Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

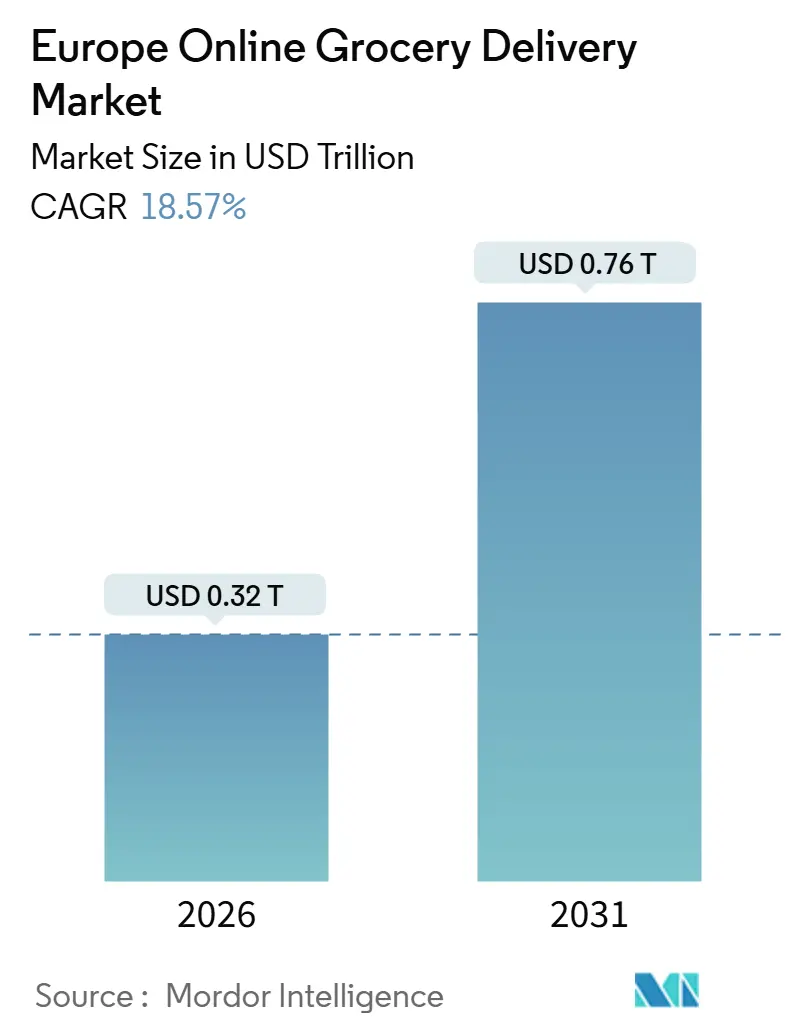

| Market Size (2026) | USD 0.32 Trillion |

| Market Size (2031) | USD 0.76 Trillion |

| Growth Rate (2026 - 2031) | 18.57% CAGR |

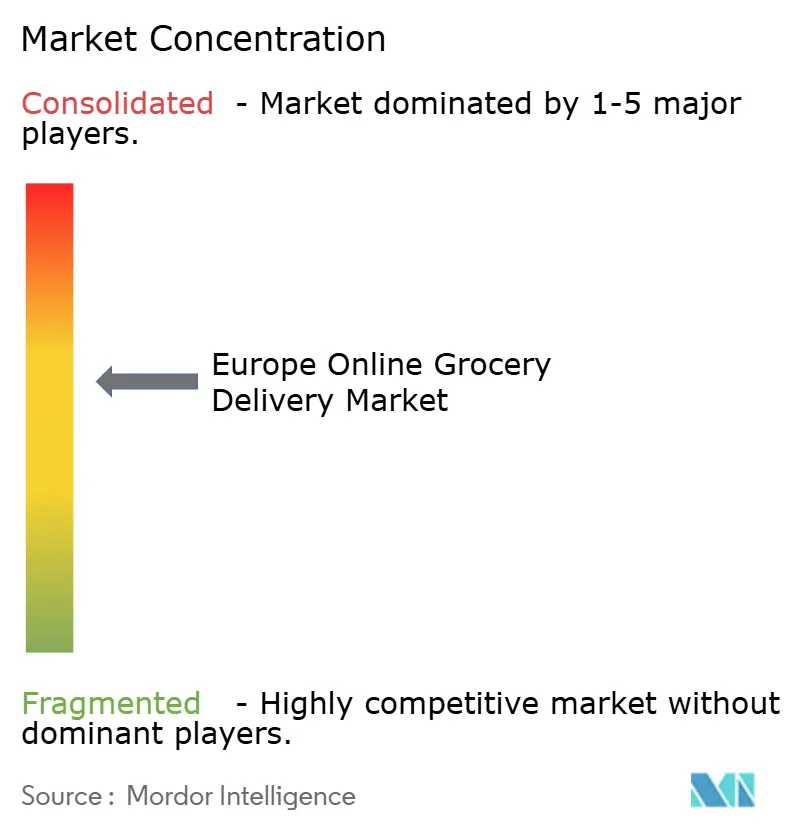

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Online Grocery Delivery Market Analysis by Mordor Intelligence

The Europe online grocery delivery market size is valued at USD 0.32 trillion in 2026 and is projected to reach USD 0.76 trillion by 2031, reflecting an 18.57% CAGR over the forecast period. Momentum stems from omnichannel grocers converting store estates into micro-fulfillment hubs, disciplined capital re-allocation by surviving quick-commerce specialists, and the rapid roll-out of retail-media monetization engines. Scheduled delivery remains the backbone of the Europe online grocery delivery market thanks to superior route density, while instant fulfillment is now scaling in dense urban cores where average basket values justify higher fees. Investments in cold-chain automation are eroding the quality gap between store-picked and online-picked fresh produce, further widening the addressable audience. Country-level outperformance skews toward Spain, where late-stage digitization and mobile-first consumer segments are pushing the Europe online grocery delivery market deeper into the mass-market.

Key Report Takeaways

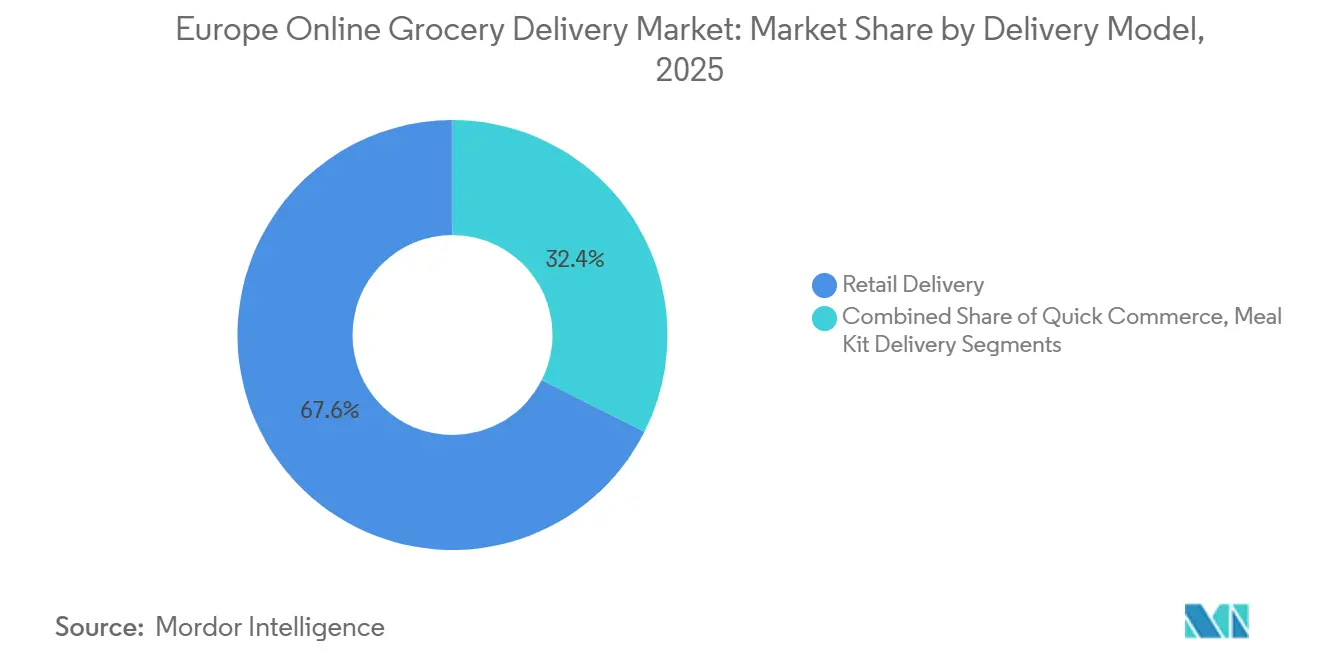

- By delivery model, retail delivery accounted for 67.57% of revenue in 2025, while quick commerce is advancing at a 19.43% CAGR through 2031.

- By platform type, omnichannel operators held 46.32% share of the Europe online grocery delivery market in 2025, whereas pure-play platforms are forecast to expand at 19.63% CAGR.

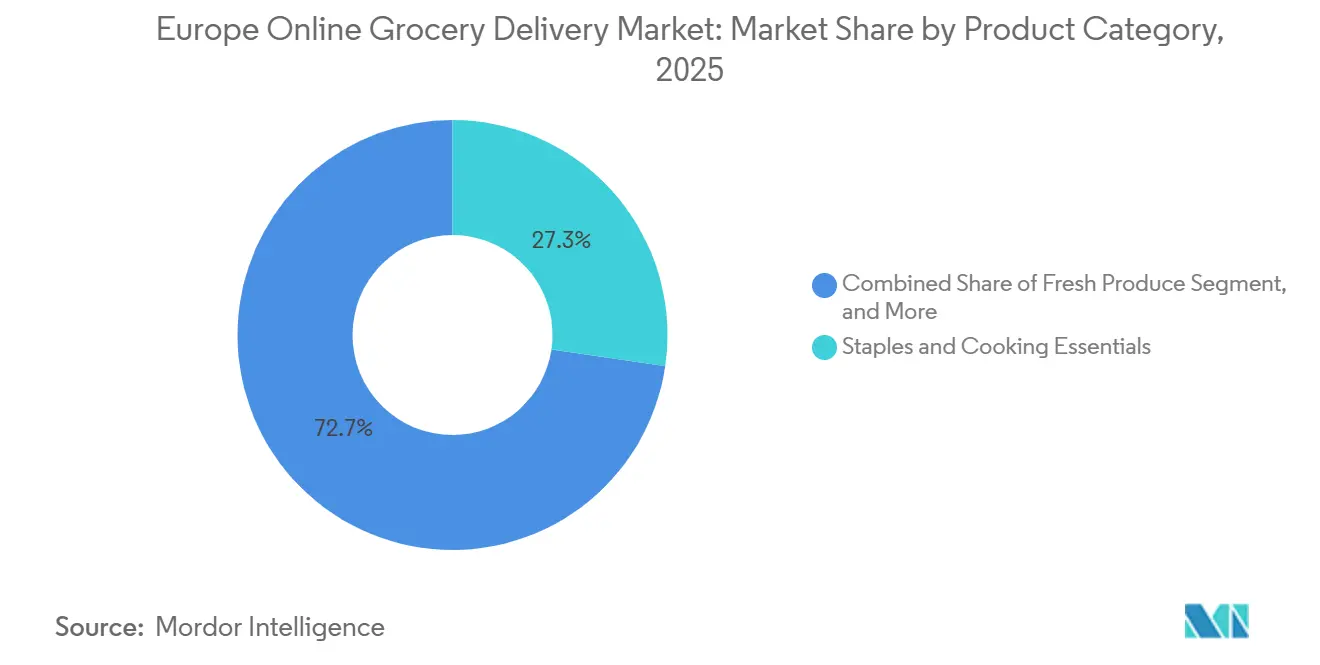

- By product category, staples and cooking essentials captured 27.31% revenue share in 2025; fresh produce is projected to grow at a 20.12% CAGR to 2031.

- By delivery type, scheduled windows commanded 59.63% share in 2025, and instant or on-demand fulfillment is rising at a 19.72% CAGR.

- By country, Germany led with 21.42% of regional revenue in 2025, and Spain is expected to post the fastest 20.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift in Shopping Mode Preferences Toward Digital Channels | +4.2% | Germany, United Kingdom, France, Spain, Italy | Medium term (2-4 years) |

| Acceleration of Same-Day Logistics Infrastructure Across Europe | +3.8% | Germany, United Kingdom, Netherlands, urban France and Spain | Short term (≤ 2 years) |

| Integration of Retail-Media Networks Boosting Platform Profitability | +3.1% | United Kingdom, Germany, France, Netherlands | Medium term (2-4 years) |

| Expansion of Private-Label Online Assortments by Leading Grocers | +2.9% | United Kingdom, Germany, France | Medium term (2-4 years) |

| AI-Driven Personalization Increasing Basket Size and Retention | +2.7% | Germany, United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Growing Investor Focus on Sustainable Last-Mile Solutions | +1.9% | Netherlands, Germany, United Kingdom, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift In Shopping Mode Preferences Toward Digital Channels

Mobile-first consumers now treat weekly stock-up and top-up missions as a single digital flow, undercutting the stickiness of traditional store visits. Omnichannel grocers respond by blending click-and-collect, same-day delivery, and loyalty ecosystems that reward cross-channel engagement. Germany and the United Kingdom show slowing shopper acquisition and are pivoting toward lifetime-value optimization, whereas Spain and Italy are still in user-acquisition mode. In Southern Europe, smartphone penetration above 90% unlocks app-centric experiences that compress decision windows and raise order frequency. Higher digital engagement lifts data exhaust, which feeds recommendation engines and lifts retention.

Acceleration Of Same-Day Logistics Infrastructure Across Europe

Micro-fulfillment centers within 10 kilometers of consumers now ship orders in under two hours, shrinking a service promise that once spanned full days. Automation raises pick-rates above 200 units per hour, letting grocers profit on baskets below GBP 50 (USD 63).[1]Ocado Group, “Full-Year Results 2025,” Ocadogroup.com Funding rounds tied to same-day infrastructure continue despite a tougher capital cycle, as investors favor tangible throughput gains over scale-at-any-cost models. Regulators forced dark-store relocations into hybrid store-warehouse formats, but operators recoup margin by applying machine-learning route optimization that squeezes extra drops per driver shift. Rapid delivery is therefore migrating from blanket coverage to selective urban corridors with the densest order heatmaps.

Integration Of Retail-Media Networks Boosting Platform Profitability

First-party shopper data has turned into a high-yield asset class. European retail-media spend is on a steep trajectory, and grocery banners capture outsized share because basket-level insights enable closed-loop attribution.[2]Tesco PLC, “Annual Report 2025,” Tescoplc.com Tesco and Sainsbury’s each launched in-house ad studios using generative AI that slashes creative lead times and democratizes participation for small suppliers. Media income improves platform EBITDA by 200 to 400 basis points, narrowing the profitability gap versus brick-and-mortar channels. Scale further compounds advantage, creating barriers for smaller pure-play operators that lack reach and logged-in user bases.

Expansion Of Private-Label Online Assortments By Leading Grocers

Private-label SKUs extend from shelf-stable essentials into fresh, organic, and ready-to-eat formats online. Gross-margin uplift of 5 to 10 percentage points versus branded goods funds promotional pricing that locks in subscription customers. Digital shelf analytics let grocers test micro-assortments quickly, retiring slow movers without physical markdowns. The strategy resonates in inflation-sensitive households that equate private label with value discipline. Early adopters report accelerating repeat rates and higher share of wallet as consumers migrate entire pantry missions to house brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fulfillment and Last-Mile Costs in Low-Density Areas | -2.8% | Rural and peri-urban Spain, Italy, France, Eastern Europe | Short term (≤ 2 years) |

| Rising Price Sensitivity Amid Persistent Food-Inflation Pressures | -2.3% | Spain, Italy, United Kingdom, Germany | Medium term (2-4 years) |

| Regulatory Scrutiny of Dark Stores and Urban Traffic Congestion | -1.9% | France, Netherlands, Germany | Short term (≤ 2 years) |

| Fragmented Cold-Chain Standards Affecting Fresh-Food Quality | -1.6% | Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Fulfillment And Last-Mile Costs In Low-Density Areas

Order density below 0.8 drops per kilometer breaks the cost curve, making fuel and labor overhead impossible to absorb. Quick-commerce pioneers exited or retrenched after discovering that nationwide coverage demanded subsidy burn rates the capital markets no longer tolerate.[3]Reuters Staff, “European Quick Commerce Faces Consolidation and Regulation,” Reuters.com Omnichannel grocers partially hedge with click-and-collect, but pure-plays must impose high minimum-order thresholds that dampen conversion. Technology fixes—dynamic routing and electric vehicles—ease pain yet cannot fully offset sparse demand pockets, limiting the total addressable slice of the Europe online grocery delivery market outside metros.

Rising Price Sensitivity Amid Persistent Food-Inflation Pressures

Although food inflation slowed to 1.5% year-over-year by February 2025, memory of double-digit surges lingers. Households now scrutinize delivery fees and trade down to private-label lines, reducing basket gross profit and pressuring contribution margins. Discounters leverage larger store estates to cross-subsidize last-mile costs, squeezing operators that rely exclusively on fees. Subscription tiers offering free delivery are spreading, but only grocers with scale can absorb the upfront revenue hit. The result is a flight to value that favors incumbents and crowds out thinly capitalized specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Model: Scheduled Windows Dominate Volume While Quick Commerce Targets Urban Premiums

Retail delivery retained 67.57% of 2025 revenue, underscoring consumer appetite for predictable slots that sync with household routines. The Europe online grocery delivery market experiences higher basket weights in this model, which amortizes last-mile costs and lifts gross contribution by 8 to 12 percentage points over rapid formats. Quick commerce, expanding at 19.43% CAGR, restricts rollout to affluent districts where shoppers pay surcharges for convenience. Platforms that narrowed geography and pushed average ticket values above EUR 25 (USD 28) reported positive unit economics by early 2026, validating a selective-density strategy. Meal-kit services, still a niche, compete by bundling recipes with proprietary ingredient packs, but face encroachment from grocers inserting ready-to-cook boxes into core assortments.

Scheduled fulfillment will continue to anchor the Europe online grocery delivery market as AI route engines raise fleet utilization, while on-demand will serve incremental missions such as forgotten dinner ingredients. Regulatory changes, notably the Platform Work Directive, inflate courier labor expense by as much as 30%, yet omnichannel retailers absorb this through cross-channel margin pools. Quick-commerce specialists must therefore maintain high density or cede ground to larger rivals that can smooth volatility across a broader cost base.

By Platform Type: Omnichannel Scale Meets Pure-Play Focus

Omnichannel operators controlled 46.32% share in 2025, monetizing store estates as micro-fulfillment grids that shrink delivery radii and unlock profitable sub-three-hour service. Their blends of transactional revenue plus advertising income elevate profitability and permit steady reinvestment in automation. Pure-play apps, set to grow at 19.63% CAGR, concentrate on a small set of markets where electric fleets and dark-store footprints already exist, limiting burn and deepening customer intimacy. The Europe online grocery delivery market size for pure-plays remains meaningful, yet consolidation is compressing the roster of competitors.

Retail-media networks represent a structural moat. Tesco and Sainsbury’s now sell audience segments built on real-time purchase behavior, generating incremental profit that rivals logistics gains. Without comparable data scale, pure-plays lean on subscription plans and tiered fees. Market watchers expect further mergers as apps seek either omnichannel partners or pan-European breadth to stay relevant.

By Product Category: Fresh Produce Accelerates As Cold-Chain Reliability Improves

Staples and cooking essentials delivered 27.31% of 2025 revenue, continuing to benefit from predictable replenishment cycles and low spoilage. IoT sensors and blockchain traceability now keep temperature excursions under 1.5%, encouraging shoppers to trial online produce for the first time. Resulting share shifts position fresh items as the fastest category at 20.12% CAGR, with organics and provenance-certified meat commanding 20-40% price premiums. This evolution enlarges the Europe online grocery delivery market share for high-margin perishable aisles.

Southern and Eastern Europe lag due to fragmented cold-chain infrastructure, yet regulatory push from the EU Farm to Fork strategy forces upgrades that level the field. Operators that control logistics end-to-end, such as Ocado and Rohlik, outcompete marketplace models that outsource fulfillment to third-party couriers. In turn, average order values climb as shoppers bundle fresh and ambient goods in a single ticket.

By Delivery Type: Instant Fulfillment Gains Urban Momentum

Scheduled windows maintained 59.63% share in 2025 because they offer superior fleet productivity. Instant services, advancing at 19.72% CAGR, require at least 15 orders per square kilometer per hour to break even, a hurdle met by fewer than 30 European cities. AI-enhanced dispatch tools integrate live traffic and weather feeds to trim cycle times, pushing average delivery below 45 minutes in core markets. The Europe online grocery delivery market responds with hybrid propositions that promise selected SKUs in under an hour and full baskets within the same day.

Regulation accelerates electrification of fleets, raising upfront capex but lowering lifetime operating costs by up to 40%. Early movers lock in supply of medium-duty electric vans and negotiate favorable charging tariffs, capturing cost advantage that lingers over late adopters. Scheduled delivery will thus remain mainstream, but instant options will define brand perception among urban digital natives.

Geography Analysis

Germany contributed 21.42% of 2025 sales, thanks to dense store networks and high disposable income. Flink’s urban focus, combined with REWE and Edeka’s click-and-collect plans, sustains two-speed growth where instant missions and weekly stock-ups coexist. The United Kingdom hosts a mature ecosystem with Tesco, Sainsbury’s, and Ocado jointly covering more than 60% of national online volume. France adds regulatory complexity via dark-store restrictions, prompting Carrefour to shift inventory to suburban hubs at higher capital cost.

Spain illustrates late-cycle acceleration, logging a 20.04% CAGR projection through 2031 as grocery e-commerce lifts from under 2% of total retail. Expansion hinges on closing cold-chain gaps and improving rural connectivity. Italy retains a click-and-collect bias because consumers favor store proximity, while the Netherlands and Czech Republic showcase profitability in mid-sized cities through app-only models like Picnic and Rohlik. Together, these dynamics reinforce the geographic mosaic that defines the Europe online grocery delivery market.

Germany sits at the epicenter of the Europe online grocery delivery market, pairing high urban density with shoppers willing to absorb service premiums. Retailers leverage more than 30,000 stores as last-mile nodes, cutting average delivery distances below eight kilometers. The United Kingdom follows closely, benefiting from a long history of online supermarket services and proprietary automation grids that hit 225 units per hour. France endures cost drag from mandatory site permits and traffic curbs, yet national coverage expands as Carrefour partners with mobility platforms to balance scale and compliance.

Spain’s digital leapfrog offers the clearest upside. Mobile-first millennials now treat grocery apps as default, exposing a largely untapped southern European opportunity. However, intense summer heat necessitates investment in refrigerated vans and insulated totes, raising entry barriers. Italy’s consumer preference for frequent, smaller trips keeps click-and-collect dominant, though rising fuel prices are nudging households toward consolidated baskets delivered to the doorstep. In Nordic and Central European markets, electric fleets thrive thanks to generous green subsidies and tighter emission zones, positioning operators such as Picnic for margin expansion.

Regulatory alignment across the EU accelerates zero-emission targets and enforces stricter worker classification, raising labor and compliance costs in the short term. Platforms with deeper balance sheets roll out electric vehicles and micro-fulfillment automation ahead of the curve, cementing leadership as regulations tighten. Smaller players may need to focus on regional niches or merge into scaled operators capable of amortizing regulatory overhead across a larger earnings base.

Competitive Landscape

The Europe online grocery delivery market features moderate fragmentation. The top five players—Tesco, Carrefour, Ahold Delhaize, Ocado, and Delivery Hero—control roughly 35-40% of regional revenue, leaving sizeable share for national champions and specialized apps. Competitive intensity shifted in 2025 toward data monetization as grocers turned loyalty programs into advertising networks. Tesco’s generative-AI studio and Sainsbury’s Pollen platform demonstrate how first-party data can yield EBITDA gains exceeding 300 basis points, funds that are redeployed into fulfillment innovation and price competitiveness.

Pure-play consolidation defines the other axis of change. DoorDash’s pending acquisition of Deliveroo and Prosus’s take-over of Just Eat Takeaway signal a new scale-driven chapter. Survivors narrow geographic scope, investing in deep density rather than surface-area expansion. Technology remains the decisive lever: Ocado’s grid automation and Picnic’s electric fleet optimization stand out as defensible advantages that lower variable costs per order.

White-space opportunities persist in mid-sized cities where density balances cost and demand. Operators exploiting in-house logistics secure incremental margin relative to those outsourcing last mile to third parties. The convergence of logistic efficiency, data-driven merchandising, and retail-media income underpins a flywheel that rewards early infrastructure bets and penalizes delayed investment.

Europe Online Grocery Delivery Industry Leaders

Flink SE

Just Eat Takeaway.com N.V.

Delivery Hero SE

Uber Technologies Inc. (Uber Eats)

Gorillas Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tesco agreed a three-year collaboration with Mistral AI to pilot hyper-personalized pricing and live route optimization across the United Kingdom.

- October 2025: Tesco introduced a generative-AI creative suite that lets brand partners build campaign assets in minutes, supporting its retail-media expansion.

- August 2025: Prosus finalized the EUR 4.1 billion (USD 4.6 billion) acquisition of Just Eat Takeaway, consolidating European food delivery under a broader portfolio.

- July 2025: Tesco deepened its partnership with LiveRamp, unlocking real-time loyalty-data targeting across multiple digital channels.

Europe Online Grocery Delivery Market Report Scope

Online Grocery Delivery is a service that allows consumers to purchase groceries—such as fresh produce, packaged foods, beverages, and household essentials—through websites or mobile apps and have them delivered to their home or a chosen location.

The Europe Online Grocery Delivery Market Report is Segmented by Delivery Model (Retail Delivery, Quick Commerce, Meal Kit Delivery), Platform Type (Pure-Play E-grocery Platforms, Multi-Category Marketplaces, Omni-Channel Retailers), Product Category (Meat and Seafood, Breakfast and Dairy Products, Snacks and Beverages, Fresh Produce, Staples and Cooking Essentials), Delivery Type (Scheduled Deliveries, Instant/On-demand Deliveries), and Country (United Kingdom, Germany, France, Spain, Italy, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Delivery Model

| Retail Delivery |

| Quick Commerce |

| Meal Kit Delivery |

By Platform Type

| Pure-Play E-grocery Platforms |

| Multi-Category Marketplaces |

| Omni-Channel Retailers |

By Product Category

| Meat and Seafood |

| Breakfast and Dairy Products |

| Snacks and Beverages |

| Fresh Produce |

| Staples and Cooking Essentials |

By Delivery Type

| Scheduled Deliveries |

| Instant/On-demand Deliveries |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By Delivery Model | Retail Delivery |

| Quick Commerce | |

| Meal Kit Delivery | |

| By Platform Type | Pure-Play E-grocery Platforms |

| Multi-Category Marketplaces | |

| Omni-Channel Retailers | |

| By Product Category | Meat and Seafood |

| Breakfast and Dairy Products | |

| Snacks and Beverages | |

| Fresh Produce | |

| Staples and Cooking Essentials | |

| By Delivery Type | Scheduled Deliveries |

| Instant/On-demand Deliveries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe online grocery delivery market in 2026?

It stands at USD 0.32 trillion and is forecast to reach USD 0.76 trillion by 2031.

Which delivery model currently dominates online grocery orders in Europe?

Scheduled retail delivery accounts for 67.57% of 2025 revenue, reflecting consumer preference for predictable time slots.

What country shows the fastest growth outlook?

Spain is projected to grow at a 20.04% CAGR through 2031 as mobile-first shoppers accelerate adoption.

How are retailers improving profitability online?

They monetize first-party data through retail-media networks, lifting EBITDA margins by up to 400 basis points.

What is the biggest logistical challenge for operators outside major cities?

Low order density inflates last-mile costs, making it hard to hit breakeven in rural and peri-urban zones.

Why is fresh produce gaining momentum online?

IoT-enabled cold-chain and blockchain traceability reduce spoilage, encouraging shoppers to trust quality and order perishable items digitally.

Page last updated on: