Laminated Busbar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laminated Busbar Market Analysis by Mordor Intelligence

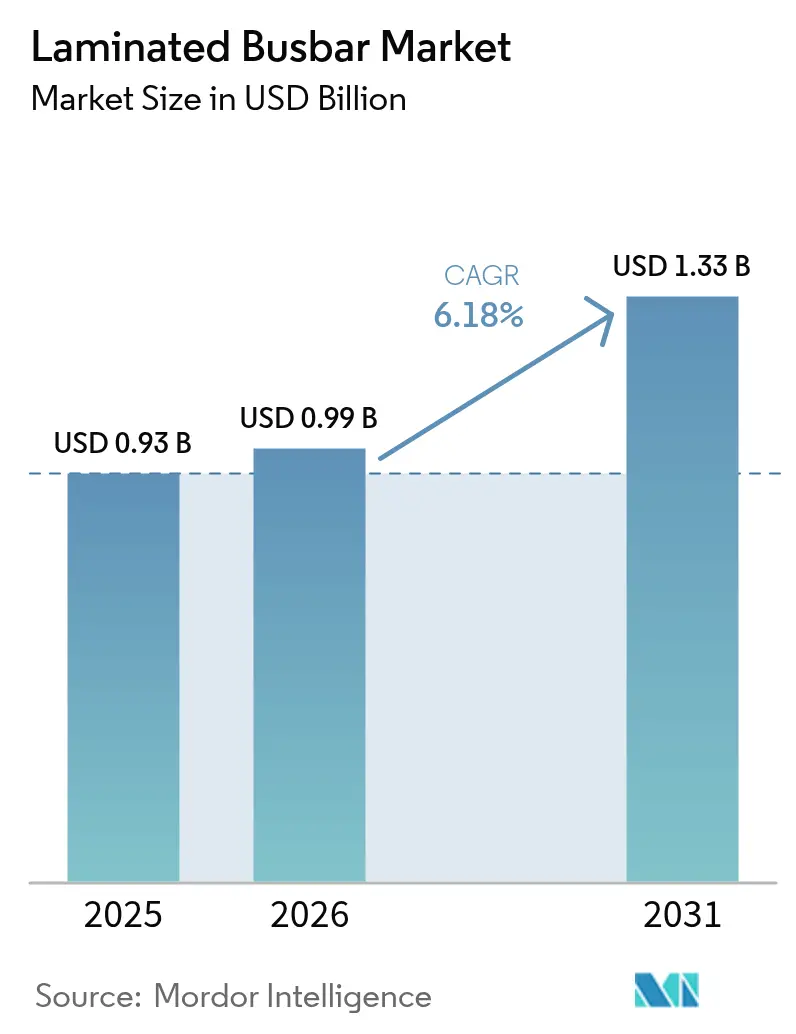

Laminated Busbar market size in 2026 is estimated at USD 987.47 million, growing from 2025 value of USD 0.93 billion with 2031 projections showing USD 1.33 billion, growing at 6.18% CAGR over 2026-2031.

Momentum comes from electrified transportation, renewable energy inverters, and high-density data center power backplanes, all of which demand compact power distribution assemblies with low inductance and high thermal efficiency. Copper remains the baseline conductor for performance-critical systems, while aluminum and hybrid metal combinations build traction in weight-sensitive applications. Supply security for raw materials and continuing advances in wide-bandgap power modules underpin new design requirements that favor laminated architectures over conventional bar or cable harnesses. Pricing pressure from volatile copper costs is partially offset by manufacturing productivity gains and the growing willingness of end users to pay a premium for enhanced safety and space savings.

Key Report Takeaways

- By conducting material, copper led with 71.05% of the laminated busbars market share in 2025, whereas aluminum is advancing at an 7.85% CAGR through 2031.

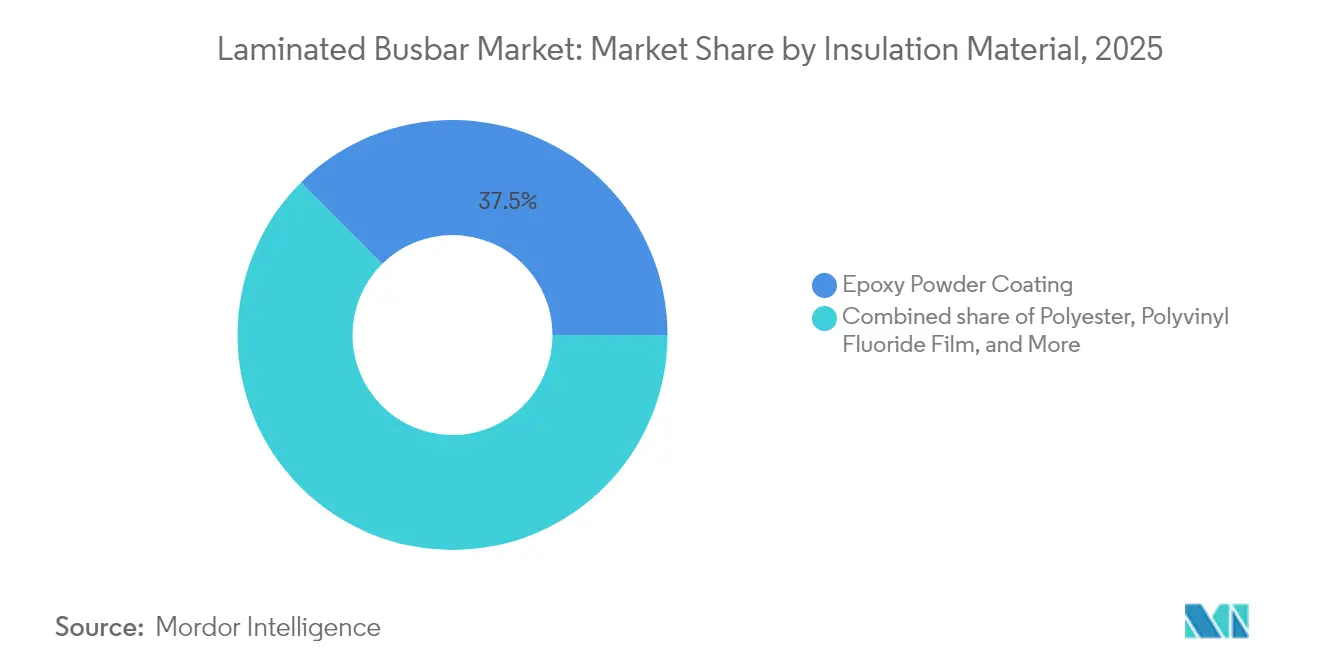

- By insulation material, epoxy coatings accounted for 37.45% revenue share of laminated busbar market in 2025; polyester films are projected to expand at a 7.55% CAGR to 2031.

- By busbar configuration, 3–5-layer products commanded 52.10% share of the laminated busbars market size in 2025, while flexible/thin formats are growing at a 9.15% CAGR.

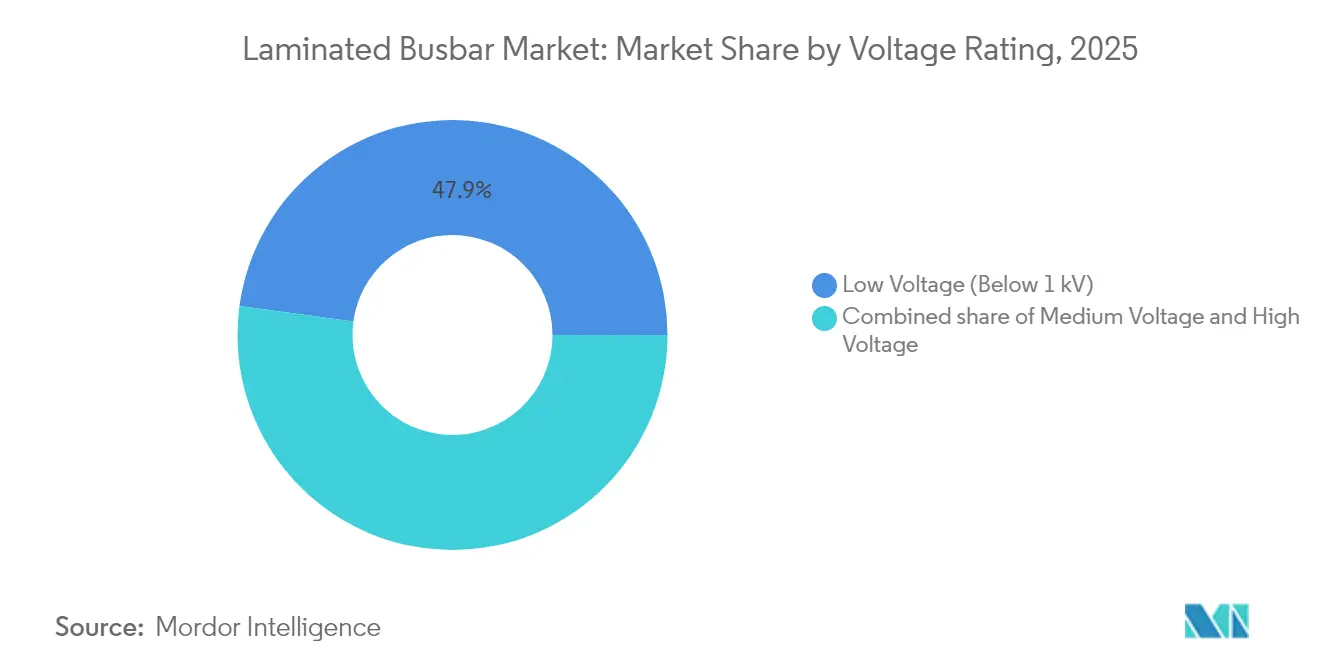

- By voltage rating, low-voltage (<1 kV) designs captured a 47.85% share of the laminated busbars market size in 2025 and are projected to grow at an 8.35% CAGR.

- By application, renewable-energy inverters held a 42.55% market share of the laminated busbars market in 2025; electric and hybrid vehicles are expected to exhibit the fastest CAGR of 14.8% through 2031.

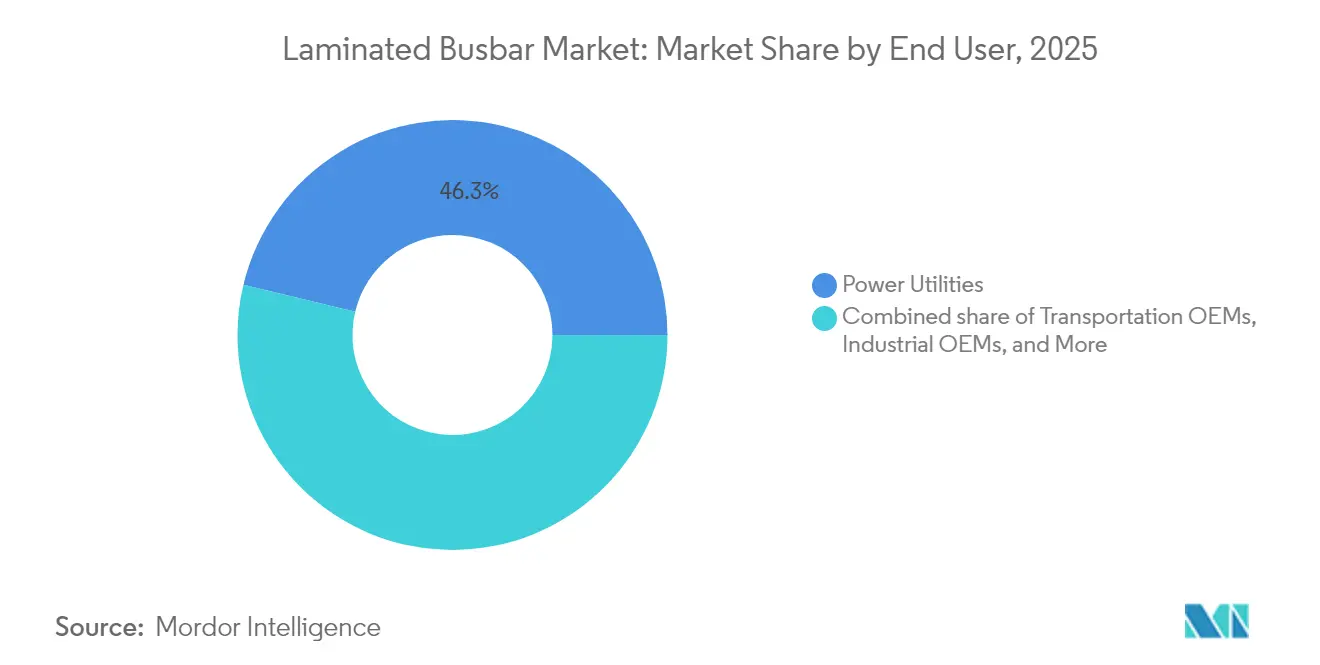

- By end user, power utilities held 46.25% of revenue in 2025, whereas transportation OEMs are forecast to rise at a 11.9% CAGR, in the laminated busbar market.

- By geography, The laminated busbar market in Asia-Pacific region led with a 40.95% market share in 2025 and is forecasted to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Laminated Busbar Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV & HEV proliferation | 1.80% | Global; strongest in APAC and North America | Medium term (2-4 years) |

| Renewable-energy inverter roll-outs | 1.20% | Global; concentrated in APAC and Europe | Long term (≥4 years) |

| Data-center power-backplane demand spike | 1.10% | North America & EU; expanding to APAC | Short term (≤2 years) |

| Industrial electrification and automation | 0.90% | Global; factory hubs in APAC | Medium term (2-4 years) |

| SiC/GaN-based high-voltage module adoption | 0.80% | North America & EU; spillover to APAC | Long term (≥4 years) |

| Modular eVTOL battery-pack architectures | 0.60% | North America & EU early adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV & HEV Proliferation Drives Compact Power Solutions

Automakers are accelerating the adoption of laminated busbars to reduce battery-pack footprints and improve thermal performance. Tesla’s structural battery and BYD’s blade format demonstrate how laminated conductors reduce assembly complexity by 40% while maintaining high current density.[1] Aluminum-copper hybrids produced via cold-cladding now combine weight savings with conductivity, and ultrasonic welding, along with silver coatings, resolve aluminum oxidation hurdles. Vehicle platforms shifting to 400 V–800 V systems require flexible busbar geometries that accommodate changing cell chemistries without compromising safety margins. The cascading effect is a broadened supply base, with materials specialists and tier-one integrators vying for long-term supply awards, boosting the laminated busbar market.

Renewable-Energy Inverter Roll-outs Expand Grid Integration

Solar and wind OEMs specify laminated busbars for low-inductance, high-current inverter stages. SiC and GaN switches now operate well past 50 kHz, and laminated geometries cut stray inductance by up to 90%, improving conversion efficiency and enabling bidirectional power flow in storage-combined assets.[2] Standardized interfaces simplify the swapping of energy-storage modules, while embedded sensors enable predictive maintenance that prevents inverter downtime in utility-scale parks, further expanding the laminated busbar market.

Data-Center Power-Backplane Demand Spike

Hyperscale facilities push rack loads past 40 kW, creating the need for 48 V DC architectures distributed via laminated busbars that minimize voltage drop. Rogers Corporation’s ROLINX offerings integrate liquid-cooling plates that stabilize the voltage rails of AI accelerators. Edge sites mirror these needs on a smaller footprint, driving demand for modular, quick-install busbar kits. Thermal design parity with server cold-plate loops further differentiates laminated solutions from legacy cable whips, strengthening the laminated busbar market.

Industrial Electrification & Automation Surge

Industry 4.0 plants require compact motor-drive cabinets with reduced arc-flash risk. Laminated busbars comply with IEC safety standards and enable the quick reconfiguration of automated lines.[3] Real-time current monitoring, inserted directly into the conductor stack, underpins predictive maintenance programs that minimize unplanned machine stops. The shift from pneumatic to electric actuation broadens the installed base of drives needing low-impedance power rails, supporting growth in the laminated busbar market.

Restraints Impact Analysis of Laminated Busbar Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper & aluminum prices | -0.40% | Global; most acute in production hubs | Short term (≤2 years) |

| Low-cost conventional busbars as substitutes | -0.30% | Emerging markets, cost-sensitive sectors | Medium term (2-4 years) |

| Heat-dissipation & delamination >1 kV | -0.20% | High-voltage uses worldwide | Long term (≥4 years) |

| Aerospace qualification burden | -0.10% | North America & EU aerospace supply chain | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper & Aluminum Prices

Copper reached USD 6.20 per pound in July 2024, prompting component suppliers to increase their price lists by up to 45%, as raw materials account for up to 70% of the cost.[4]“Commodity Metal Cost Update,” LAPP Tannehill, lapptannehill.com Multi-year inverter or grid contracts limit pass-through ability, eroding margins. Aluminum swings add another layer of uncertainty just as hybrids gain share. Some OEMs hedge their bets with long-term supply agreements or explore copper-clad aluminum conductors that reduce exposure without compromising conductivity.

Heat-Dissipation & Delamination Beyond 1 kV

Voltage above 1 kV increases insulation-stress levels, where thermal cycling can spark delamination, corona inception, and partial discharge. Epoxy and polyimide stacks must strike a balance between dielectric strength and heat flow restrictions. Precision lamination, void-free curing, and non-destructive inspection become mandatory. Condition-monitoring circuits embedded in the laminate alert operators before insulation breakdown, but cost premiums slow uptake in price-sensitive grids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Laminated Busbar Market Segment Analysis

By Conducting Material:

Copper Leads, Aluminum ScalesCopper captured 71.05% of the laminated busbars market share in 2025, driven by its unmatched conductivity and mature processing routes. This dominance is anchored by high-power inverters and battery packs that cannot compromise on resistive losses or heat rise. However, aluminum sections are expected to accelerate at an 7.85% CAGR as vehicle OEMs trade density for weight savings and achieve a 40% reduction in raw-material costs. Cold-clad bimetal strip from Samuel Taylor and similar suppliers enables jointless aluminum-copper interfaces that maintain current paths and mechanical integrity. As a result, specification engineers increasingly approve hybrids for 800 V traction inverters and charging modules, reshaping bill-of-materials norms.

Aluminum adoption forces insulation labs to rethink dielectric thickness for lower melting-point conductors, while silver-flash or nickel-plate coatings extend mating-surface life. Weight-optimized rail designs trim pack mass in long-range EVs, unlocking extra kilowatt-hours or payload. Suppliers targeting the laminated busbars industry invest in ultrasonic welding lines and automated quality control to guarantee consistent clad integrity across large production batches.

By Insulation Material:

Epoxy Retains Pole, Films Gain MomentumEpoxy powder coating accounted for 37.45% of the revenue in 2025 by combining robust mechanical protection with low per-part costs, making it the default choice for switchgear and factory automation cabinets. Yet polyester and polyimide films are gaining traction at a 7.55% CAGR because thinner stacks translate to lower inductance and better thermal pathways. Specialty films withstand the rapid temperature swings commonly seen in SiC traction modules, supporting junction temperatures exceeding 175°C without cracking.

Film laminates enable busbars under 2 mm thick that snake through cramped battery-pack cavities. Heat-resistant fiber reinforcements and ceramic fillers raise breakdown voltage while maintaining flexibility. Environmental, health, and safety teams also note that newer solvent-free film adhesives lower volatile organic compound emissions in production, advancing corporate sustainability targets without sacrificing product lifespan.

By Busbar Configuration:

Multi-Layer Dominates, Flex Steals GrowthThree- to five-layer designs accounted for 52.10% of the laminated busbars market size in 2025, offering engineers a balanced mix of current-carrying cross-sections and manageable assembly steps. These stacks route positive, negative, and sense lines in compact footprints, delivering inductance steps of less than 10 nH for many inverter layouts. Flexible or thin laminates, however, are outpacing the aggregate market at 9.15% CAGR, addressing vibration-prone e-mobility and aerospace cabins where rigid bars risk fatigue.

Flex designs utilize thin copper foil or aluminum sheets, combined with high-temperature adhesive, to fold around modules or contour battery cells. Advanced lamination presses and laser-assisted cutting enable the creation of complex shapes without compromising insulation gaps. Meanwhile, six-layer constructions serve megawatt EV chargers and utility STATCOM boards that require parallel copper planes for heat dissipation and EMI cancellation.

By Voltage Rating:

Low-Voltage Focus Fuels ScaleLow-voltage assemblies below 1 kV accounted for 47.85% of the laminated busbars market size in 2025 and are expected to post an 8.35% CAGR as EV drivetrains, 48 V server racks, and decentralized DC microgrids proliferate. These designs utilize thinner insulation and a higher permissible current density per square millimeter compared to their medium-voltage peers. Medium-voltage (1-35 kV) remains the workhorse for industrial drives and renewable energy transformers, while segments above 35 kV grow slowly because certification and safety audits extend project lead times.

Busbar makers serving data-center developers increasingly quote 48V backplane kits with quick-lock fasteners, halving installation cycles. Conversely, medium-voltage stacks incorporate thicker ceramic-filled epoxies to tame partial discharge. High-voltage prototypes draw on aerospace insulation expertise, yet they await economies of scale before widespread adoption.

By Application:

Renewable Energy Holds Lead, EVs AccelerateRenewable-energy inverters accounted for 42.55% of the laminated busbars market share in 2025, thanks to mature demand in solar farms and offshore wind converters. These projects value laminated pathways that minimize inductance in multi-megawatt string inverters and grid-interface STATCOMs. Electric and hybrid vehicles now represent the fastest-growing segment, with a 14.8% CAGR, driven by aggressive production targets and increasingly larger battery packs. Traction inverters, onboard chargers, and DC-link capacitors each require bespoke conductor layouts, encouraging suppliers to standardize on modular building blocks.

Data-center racks, industrial motor drives, and mass-transit rolling stock continue to experience steady double-digit growth as digitalization and electrification expand globally. Aerospace and eVTOL opportunities remain niche but premium, with stringent certification driving high-margin specialty designs that serve as technology showcases.

By End User:

Utilities Anchor, Transportation SurgesPower utilities retained 46.25% revenue share in 2025 because sub-station switchgear and inverter stations historically favored laminated solutions for heat-rise control. Utility demand remains resilient as grid-modernization spending escalates and energy-storage systems proliferate. Transportation OEMs, including automotive and aviation, will experience a 11.9% CAGR to 2031, reflecting the wholesale shift to electrified platforms.

Industrial OEMs deploy busbars in servo-driven automation, while residential and commercial installers adopt plug-and-play low-voltage busways for energy-storage cabinets. Each user group values rapid installation, reduced maintenance, and higher safety margins relative to bare-bar iterations, reinforcing laminated uptake across verticals.

Geography Analysis

APAC Laminated Busbar Market

The Asia-Pacific region dominated the laminated busbars market in 2025, with a 40.95% share, and is expected to expand at a 7.2% CAGR as vertically integrated supply chains in China, Japan, and South Korea compress lead times and reduce costs. The laminated busbars market size in the region benefits from large-volume EV production lines that secure multiyear busbar contracts tied to battery-pack ramps. India accelerates renewable-energy inverter deployment, adding further pull for regional lamination capacity.

North America Laminated Busbar Market

North America ranked second, driven by hyperscale data-center retrofits and ambitious automotive electrification timelines. Tesla’s structural battery programs alone create recurring demand spikes for custom conductor layouts, while 48V rack conversions in cloud campuses secure steady orders for pre-engineered backplane kits. Federal incentives to localize critical-component manufacturing add momentum to US-based lamination investments.

Europe Laminated Busbar Market

Europe relies on stringent environmental directives and industry automation to maintain steady adoption. Wind-energy OEMs rely on busbars that pair with SiC power modules in offshore converter stations, whereas German machine-tool makers retrofit factory panels with laminated boards to shrink cabinet footprints. Regional suppliers differentiate through low-carbon copper sourcing and cradle-to-grave recycling programs, resonating with EU sustainability goals.

Competitive Landscape

The laminated busbars market is moderately fragmented, with a balance of long-standing conglomerates and niche innovators. Eaton, Rogers Corporation, and Mersen sustain broad product portfolios that cater to utility and industrial customers, leveraging worldwide distribution footprints. Eaton’s 2025 agreement to acquire Resilient Power Systems advances its solid-state transformer roadmap, solidifying the group’s presence in the EV charging and energy storage domains. Rogers Corporation continues to foreground ROLINX technology with integrated thermal plates, targeting AI-heavy data center racks.

Specialist houses focus on SiC/GaN module attachment, thin-film insulation, and ultra-flexible aluminum conductors, carving out high-margin segments in eVTOL prototypes and next-generation traction inverters. Legrand’s entry into North American data-center busbars through its 2025 Power Bus Way acquisition illustrates how electrical infrastructure giants seek adjacency growth. Simultaneously, semiconductor vendors venture downstream; Amphenol’s USD 2.025 billion acquisition of Carlisle Interconnect Technologies adds depth in harsh-environment power distribution.

Product differentiation hinges on thermal performance, conductor bend radius, and embedded monitoring. Competitors race to certify polyimide-based insulation stacks for 200°C junctions, aiming to secure a multi-year supply during the early rollouts of SiC/GaN. Supply-chain resilience gains importance as copper price shocks and geopolitical events disrupt raw-metal flows, prompting strategic stockpiles and localized plating capacity investments.

Laminated Busbar Industry Leaders

Methode Electronics Inc.

Rogers Corporation

Mersen SA

Sun.King Power Electronics Group Ltd.

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Laminated Busbar Market Companies Covered in this Report

- Eaton Corporation plc

- Rogers Corporation

- Mersen SA

- Methode Electronics Inc.

- Amphenol Corporation

- Molex LLC

- Sun.King Power Electronics Group Ltd

- Zhuzhou CRRC Times Electric Co., Ltd

- Storm Power Components

- Segue Electronics Inc.

- EMS Industrial & Service Company

- Ryoden Kasei Co., Ltd

- Shanghai Eagtop Electronic Technology Co., Ltd

- Suzhou West Deane Machinery Inc.

- Raychem RPG Private Limited

- Zhejiang RHI Electric Co., Ltd

- Electronic Systems Packaging LLC

- Idealec SAS

- Advanced Energy Industries, Inc.

- Delta Electronics, Inc.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Littelfuse Inc.

Recent Industry Developments in Laminated Busbar Market

- July 2025: Eaton agreed to acquire Resilient Power Systems Inc., a specialist in solid-state transformers focused on the EV and data center markets, with the closing slated for Q3 2025.

- May 2025: Legrand purchased Power Bus Way, a cable-bus supplier generating EUR 70 million in annual revenue, marking its first North American data center acquisition.

- March 2025: Eaton signed a USD 1.4 billion deal to acquire Fibrebond Corporation, targeting modular power enclosures for multi-tenant data centers.

- October 2024: Eaton reported record Q3 2024 earnings of USD 2.53 per share on USD 3.0 billion Electrical Americas sales, up 14% year-over-year.

Global Laminated Busbar Market Report Scope

The laminated busbar market report includes:

Segmentation Overview

| Copper |

| Aluminum |

| Hybrid (Cu-Al composite) |

| Epoxy Powder Coating |

| Polyvinyl Fluoride Film |

| Polyester |

| Heat-Resistant Fiber |

| Polyimide/Kapton |

| Others |

| Multi-layer (3 to 5 layers) |

| High-layer (More Than 5 layers) |

| Flex/Thin busbars |

| Low Voltage (Below 1 kV) |

| Medium Voltage (1 to 35 kV) |

| High Voltage (Above 35 kV) |

| Electric and Hybrid Vehicles |

| Renewable Energy (Solar, Wind, ESS) |

| Data Centers and Cloud Infrastructure |

| Industrial Drives and Machinery |

| Rail and Mass Transit |

| Aerospace and eVTOL |

| Power Utilities |

| Industrial OEMs |

| Transportation OEMs |

| Residential and Commercial Construction |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germnay |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Conducting Material | Copper | |

| Aluminum | ||

| Hybrid (Cu-Al composite) | ||

| By Insulation Material | Epoxy Powder Coating | |

| Polyvinyl Fluoride Film | ||

| Polyester | ||

| Heat-Resistant Fiber | ||

| Polyimide/Kapton | ||

| Others | ||

| By Busbar Configuration | Multi-layer (3 to 5 layers) | |

| High-layer (More Than 5 layers) | ||

| Flex/Thin busbars | ||

| By Voltage Rating | Low Voltage (Below 1 kV) | |

| Medium Voltage (1 to 35 kV) | ||

| High Voltage (Above 35 kV) | ||

| By Application | Electric and Hybrid Vehicles | |

| Renewable Energy (Solar, Wind, ESS) | ||

| Data Centers and Cloud Infrastructure | ||

| Industrial Drives and Machinery | ||

| Rail and Mass Transit | ||

| Aerospace and eVTOL | ||

| By End-User | Power Utilities | |

| Industrial OEMs | ||

| Transportation OEMs | ||

| Residential and Commercial Construction | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germnay | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the laminated busbars market growth through 2031?

The primary catalysts are EV battery-pack expansion, renewables inverter installations, and data-center power upgrades that need compact, low-inductance power rails delivering higher efficiency and safety.

How big will the laminated busbars market be by 2031?

The laminated busbars market size is projected to reach USD 1.33 billion by 2031, up from USD 987.47 million in 2026 at a 6.18% CAGR over 2026-2031.

Which region leads global demand?

Asia-Pacific holds 40.95% of laminated busbars market share and is expected to maintain leadership due to strong EV production, renewable-energy projects, and integrated metal-processing supply chains.

Why are aluminum busbars gaining popularity?

Aluminum offers roughly 40% cost savings and significant weight reduction compared to copper; new clad and coating technologies now mitigate prior conductivity and oxidation drawbacks.

What application segment is growing fastest?

Electric and hybrid vehicles show the highest growth, forecast at a 14.8% CAGR because laminated busbars streamline battery-pack architecture and improve thermal performance.

How does copper price volatility affect suppliers?

Copper represents up to 70% of production cost; recent price spikes force manufacturers either to raise prices or shift toward hybrid and aluminum-based designs to protect margins.

Page last updated on: