 percentage points above staffed registers, costing U.K. grocers GBP 2 billion (USD 2.5 billion) in 2024. Lidl paused an AI-surveillance rollout after privacy pushback, showing how theft solutions can collide with customer sentiment. Diebold Nixdorf’s Vynamic Smart Vision claims 30% loss reduction but adds USD 5,000-8,000 in license fees per terminal. Walmart still employs 4,000 asset-protection associates for kiosk monitoring. Thus, loss-prevention spend partially offsets labor savings and tempers the self-checkout system market’s cost-case narrative.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Hardware as Integration Complexity Rises

Services will expand at an 11.31% CAGR through 2031, outstripping hardware’s installed-base dominance because retailers need POS integration, computer-vision analytics, and managed upgrades. Integration contracts average USD 50,000-120,000 for mid-sized grocers, pushing the self-checkout system market size in services toward a larger revenue pool.[5]ECR Software Corporation, “Integration Cost Benchmarks,” ECRS.COM Maintenance at 15-20% of hardware cost and rising demand for training lift recurring billings. Hardware retains scale thanks to scanners, payment modules, and scales, yet commoditization squeezes margin. Modular kiosks from Pan-Oston let retailers refresh payment modules without full replacements, trimming lifecycle expense. Software subscriptions linked to AI detection and loyalty engines provide predictable income, sharpening vendor focus on cloud updates over physical units.

Software-led value creation also injects competitive tension as computer-vision specialists monetize algorithms independently of hardware. This pivot raises switching risk for legacy vendors anchored to terminal sales. As retailers standardize on open APIs, best-of-breed analytics can bolt onto any kiosk platform, redistributing power inside the self-checkout system market. Vendors that bundle white-label media networks on kiosk screens add a higher-margin revenue stream, attracting CPG advertising dollars and further elevating service share.

By Transaction Type: Cashless Lanes Accelerate as Digital Wallets Gain Share

Cash-based terminals retained 61.79% of self-checkout system market share in 2025, but cashless lanes are tracking a 12.02% CAGR to 2031 on the back of wallet apps and contactless cards. Cashless kiosks remove bill recyclers and coin hoppers, cutting capex and ongoing vault-cash courier fees. Target quantified a 40% lower operating cost for cashless units. Hybrid kiosks give flexibility in cash-dependent regions yet introduce mechanical complexity and service calls. India’s UPI surge illustrates an accelerating glide path toward full cashless, while underbanked communities in parts of the United States still mandate cash acceptance. Regulatory nudges that cap interchange or nudge digital acceptance will keep steering capital toward electronic-only lanes, broadening the self-checkout system market.

The shift also widens inclusion of value-added services such as buy-now-pay-later at the kiosk, boosting average ticket sizes. Yet retailers must balance payment optionality with queue time: cash transactions remain slower due to bill validation. Over time, differential hardware savings and faster line speeds will tip more operators toward pure cashless configurations.

By Model Type: Mobile Platforms Disrupt Fixed Infrastructure

Standalone kiosks delivered 47.07% of 2025 revenue, but mobile and tablet solutions are pacing at a 9.87% CAGR. Walmart Plus Scan and Go lets members bypass fixed lanes, signaling that in-app checkout can coexist with kiosk fleets. Amazon’s Dash Cart embeds scanners in shopping carts, merging scan-and-go with weight sensors. Countertop and wall-mounted forms thrive where floor space is scarce, including pharmacies and quick-service restaurants. Modular systems from StrongPoint allow attachments such as cash acceptors or 2-D scanners without whole-unit swaps.

As 5G and edge computing mature, mobile models can offload vision processing to cloud services, reducing on-cart hardware costs and unlocking new entrants. For retailers, agile models lower capex and accelerate pilots, fostering broader dispersion of the self-checkout system market. Yet mobile’s success hinges on high app adoption and reliable store Wi-Fi, meaning fixed kiosks will remain a cornerstone in high-traffic stores for the foreseeable future.

By End-User Industry: Travel Venues Prioritize Throughput Over Labor Savings

Retail maintained 59.68% of 2025 deployments, but travel hubs are advancing at a 10.27% CAGR as airports, rail hubs, and stadiums aim to cut queue times. Heathrow’s 2025 pilot of Zippin’s Walk-Up lanes processed duty-free baskets in under 45 seconds. The O2 arena’s Amazon Just Walk Out concessions reduced event-rush transaction times to below 30 seconds. Cruise operators and train stations are exploring compact kiosks that handle both tickets and retail, improving passenger flow.

Specialty retail segments such as pharmacy and DIY adopt kiosks selectively, reserving staffed counters for high-touch advisory moments. Luxury stores continue to favor personal interaction, limiting kiosk rollout. Yet entertainment venues, cinemas, and theme parks see value in autonomous micro-stores that extend selling capacity without expanding footprint. This pattern diversifies end-market revenue and cements the self-checkout system industry’s cross-vertical relevance.

Geography Analysis

North America commanded 58.47% of revenue in 2025 on the strength of high labor costs, near-universal POS card penetration, and early adopter culture. U.S. grocers invest heavily in AI analytics, while Canadian retailers extend kiosk footprints alongside rising minimum wages. Mexico’s organized retail sector mirrors these drivers, although cash acceptance remains critical in rural areas.

Europe ranks second, with momentum in the United Kingdom, Germany, and France. The self-checkout system market size in Europe faces new compliance overhead as the AI Act designates biometric vision as high-risk, requiring third-party audits.[6]European Commission, “Artificial Intelligence Act,” EC.EUROPA.EU German discounters such as Lidl balance shrinkage variability with aggressive cost targets, creating fertile ground for computer-vision analytics. Southern Europe lags due to high cash preference and smaller store footprints, but tourism hubs are piloting compact units.

Asia Pacific is the fastest-growing region at an 11.86% CAGR, propelled by China’s unmanned-store boom and India’s National Retail Policy. China’s self-checkout system market benefits from mature QR-code payments and state support for smart retail.[7]Ministry of Commerce, People’s Republic of China, “Unmanned Retail Report,” MOFCOM.GOV.CN India’s GST harmonization and digital-wallet surge foster organized retail formats that favor kiosks. Japan’s acute labor shortage drives convenience stores to install compact units even in sub-500 square-foot shops. South Korea and ASEAN grocers pilot smartphone scan-and-go to serve mobile-centric shoppers, while Australia extends kiosks in response to wage hikes and turnover.

South America grows off a smaller base; Brazil and Argentina lead adoption as fintech wallets expand. Import tariffs and volatile exchange rates temper pace. The Middle East invests via smart-city initiatives, with Dubai promoting cashless retail as part of its digital-economy blueprint.[8]Department of Economy and Tourism, Dubai, “Cashless Transaction Strategy,” DUBAIDET.AE Africa remains nascent, though South Africa pilots kiosks in urban supermarkets. Overall, regional dynamics point to converging global appetite for the self-checkout system market tempered by local payment and labor variables.

Competitive Landscape

Legacy POS vendors NCR Voyix, Diebold Nixdorf, and Toshiba Global Commerce Solutions controlled an estimated 45% of hardware shipments in 2025, yet hardware gross margins narrowed as kiosks commoditized. NCR Voyix transitioned to an ODM model with Ennoconn in 2024 to focus on software and managed services. Diebold Nixdorf launched Vynamic Smart Vision to embed Azure-based produce recognition, seeking to lift attach-rate revenue.

Disruptors Mashgin, Standard AI, and Zippin bypass barcodes using computer vision, winning convenience stores, stadiums, and corporate cafeterias. Mashgin’s 440 million 2024 transactions provide scale proof for AI kiosks.[9]Mashgin, “Company Overview,” MASHGIN.COM Standard AI, backed by USD 35 million in Series B funding, positions its retro-fit camera rig as a capex-light pathway for existing retailers.[10]Standard AI, “Series B Funding Release,” STANDARD.AI

White-space growth lies in healthcare and banking. Amazon Pharmacy’s 2025 kiosk pilot dispenses pre-packed prescriptions in minutes, foreshadowing broader healthcare migration. Banks are trialing self-service machines for routine teller tasks, freeing advisors for complex queries. Competitive intensity now hinges on AI performance, integration ease, and the ability to bundle retail-media capabilities that create incremental profit pools beyond transaction processing.

Self-checkout System Industry Leaders

Diebold Nixdorf, Inc.

Fujitsu Ltd.

NCR Corporation

ECR Software Corporation

Toshiba Global Commerce Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Amazon Pharmacy introduced prescription-pickup kiosks at One Medical sites in Los Angeles, trimming wait time to two minutes.

- February 2025: Mashgin inked a roll-out with Wesco to install AI kiosks across 200 additional U.S. convenience stores, lifting its footprint to 4,000 locations.

- January 2025: Toshiba Global Commerce Solutions debuted the MxP Vision Kiosk at NRF 2025, integrating Intel depth cameras for 0.5-second item recognition.

Global Self-checkout System Market Report Scope

Self-checkout systems, now prevalent in retail, grocery, and hospitality sectors, empower customers to complete transactions and place orders independently. In response to evolving demands, today's self-checkout systems undergo tailored re-engineering and manufacturing, enhancing store compatibility, functionality, cost-effectiveness, form factor, and reliability. As secure, self-payment technologies gain traction, kiosk vendors are increasingly offering cashless solutions, a trend poised to drive market growth in the coming years.

The Self-Checkout System Market Report is Segmented by Offering (Hardware, Software, Services), Transaction Type (Cash, Cashless, Hybrid), Model Type (Standalone, Countertop, Mobile/Tablet-Based, Wall-Mounted, Modular), End-User Industry (Retail, Entertainment, Travel, Financial Services, Healthcare, Other), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Payment Modules |

| Barcode Scanners | |

| Weighing Scales | |

| Display and Touch Panels | |

| Other Hardwares | |

| Software | POS Integration Software |

| Computer-Vision Software | |

| Fraud-Prevention Analytics | |

| Loyalty and CRM Integration | |

| Services | Integration and Deployment |

| Maintenance and Support | |

| Managed Services | |

| Consulting and Training |

| Cash |

| Cashless |

| Hybrid |

| Standalone |

| Countertop |

| Mobile/Tablet-Based |

| Wall-Mounted |

| Modular |

| Retail | Supermarkets and Hypermarkets |

| Department Stores | |

| Convenience Stores | |

| Specialty Stores | |

| Pharmacy and Drugstores | |

| Entertainment | Cinemas |

| Theme Parks | |

| Stadiums | |

| Travel | Airports |

| Railway Stations | |

| Cruise Terminals | |

| Financial Services | Bank Branches |

| Healthcare | Hospitals |

| Pharmacies | |

| Other End-User Industries | Quick Service Restaurants |

| Universities and Campuses |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Benelux | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | North Africa |

| South Africa | |

| Rest of Africa |

| By Offering | Hardware | Payment Modules |

| Barcode Scanners | ||

| Weighing Scales | ||

| Display and Touch Panels | ||

| Other Hardwares | ||

| Software | POS Integration Software | |

| Computer-Vision Software | ||

| Fraud-Prevention Analytics | ||

| Loyalty and CRM Integration | ||

| Services | Integration and Deployment | |

| Maintenance and Support | ||

| Managed Services | ||

| Consulting and Training | ||

| By Transaction Type | Cash | |

| Cashless | ||

| Hybrid | ||

| By Model Type | Standalone | |

| Countertop | ||

| Mobile/Tablet-Based | ||

| Wall-Mounted | ||

| Modular | ||

| By End-User Industry | Retail | Supermarkets and Hypermarkets |

| Department Stores | ||

| Convenience Stores | ||

| Specialty Stores | ||

| Pharmacy and Drugstores | ||

| Entertainment | Cinemas | |

| Theme Parks | ||

| Stadiums | ||

| Travel | Airports | |

| Railway Stations | ||

| Cruise Terminals | ||

| Financial Services | Bank Branches | |

| Healthcare | Hospitals | |

| Pharmacies | ||

| Other End-User Industries | Quick Service Restaurants | |

| Universities and Campuses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Benelux | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | North Africa | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the self-checkout system market in 2031?

The market is forecast to reach USD 9.03 billion by 2031 at an 8.63% CAGR.

Which segment will add the most incremental revenue by 2031?

Services, growing at an 11.31% CAGR, will add the greatest incremental revenue as retailers seek integration and analytics.

How fast is the cashless checkout segment expanding?

Cashless lanes are forecast to grow at a 12.02% CAGR between 2026 and 2031.

Which region is expected to record the quickest growth?

Asia Pacific is projected to advance at an 11.86% CAGR, fueled by China's unmanned retail and India's policy support.

What technology shift is most disruptive to traditional kiosks?

Computer-vision checkout that eliminates barcode scanning is compressing transaction time and attracting retailer investment.

How are retailers offsetting kiosk hardware costs?

Many are selling advertising on kiosk screens, generating media revenue that can cover up to 20% of annual hardware amortization.

Page last updated on: