Kuwait Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

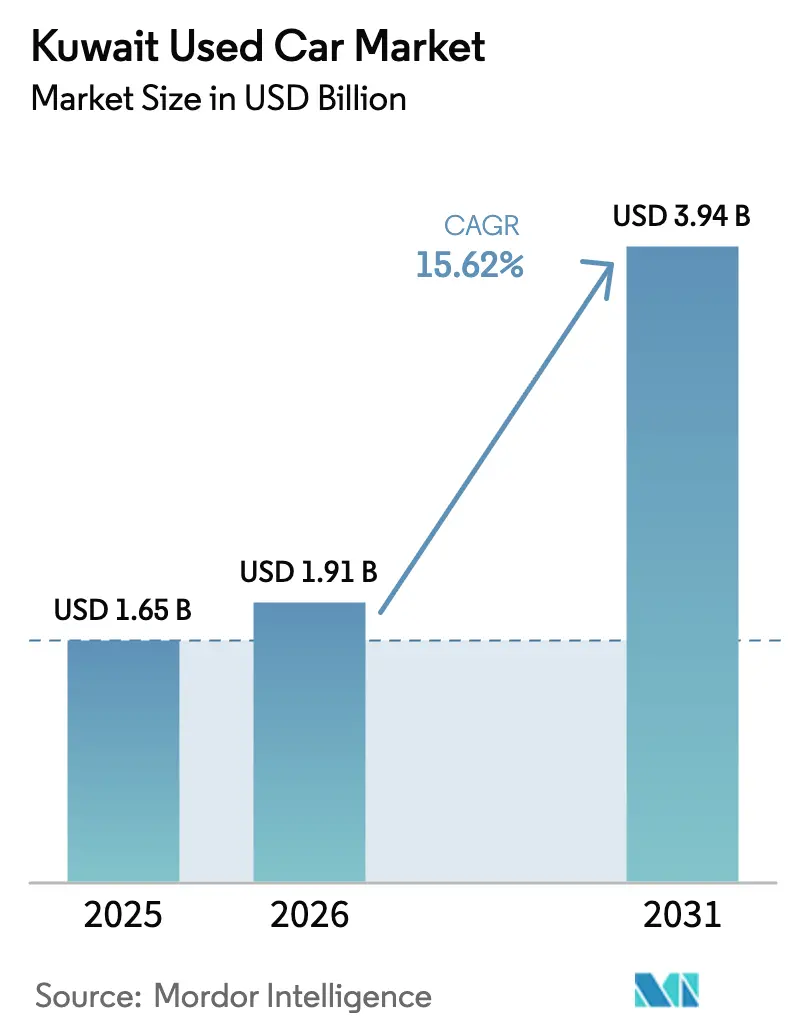

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Used Car Market Analysis by Mordor Intelligence

The Kuwait used car market size was valued at USD 1.65 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 3.94 billion by 2031, at a CAGR of 15.62% during the forecast period (2026-2031). Sustained household purchasing power, abundant bank liquidity, and steady inflow of government-maintained fleet vehicles strengthen price stability and attract first-time buyers. The new traffic law restricting expatriates to a single vehicle is nudging multi-car households to trade down or consolidate into better-equipped pre-owned models. At the same time, domestic interest-rate cuts lift loan affordability across income tiers. Online marketplaces are scaling quickly after the Dubizzle Group absorbed Drive Arabia in May 2024, giving digital channels broader inventory visibility and data-driven pricing tools. Demand is also rising for vehicles certified by original-equipment manufacturers because inspection, warranty, and recall coverage narrow perceived quality risks. Electric vehicles are still a niche subset, yet their growth rate points to a structural pivot as charging corridors around Kuwait City and Ahmadi come onstream.

Key Report Takeaways

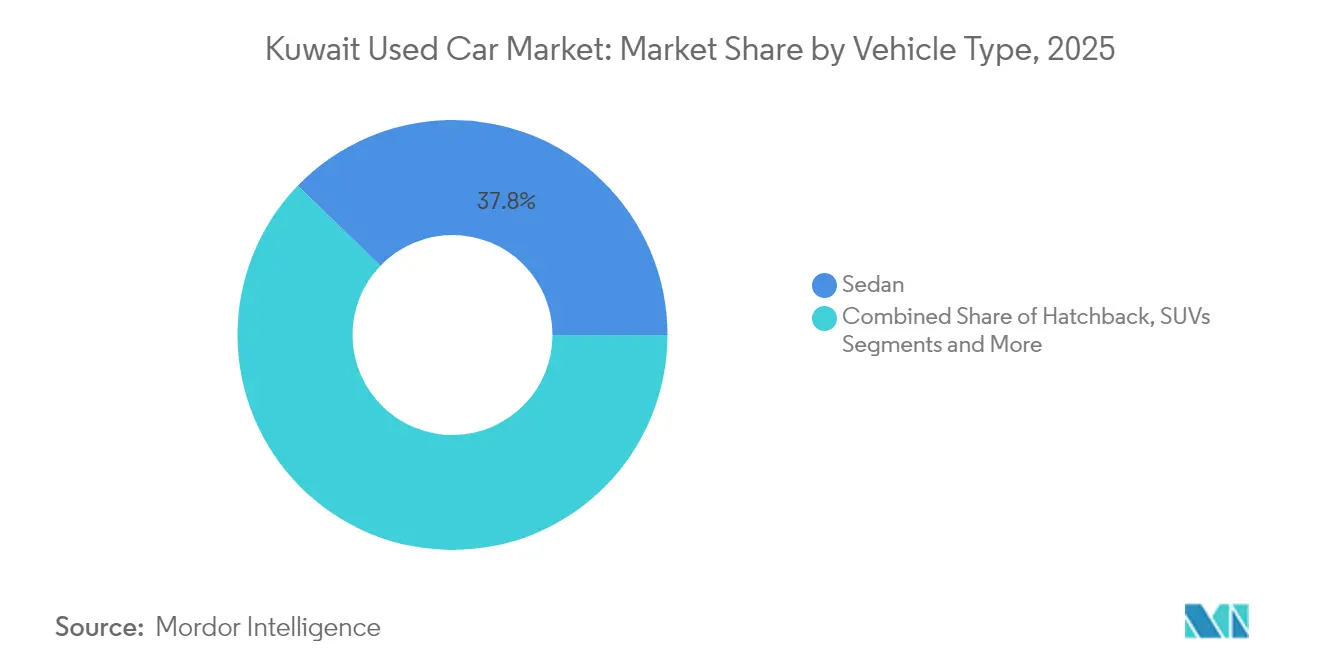

- By vehicle type, sedans held 37.80% of the Kuwait used car market share in 2025, while sport utility vehicles (SUVs) are projected to expand at 17.10% CAGR through 2031.

- By vendor type, unorganized vendors controlled 71.55% revenue in 2025, while organized vendors are advancing at 8.75% CAGR to 2031.

- By fuel type, gasoline units dominated with 85.10% share of Kuwait used car market size in 2025; electric vehicles lead growth at 20.95% CAGR.

- By vehicle age, the 3-5 year band commanded 33.95% share of Kuwait used car market size in 2025, whereas 0-2 year cars are climbing at 13.15% CAGR.

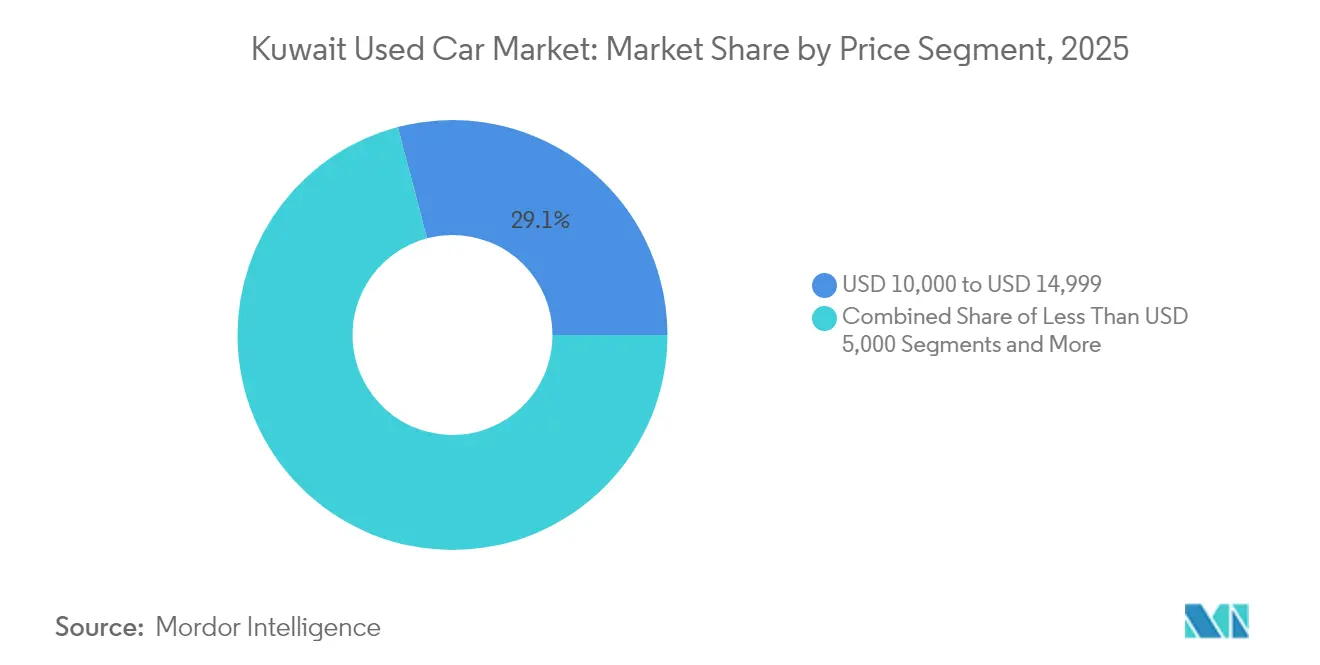

- By price, the USD 10,000–14,999 bracket captured 29.10% market share in 2025; the USD 30,000+ tier shows the fastest 11.10% CAGR to 2031.

- By channel, offline outlets retained 60.55% share in 2025, yet online platforms are scaling at 18.25% CAGR as digital familiarity deepens.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's used car market share coverage captures this comparative structure.

Kuwait Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Online Classified Platforms | +1.5% | National, with concentration in Kuwait City and Ahmadi | Medium term (2-4 years) |

| Rising New-Car Prices | +1.2% | National, affecting all income segments | Short term (≤ 2 years) |

| Favorable Import Regulations | +0.8% | National, with port-adjacent areas benefiting first | Long term (≥ 4 years) |

| OEM-Certified Pre-Owned Programs | +0.6% | National, urban areas leading adoption | Medium term (2-4 years) |

| Government Fleet Renewal | +0.4% | National, with government district concentration | Short term (≤ 2 years) |

| Sharia-Compliant Used-Car Financing | +0.3% | National, targeting underbanked segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Online Classified Platforms and Digital Retailing

Digital transformation fundamentally alters Kuwait's used car distribution model, with online platforms capturing increasing transaction volume through enhanced transparency and convenience features. The shift accelerated following Dubizzle Group's strategic acquisition of Drive Arabia in May 2024, creating a comprehensive automotive ecosystem that combines listing services with pricing intelligence and specification databases. Local platforms like Motorgy differentiate through value-added services, including pre-purchase inspections, safe payment guarantees, and ownership transfer assistance, addressing traditional pain points in private party transactions. The emergence of specialized platforms like Q8car and 4Sale demonstrates market fragmentation, with each targeting specific customer segments through tailored user experiences and mobile applications. Regional data indicates consumers increasingly prefer online research before in-store visits, with platforms like Dubizzle dominating the digital landscape across the GCC.[1]"Autodata bi-annual report highlights key insights shaping the used car market," AutoData Middle East, www.autodatame.com This digital-first approach particularly resonates with younger demographics who value transparency, price comparison capabilities, and transaction efficiency over traditional relationship-based purchasing.

Rising New-Car Prices Shifting Demand Toward Used Cars

Inflationary pressures on new vehicle pricing create a compelling economic case for used car purchases, particularly as Kuwait's expatriate population faces income constraints amid regulatory changes. The pricing differential has widened as global supply chain disruptions and semiconductor shortages have inflated new vehicle costs. At the same time, used car values have remained relatively stable due to a steady supply from government fleet renewals and private sales. Kuwait's high-income economy traditionally favored new vehicle purchases, but changing demographics and economic pressures are normalizing used car ownership across broader income segments. For instance, with a median 2025 sedan priced at KWD 8,800 new versus KWD 5,600 three years used, rational consumers now favor second-hand units to avoid front-loaded depreciation.

Favorable Import Regulations Boosting Vehicle Inflow

Kuwait's streamlined vehicle import procedures and competitive duty structures facilitate a steady inflow of quality used vehicles from key source markets, supporting inventory levels and price stability. The government's vehicle export service through the Ministry of Interior demonstrates institutional support for cross-border automotive trade, with standardized procedures including technical inspections and documentation requirements that ensure imported vehicles meet the necessary safety standards.[2]"Kuwait Government Online," Kuwait Government, e.gov.kw Import regulations favor GCC-specification vehicles, which command premium pricing due to their suitability for local climate conditions and service network compatibility. Toyota and Nissan are leading market preferences. The regulatory framework's stability provides predictability for importers and dealers, enabling them to maintain consistent inventory levels and pricing strategies. Recent policy discussions around vehicle import duties and environmental standards suggest the government is balancing revenue generation with consumer affordability, while also considering emissions reduction targets. This regulatory environment supports the market's growth trajectory by ensuring adequate supply diversity and competitive pricing across vehicle segments.

Expansion of OEM-certified pre-owned programs

Dealer groups in manufacturer-verified reconditioning to elevate trust and command pricing power. Ali Alghanim & Sons markets BMW Premium Selection units that undergo a 200-point inspection and carry a two-year unlimited-kilometer warranty, fetching a 9-12% premium over similar non-certified cars. Abdulmohsen Al Babtain’s new Genuine Spare Parts hub in Shuwaikh improves turnaround time for recall or cosmetic repairs, enabling same-week delivery on most certified Nissan models. Certified inventory also attracts lenders, as banks extend higher loan-to-value ratios for cars covered by factory warranties, enhancing affordability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Trust and Transparency | -0.7% | National, more pronounced in unorganized vendor segments | Medium term (2-4 years) |

| Limited Supply of Quality Used EVs | -0.5% | National, with urban areas most affected | Long term (≥ 4 years) |

| Mandatory ADAS Recalibration | -0.4% | National, affecting premium vehicle segments | Short term (≤ 2 years) |

| High Insurance Premiums | -0.3% | National, impacting budget-conscious consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited supply of quality used EVs

Kuwait's electric vehicle infrastructure development creates demand for used EVs that exceeds current supply availability, constraining this high-growth segment's expansion potential. The government's ambitious plans for EV adoption, including requirements for state bodies to purchase 5% zero-emission vehicles and the Ministry of Electricity and Water's charging station development program, generate interest that outpaces the availability of used EVs.The challenge is exacerbated by EV owners' tendency to retain vehicles longer due to high initial purchase prices and concerns about resale values in a developing market.

Limited trust and transparency in vehicle history

Information asymmetry between buyers and sellers continues to constrain market growth, particularly in the unorganized vendor segment, where standardized disclosure practices are inconsistent. The challenge is compounded by Kuwait's vehicle ownership transfer requirements, which mandate valid insurance and proper documentation but do not address comprehensive vehicle history disclosure. The lack of centralized vehicle history databases means buyers must rely on seller representations and limited inspection capabilities, creating risk premiums that suppress transaction volumes. Digital platforms are attempting to address this through inspection services and seller verification, but comprehensive solutions require industry-wide standardization and potentially regulatory intervention. The trust deficit is particularly pronounced for higher-value vehicles where potential losses from undisclosed issues can be substantial, leading to conservative buyer behavior and extended decision-making cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sedans retain cultural gravitas amid SUV ascent

Sedans contributed 37.80% to the Kuwait used car market share in 2025 and will continue to anchor demand because urban commuting favors their ride comfort and fuel economy. Toyota Camry and Honda Accord preserve residual values above 65% after three years, making them liquidity-rich assets in private resales. Sport-utility vehicles (SUVs) are scoring rapid mindshare among younger Kuwaitis keen on desert leisure, while entry-level electric crossovers from Chinese marques add an affordable electrification pathway. SUVs are estimated to demonstrate the highest CAGR of 17.10% over the forecast period. Multi-purpose vans fulfil both large family and app-based delivery requirements, though supply remains thin. The “Others” slice, featuring coupes and sports cars, skews premium and rides on the nation’s high disposable income.

Model proliferation is altering consumer calculus. Chinese brands logged a 150% spike in Kuwaiti inquiries during mid-2024, injecting price competition that could compress sedan premiums. Yet, prestige perceptions still steer buyers toward Japanese and German badges, particularly at the USD 10,000–14,999 sweet spot. Over the forecast horizon, sedan dominance will likely ease but remain plurality, while the electric sub-segment chips away share as infrastructure densifies.

By Vendor Type: Cost Agility versus Service Assurance

Unorganized lots captured 71.55% of revenue in 2025 because they undercut authorized workshops by up to 20% on service and parts. These micro-dealers operate from low-rent yards across Farwaniya and Jahra, passing savings directly to cash buyers. However, organized vendors are scaling at 8.75% CAGR as consumers weigh lifetime cost against upfront price, especially once factory warranties lapse. Dealers like ALSAYER provide bundled after-sales, insurance facilitation, and guaranteed trade-in values, cornering repeat customers.

Digital storefronts further reduce the cost gap by eliminating multiple middlemen. Organized players listing on Motorgy or their portals can rotate inventory 30% quicker, freeing working capital. Regulatory scrutiny may raise compliance costs for informal vendors, tilting market preference toward structured outlets and delaying the point at which price alone dictates choice.

By Fuel Type: Cheap petrol anchors gasoline grip

Gasoline vehicles maintained commanding market leadership with an 85.10% share in 2025, reflecting Kuwait's low fuel prices and established infrastructure. Electric vehicles represent the fastest-growing fuel type, with a 20.95% CAGR from 2026 to 2031. The gasoline segment's dominance is reinforced by Kuwait's subsidized fuel pricing structure and consumers' familiarity with internal combustion engine maintenance and service networks, creating natural barriers to alternative fuel adoption. Diesel vehicles serve commercial and heavy-duty applications but face declining consumer preference due to environmental concerns and regulatory pressures. Hybrid vehicles occupy a transitional position, appealing to environmentally conscious consumers not ready for full electric adoption.

The electric vehicle segment's rapid growth reflects government policy initiatives, including the Ministry of Commerce's technical committee formation with 14 government agencies to establish EV conditions and charging infrastructure development. Regional trends show significant increases in used EV and hybrid residual values, outperforming traditional petrol and diesel vehicles, indicating strong demand fundamentals despite supply constraints. Other fuel types, including LPG and CNG, maintain niche positions primarily in commercial applications. The fuel type segmentation is experiencing fundamental shifts as the government targets 5% zero-emission vehicle purchases by state bodies, creating demonstration effects that influence consumer preferences and market dynamics.

By Vehicle Age: Depreciation calculus shapes buyer psychology

Cars aged 3-5 years control 33.95% of transactions because they avoid the steepest depreciation while qualifying for extended warranty packages. The average remaining warranty of 19 months translates into lower perceived risk, enticing mid-income households that aim to maximize value over a planned 48-month ownership span. The 0-2 year tranche grows at 13.15% CAGR as corporate lease returns flood the market. These cars often carry connected-car features and advanced driver-aid suites that consumers desire but are too expensive in new-car form.

Older segments beyond eight years draw budget buyers who prioritize acquisition price over safety tech. Yet, they face rising insurance premiums of up to 15% yearly, nudging owners toward earlier disposal cycles. Academic modelling of Kuwaiti auto-travel cost found many consumers misjudge the compound cost of keeping a decade-old sedan, overlooking cumulative maintenance outlays. Better cost transparency through online TCO calculators may accelerate the upgrade cycle and increase turnover in the near-new segment.

By Price Segment: Middle Market Drives Transaction Volume

The USD 10,000-14,999 price segment captures the largest market share at 29.10% in 2025, aligning with middle-income purchasing power and financing capabilities, while the premium USD 30,000+ segment exhibits the strongest growth at 11.10% CAGR during 2026-2031. This price distribution reflects Kuwait's income demographics and the availability of financing options that make mid-range vehicles accessible to the broadest consumer base. The middle market segment benefits from the intersection of affordability and quality, offering vehicles with desirable features and remaining useful life at prices that align with typical consumer budgets and loan qualification criteria.

The premium segment's growth reflects Kuwait's high-income demographics and preference for luxury vehicles. Lower price segments under USD 10,000 serve budget-conscious consumers and first-time buyers, while segments between USD 15,000-29,999 cater to consumers seeking higher-specification vehicles with advanced features.

By Sales Channel: Digital Transformation Accelerates

Offline channels maintain market dominance with 60.55% share in 2025, reflecting established dealer relationships and consumer preferences for physical vehicle inspection, while online channels emerge as the fastest-growing segment at 18.25% CAGR during 2026-2031. The offline channel's continued strength stems from the high-involvement nature of vehicle purchases where consumers value the ability to physically inspect, test drive, and negotiate in person with experienced sales professionals. Traditional dealerships, independent dealers, and physical auction houses provide established infrastructure and trusted relationships that many consumers prefer for significant purchases.

Digital transformation rapidly reshapes channel preferences, particularly among younger demographics who value convenience, transparency, and price comparison capabilities. Dubizzle Group's strategic acquisition of Drive Arabia in May 2024 demonstrates platform operators' commitment to creating comprehensive online automotive ecosystems that combine listing services with pricing intelligence and transaction support. Online classified portals are evolving beyond simple listing services to offer integrated financing, inspection, and delivery services that address traditional online purchasing barriers. Pure-play e-retailers and OEM-certified online stores are developing hybrid models that combine digital convenience with physical fulfillment capabilities. The channel evolution reflects broader consumer behavior changes where online research precedes offline transactions, creating opportunities for integrated omnichannel strategies that leverage both digital efficiency and physical trust-building.

Geography Analysis

Kuwait City, Ahmadi, and Hawalli make up more than 70% of transaction volume, with the capital anchoring inventory flows from port to showroom. Government asset-disposal auctions take place in Shuwaikh, ensuring a steady pipeline for central dealers, who then distribute to peripheral towns overnight. The country's compact size allows nationwide same-day vehicle delivery, favoring centralized reconditioning hubs over distributed service points. High urban density also supports a network of battery-swap micro-stations that underpin early EV adoption, especially along the Sixth Ring Road corridor.

Cross-border dynamics shape sourcing. Importers favor vehicles originally sold in the UAE due to shared GCC standards, while premium dealers fetch low-mileage German sedans from Oman’s corporate fleets. Proximity to Saudi Arabia presents outbound opportunities for Kuwaiti dealers, who re-export older SUVs once local appetite wanes. Regulatory uniformity across the Customs Union simplifies paperwork, but Kuwait’s distinct insurance requirement at registration remains a unique cost that buyers factor into purchasing timelines.

Regional policy shocks echo quickly because of the geographic concentration. The April 2025 single-car rule for expatriates had an immediate nationwide effect, raising demand for multi-purpose vehicles with flexible seating. Likewise, any port congestion or customs-system outage in Kuwait City can momentarily crimp countrywide supply, underscoring the need for digital clearance redundancy. Overall, the tightly knit geography accelerates the diffusion of technology and regulation, making the used car market in Kuwait highly sensitive yet agile.

Analysis of the used car market by Mordor Intelligence spans multiple other regional evaluations across Africa, supported by country-level insights for Oman, Netherlands, Qatar, Tanzania, South Africa, Portugal, Egypt, and Ethiopia, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Kuwaiti used car market exhibits moderate fragmentation. Legacy groups such as ALSAYER combine 70-plus years of brand stewardship with integrated service, parts, and financing, letting them extract scale efficiencies that informal yards cannot match. Still, no single entity eclipses 20% share, leaving room for agile newcomers. Technology now sets the competitive pace. Dubizzle leverages machine-learning price engines and escrow to keep buyer abandonment under 12%, the lowest in the GCC. Emerging platforms like Motorgy monetize inspection data, selling anonymized valuation feeds to banks hungry for smarter risk scoring.

Strategic talent moves intensify rivalry. Alghanim Industries installed former GM Europe President Mahmoud Samara as CEO in January 2024 to spearhead omnichannel rollouts and smooth supply integration from its multibrand portfolio. Meanwhile, ALSAYER pilots subscription-based access that bundles maintenance and insurance into monthly fees, targeting expatriates with short-term residency. Competitive differentiation is increasingly tied to post-sale ecosystem services—extended warranties, concierge registration, and bundled telematics—rather than plain inventory breadth.

Consolidation is gathering steam across borders. Al-Ghanim Group secured exclusive Rolls-Royce rights in Iraq during 2025, signaling ambitions to form a trans-GCC luxury network. Should Saudi Arabia’s Public Investment Fund finalize its proposed partnership with Nissan, Kuwaiti dealers may gain preferential access to regional stock, smoothing supply volatility. Such moves underscore the intertwining of Kuwait’s market with broader Gulf strategies, meaning local players must scale digital capability and capital strength to remain competitive.

Kuwait Used Car Industry Leaders

-

ALSAYER Group Holding.

-

YallaMotor.com

-

Alghanim & Sons Automotive

-

Dubizzle Group

-

AL BABTAIN GROUP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kuwait implemented comprehensive traffic law reforms through Decree-Law No. 5 of 2025, introducing mandatory valid insurance for vehicle licensing and restricting expatriates to single vehicle ownership, fundamentally altering demand patterns in the used car market. The legislation includes severe penalties for traffic violations and grants the Minister of Interior authority to regulate vehicle licensing numbers and insurance tariffs, creating new regulatory oversight mechanisms that will influence market operations.

- May 2024: Dubizzle Group completed the acquisition of Drive Arabia, consolidating automotive advertising platforms and expanding service offerings across the MENA region. CEO Haider Ali Khan emphasized strategic vision to improve user experience and planned significant investment in enhanced pricing and specification tools.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Kuwait's used car market as every pre-owned passenger vehicle that has already been registered at least once and is resold through dealer forecourts, classified portals, auctions, or direct peer-to-peer transactions inside Kuwait's borders, whether the car was originally imported or first purchased new in the country. We convert all transaction values into constant 2024 US dollars so clients see a clean like-for-like trend.

Scope Exclusions: Commercial trucks above 3.5 tons, motorcycles, and salvage units dismantled solely for parts remain outside scope.

Segmentation Overview

-

By Vehicle Type

- Hatchback

- Sedan

- Sport Utility Vehicles (SUVs)

- Multi-Purpose Vehicles (MPVs)

- Others (Convertibles, Coupes, Crossovers, Sports Cars)

-

By Vendor Type

- Organized

- Unorganized

-

By Fuel Type

- Gasoline

- Diesel

- Hybrid

- Electric

- Other Fuel Types (LPG/CNG/Others)

-

By Vehicle Age

- 0 – 2 Years

- 3 – 5 Years

- 6 – 8 Years

- 9 – 12 Years

- More than 12 Years

-

By Price Segment (USD)

- less than USD 5,000

- USD 5,000 – USD 9,999

- USD 10,000 – USD 14,999

- USD 15,000 – USD 19,999

- USD 20,000 – USD 29,999

- More than USD 30,000

-

By Sales Channel

-

Online

- Digital Classified Portals

- Pure-play e-Retailers

- OEM-Certified Online Stores

-

Offline

- OEM-Franchised Dealers

- Multi-brand Independent Dealers

- Physical Auction Houses

-

Online

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with franchise dealers, independent lots, online platform managers, finance officers, and workshop owners across Kuwait City, Hawalli, and Jahra. These conversations verified churn rates, emerging certified-pre-owned volumes, and typical price spreads that raw desk research cannot capture on its own.

Desk Research

We first harvested baseline volumes from public sources such as Kuwait Central Statistical Bureau registration bulletins, General Administration of Customs import manifests, International Trade Center HS-8703 trade data, and the GCC Automotive Manufacturers Association sales dashboard. These datasets show how many passenger cars flow into, and cycle within, the national fleet each year. Company filings, local classifieds archive counts, and news collected via Dow Jones Factiva and D&B Hoovers helped us triangulate average selling prices, dealer footprints, and finance penetration. Numerous additional repositories were reviewed; the sources listed merely illustrate the breadth of material consulted.

A second sweep covered regulatory notices on age and emission limits, Central Bank credit reports, and patent trends on vehicle re-inspection technology. Together, they clarify compliance costs, funding availability, and technology adoption curves that nudge demand.

Market-Sizing & Forecasting

We applied a top-down reconstruction that starts with active vehicle stock, adds annual imports, subtracts scrappage, and thereby derives the potential pool of cars entering resale each year. Results are cross-checked through selective bottom-up roll-ups of sampled dealer volumes multiplied by observed average selling prices. Key variables feeding the multivariate regression forecast include GDP per capita, expatriate population share, consumer credit growth, new-to-used price differential, and online listing velocity. Where dealer roll-ups showed gaps, three-year moving averages filled missing points before rerunning the model.

Data Validation & Update Cycle

Our team compares model outputs with bank loan disbursements, port entry data, and platform traffic signals, then flags anomalies for senior review. Reports refresh every twelve months, with interim updates if policy shifts or macro shocks materially alter our base case.

Why Mordor's Kuwait Used Car Baseline Commands Reliability

Published estimates often diverge because each firm carves borders differently, leans on unique price assumptions, or refreshes numbers on a slower cadence.

Key gap drivers in Kuwait include whether informal peer-to-peer trades are counted, how fast online channel growth is projected, and the inflation adjustment applied to imported vehicles landed in Kuwaiti dinar before conversion to dollars.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.65 billion (2025) | Mordor Intelligence | |

| USD 1.55 billion (2024) | Regional Consultancy A | Omits informal peer-to-peer sales; keeps average price constant across forecast window |

| USD 1.50 billion (2024) | Trade Journal B | Blends light commercial pickups with passenger cars and ignores online-only transactions |

The comparison shows that Mordor's disciplined scope setting, annual refresh, and dual validation steps deliver a balanced, transparent baseline that decision-makers can trace back to observable variables and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Kuwait used car market?

The Kuwait used car market is worth USD 1.91 billion in 2026 and is forecast to reach USD 3.94 billion in 2031, advancing at a 15.62% CAGR.

Which vehicle type sells the most in Kuwait’s used market?

Sedans lead with 37.80% market share because they balance prestige, comfort, and running cost advantages.

How fast are online channels growing compared with traditional dealerships?

Online platforms are expanding at 18.25% CAGR, market rate as buyers favor transparent, digital transactions.

Why do gasoline cars still dominate despite EV incentives?

Subsidized fuel prices and mature service infrastructure keep gasoline vehicles at 85.10% share, though EVs are the fastest-growing niche.

Page last updated on: