Oligonucleotide Synthesis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

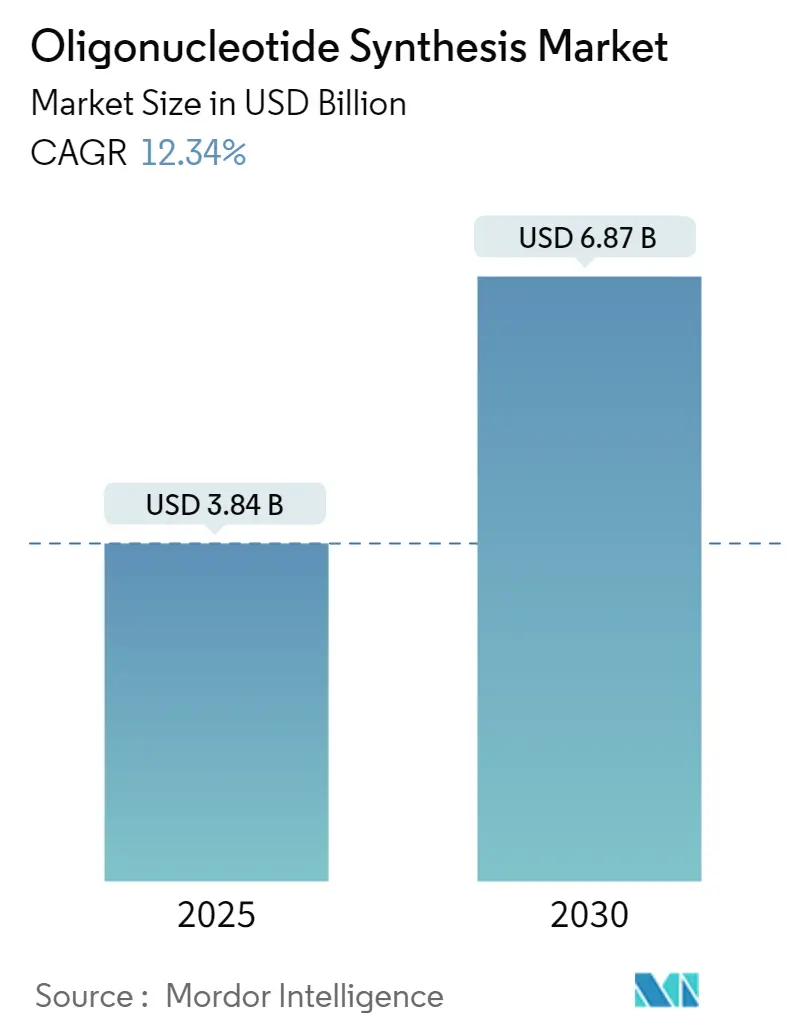

| Market Size (2025) | USD 3.84 Billion |

| Market Size (2030) | USD 6.87 Billion |

| Growth Rate (2025 - 2030) | 12.34% CAGR |

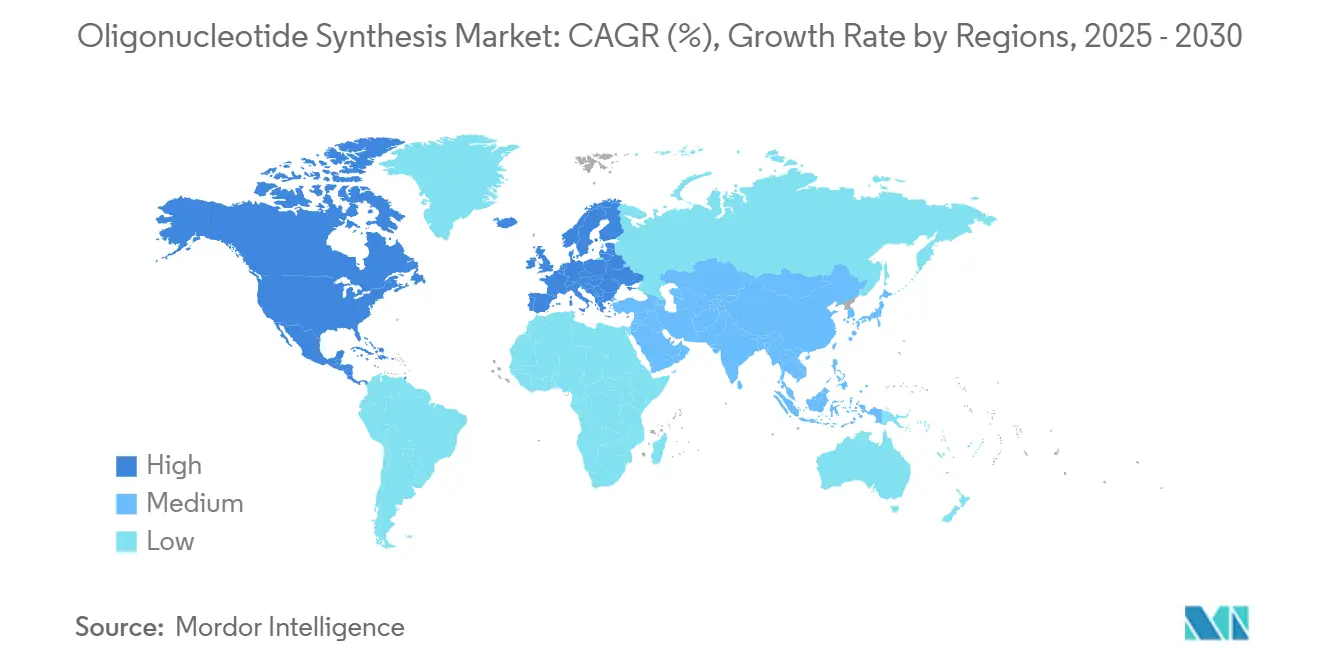

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oligonucleotide Synthesis Market Analysis by Mordor Intelligence

The oligonucleotide synthesis market reached USD 3.84 billion in 2025 and is forecast to climb to USD 6.87 billion by 2030, advancing at a 12.34% CAGR as therapeutic breakthroughs accelerate demand. Enzymatic platforms that create longer, cleaner strands without hazardous reagents are reshaping the oligonucleotide synthesis market by challenging four decades of phosphoramidite dominance. Government grants, notably the NIH’s RNA-focused USD 15.4 million program, catalyze new production methods while contract manufacturers scale capacity to meet rising pharmaceutical outsourcing needs. Clinical approvals underscore momentum: 22 nucleic-acid drugs cleared regulators by late 2023, and four more won clearance in 2024, pulling the oligonucleotide synthesis market beyond its research-reagent roots into industrial-scale biologics. Environmental scrutiny of PFAS-linked reagents pressures legacy processes, amplifying interest in enzymatic alternatives that reduce waste while complying with evolving regulations.

Key Report Takeaways

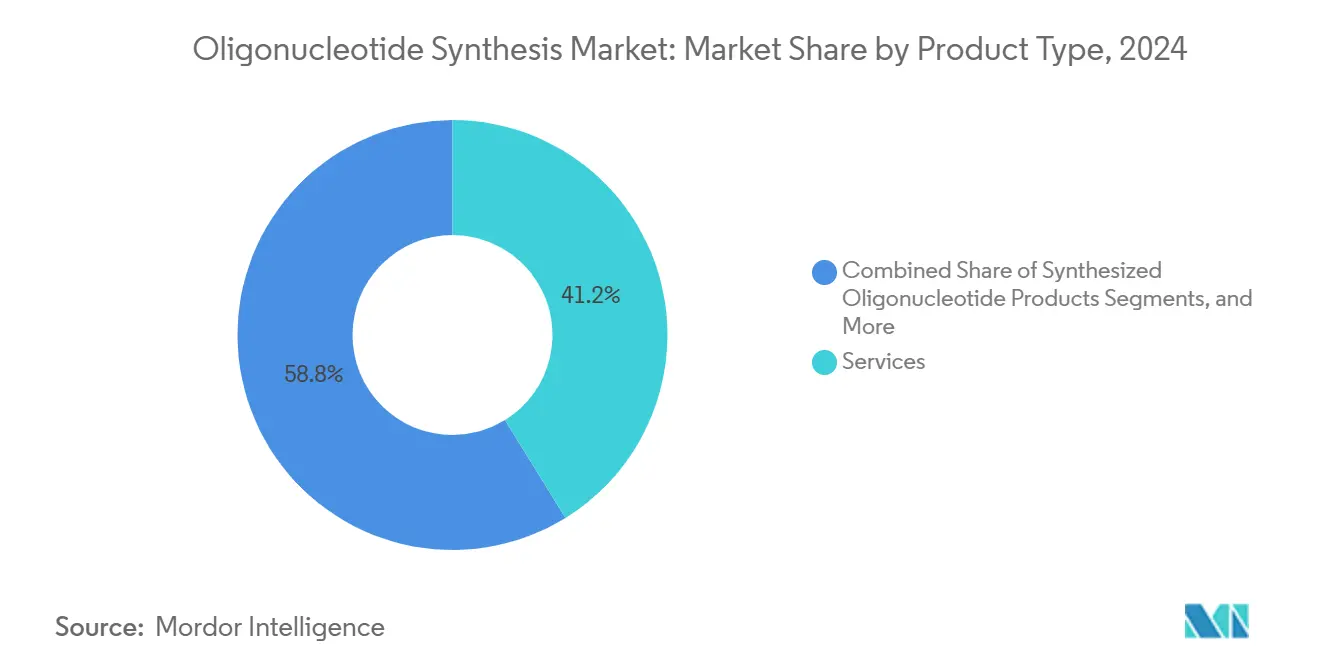

- By product type, services accounted for 41.25% revenue share of the oligonucleotide synthesis market in 2024, while synthesized oligonucleotide products are positioned to post the fastest growth through 2030.

- By chemistry, DNA dominated with 43.45% of oligonucleotide synthesis market share in 2024; RNA is on course to narrow the gap as mRNA and CRISPR pipelines mature.

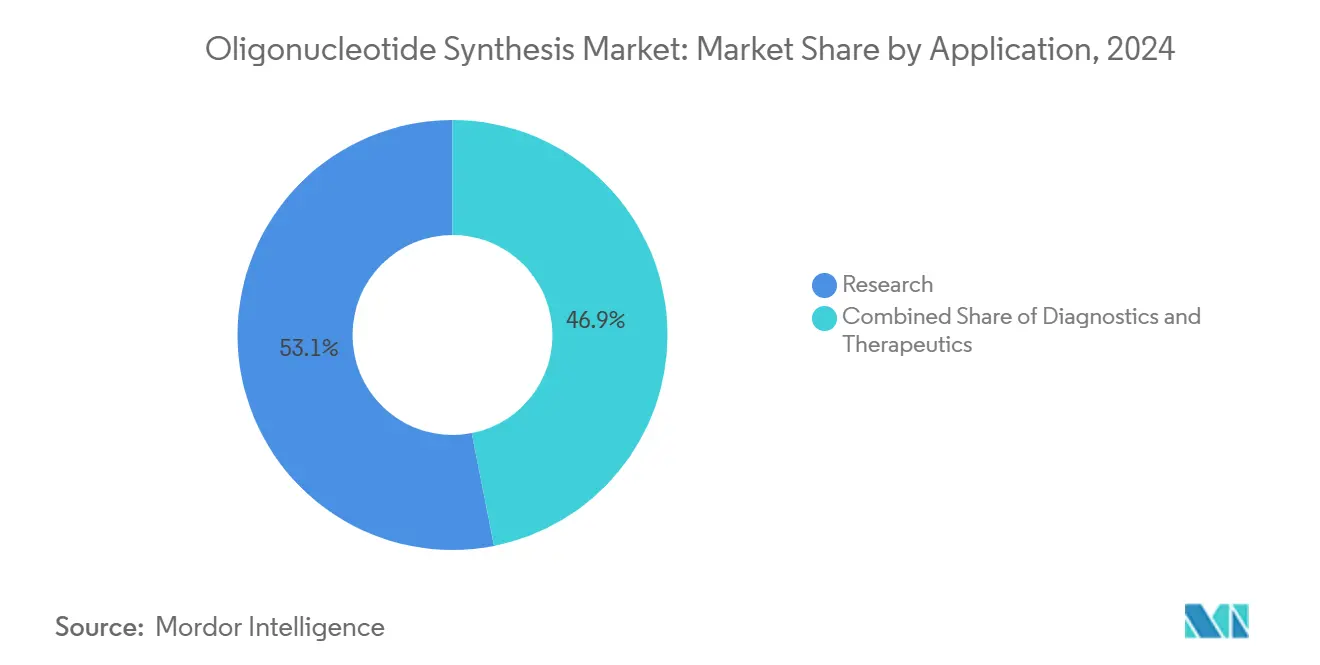

- By application, research held 53.15% share of the oligonucleotide synthesis market size in 2024, yet therapeutics already command premium pricing and are expanding the fastest.

- By end-user, academic institutes generated 72.81% volume in 2024, while pharmaceutical and biotechnology companies delivered the highest value through clinical-grade contracts.

- By geography, North America led with 42.81% share in 2024, whereas Asia-Pacific shows the steepest upward curve on the back of USD 4 billion in Chinese funding rounds and multi-hundred-million-dollar capacity additions.

Global Oligonucleotide Synthesis Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government funding surge post-pandemic | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Clinical adoption of synthesized oligos in advanced diagnostics | +1.8% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Expansion of contract development & manufacturing (CDMO) capacity | +1.5% | Global, with major investments in Asia-Pacific | Medium term (2-4 years) |

| Patent cliffs driving next-gen antisense/RNA therapies | +1.2% | North America and Europe primarily | Long term (≥ 4 years) |

| Micro-array based ultrahigh-throughput synthesis platforms | +0.9% | Global, technology centers in North America | Short term (≤ 2 years) |

| Enzymatic, benchtop "DNA printer" launch pipelines | +0.7% | North America and Europe initially | Medium term (2-4 years) |

Source: Mordor Intelligence

Government Funding Surge Post-Pandemic

Federal investment elevated oligonucleotides to critical-infrastructure status for pandemic preparedness and precision medicine. The NIH earmarked USD 15.4 million for RNA research that improves microfluidic long-strand synthesis and nanopore sequencing, while its Technology Development Coordinating Center secures USD 1.5 million annually through 2029 to refine nucleic-acid production systems [1]National Human Genome Research Institute, “RNA Technology Development Funding,” genome.gov. Parallel European grants create a trans-Atlantic push to localize supply chains, reinforce biosecurity, and accelerate oligonucleotide standards that underpin therapeutic approvals.

Clinical Adoption of Synthesized Oligos in Advanced Diagnostics

Fresh FDA guidance issued in 2024 clarifies quality requirements, accelerating diagnostic assay rollouts and boosting the oligonucleotide synthesis market [2]FDA, “Drug Development Guidance for Nucleic Acid–Based Therapeutics,” fda.gov. GalNAc-conjugated antisense oligos received their first approval, confirming precise delivery chemistries that rely on high-fidelity synthesis. Personalized “N-of-1” treatments now demand rapid micro-batch production, prompting service providers to integrate design-to-clinic workflows that transform how rare-disease patients are treated.

Expansion of Contract Development & Manufacturing (CDMO) Capacity

Agilent’s USD 725 million build-out, WuXi STA’s 27 production lines, and MilliporeSigma’s EUR 300 million Korean facility collectively double global therapeutic output, signalling how CDMOs anchor the oligonucleotide synthesis market. Outsourced operations supply GMP-grade strands faster than in-house teams can qualify equipment, positioning CDMOs as strategic allies for drug sponsors racing toward commercialization.

Patent Cliffs Driving Next-Gen Antisense/RNA Therapies

The expiry of foundational antisense patents invites new entrants, while high-profile CRISPR disputes exemplified by Broad Institute vs. CVC reshape licensing flows without dimming investor enthusiasm. Recent rulings that invalidated select guide-RNA claims open freedom-to-operate for smaller firms, lifting barriers that once limited oligonucleotide portfolios.

Enzymatic, Benchtop “DNA Printer” Launch Pipelines

DNA Script’s SYNTAX, Ansa’s 1,005-base record, and Telesis Bio’s Gibson SOLA highlight how template-free polymerases deliver longer strands with fewer toxic reagents, aligning production with rising sustainability mandates. Wider availability sparks biosecurity reviews, leading to new sequence-screening frameworks that balance open innovation against dual-use risks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent high purification & QC costs | -1.4% | Global, particularly affecting smaller players | Long term (≥ 4 years) |

| IP disputes around CRISPR / gene-editing sequences | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Supply bottlenecks for specialty phosphoramidites | -0.6% | Global, with Asia-Pacific supply chain concentration | Short term (≤ 2 years) |

| PFAS-linked environmental regulations on fluorinated nucleic acids | -0.4% | Europe and North America regulatory focus | Medium term (2-4 years) |

Source: Mordor Intelligence

Persistent High Purification & QC Costs

Therapeutic-grade purification can consume 60-70% of manufacturing budgets as high-performance liquid chromatography remains the standard for removing truncated strands and reactive impurities. Yield erosion, demonstrated by 30-mer sequences falling to 55% at 98% coupling efficiency, forces over-production that inflates reagent use and waste disposal, stressing smaller players that lack economies of scale.

IP Disputes Around CRISPR / Gene-Editing Sequences

Overlapping patent claims create legal landmines where a single guide RNA may trigger multiple licenses, driving up costs and delaying launches. Although some patents were invalidated in 2024, ongoing appeals sustain uncertainty, prompting conservative sequence designs that narrow the addressable therapeutic space.

Segment Analysis

By Product Type: Services Anchor Outsourcing Momentum

Services generated 41.25% of overall 2024 revenue as pharmaceutical sponsors prioritized turnkey solutions that compress development timelines. This dominance confirms the oligonucleotide synthesis market preference for external capacity that bundles synthesis, purification, and regulatory support into single-vendor contracts. The model suits high-value clinical batches where each lot must pass stringent GMP audits. Reagent consumption scales in parallel, offering steady annuity streams for consumables providers even as benchtop enzymatic platforms appear.

Looking ahead, service revenue is expected to outpace product sales because compliance complexity continues to rise. CDMOs spread analytical costs across dozens of clients, whereas individual biotechs seldom justify multi-million-dollar cleanroom investments. Equipment suppliers respond with higher-throughput instruments such as 384-well synthesizers that cut per-oligo costs, yet most machines will still land inside service facilities rather than drug-maker labs. The oligonucleotide synthesis market size expansion therefore tracks CDMO build-outs, while specialized benchtop systems address niche rapid-turnaround needs within research cores.

Note: Segment shares of all individual segments available upon report purchase

By Chemistry: DNA Holds Sway as RNA Accelerates

DNA retained 43.45% command of the oligonucleotide synthesis market in 2024 thanks to mature phosphoramidite protocols that deliver >99% coupling efficiency for strands up to 120 bases. RNA’s 13.78% share is set to climb as mRNA vaccines, CRISPR guides, and siRNA drugs gain clinical traction. Enzymatic synthesis favors RNA because aqueous enzymology avoids the acidic deprotection steps that degrade 2'-hydroxyl groups, extending feasible lengths beyond 200 bases without capping agents.

Modified backbones such as phosphorothioates and 2'-O-methyl riboses already dominate antisense and RNAi therapeutics, commanding multiples of DNA’s price per base. Niche chemistries (LNA, PNA, Morpholino) occupy small slices yet supply indispensable tools for stability-critical indications. As therapeutic demand intensifies, production shifts toward GMP-compliant enzymes and greener solvents, lifting the oligonucleotide synthesis market share of RNA while DNA remains foundational for gene-assembly and PCR primer volumes.

By Application: Research Volume Meets Therapeutic Value

Research retained 53.15% of 2024 activity, but therapeutics, with 14.51%, drive the lion’s share of profit as each clinical oligo can bill at 10- to 20-fold the price of a laboratory primer. Twenty-two approved nucleic-acid medicines by 2023 validated the modality, while four 2024 approvals confirm a steady pipeline. Companion diagnostics marry drug and test, doubling sequence orders per indication and tightening links between therapeutic and diagnostic markets.

From 2025 onward, therapeutic CAGR is positioned to outrun research volumes. Patent expiries on first-generation antisense constructs open room for rare-disease developers, and venture funding flows into start-ups crafting personalized oligos. Consequently, the oligonucleotide synthesis market size attached to therapeutics will expand faster than any other segment, even if absolute unit counts stay below research quantities.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Academic Institutes Lead Volume, Pharma Captures Margin

Academic institutions drove 72.81% of sequences in 2024, underlining how discovery science still underpins oligonucleotide demand. University labs churn through primers and probes for CRISPR screens, transcriptomics, and synthetic biology. Yet revenue skews toward pharmaceutical and biotechnology companies, which represented only 14.21% of volume but booked the majority of dollar value through GMP projects.

Hospitals and diagnostic labs are the fastest-growing cohort as genetic tests migrate from central reference labs to point-of-care settings. This wave feeds the oligonucleotide synthesis market with medium-scale orders demanding medical-grade quality but not full GMP rigor, carving out a mid-tier service niche. As precision-medicine trials proliferate, academic–industry collaborations will deepen, funneling grant-backed discoveries into clinical pipelines that rely on CDMO strength.

Geography Analysis

North America captured 42.81% share in 2024, propelled by FDA guidance that de-risks development and by NIH funding that subsidizes platform innovation. United States-based firms leverage integrated ecosystems spanning venture capital, academic excellence, and manufacturing know-how. Canada benefits from proximity, with emerging GMP suites attracting cross-border projects. Mexico’s low-cost sites are beginning to draw reagent packaging and QC functions, though synthesis remains concentrated further north.

Asia-Pacific held 14.71% yet registers the highest growth trajectory. Chinese sponsors poured more than USD 4 billion into small-nucleic-acid ventures during 2024, while provincial governments fast-tracked plant permits to localize supply. South Korea secured EUR 300 million from MilliporeSigma for a duplex biologics campus, and Singapore’s regulatory certainty lured multi-line expansions from WuXi STA and GenScript. India’s “Make in India” drive birthed CoDx-CoSara’s new Gujarat facility, signaling regional intent to rise up the value chain.

Europe remains an innovation powerhouse but encounters PFAS-related chemical restrictions that complicate legacy phosphoramidite workstreams[3]American Chemical Society, “PFAS Restrictions Push Greener Oligonucleotide Chemistry,” pubs.acs.org. Germany’s BioSpring tripled capacity and added 1,500 jobs, offsetting supply headaches by pioneering fluorine-free reagents. The United Kingdom’s Catapult centers pair public grants with biotech spin-outs, while France cultivates enzymatic start-ups. Elsewhere, Brazil and Argentina lead Latin American uptake of genetic therapies, and Gulf states build precision-medicine hubs anchored by imported oligonucleotides, foreshadowing localized production over the next decade.

Competitive Landscape

The oligonucleotide synthesis market shows moderate fragmentation. Thermo Fisher, Agilent, and Danaher’s Integrated DNA Technologies wield global plants, broad reagent portfolios, and automated analytics. Agilent’s USD 725 million capacity upgrade and BIOVECTRA acquisition illustrate how scale secures high-value therapeutic contracts. Twist Bioscience, DNA Script, and Ansa Biotechnologies disrupt with enzymatic innovations that extend sequence length and cut solvent use, reshaping buyer preference toward greener chemistry.

Strategic M&A quickens: Merck’s USD 600 million Mirus Bio purchase adds lipid nanoparticle know-how, while Thermo Fisher’s USD 3.1 billion deal for Olink expands proteomic adjacency. Smaller firms carve niches in personalized medicine; Aldevron and IDT completed a bespoke CRISPR therapeutic from design to clinic in six months, demonstrating agile pathways big incumbents now chase. Patent maneuvers remain potent weapons, evidenced by Editas-Vertex licensing pacts that lock down CRISPR components even amid legal flux. Environmental regulation and supply-chain localization further complicate competition, rewarding players that pre-emptively adapt chemistry and geographic footprint.

Oligonucleotide Synthesis Industry Leaders

-

Thermo Fisher Scientific

-

Agilent Technologies

-

Merck KGaA

-

Bio-Synthesis Inc

-

Eurofins Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Astellas Pharma obtained FDA approval to remove dosing-duration limits from IZERVAY (avacincaptad pegol) for geographic atrophy.

- February 2025: India’s Jawaharlal Nehru Centre hosted the first Regional Nucleic Acid Therapeutics Meeting, uniting academia and industry on oligonucleotide drug topics.

- January 2025: Maravai LifeSciences bought Molecular Assemblies assets, bringing Fully Enzymatic Synthesis into TriLink BioTechnologies.

- December 2024: Co-Dx and CoSara Diagnostics opened an oligonucleotide synthesis facility in Ranoli, India, under the “Make in India” banner.

Global Oligonucleotide Synthesis Market Report Scope

Oligonucleotide synthesis is the chemical synthesis of relatively short fragments of nucleic acids with a defined chemical structure (sequence).

The Oligonucleotide Synthesis Market is Segmented by Product Type (Synthesized Oligonucleotide Products, Reagents, Equipment, and Services), Application (Research, Therapeutics, and Diagnostics), End-user (Academic Research Institutes, Pharmaceutical and Biotechnology Companies, and Hospital and Diagnostic Laboratories), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product Type | Synthesized Oligonucleotide Products | ||

| Reagents | |||

| Equipment | |||

| Services | |||

| By Chemistry | DNA (Phosphoramidite) | ||

| RNA | |||

| LNA / PNA / Morpholino | |||

| By Application | Research | ||

| Diagnostics | |||

| Therapeutics | |||

| By End-user | Academic Research Institutes | ||

| Pharmaceutical & Biotechnology Companies | |||

| Hospital & Diagnostic Laboratories | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of APAC | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of MEA | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Synthesized Oligonucleotide Products |

| Reagents |

| Equipment |

| Services |

| DNA (Phosphoramidite) |

| RNA |

| LNA / PNA / Morpholino |

| Research |

| Diagnostics |

| Therapeutics |

| Academic Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Hospital & Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

How big is the Oligonucleotide Synthesis Market?

The Oligonucleotide Synthesis Market size is expected to reach USD 3.84 billion in 2025 and grow at a CAGR of 12.34% to reach USD 6.87 billion by 2030.

What is driving the rapid growth of the oligonucleotide synthesis market?

Strong therapeutic pipelines, enzymatic production advances, and expanding CDMO capacity collectively fuel a 12.34% CAGR through 2030.

Who are the key players in Oligonucleotide Synthesis Market?

Thermo Fisher Scientific, Agilent Technologies, Merck KGaA, Bio-Synthesis Inc and Eurofins Scientific are the major companies operating in the Oligonucleotide Synthesis Market.

Which is the fastest growing region in Oligonucleotide Synthesis Market?

Asia-Pacific, led by China and South Korea, records the steepest growth thanks to multi-billion-dollar funding rounds and new manufacturing plants.