Global Diabetic Retinopathy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

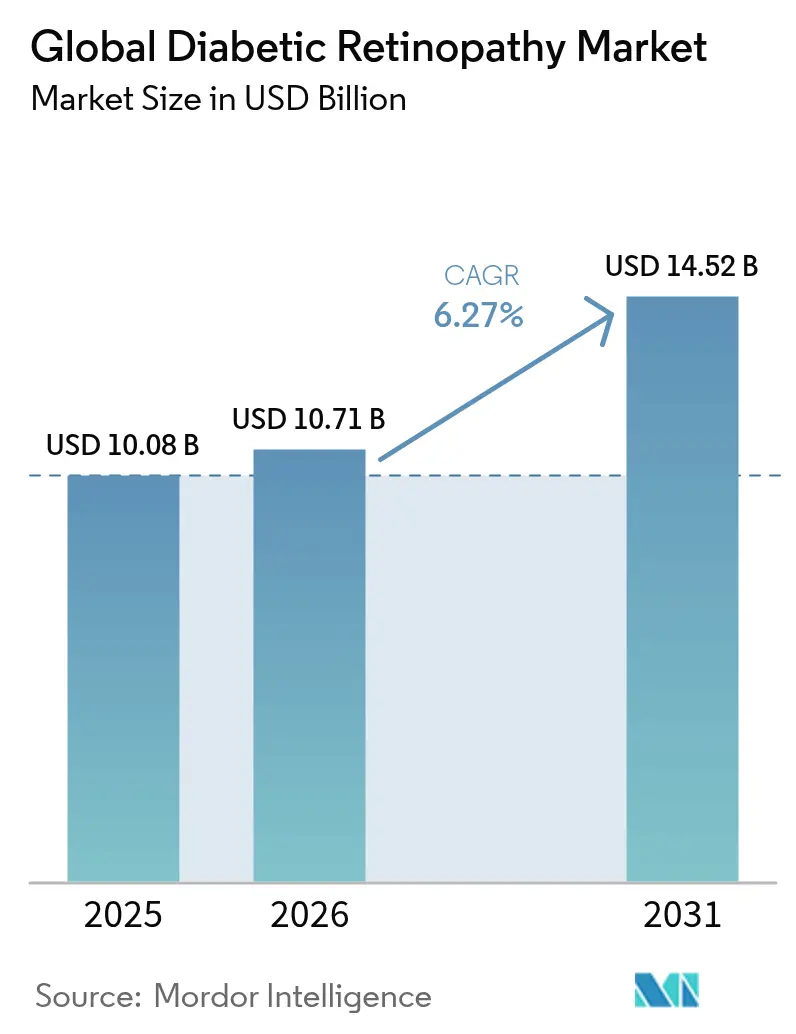

| Market Size (2026) | USD 10.71 Billion |

| Market Size (2031) | USD 14.52 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Diabetic Retinopathy Market Analysis by Mordor Intelligence

The diabetic retinopathy market size is expected to grow from USD 10.08 million in 2025 to USD 10.71 million in 2026 and is forecast to reach USD 14.52 million by 2031 at 6.27% CAGR over 2026-2031. Growth stems from the rising global diabetes burden, rapid uptake of AI-enabled screening, and broader therapeutic choices that now include sustained-release biologics and pipeline gene therapies. Aging populations amplify demand, with nearly 10 million patients in the United States and more than 100 million worldwide living with some form of diabetic retinopathy. North America retains leadership on the strength of advanced health systems, while Asia-Pacific shows the fastest gains as tele-ophthalmology programs scale across large diabetic populations. Competitive intensity rose sharply in 2024 when five aflibercept biosimilars entered the United States, triggering price competition and widening patient access.

Key Report Takeaways

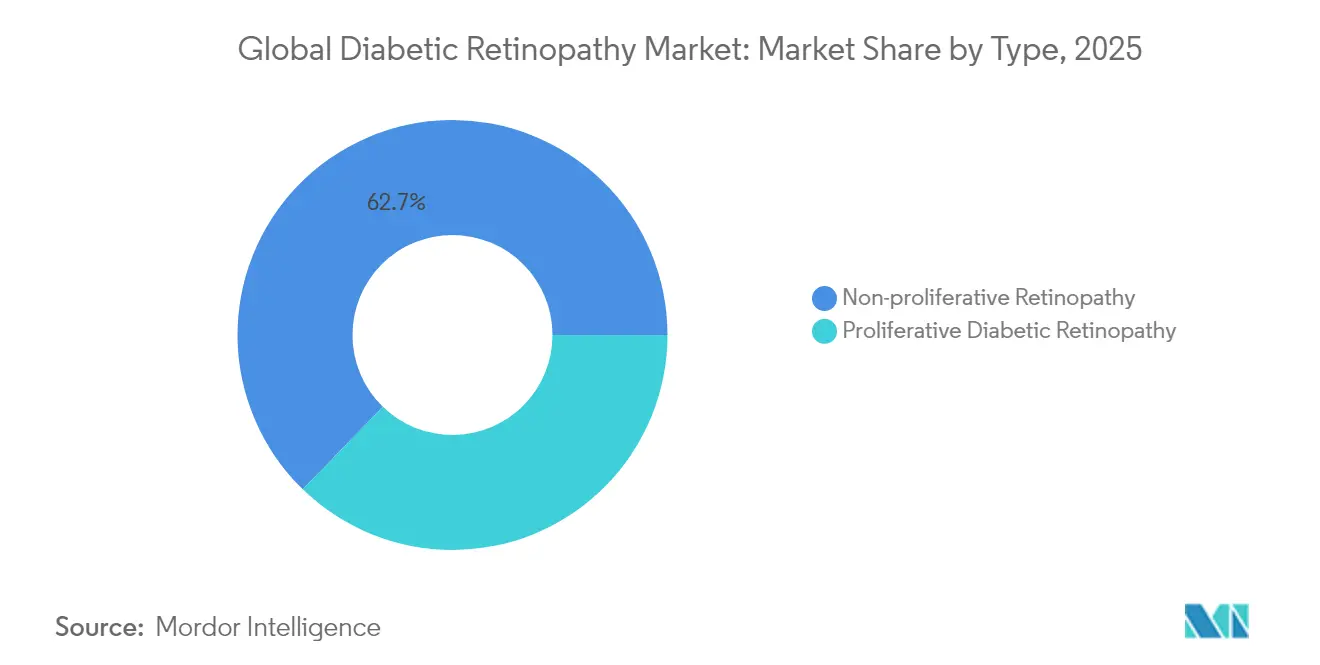

- By disease stage, non-proliferative retinopathy held 62.74% of diabetic retinopathy market share in 2025, whereas proliferative disease is forecast to grow at 7.12% CAGR through 2031.

- By management approach, anti-VEGF agents commanded 55.62% share of the diabetic retinopathy market size in 2025; vitrectomy is projected to advance at 7.88% CAGR between 2026 and 2031.

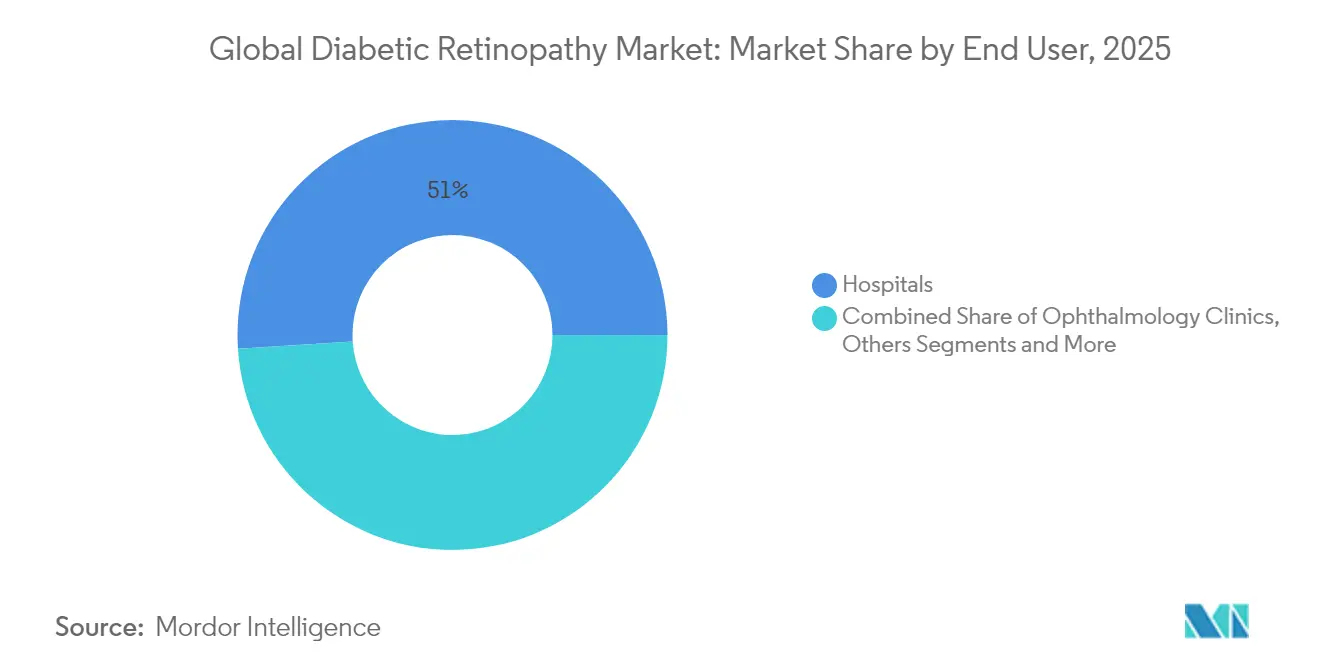

- By end-user, hospitals led with 51.02% revenue share in 2025, while ophthalmology clinics are set to expand at 7.43% CAGR to 2031.

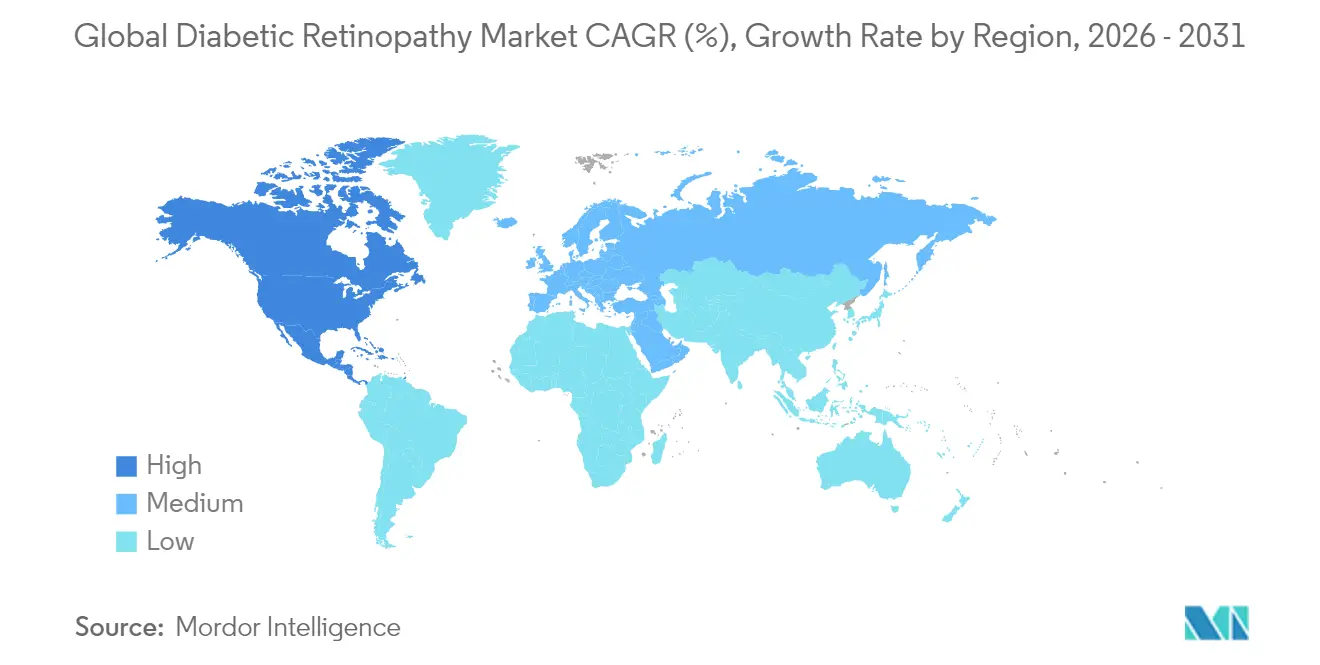

- By geography, North America captured 42.98% of the diabetic retinopathy market in 2025; Asia-Pacific is expected to post the highest regional CAGR of 7.95% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diabetic Retinopathy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Diabetes Prevalence & Earlier Screening | +1.8% | Global, with highest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Aging Population Increasing Vision-Threatening Cases | +1.2% | North America & EU, spill-over to developed Asia-Pacific | Long term (≥ 4 years) |

| Expanding Indications & Reimbursement For Long-Acting Anti-VEGF Biologics | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| AI-Enabled Retinal Screening Adoption In Primary Care Clinics | +0.9% | Global, early gains in North America, Asia-Pacific adoption | Medium term (2-4 years) |

| Growth Of Tele-Ophthalmology Programs In Low-Resource Regions | +0.7% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Venture Funding In Regenerative Cell & Gene Therapies For DR | +0.4% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Diabetes Prevalence & Earlier Screening

International Federation of Diabetes data foresee 12% of the world’s adults living with diabetes by 2045, enlarging the treatable pool for the diabetic retinopathy market [1]International Diabetes Federation, “IDF Diabetes Atlas,” idf.org. Meta-analyses confirm disease rates above 22% in multiple screening programs, underlining a consistent burden across regions. AI tools that deliver 92-93% sensitivity now detect micro-aneurysms at routine primary-care visits, shifting diagnosis to earlier, more treatable stages. Chile’s national tele-ophthalmology network cut specialist referrals to 15% while preserving coverage, showing scalable early detection in lower-resource settings.

Aging Population Increasing Vision-Threatening Cases

Patients with more than 10 years of diabetes carry 4.36-fold higher odds of retinopathy, and most are over 60 years old. China reports prevalence between 24.7% and 43.1%, highlighting the aging-duration nexus in the region. Female patients have shown bigger increases in blindness, suggesting the need for gender-specific care strategies. Vitrectomy demand mirrors these trends, expanding 8.14% annually as elderly patients present with complex proliferative disease.

Expanding Indications & Reimbursement for Long-Acting Anti-VEGF Biologics

Five U.S. aflibercept biosimilars secured FDA approval in 2024, creating downward price pressure and broader payer coverage. Genentech’s Susvimo received clearance for continuous delivery with two refills a year, and Regeneron’s Eylea HD is under priority review for longer dosing intervals, both directly addressing the 46% break-off rate seen in diabetic macular edema.

AI-Enabled Retinal Screening Adoption in Primary-Care Clinics

AEYE Health won FDA clearance for the first fully autonomous AI algorithm that needs only one image per eye, achieving 99% imageability and over 92% sensitivity. Less than 5% of U.S. diabetics accessed AI screening between 2019-2023, leaving substantial headroom for expansion. India’s plan to scan 1 billion eyes over 10 years illustrates the scalability of AI combined with low-cost handheld cameras. Real-world Czech data show AI outperforms general ophthalmologists in sensitivity while raising follow-up adherence by 89%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Retinal Specialists In Emerging Markets | -1.1% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| High Treatment Burden & Poor Adherence To Injection Regimens | -0.8% | Global, with highest impact in elderly populations | Medium term (2-4 years) |

| Delayed Regulatory Pathways For First-In-Class Biosimilars | -0.6% | Global, with early impact in North America and Europe | Short term (≤ 2 years) |

| Limited Real-World Evidence For Novel Combination Therapies | -0.4% | Global, concentrated in developed markets with advanced healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Retinal Specialists in Emerging Markets

The United States is projected to face a 12% fall in ophthalmologist supply versus a 24% rise in demand by 2035, and rural counties may meet only 26-29% of their staffing need [2]American Academy of Ophthalmology, “Ophthalmologist Workforce Projections,” aaojournal.org . Asia-Pacific shows even sharper gaps as diabetic prevalence climbs faster than specialist training, prompting governments to fund telemedicine hubs and AI triage to extend reach. Arkansas illustrated scalable coverage using statewide teleretinal screening linked to urban retina centers, an approach now copied in Latin America and South Asia.

High Treatment Burden & Poor Adherence to Injection Regimens

Real-world audits find 46% of diabetic macular edema patients discontinue anti-VEGF therapy at least once, twice the dropout seen in age-related macular degeneration. Monthly office visits, cost, and co-morbidities all undermine adherence. Continuous delivery reservoirs such as Susvimo, extended-interval Eylea HD, and one-time RGX-314 gene therapy aim to relieve this burden and are already showing superior durability in trials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Proliferative Dominance Drives Early Intervention

Non-proliferative disease accounted for 62.74% diabetic retinopathy market share in 2025, underscoring the impact of screening that now captures pathology earlier. AI systems detecting subtle micro-aneurysms push more patients into preventive care pathways rather than late-stage surgery. Proliferative cases, although smaller, will rise at 7.12% CAGR as aging and disease duration fuel advanced pathology, expanding demand for surgery and regenerative therapies.

Clinical management differs sharply. Non-proliferative patients benefit from systemic agents such as fenofibrate, which cut progression by 27% in trials. Proliferative disease increasingly involves vitrectomy, the fastest-growing modality at 7.88% CAGR. Early gene therapy data show 2-step DRSS improvement in 20% of treated non-proliferative patients, suggesting future disease-stage-specific regimens. The diabetic retinopathy market size for proliferative interventions is projected to outpace overall growth despite the segment’s current smaller base.

By Management Approach: Anti-VEGF Leadership Faces Sustained-Release Disruption

Anti-VEGF drugs held 55.62% of the diabetic retinopathy market size in 2025 on entrenched physician familiarity and wide-ranging guideline support . The segment is pivoting toward durability. Susvimo’s reservoir requires two refills a year, and Vabysmo offers dual-pathway inhibition, both carving share from monthly injectables.

Vitrectomy volume will expand fastest at 7.88% CAGR as surgeons treat complex tractional detachments in proliferative disease, with Japan reporting 97.3% single-surgery success. Steroid implants fill a niche for inflammation-driven edema, lowering injection frequency from 4.7 to 1.4 annually. Laser photocoagulation remains useful in combination protocols; meta-analyses show ranibizumab plus laser yields better vision than monotherapy in select cases. Overall, the diabetic retinopathy market continues to shift from frequent injections toward longer-lasting biologics, surgery, and, eventually, one-time gene therapy.

By End-User: Hospital Dominance Shifts Toward Specialized Clinic Growth

Hospitals commanded 51.02% share of the diabetic retinopathy market in 2025 thanks to operating-room access for vitrectomy and multi-disciplinary management of co-morbidities. Procedure-heavy proliferative cases solidify hospital strength, yet cost pressures encourage migration to outpatient settings.

Ophthalmology clinics will grow at 7.43% CAGR, boosted by consolidation that creates nationwide retinal care networks, such as Cencora’s USD 5.1 billion purchase of Retina Consultants of America. Ambulatory surgical centers gain momentum as sustained-release devices like Susvimo can be implanted in minor-procedure suites. AI screening now launches in primary-care offices, routing positive cases to clinic-based retina specialists, broadening the referral funnel. These shifts produce a more distributed care model while maintaining hospital dominance for the most complex surgeries.

Geography Analysis

North America captured 42.98% of diabetic retinopathy market share in 2025, supported by early adoption of FDA-cleared AI devices, fast biosimilar uptake, and generous payer coverage. The region hosts 71.15% of global diabetic eye research publications from 2012-2021, reinforcing its innovation leadership. A looming 30% shortfall in ophthalmologist supply by 2035 tempers growth, particularly in rural areas, and fuels demand for tele-retina solutions.

Asia-Pacific is expected to grow at 7.95% CAGR through 2031, the highest of all regions, propelled by diabetes incidence and large population bases. China’s diabetic retinopathy prevalence up to 43.1% among diabetics underscores the region’s unmet need. India’s plan to screen 1 billion eyes with AI-enabled handheld cameras highlights large-scale digital health adoption. Government reimbursement expansion and rising medical tourism further spur growth.

Europe demonstrates steady growth on the strength of robust universal health systems and swift biosimilar integration. Latin America leverages tele-ophthalmology, exemplified by Chile’s network that detects retinopathy in 22% of screened diabetics while cutting unnecessary referrals. The Middle East and Africa remain nascent but attractive due to high diabetes prevalence in Gulf states and incremental investment in specialty care infrastructure.

Competitive Landscape

The diabetic retinopathy market shows moderate consolidation. Top participants include Genentech (Susvimo, ranibizumab biosimilars), Regeneron (Eylea, Eylea HD), Roche (Vabysmo), Novartis (Beovu), Bayer, AbbVie/REGENXBIO (RGX-314), and emerging biosimilar developers. Five aflibercept biosimilars approved in 2024—Yesafili, Opuviz, Enzeevu, Pavblu, and one unbranded—apply price pressure yet widen access.

Differentiation now centers on durability. Susvimo’s port-delivery system and Eylea HD’s extended intervals are setting new treatment expectations. Roche’s Vabysmo leveraged dual inhibition to reach 847 million Swiss francs in Q1 2024 sales, proving rapid physician adoption.

M&A and partnerships reshape service delivery. Cencora’s acquisition of Retina Consultants of America builds a national clinic platform, while AEYE Health pairs with Optomed to commercialize AI-enabled handheld cameras. Gene therapy represents the next competitive frontier; RGX-314’s Phase 3 program aims to establish a one-time treatment that could shift future share dynamics.

Global Diabetic Retinopathy Industry Leaders

Regeneron Pharmaceuticals, Inc.

Alimera Sciences

Oxurion NV.

Abbvie Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FDA approved Genentech’s Susvimo for diabetic retinopathy, the first continuous-delivery therapy requiring one refill every nine months after positive Pavilion study results.

- April 2025: Vantage dosed its first subject in a Phase II diabetic retinopathy trial exploring an innovative therapeutic candidate.

- January 2025: AbbVie and REGENXBIO announced plans to start Phase 3 trials of RGX-314 gene therapy using the SCS Microinjector system for one-time treatment.

- May 2024: AEYE Health and Optomed secured FDA clearance for the Optomed Aurora handheld fundus camera with integrated AI for autonomous screening.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global diabetic retinopathy market as the yearly revenue generated by therapeutic and surgical interventions, namely anti-VEGF biologics, intra-ocular steroids, laser photocoagulation, and vitrectomy, administered to patients diagnosed with non-proliferative or proliferative diabetic retinopathy across all care settings. We also capture procedure-linked consumables whenever their cost is inseparable from the intervention fee.

(Exclusion) Screening devices, standalone diagnostic software, and glucose-monitoring products fall outside this scope, ensuring our numbers reflect treatment demand only.

Segmentation Overview

- By Type

- Proliferative Diabetic Retinopathy

- Non-proliferative Retinopathy

- By Management Approach

- Anti-VEGF Drug

- Intraocular Steroid Injection

- Laser Surgery

- Vitrectomy

- By End-user

- Hospitals

- Ophthalmology Clinics

- Ambulatory Surgical Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed retina specialists, hospital pharmacy leads, and payer gatekeepers across North America, Europe, Asia-Pacific, and Latin America. Their insights refined treated population shares, typical dosage patterns, off-label steroid use, and price corridors, allowing us to reconcile secondary estimates with real-world practice.

Desk Research

Mordor analysts began with a structured scan of authoritative, open-access sources such as the International Diabetes Federation's prevalence dashboards, the World Health Organization's blindness burden files, and regional ophthalmology associations that disclose treated case volumes. National health insurance claims portals, customs import tallies for anti-VEGF vials, and peer-reviewed journals in PubMed supplied procedure counts and adherence ratios.

Those inputs were enriched through filings and investor decks from leading biologics manufacturers, patent activity retrieved via Questel, and sales splits drawn from D&B Hoovers. Additional context on hospital capacity and reimbursement ceilings came from government budget documents and Dow Jones Factiva news archives. The list above is illustrative; many other public and paid references informed desk validation.

Market-Sizing & Forecasting

A top-down model converts diagnosed diabetes prevalence into a DR patient pool, applies region-specific progression rates, and then layers treatment penetration by modality. Supplier roll-ups and sampled average selling prices provide bottom-up cross-checks that temper the initial totals. Key variables include diagnosed diabetes prevalence, annual screening coverage, anti-VEGF dose frequency, laser retreatment ratios, unit ASP trends, and country-level reimbursement caps.

For projection, multivariate regression links procedure volume to expected diabetes growth, aging curves, and payer policy shifts, while exponential smoothing handles price evolution. Where bottom-up inputs are thin (e.g. vitrectomy ASPs in emerging markets), we bridge gaps with expert-verified medians before triangulating the final series.

Data Validation & Update Cycle

Outputs undergo variance checks against historical import data and manufacturer revenue, followed by two-step peer review inside Mordor. Models refresh every twelve months, and analysts inject mid-cycle updates when material events, such as drug recalls and reimbursement resets, arise.

Why Our Diabetic Retinopathy Baseline Inspires Confidence

Published figures often diverge because firms start from different base years, tuck diagnostics into therapy totals, or assume uniform drug dosing worldwide.

Major gap drivers stem from (i) scope creep that mixes screening equipment with treatment spend, (ii) aggressive biosimilar price erosion assumptions, and (iii) outdated epidemiology tables that ignore the 2024 IDF revision. Mordor Intelligence excludes such distortions and revisits every underlying metric annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.08 B (2025) | Mordor Intelligence | |

| USD 9.48 B (2024) | Global Consultancy A | Older base year and narrower modality list omits vitrectomy spend |

| USD 8.70 B (2024) | Trade Journal B | Assumes uniform 30 % biosimilar price cut worldwide |

| USD 8.43 B (2024) | Industry Publisher C | Bundles low-cost diagnostics but excludes high-value anti-VEGF re-treatments |

Taken together, the comparison shows how our disciplined scope selection, yearly refresh cadence, and dual-track validation yield a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current Global Diabetic Retinopathy Market size?

The diabetic retinopathy market size was USD 10.71 million in 2026 and is forecast to reach USD 14.52 million by 2031.

Who are the key players in Global Diabetic Retinopathy Market?

Regeneron Pharmaceuticals, Inc., Alimera Sciences, Oxurion NV., Abbvie Inc. and F. Hoffmann-La Roche Ltd are the major companies operating in the Global Diabetic Retinopathy Market.

Which is the fastest growing region in Global Diabetic Retinopathy Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Diabetic Retinopathy Market?

North America held 42.98% of global revenue in 2025, driven by advanced care infrastructure and rapid adoption of AI-based screening.

How are new biologics changing the diabetic retinopathy market?

Long-acting platforms such as Genentech’s Susvimo and Regeneron’s Eylea HD reduce injection frequency, improving adherence and strengthening their competitive position.

Page last updated on: