Oman Automotive Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

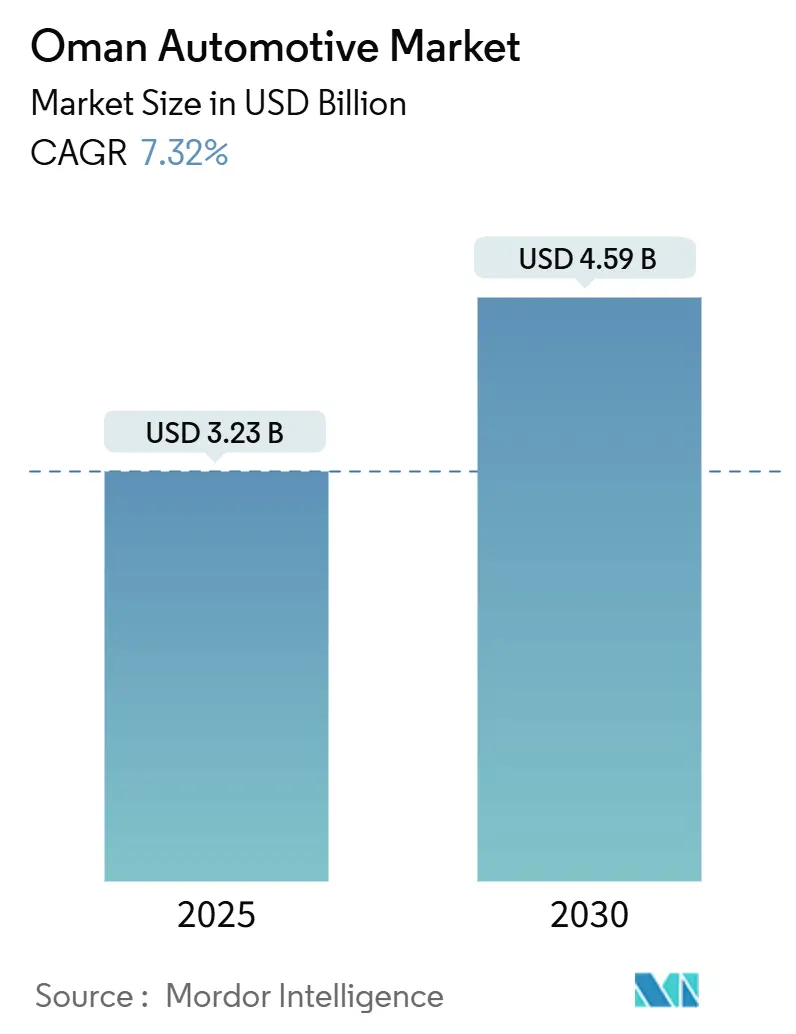

| Market Size (2025) | USD 3.23 Billion |

| Market Size (2030) | USD 4.59 Billion |

| Growth Rate (2025 - 2030) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Automotive Market Analysis by Mordor Intelligence

The Oman Automotive Market size is estimated at USD 3.23 billion in 2025, and is expected to reach USD 4.59 billion by 2030, at a CAGR of 7.32% during the forecast period (2025-2030). Robust infrastructure outlays under Vision 2040, such as the Al-Batinah Expressway, shorten freight lead-times and expand commuter catchment areas, spurring fresh vehicle demand across personal and commercial segments. Oman acceded to the TIR Convention in October 2018; the Convention entered into force for Oman on May 29, 2019, and TIR became operational in the Sultanate in August 2020. Two-wheeler uptake gains momentum as young urbanites pursue low-cost mobility, while EV prospects brighten because mandatory charger installations at service stations narrow perceived range anxiety. Dealer digitization, evidenced by Towell Auto’s SAP S/4HANA roll-out, complements the surge in online classifieds, giving shoppers real-time price transparency and nationwide inventory visibility.

Key Report Takeaways

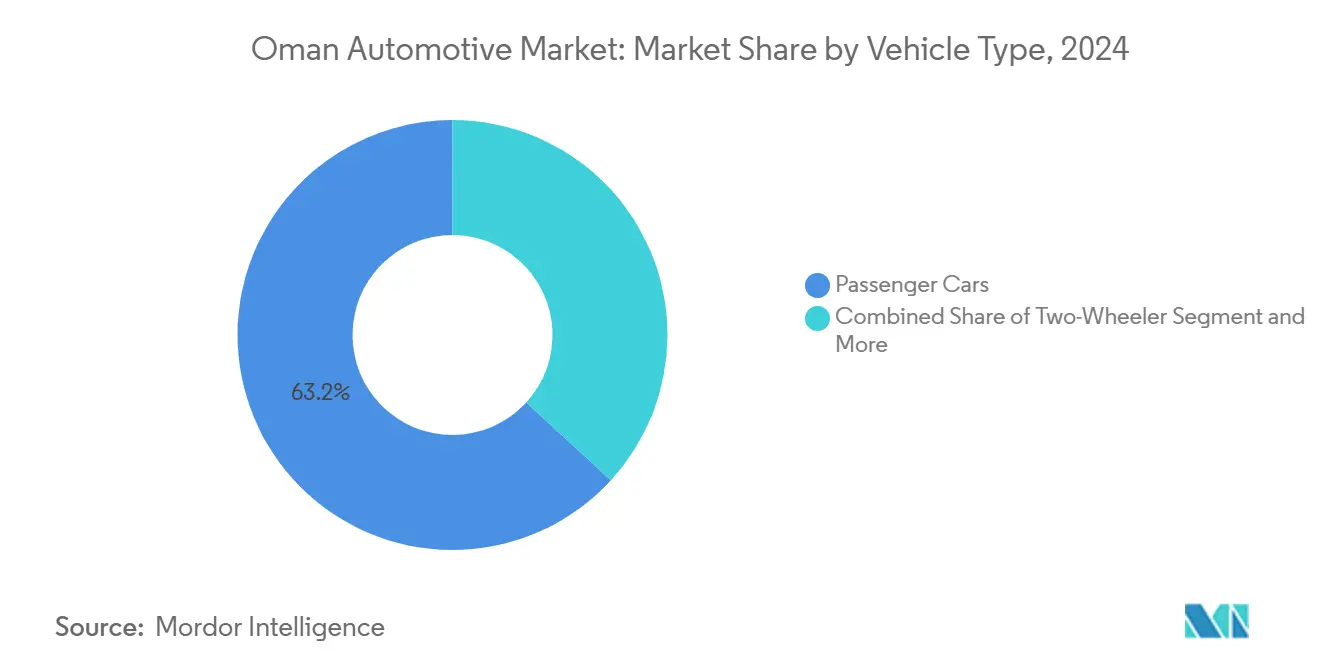

- By vehicle type, passenger cars led with 63.15% of the Oman automotive market share in 2024; the two-wheeler segment is projected to expand at a 7.35% CAGR through 2030, the fastest within the vehicle-type hierarchy.

- By propulsion, internal-combustion engines held 87.18% of the Oman automotive market share in 2024, while electric vehicles are expected to post the highest growth at a 7.37% CAGR from 2024 to 2030.

- By application, personal use commanded a 78.11% share of 2024 sales, while public transport is projected to show a 7.38% CAGR through 2030.

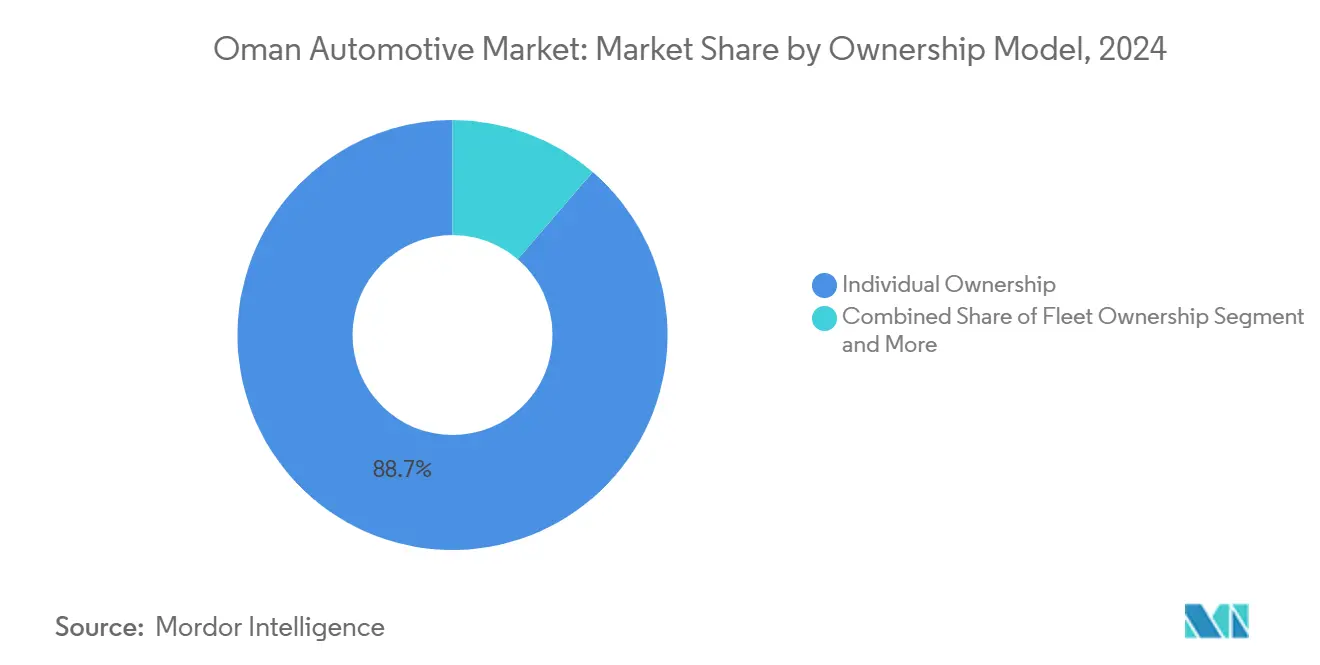

- By ownership, the individual ownership segment dominated at 88.73% in 2024; subscription programs record the quickest rise at 7.44% CAGR.

- By sales channel, OEM dealers controlled 59.36% of transactions in 2024, yet online portals accelerated at a 7.41% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Oman representing one among them. The global report on automotive market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Oman Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 Road-Infrastructure Expansion | +1.8% | National, with early gains in Muscat, Al Batinah, Dhofar | Medium term (2-4 years) |

| Easy Consumer Credit and Dealer Finance Offers | +1.2% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Fleet-Electrification Targets Of Oil and Gas Majors | +1.1% | National, with industrial zones priority | Medium term (2-4 years) |

| Gradual Fuel-Subsidy Reform | +1.0% | National, urban areas first | Long term (≥ 4 years) |

| Surge In Online Used-Vehicle | +0.9% | National, with Muscat leading adoption | Short term (≤ 2 years) |

| Biodiesel Blending | +0.7% | National, commercial vehicle focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2040 Road-Infrastructure Expansion

Oman’s massive pipeline of highways and feeder roads under Vision 2040 compresses travel times, catalyzing both commuter car purchases and fresh truck demand for construction logistics[1]Oman Observer, “Vision 2040 Transport Projects to Push Logistics Boom,” omanobserver.om. Large fleets such as TruckOman deploy additional flatbeds to shuttle materials between Sohar and Duqm, amplifying heavy-duty registrations. Industrial city tenants managed by Madayn—housing 60,000-plus employees—rely on light vans to ferry staff between work zones and satellite towns. Seamless customs clearance through the GCC Integrated Tariff further elevates cross-border traffic, attracting new entrants like Fahud Desert Trading to scale operations. Passenger-car sales rise in tandem as newly paved corridors stimulate suburban housing, reinforcing the Oman automotive market’s growth trajectory.

Easy Consumer Credit & Dealer Finance Offers

Liberalized banking rules permit tenors up to 72 months, cutting monthly installments and widening buyer eligibility[2]National Finance, “Auto Loan Products,” nationalfinance.co. Dealer groups embed instant credit checks within showroom tablets, slashing approval cycles to under 30 minutes. The strategy boosts conversion ratios in entry-level hatchbacks and the two-wheeler niche—segments where price elasticity is acute. Cross-border funding, illustrated by Karwa Motors’ facility, funnels external liquidity into domestic stock, allowing dealers to maintain broad model ranges. Digital loan portals integrated with SAP back-ends push tailored offers to prospects browsing inventory online, converting web traffic into showroom footfall.

Fleet-Electrification Targets of Oil & Gas Majors

Petroleum Development Oman mandates phased EV adoption across field-service units, locking in predictable demand for light commercial EVs[3]Petroleum Development Oman, “Sustainability Report 2025,” pdo.co.om. OOMCO EVO network: 133 charging points across 66 locations (end-2024), many sited at refinery perimeters where company fleets dwell overnight. Joint engineering teams optimize shift scheduling to accommodate battery dwell time, ensuring parity in uptime with diesel counterparts. Pilot hydrogen trucks undergo route testing between Fahud and Muscat, signalling broader alternative-fuel pathways. These proof points influence private logistics firms to insert EV-range vans into tender bids, driving the Oman automotive market toward electrification.

Biodiesel Blending Improving TCO for CV Fleets

Mandated biodiesel blends shave minimal off fuel bills for operators like Al Nowras Logistics, which runs 200 rigs on long corridors to Saudi Arabia. Local feedstock sourcing converts agri-waste into revenue, aligning logistics players with national circular-economy goals. Vehicle makers deliver factory-tuned engines for B20 blends, extending oil-change intervals and reducing downtime. Fleet-management software benchmarks biodiesel mileage against conventional diesel, reinforcing financial gains in quarterly reviews. The net savings finance fleet renewals, lifting medium-truck sales volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Preference | -1.4% | National, stronger in rural and industrial areas | Medium term (2-4 years) |

| Cheap Gasoline | -1.1% | National, particularly urban centers | Short term (≤ 2 years) |

| Battery-Degrading Desert Temperatures | -0.9% | National, intensified in interior regions | Long term (≥ 4 years) |

| Limited Public Charging Network | -0.8% | Regional, affecting non-Muscat governorates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Large ICE SUVs & Pickups

Listings on OpenSooq show Toyota leading with multiple vehicles, most of them Land Cruisers and Hilux variants favored for off-road weekends and family excursions. Price points for models like Great Wall H9 hover around OMR 12,500, underscoring willingness to pay for size and perceived status. Higher ground clearance and payload capacity suit rugged tracks prevalent in interior governorates. Premium makers such as Lexus still move multiple units on classifieds, reflecting robust luxury appetite despite subsidy cuts. Lack of mass-market electric SUVs with similar tow ratings entrenches ICE dominance, restraining the Oman automotive market’s electrification curve.

Limited Public Charging Network Outside Muscat

Kempower’s DC clusters and Zerova’s forecourt units concentrate inside the capital, leaving Dhofar-bound drivers to rely on Muscat-origin range. OOMCO’s sockets remain inadequate for Musandam or Al Wusta itineraries that exceed 500 km round-trip. The Authority for Public Services Regulation prioritizes fast chargers, which carry high capex and slow rural roll-outs. Private landlords hesitate without volume guarantees, spacing out the corridor network build. Consequently, households in secondary cities postpone EV purchases, slowing geographic penetration and moderating overall market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Retain Primacy While Two-Wheelers Accelerate

Passenger cars captured 63.15% of the Oman automotive market share in 2024. Dealer loyalty programs, broad model ranges, and high residual values underpin this leadership. Toyota filters nearly two-fifths of segment sales through the Saud Bahwan network, complemented by Nissan and Hyundai lines distributed by Al Hashar and OTE Group. Urban congestion, however, pushes millennials toward motorbikes, posting a 7.35% CAGR.

Growth stems from strict parking supply in Muttrah and Ruwi, where motorcycles halve commute times. Ride-sharing couriers prefer 150 cc bikes for last-mile parcels, driving bulk orders that lift wholesale volumes. Passenger-car demand stays resilient because suburban real-estate expansion in Al Amerat necessitates family sedans. Three-wheelers remain a niche but gain traction in municipal waste contracts requiring compact vehicles. Off-highway sales remain cyclical, linked to oil-rig capex budgets and limestone-mine expansions near Ibri.

By Propulsion Type: ICE Still Dominant But EV Curve Steepens

Internal-combustion cars represented 87.18% of 2024 deliveries. Abundant fuel supply, skilled mechanics, and plentiful spare parts sustain the legacy fleet. Yet EV registrations rise at 7.37% CAGR, outpacing all other powertrains. Government decrees obligate every new fuel station to host at least one 50 kW DC charger, guaranteeing future coverage.

Corporate fleets spearhead adoption: PDO just placed a 50-unit order for compact EV crossovers, securing volume discounts. Hybrids serve as a middle road, alluring consumers worried about range while capturing tax breaks on low-emission vehicles. Warranty extensions from six to eight years on traction batteries alleviate desert-heat fears. OEMs fine-tune thermal-management software to cap cell degradation under 45 °C ambient temperatures, trimming one operational barrier.

By Application: Personal Use Dominates, Public Transport Takes Off

Personal-use purchases stood at 78.11% in 2024, reflecting ingrained ownership culture and limited intercity buses. The market size attributable to personal-use purchases increased in 2024. Muscat's expanding suburbs such as Al Mouj promote two-car households, sustaining volume.

Public transport posts the highest 7.38% CAGR due to April 2025 rules mandating all the taxis enroll on ride-hailing apps. Operators upgrade fleets to comply with platform age caps, cycling older sedans into the rural used-car pool. Taxi Muscat quadruples cars to 4,000 by end-2025, while Yango launches with 300 sedans and an option for 1,000 more. Logistics and industrial-use vehicles piggyback on refinery expansions, keeping heavy-truck backlogs healthy at local assemblers.

By Ownership Model: Individuals Rule But Subscriptions Gain Mindshare

The individual ownership segment accounted for 88.73% of the automotive market ownership in Oman in 2024. Bank auto-loan penetration exceeds three-fifths in Muscat, reinforcing ownership. Subscription services, though small, notch a 7.44% CAGR. Start-ups offer month-to-month Nissan Sunny access for OMR 160, bundling insurance and maintenance.

Younger professionals gravitate to these plans to avoid upfront down-payments. Enterprise Rent-A-Car’s March 2025 deal with Audi Oman introduces premium tiers priced at OMR 750 monthly for Q5 hybrids, hinting at upscale potential. Corporate leasing expands double-digits as multinationals prefer off-balance-sheet mobility, averaging 36-month tenors.

By Sales Channel: Dealers Dominate as Online Click-And-Buy Sprints Forward

OEM-tied dealers accounted for 59.36% of vehicle sales in 2024, in part due to 50-point inspection guarantees and bundled service contracts. Oman's automotive market size surpassed the billion-dollar mark, due to the channel's performance. Online portals clock 7.41% CAGR, fed by OpenSooq’s multiple live ads and Dubizzle’s mobile relaunch. Integrated payment gateways enable escrow protection, thereby increasing completion rates.

Independent used-car yards still thrive along Wadi Kabir highway, serving budget buyers. Yet digital natives syndicate inventory online, exposing out-of-city lots to Muscat shoppers. Towell Auto merges SAP analytics with web storefronts, triggering instant stock reallocations among its 17 showrooms. Manufacturers are eyeing direct-to-consumer pilots once e-commerce licensing matures, potentially reshaping the dealer landscape post-2027.

Geography Analysis

Muscat captured roughly three-fifths of 2024 registrations, anchored by its more than million residents and the bulk of corporate headquarters. The city’s charger density and metro road grid support early EV take-up, solidifying its lead in both ICE and electric sales. Al Batinah follows as the fastest-growing region at an estimated robust CAGR through 2030, fueled by the Al-Batinah Expressway and industrial estates in Sohar that elevate freight and commuter volumes.

Dhofar’s Salalah Free Zone sustains light-truck demand tied to agro-exports and khareef tourism peaks. Interior governorates such as Al Dakhiliyah continue to prioritize pickups for farm-to-market logistics, maintaining steady but moderate growth. Charging scarcity outside Muscat suppresses EV interest in these areas, yet subsidy reform nudges consumers toward hybrids as a transitional solution.

Cross-border trade with UAE and Saudi Arabia leverages TIR corridors, stimulating trailer sales and service-station upgrades along the Haima–Ibri route. Sohar Port’s automotive terminal expedites imports, enabling dealers to shorten lead-times and curb inventory carrying costs. Royal Oman Police expands inspection bays in Duqm and Nizwa, standardizing compliance and improving vehicle condition transparency nationwide.

Competitive Landscape

The Oman automotive market is moderately concentrated: the top five dealer groups collectively hold roughly three-fifths of new-car volumes. Saud Bahwan leads via Toyota and Lexus franchises, banking on 40-plus service centers and same-day parts delivery. Al Hashar Automotive follows with Nissan and Renault, capitalizing on compact SUV demand. OTE Group, with its diverse lineup featuring Hyundai, Chevrolet, and GWM, spans the market from affordable hatchbacks to premium pickups.

Technological upgrades differentiate rivals. Towell Auto’s SAP backbone grants 360-degree customer views, slashing warranty-claim cycle time by quarter. Bahwan International embeds predictive stocking algorithms, elevating parts-fill rates to almost full. New entrants BYD and VinFast inked December 2024 distribution pacts, bringing direct-sale agile retail formats that pressure legacy showroom footprints.

Digital platforms intensify competition on transparency. OpenSooq and Dubizzle aggregate listings, eroding dealer pricing power. Subscription and ride-hailing models challenge outright purchase volumes yet open fleet-service revenue streams for adaptable dealers. Regulatory vigilance, such as the Consumer Protection Authority’s June 2024 Audi e-Tron GT recall, demands robust quality-management systems, favoring well-capitalized incumbents.

Oman Automotive Industry Leaders

Toyota Motor Corp.

Nissan Motor Co.

Hyundai Motors

Mitsubishi Motors

Kia Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Towell Auto Group rolled out SAP S/4HANA, aiming to modernize its operations across multiple brands, enhancing efficiency, streamlining processes, and improving overall operational agility.

- March 2025: Enterprise Rent-A-Car forged a partnership with Audi Oman, enhancing its rental fleet with eight premium models, catering to the growing demand for luxury vehicles in the region and strengthening its position in the Omani car rental market.

- February 2025: Škoda Auto made its Omani debut through Premium Motors and Alfardan Group, introducing an innovative fully digital showroom concept, offering customers a seamless and interactive car-buying experience while showcasing the brand's commitment to digital transformation and customer-centric solutions.

Oman Automotive Market Report Scope

| Two-Wheeler |

| Three-Wheeler |

| Passenger Cars |

| Commercial Vehicle |

| Off-Highway Vehicles |

| Internal Combustion Engine |

| Hybrid Vehicle |

| Electric Vehicle |

| Personal |

| Commercial |

| Public Transport |

| Industrial Use |

| Individual Ownership |

| Fleet Ownership |

| Subscription-Based |

| Shared Mobility |

| OEM Dealers |

| Independent Dealers |

| Online Platforms |

| Direct-to-Consumer |

| By Vehicle Type | Two-Wheeler |

| Three-Wheeler | |

| Passenger Cars | |

| Commercial Vehicle | |

| Off-Highway Vehicles | |

| By Propulsion Type | Internal Combustion Engine |

| Hybrid Vehicle | |

| Electric Vehicle | |

| By Application | Personal |

| Commercial | |

| Public Transport | |

| Industrial Use | |

| By Ownership Model | Individual Ownership |

| Fleet Ownership | |

| Subscription-Based | |

| Shared Mobility | |

| By Sales Channel | OEM Dealers |

| Independent Dealers | |

| Online Platforms | |

| Direct-to-Consumer |

Key Questions Answered in the Report

How big is the Oman automotive market in 2025?

It is valued at USD 3.23 billion and is projected to reach USD 4.59 billion by 2030.

What is the expected CAGR for Oman’s vehicle market to 2030?

The Oman automotive market is forecast to grow at a 7.32% CAGR over 2025–2030.

Which vehicle type sells the most units in Oman?

Passenger cars lead, holding 63.15% of 2024 sales.

Which segment is growing the fastest?

Two-wheelers record the quickest rise, with a 7.35% CAGR through 2030.

Why are electric vehicles gaining traction in Oman?

Mandatory charger installation at fuel stations and corporate fleet electrification are shrinking the ICE-EV cost gap.

Which sales channel is expanding quickest?

Online platforms grow at a 7.41% CAGR thanks to portals like OpenSooq and Dubizzle.

Page last updated on: