Oilfield Scale Inhibitor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

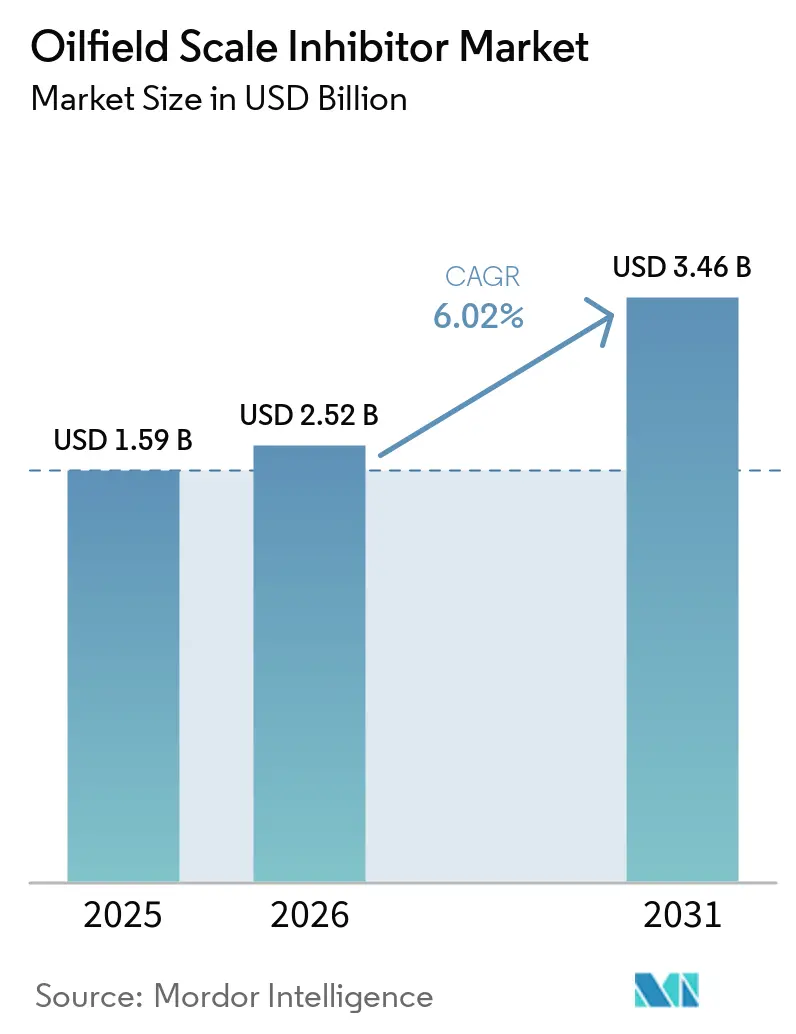

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oilfield Scale Inhibitor Market Analysis by Mordor Intelligence

The Oilfield Scale Inhibitor Market size is expected to increase from USD 1.59 billion in 2025 to USD 2.52 billion in 2026 and reach USD 3.46 billion by 2031, growing at a CAGR of 6.02% over 2026-2031. As offshore tiebacks expand and squeeze treatments gain traction, stricter regulations on produced water are driving up the demand for threshold chemistries in shale, pre-salt, and mature oil fields. Integrated service models, which combine digital monitoring with chemical supply, are bolstering the oilfield scale inhibitor market. This approach received a notable boost after SLB acquired ChampionX. Meanwhile, as the Permian Basin produces substantial water volumes daily and the Asia-Pacific region faces an annual decline in mature fields, effectively managing brine and dosing inhibitors becomes crucial for cost efficiency. While phosphonate blends dominate due to their high-temperature stability, environmentally friendly polymeric alternatives are on the rise. This transition is primarily fueled by the stringent phosphorus discharge limits imposed by EPA NPDES permits in the Gulf of Mexico.

Key Report Takeaways

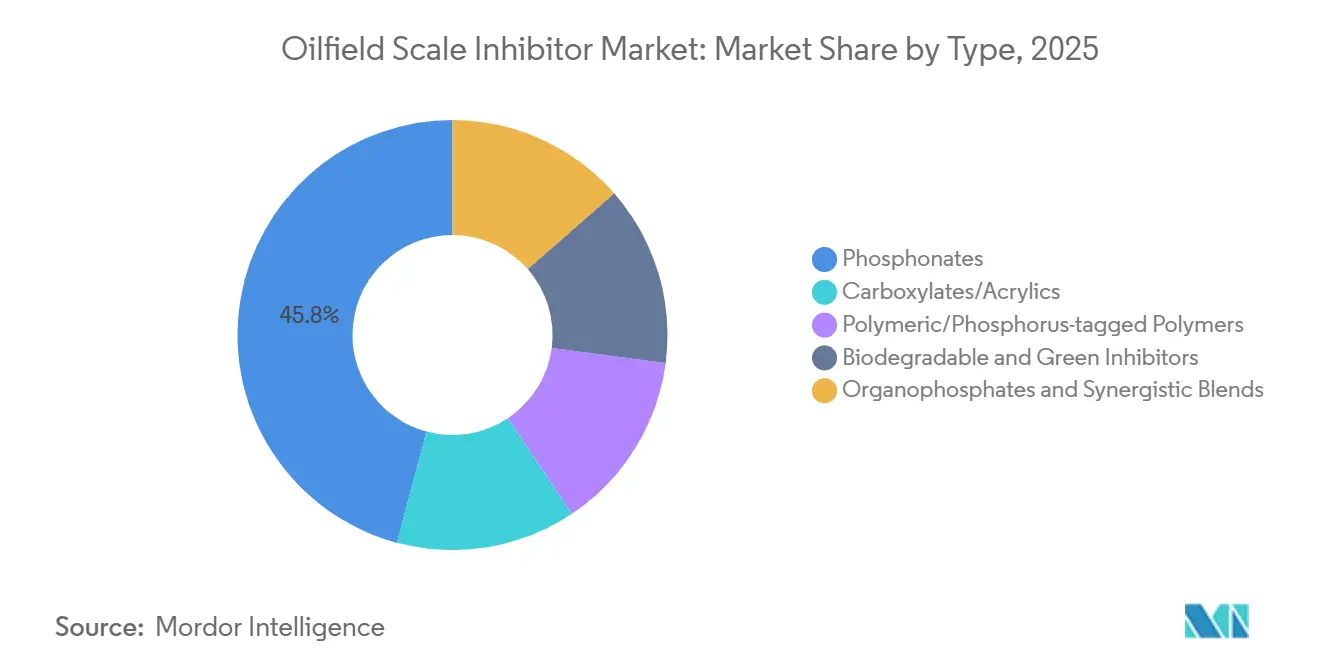

- By type, phosphonates led with 45.82% of the oilfield scale inhibitor market share in 2025, and phosphonates are projected to expand at a 6.83% CAGR from 2026 to 2031.

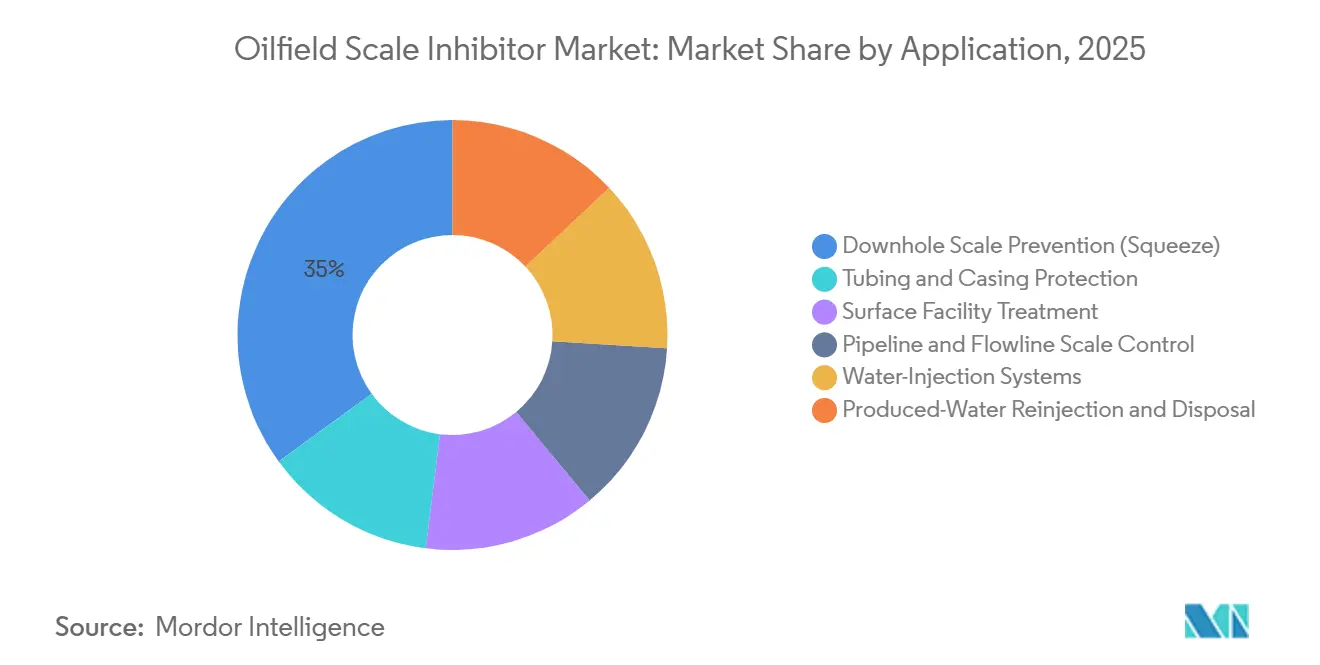

- By application, downhole scale prevention (squeeze) led with 35.01% of the oilfield scale inhibitor market share in 2025; water-injection systems are projected to expand at a 6.92% CAGR from 2026 to 2031, the fastest growth among all segments.

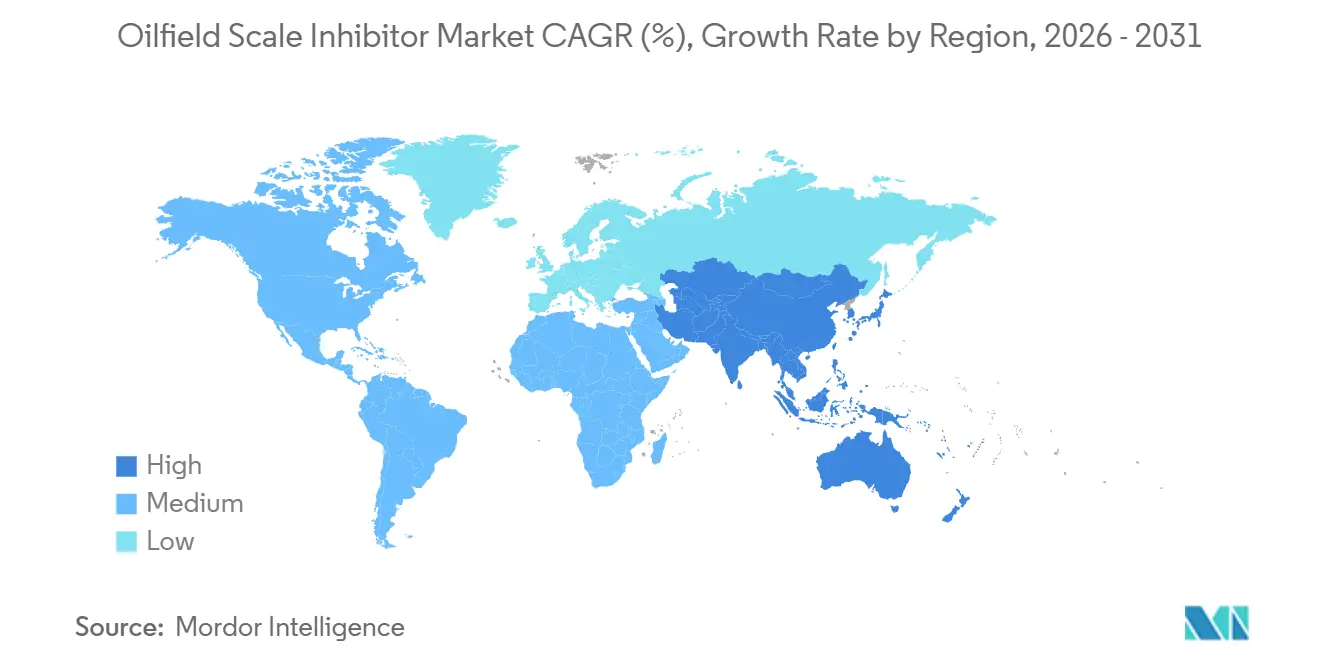

- By geography, North America accounted for 36.11% of the oilfield scale inhibitor market size in 2025, while Asia-Pacific is advancing at a 6.79% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oilfield Scale Inhibitor Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for scale control in mature fields | +1.8% | Global, concentrated in North America (Permian), ASEAN (Indonesia, Malaysia), North Sea | Medium term (2-4 years) |

| Expansion of offshore exploration and pipeline activities | +1.5% | Global, with emphasis on Brazil pre-salt, China offshore, Gulf of Mexico, West Africa | Long term (≥4 years) |

| Adoption of EOR techniques elevates chemical consumption | +1.2% | Middle East (Saudi Arabia, UAE, Kuwait), ASEAN (Indonesia), North America (CO₂ EOR in Permian) | Medium term (2-4 years) |

| Growth in unconventional oil resources | +0.9% | North America (Permian, Eagle Ford), South America (Argentina Vaca Muerta) | Short term (≤2 years) |

| Real-time digital inhibitor dosing and monitoring | +0.4% | Global, early adoption in North America and the Middle-East | Long term (≥4 years) |

| Shift toward produced-water reinjection in water-scarce regions | +0.7% | Middle East (Saudi Arabia, UAE, Kuwait), North Africa, parts of ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Scale Control in Mature Fields

Operators face increasing challenges in managing the growing volumes of brine, which have a high potential for scaling, as mature reservoirs worldwide experience rising water cuts. In the Permian Basin, operators generate significant volumes of produced water daily, with water-to-oil ratios ranging from 3:1 to 12:1[1]Produced Water Society, “Permian Basin Produced Water Management,” producedwatersociety.com. As they reinject and recycle this water, they inadvertently concentrate carbonate and sulfate ions, leading to a heightened reliance on advanced squeeze programs. While the Asia-Pacific region has grappled with a sustained production decline, intensifying workover and Enhanced Oil Recovery (EOR) activities, Norway's newly tapped North Sea fields have adopted a dual approach - pairing 18-24 month squeeze cycles with online residual analyzers to curtail downtime on floating facilities. Given these dynamics, the oilfield scale inhibitor market has emerged as a cost-effective safeguard, protecting against potential million-dollar daily losses stemming from scale-induced outages.

Expansion of Offshore Exploration and Pipeline Activities

By 2025, Brazil's pre-salt output surged, reaching millions of barrels per day. Each new FPSO now features inhibitor packages specifically designed for CO₂-rich fluids, spanning 18-kilometer tiebacks. CNOOC increased its production, achieving millions of barrels of oil equivalent per day. The company adopted seawater injection, a strategy that increases the risk of calcium-sulfate scaling in subsea manifolds. In the West-African region, deepwater systems face similar challenges, relying on long-residence squeeze chemistries that are expected to enhance revenue in the oilfield scale inhibitor market during the forecast period of 2026–2031.

Adoption of EOR Techniques Elevating Chemical Consumption

In Indonesia, investments in polymer floods at Rantau and Minas have led to a heightened brine salinity and pH levels[2]ASEAN Centre for Energy, “ASEAN Oil and Gas Updates 2024,” aseanenergy.org. As a result, formulators are pairing phosphonate cores with dispersant polymers to enhance efficacy. Meanwhile, Saudi Aramco and ADNOC are making substantial investments in CO₂ capture and injection hubs. In these environments, acid-stable carboxylate inhibitors are used alongside traditional aminomethylene phosphonates. These initiatives are expanding volume opportunities in the oilfield scale inhibitor market.

Growth in Unconventional Oil Resources

Argentina's Vaca Muerta is forecast to witness multiple fracture stages. Each stage utilizes proppant-coated solid inhibitors that release active molecules for nearly a year. Concurrently, North American shale operators, despite recycling all their produced water, face challenges with the total dissolved solids reaching elevated levels. This issue intensifies barium-sulfate precipitation, leading to a surge in demand for oilfield scale inhibitors.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude prices curbing chemical budgets | -1.3% | Global, acute in North America shale, Latin America independents | Short term (≤2 years) |

| Tightening discharge regulations on phosphorus and heavy metals | -0.8% | North America (EPA), Europe (ECHA/REACH), Asia-Pacific (China MEE) | Medium term (2-4 years) |

| All-electric subsea systems are reducing chemical injection points | -0.5% | Global offshore, concentrated in Norway, Brazil, Gulf of Mexico | Long term (≥4 years) |

| Persistent supply-chain risk for phosphonate intermediates | -0.6% | Global, concentrated supply in China and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude Prices Curbing Chemical Budgets

Brent prices are projected to peak in Q2 2026 before declining in the following year. This significant drop has historically led to a reduction in discretionary chemical spending. In response, North American independents are already postponing non-critical squeezes, putting pressure on premium suppliers in the oilfield scale inhibitor market.

Tightening Discharge Regulations on Phosphorus and Heavy Metals

In the Gulf of Mexico, NPDES permits cap phosphorus levels, prompting a transition away from traditional aminomethylene phosphonates. Concurrently, rising costs due to compliance with REACH and China MEE regulations have positioned biodegradable polymers as the fastest-growing segment in the oilfield scale inhibitor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Phosphonates Anchor Thermal Stability, Green Inhibitors Advance

In 2025, phosphonates, with a robust thermal endurance and a calcium tolerance exceeding 1,000 mg/L, captured a dominant 45.82% share of the oilfield scale inhibitor market, growing at an annual rate of 6.83% CAGR from 2026 to 2031. By 2026, ongoing seawater-injection projects in the Middle-East, increasingly favoring aminomethylene blends at sub-ppm treatment rates, will support this growth. While carboxylates and acrylics are gaining traction - driven by EPA and REACH pressures to curtail phosphorus discharge - these alternatives often require double-digit ppm dosages. This necessity has limited their adoption in deepwater Brazil, where chemical logistics heavily impact total costs. In produced-water reinjection networks, where managing suspended solids alongside scaling ions is vital, polymeric and phosphorus-tagged hybrids are becoming more popular. Notably, PETRONAS utilizes multifunctional dispersants throughout its extensive pipeline network. Although biodegradable formulations occupy a niche segment, they are witnessing the fastest growth rate in percentage terms. Operators in the North Sea are investing in products classified under OSPAR's “Yellow C” designation, highlighting the market's environmental focus.

For wells facing challenges like hydrogen sulfide or iron co-production, organophosphates and synergistic blends provide solutions where traditional single-chemistry methods falter. Suppliers are trialing tracer-tagged molecules to enhance efficiency. Detectable via fiber optics, these molecules allow operators to accurately map downhole distribution and reduce overtreatment, potentially boosting the market share for these specialized solutions. The landscape is intricate: while global giants register REACH dossiers, regional formulators champion classic phosphonates, benefiting from lighter oversight. As environmental regulations tighten and operational temperatures rise, the demand for diverse chemistries ensures a balanced market, accommodating both established and emerging inhibitor families during the forecast period of 2026–2031.

By Application: Downhole Squeeze Dominates, Water Injection Accelerates

In 2025, downhole squeeze programs captured a commanding 35.01% share of the oilfield scale inhibitor market, underscoring their dominance. With a residence life spanning 12–24 months, these programs notably curtail the necessity for offshore interventions. As Argentina's Vaca Muerta ramped up its multi-well pad operations, the market for squeeze treatments surged, propelled by a heightened demand for robust proppant-coated inhibitors. Continuous tubing-string injection, securing the second spot, plays a crucial role in high-water-cut Permian wells, particularly where recycled produced water's salinity outstrips that of seawater. While surface-facility dosing claims a mid-teens market share, Brazil's pre-salt compact seabed separators are reshaping the market landscape. These separators not only concentrate ions and boost treatment rates per barrel but also catalyze innovations in ultra-concentrated blends.

Water-injection systems, leading the charge with a 6.92% CAGR during the forecast period of 2026–2031, are set to see substantial investments in Kuwait. These projects focus on the injection of treated seawater and produced water. The market share of oilfield scale inhibitors associated with these injection networks is on the rise. This uptick is largely driven by Middle-Eastern megaprojects clinching multi-year supply contracts, often with residual-based payment terms. With the advent of all-electric subsea layouts rendering injection umbilicals obsolete, the emphasis has shifted to pipeline and flowline control. This evolution is propelling the use of topside overdosing or solid inserts, crucial for protecting tiebacks that extend up to 18 kilometers in regions like the Gulf of Mexico and West Africa. Meanwhile, produced-water disposal wells, now facing scrutiny over induced seismicity concerns, are pivoting to low-phosphorus polymers. These polymers not only prevent formation plugging but also ensure a sustained, albeit niche, demand within the oilfield scale inhibitor market.

Geography Analysis

In 2025, North America commanded a 36.11% share of the oilfield scale inhibitor market, driven by activities converging in shale regions, the offshore Gulf, and Vaca Muerta. Continuous chemical dosing was essential for the produced-water stream in the Permian Basin. Operators in the Appalachian shale, facing price pressures and extended squeeze intervals, are resulting in mixed dynamics across the region. While North America's oilfield scale inhibitor market was on a steady growth trajectory during the forecast period 2026–2031, fluctuations in crude prices posed challenges to short-term budgets. In Canada, oil sands operations, requiring inhibitors compatible with hot bitumen, experienced consistent but slower unit growth.

Asia-Pacific led as the fastest-growing region, registering a 6.79% CAGR during the forecast period 2026–2031. China's offshore expansions, Indonesia's polymer floods, and Malaysia's burgeoning pipeline network spurred heightened chemical usage. Despite annual declines in ASEAN fields prompting workovers and increased brine pH and scaling risks, the oilfield scale inhibitor market's outlook remained optimistic. CNOOC's production boost in the base year 2025, alongside seawater injections in Bohai Bay, amplified demand. Furthermore, the collaboration between ONGC and Reliance in India's KG basin unlocked volumes necessitating high-salinity-tolerant chemicals. PETRONAS's two-decade extension of the PM3 project underscored the enduring chemical demand in Southeast Asia.

Europe experienced modest growth yet sustained stable consumption. In the base year 2025, Norway's seven newly tapped fields favored high-performance inhibitors, particularly those adept against electrified subsea systems. The United Kingdom's decommissioning activities spurred sporadic demand for well-preservation chemicals, offsetting the nation's gradual production declines. Russia's market, while sizable, remained opaque due to sanctions and leaned predominantly on domestic phosphonate production. The Middle-East, though not leading in percentage growth, was poised for the most substantial absolute volume increase. Industry giants such as Saudi Aramco, ADNOC, and Kuwait Oil Company made significant investments in injection and enhanced oil recovery (EOR) infrastructure. In South America, Brazil emerged as a focal point, particularly in regions outside Argentina. Petrobras, capitalizing on its production in the base year 2025, deployed acid-stable inhibitors specifically designed for CO₂-rich pre-salt fluids.

Competitive Landscape

The oilfield scale inhibitor market is moderately consolidated. Clariant's ClariHub digital portal has introduced life-cycle carbon disclosures, aligning with national oil companies that are embedding ESG clauses into their tenders. In Houston, Nouryon's newly launched innovation center is accelerating the co-development of biodegradable blends. At the same time, up-and-coming disruptors are advocating for tracer-enabled "smart inhibitors." These inhibitors, detectable via fiber optics, hold the potential for substantial chemical savings upon widespread adoption.

Oilfield Scale Inhibitor Industry Leaders

Baker Hughes Company

SLB (Schlumberger)

ChampionX

Halliburton

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SLB successfully completed its acquisition of ChampionX Corporation, establishing a unified oilfield services platform. This USD 7.8 billion transaction integrates chemical expertise with advanced digital monitoring capabilities. The consolidation of scale inhibitor supply with comprehensive production optimization services enables operators to implement predictive chemical management systems, reducing intervention costs while ensuring production efficiency.

- February 2024: BASF announced significant investment expansion in its Basoflux paraffin inhibitor production capacity, targeting growing demand from unconventional resource operators. The investment includes the development of solid inhibitor technologies that provide sustained chemical release without requiring continuous injection systems.

Global Oilfield Scale Inhibitor Market Report Scope

An oilfield scale inhibitor is defined as a specialized chemical agent used to prevent, delay, or disperse the formation and accumulation of insoluble inorganic salt crystals, such as calcium carbonate and barium sulfate, on downhole equipment, casing, tubing, and surface facilities. These inhibitors function at low concentrations (in parts per million) by modifying crystal morphology, preventing crystal nucleation, or dispersing suspended particles to avoid surface adherence, thereby ensuring flow assurance in oilfield operations.

The scale inhibitors market is segmented by type, application, and geography. By type, the market is segmented into phosphonates, carboxylates/acrylics, polymeric/phosphorus-tagged polymers, biodegradable and green inhibitors, and organophosphates and synergistic blends. By application, the market is segmented into downhole scale prevention (squeeze), tubing and casing protection, surface facility treatment, pipeline and flowline scale control, water-injection systems, and produced-water reinjection and disposal. The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Phosphonates |

| Carboxylates/Acrylics |

| Polymeric/Phosphorus-tagged Polymers |

| Biodegradable and Green Inhibitors |

| Organophosphates and Synergistic Blends |

| Downhole Scale Prevention (Squeeze) |

| Tubing and Casing Protection |

| Surface Facility Treatment |

| Pipeline and Flowline Scale Control |

| Water-Injection Systems |

| Produced-Water Reinjection and Disposal |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Phosphonates | |

| Carboxylates/Acrylics | ||

| Polymeric/Phosphorus-tagged Polymers | ||

| Biodegradable and Green Inhibitors | ||

| Organophosphates and Synergistic Blends | ||

| By Application | Downhole Scale Prevention (Squeeze) | |

| Tubing and Casing Protection | ||

| Surface Facility Treatment | ||

| Pipeline and Flowline Scale Control | ||

| Water-Injection Systems | ||

| Produced-Water Reinjection and Disposal | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for scale inhibitors become by 2031?

The oilfield scale inhibitor market size is projected to reach USD 3.46 billion by 2031, up from USD 2.52 billion in 2026, registering a 6.02% CAGR from 2026 to 2031.

What chemistries dominate current oilfield use?

Phosphonates hold 45.82% market share because they tolerate high temperature and salinity, especially in Middle Eastern water-injection projects.

Which application is growing fastest?

Water-injection systems lead growth at a 6.92% CAGR from 2026 to 2031 as Kuwait, Saudi Arabia, and ADNOC expand large-scale reinjection networks.

How are digital technologies changing chemical consumption?

Platforms that measure residual inhibitor online and automatically adjust pumps are cutting wastage and extending squeeze intervals.

How could subsea electrification affect demand?

All-electric wells remove chemical umbilicals, potentially reducing continuous dosing volumes but raising the value of long-life solid inhibitors placed downhole.

Page last updated on: