Oman EV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

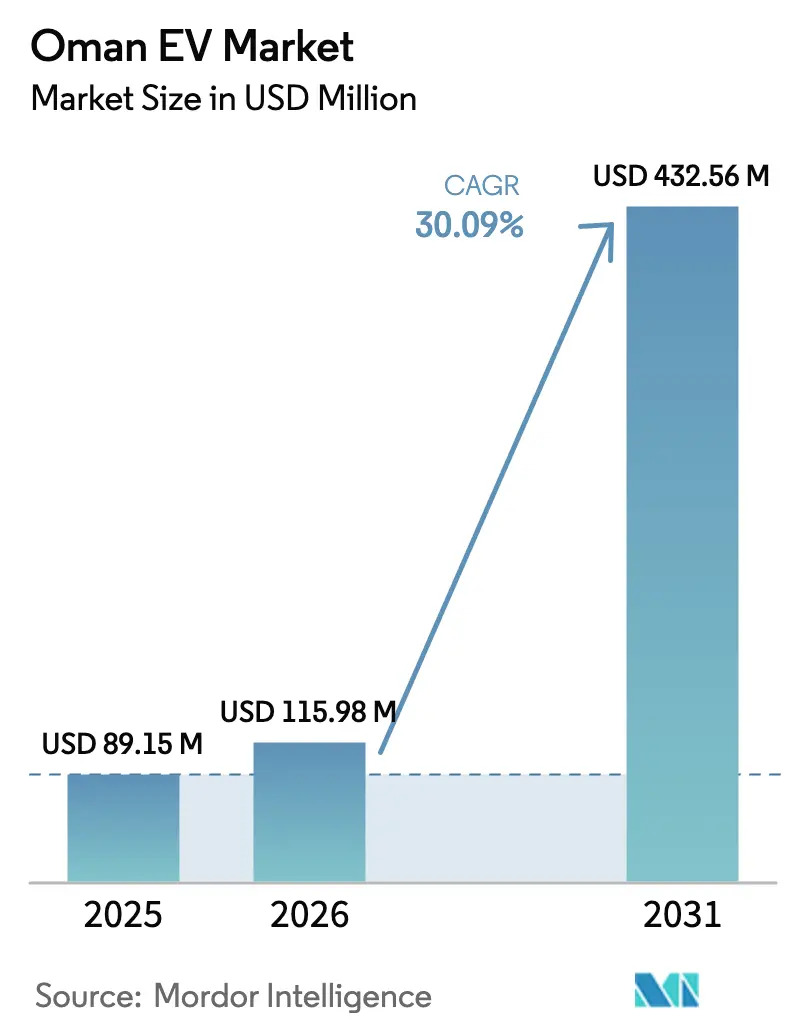

| Base Year Market Size (2025) | USD 89.15 Million |

| Market Size (2026) | USD 115.98 Million |

| Market Size (2031) | USD 432.56 Million |

| Growth Rate (2026 - 2031) | 30.09% CAGR |

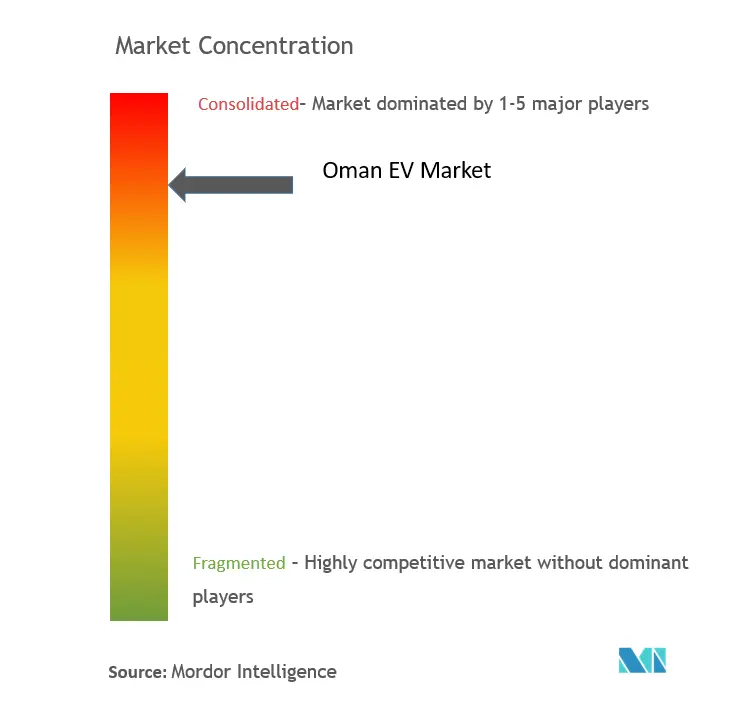

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman EV Market Analysis by Mordor Intelligence

The Oman EV Market size was valued at USD 89.15 million in 2025 and estimated to grow from USD 115.98 million in 2026 to reach USD 432.56 million by 2031, at a CAGR of 30.09% during the forecast period (2026-2031). Robust policy support under Vision 2040, falling battery prices, and rising foreign direct investment position the Oman Electric Vehicle market for rapid acceleration over the next five years. Strategic partnerships among automakers, energy companies, and zone authorities are reshaping the competitive landscape, while localized battery manufacturing is poised to cut supply-chain costs. Fleet electrification programs across logistics, public transit, and ride-hailing are broadening end-use demand, even as rural charging gaps and legacy fuel subsidies temper near-term momentum. The Oman Electric Vehicle market is becoming a pivotal plank in the Sultanate’s net-zero roadmap and a catalyst for industrial diversification.

Key Report Takeaways

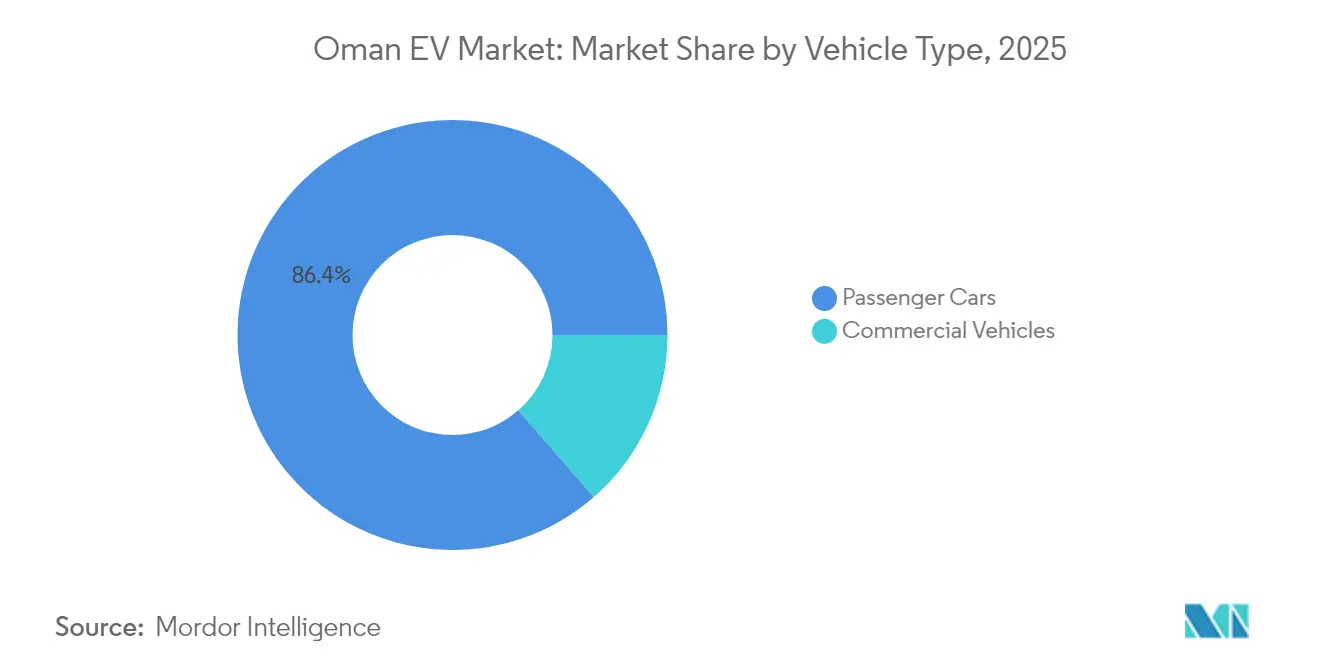

- By vehicle type, passenger cars led the Oman Electric Vehicle market share with 86.42% in 2025; commercial vehicles are set to record the fastest 30.21% CAGR to 2031.

- By drive-train technology, battery electric vehicles accounted for an 82.76% share of the Oman Electric Vehicle market size in 2025, while hybrid electric vehicles are advancing at a 30.17% CAGR through 2031.

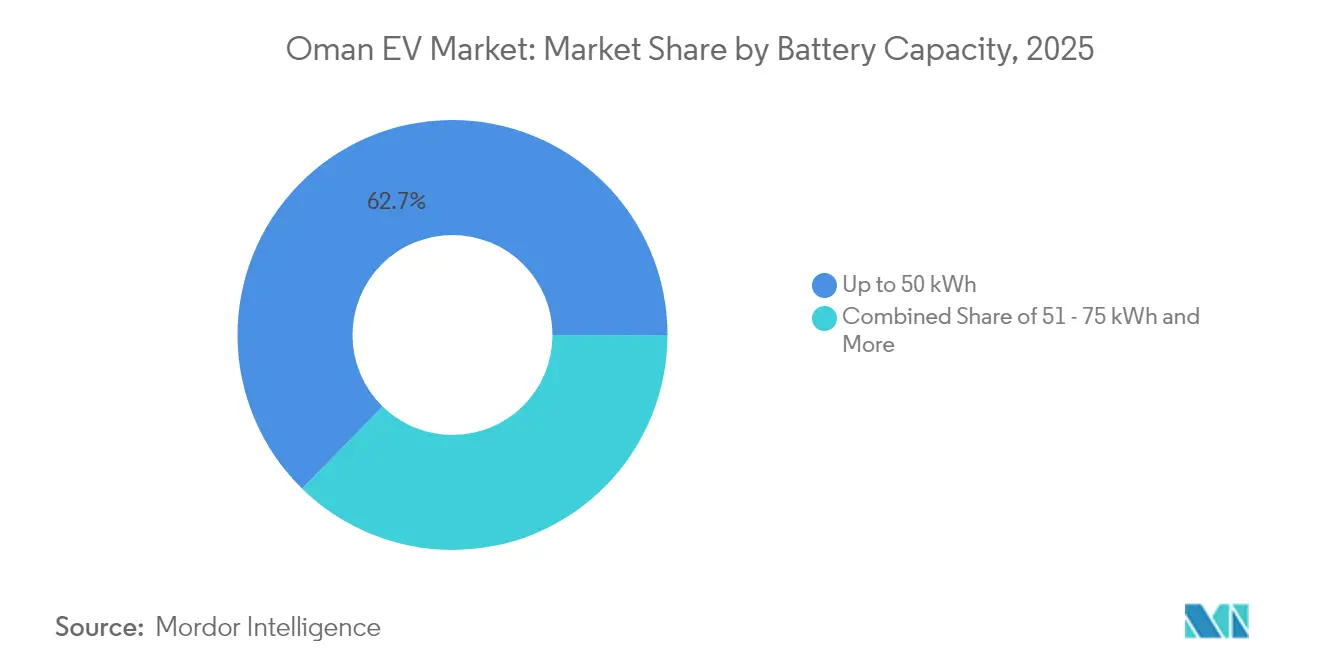

- By battery capacity, the up-to-50 kWh segment commanded 62.68% of the Oman Electric Vehicle market size in 2025; batteries above 75 kWh will grow at a 30.24% CAGR between 2026-2031.

- By end user, private individual owners held 71.64% of the Oman Electric Vehicle market share in 2025, whereas government & public-sector fleets are projected to expand at a 30.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman EV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling Battery Prices | +7.1% | National, spillover effects across GCC | Short term (≤ 2 years) |

| Net-Zero 2050 & 35% EV-Sales Target | +6.2% | National, with early adoption in urban centers | Long term (≥ 4 years) |

| Duqm SEZ Battery-EV Manufacturing | +5.4% | Regional, centered in Duqm with national distribution | Long term (≥ 4 years) |

| Government Mandate For EV Chargers | +4.8% | National, concentrated in Muscat, Al Batinah, Dhofar | Medium term (2-4 years) |

| Corporate / Fleet Electrification Momentum | +3.9% | National, concentrated in Muscat, Sohar, Duqm | Medium term (2-4 years) |

| Smart-Meter Rollout | +2.1% | National, phased deployment across governorates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Battery Prices & Influx of Affordable Chinese EVs

Over the past decade, plummeting lithium-ion battery costs have enabled Chinese automakers to price their electric vehicles on par with traditional internal combustion engine models. BYD now distributes five models through three Omani showrooms, while MG Motor leverages aggressive financing to challenge Japanese incumbents. Hunan Zhongke Electric’s anode-materials project at Sohar Port will supply 200,000 metric tons annually, shrinking transport costs and import duties for regional battery demand. Vertical integration covering battery cells, vehicle assembly, and bundled charging subscriptions further compresses retail prices, giving Chinese OEMs a first-mover advantage in the Oman Electric Vehicle market.

Net-Zero 2050 & 35% EV-Sales Target by 2035

Oman’s pledge to hit net-zero emissions by 2050 is anchored in a transport-sector plan that seeks one-third of EV sales by 2035. The Ministry of Transport, Communications and Information Technology estimates road transport emitted 15.9 Mt CO₂ in 2024; shifting to electric drivetrains is therefore pivotal to the national carbon budget [1]“Green Mobility Plan 2025,” Ministry of Transport, Communications and Information Technology, mtcit.gov.om .

Renewable-energy mandates that lift clean-power generation to significant levels by 2029 create a virtuous cycle in which zero-carbon electricity feeds zero-tailpipe vehicles. Public-sector role modeling is visible through Mwasalat’s deployment of electric and hydrogen buses and the Royal Oman Police’s dedicated EV license-plate scheme launched in May 2025. These visible commitments amplify investor interest in domestic battery plants and charging networks, knitting the mobility transition into Vision 2040’s diversification agenda.

Duqm SEZ Battery-EV Manufacturing Catalyst

The Duqm Special Economic Zone is evolving into an integrated hub that links upstream materials, cell production, and final-assembly lines. Mays Motors plans to assemble its ‘Mays Alive’ e-SUV in the zone, leveraging duty-free imports of components and proximity to Hunan Zhongke Electric’s future anode plant. This cluster effect is expected to reduce shipping costs, shorten lead times, and anchor skilled jobs inside Oman. Once operational, the local supply chain could shave several percentage points off landed-vehicle prices, bolstering the Oman Electric Vehicle market’s competitiveness against GCC imports.

Government Mandate for EV Chargers at All Fuel Stations

Mandatory installation of chargers at every fuel station transforms energy-retail economics across the Oman Electric Vehicle market. Shell opened a solar-powered hydrogen-electric hub near Muscat Airport in February 2025, integrating 130 kg per day of green hydrogen output with fast EV charging and signaling a move toward multi-energy forecourts [2]“Shell Opens First Hydrogen-Electric Station in Muscat,” Shell Oman, shell.com .

Porsche partnered with Shell to roll out eight DC stations and 125 AC destination chargers, allowing premium brands to fold infrastructure into customer-service propositions. The regulation leverages the existing fuel-station footprint to scale infrastructure quickly, lowering capital barriers and minimizing land-use friction. National standards overseen by the Authority for Public Services Regulation harmonize connector types and tariff structures, preventing fragmentation that could slow adoption. As coverage expands into secondary cities, charging accessibility will lift consumer confidence and catalyze fleet conversions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Public Charging Network | -3.2% | National, acute in rural and remote areas | Short term (≤ 2 years) |

| High Upfront EV Cost | -2.8% | National, particularly affecting price-sensitive segments | Medium term (2-4 years) |

| Extreme Heat Degrading Battery Performance | -2.1% | National, most severe in interior regions and summer months | Long term (≥ 4 years) |

| Electricity-Subsidy Phase-Out | -1.7% | National, disproportionate impact on residential charging users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Public Charging Network Beyond Muscat

Most rapid-charging stations are concentrated in the capital corridor, leaving rural highways underserved and heightening range anxiety for long-distance drivers. Commercial fleets face route-planning constraints and may retain diesel back-ups to avoid delivery disruptions. Shell and OQ Group prioritize high-traffic sites to maximize utilization, but this demand-driven approach risks a chicken-and-egg stalemate in less-populated governorates. Government co-funding programs are therefore essential to seed infrastructure in remote areas and de-risk private investment. A more evenly distributed network would unlock intercity tourism and logistics opportunities, broadening the Oman Electric Vehicle market beyond Muscat.

High Upfront EV Cost vs Subsidized ICE Fuel

Although lifetime operating costs favor EVs, Omani consumers still pay subsidized pump prices that blur the savings signal. Electricity-tariff reforms set to phase out cross-subsidies from 2026 will narrow the price gap and lift residential charging costs, partially eroding the EV value proposition. Limited financing products stretch payback periods for middle-income buyers, dampening conversion rates among the largest addressable segment. Policy levers such as interest-rate buy-downs and scrappage incentives could bridge the affordability gap until battery prices fall further.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Passenger cars held 86.42% of the Oman Electric Vehicle market share in 2025; however, commercial vehicles will post a 30.21% CAGR by 2031. The segment’s surge stems from predictable duty cycles that align with depot charging, allowing logistics operators to optimize battery utilization during nightly downtimes. Light vans used by e-commerce couriers illustrate the cost advantage, saving an estimated USD 2,500 in annual fuel and maintenance compared with diesel equivalents. Bus operators such as Mwasalat leverage route regularity to maximize regenerative braking and reduce brake-wear costs, reinforcing total-cost savings.

Logistics operators targeting last-mile delivery already account for a minimal of new commercial-vehicle EV registrations, a share likely to double by 2027 if fuel subsidies continue to ease. Government procurement policies that favor electric buses for urban routes further de-risk fleet investments. Commercial-segment momentum signals a structural shift in fleet strategy that will ripple across dealership inventories and after-sales ecosystems.

By Drive Train Technology: BEV Dominance Amid HEV Acceleration

Battery electric vehicles held an 82.76% share of the Oman Electric Vehicle market in 2025, reflecting supportive charging policies and improving range. However, hybrid electric vehicles are poised to expand at a 30.17% CAGR through 2031 as consumers outside Muscat hedge against limited fast-charging coverage. Plug-in hybrids provide daily electric commuting while retaining gasoline back-up for weekend trips, easing range anxiety. Models with advanced thermal-management systems maintain battery health in 50 °C summer heat, a critical requirement under Gulf conditions. OEMs, including Hyundai and Nissan, have begun offering eight-year, 160,000 km battery warranties tailored to regional climate stresses, enhancing buyer confidence.

Standardizing CCS-2 connectors and 150 kW DC charging protocols across public networks simplifies ownership, leveling the playing field for multiple drivetrain formats. Over time, as public chargers proliferate, BEVs are expected to consolidate dominance; yet in the interim, HEVs will serve as an on-ramp for hesitant buyers and rural drivers.

By Battery Capacity: Premium Range Expansion Accelerates

Up to 50 kWh packs anchor the mass Oman electric vehicle market with 62.68% share in 2025, powering compact cars and ride-hailing sedans optimized for urban stop-start traffic. Batteries above 75 kWh scale at a 30.24% CAGR and are increasingly featured in premium SUVs that tackle intercity journeys without mid-route charging. Buoyed by rising disposable incomes and a growing demand for road trips, the Oman Electric Vehicle market share is expected to grow significantly over the forecast period. Mid-tier 51-75 kWh batteries cater to family cars, balancing purchase price and range.

Localized anode production at Sohar is expected to shave fairly off battery import costs, narrowing retail price gaps between capacity tiers. High-temperature additives and liquid-cooling plates are becoming standard, extending cycle life despite desert conditions. Time-of-use tariffs introduced via smart meters incentivize overnight charging of large batteries, mitigating grid-peak pressure and lowering owner bills.

By End User: Government Leadership Catalyzes Private Adoption

Private individual owners commanded 71.64% of the Oman Electric Vehicle market share in 2025, buoyed by personal-import programs and expanding dealership networks. Government and public-sector fleets will grow at a 30.20% CAGR, setting benchmarks through high-visibility deployments and duty-cycle data transparency. Mwasalat’s 15 hydrogen vehicles underscore multi-technology experimentation, while municipal agencies task electric pickups with street-maintenance duties. EV plates introduced by the Royal Oman Police simplify enforcement of parking privileges and potential congestion-zone exemptions, incentivizing corporate fleets to switch early.

Ride-hailing leaders such as Otaxi are piloting EV-only driver tiers that promise lower commission rates in exchange for verified charging schedules, spurring gig-driver interest. Small-business owners increasingly lease light vans under pay-per-kilometer plans that bundle insurance and charging access. These service innovations, backed by soft-loan schemes from local banks, will broaden the consumer base and reduce the upfront cost hurdle.

Geography Analysis

Muscat anchors three-fifths of national EV registrations, courtesy of dense charging, higher incomes, and an early-adopter culture. The capital’s corridor from Seeb to Muttrah hosts more than 150 kW chargers, enabling intra-city fleets to complete multiple daily duty cycles. Sohar’s industrial cluster is emerging as a secondary pole; battery-materials investment will likely translate into early dealer discounts and job-linked vehicle-purchase programs. Duqm, with its special economic zone, is positioned to host assembly plants and logistics hubs, catalyzing adoption among port services and freight forwarders.

Interior governorates like Ad Dakhiliyah experience lower penetration due to sparse fast chargers and limited dealer coverage. The government's co-location of EV chargers with rural health clinics and police stations will bridge this gap by 2027. Dhofar’s tourism economy stands to benefit from quieter, low-emission transport along heritage routes, and pilot projects already equip eco-resorts with solar-powered chargers. Cross-border corridors with the UAE and Saudi Arabia are under study for CCS-2 interoperability, which would open GCC-wide road-trip possibilities and boost premium-segment demand.

Extreme heat gradients influence charging-station design; Muscat’s coastal humidity requires sealed electronics, while interior desert stations employ shaded canopies and high-flow liquid cooling. Grid-hardening investments synchronize with renewable-energy rollouts, ensuring stable voltage for high-power DC units. Overall, geographic disparities are narrowing as federal incentives and private capital converge on nationwide coverage, broadening the Oman Electric Vehicle market footprint beyond primary urban centers.

Competitive Landscape

Chinese OEMs such as BYD and MG Motor have seized price leadership, leveraging upstream battery control and modular platform sharing to undercut Japanese and European rivals. BYD’s five-model lineup now spans hatchbacks to luxury SUVs, while MG’s financing bundles appeal to first-time EV buyers. Tesla maintains technology cachet, but its higher price points confine volume to affluent urbanites. Nissan and Hyundai focus on durability, offering battery-health guarantees tailored for Gulf climates and co-developing roadside assistance programs with local insurers.

Energy-automaker alliances are emerging as decisive differentiators. Porsche’s tie-up with Shell secures 350 kW chargers along major highways, granting customers exclusive booking windows. OQ and Geely are evaluating joint-venture assembly at Duqm, potentially adding upstream integration to the competitive mix. Local start-up Mays Motors draws on government grants to prototype an e-SUV designed for desert performance, eyeing fleet contracts with tourism operators.

Service innovation is turning into a battlefield. Subscription-based battery swapping, introduced by Nio in the neighboring UAE, is being market-tested in Oman for taxi fleets. Dealers compete on bundled rooftop solar packages and extended service plans, including mobile charger vans for roadside support. As the top five brands control under two-fifths of national EV sales, competition remains vigorous, and customer switching costs are low, sustaining aggressive pricing in the Oman Electric Vehicle market.

Oman EV Industry Leaders

Porsche AG

Audi AG

BMW AG

Volvo Car Group

MG Motor (SAIC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hunan Zhongke Electric confirmed a USD 1.1 billion lithium-ion anode-materials facility at Sohar Port and Free Zone with 200,000 metric tons annual capacity.

- May 2025: Royal Oman Police launched mandatory yellow and red license plates for all electric vehicles, creating a unique identifier framework.

- February 2025: Oman Shell opened the nation’s first solar-powered green hydrogen and EV fast-charging hub near Muscat International Airport.

Oman EV Market Report Scope

An electric vehicle (EV) is a vehicle powered primarily by electricity. The electricity required is stored in rechargeable batteries. In some models, it is supplied by an external source, such as a plug-in charger. EVs are considered ideal as they produce zero tailpipe emissions and offer a sustainable alternative to traditional ICE vehicles.

The Omani EV market is segmented by vehicle type, propulsion type, battery type, range, drive type, battery capacity, and end user. By vehicle type, the market is segmented into two-wheel, passenger car, and commercial vehicle. By propulsion type, the market is segmented into battery electric vehicles (BEV), hybrid electric vehicles (HEV), and plug-in hybrid electric vehicles (PHEV). By battery type, the market is segmented into LFP, NMC, and other battery types. By range, the market is segmented as upto 150 km, 151-300 km, and above 300 km. By drive type, the market is segmented as all-wheel drive, front-wheel drive, and rear-wheel drive. By battery capacity, the market is segmented as less than 20 kwh, 20-40 kwh, 40-60 kwh, 60-100 kwh, and above 100 kwh. By end user, the market is segmented as shared mobility providers, government organizations, and personal users. The report offers market size and forecast in value (USD) for all the above segments.

| Passenger Car | Hatchback |

| Sedan | |

| Sport-Utility Vehicle | |

| Multi-Purpose Vehicle | |

| Commercial Vehicle | Light Commercial Vehicles |

| Medium Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Buses & Coaches |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Up to 50 kWh |

| 51 – 75 kWh |

| Above 75 kWh |

| Private Individual Owners | |

| Commercial Fleet Operators | Ride-hailing & Car-sharing |

| Logistics & Delivery | |

| Government & Public-Sector Fleets |

| By Vehicle Type | Passenger Car | Hatchback |

| Sedan | ||

| Sport-Utility Vehicle | ||

| Multi-Purpose Vehicle | ||

| Commercial Vehicle | Light Commercial Vehicles | |

| Medium Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Buses & Coaches | ||

| By Drive Train Technology | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| By Battery Capacity | Up to 50 kWh | |

| 51 – 75 kWh | ||

| Above 75 kWh | ||

| By End User | Private Individual Owners | |

| Commercial Fleet Operators | Ride-hailing & Car-sharing | |

| Logistics & Delivery | ||

| Government & Public-Sector Fleets | ||

Key Questions Answered in the Report

What is the current value of the Oman Electric Vehicle market?

The market is valued at USD 115.98 million in 2026 and is projected to grow rapidly through 2031.

What CAGR is forecast for electric vehicles in Oman through 2031?

A robust 30.09% CAGR is expected between 2026 and 2031.

Which vehicle type is growing fastest in Oman?

Commercial vehicles, including buses and delivery vans, are projected to expand at a 30.21% CAGR from 2026 to 2031.

How does government policy support EV adoption in Oman?

Policies mandate chargers at every fuel station, set a 35% EV-sales goal by 2035, and roll out dedicated EV license plates, all accelerating infrastructure and consumer confidence.

Where are most public EV chargers located in Oman?

The highest density is in the Muscat Capital Area, though expansion to Sohar and Duqm is underway.

Page last updated on: