Crude Oil Flow Improvers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crude Oil Flow Improvers Market Analysis by Mordor Intelligence

The crude oil flow improvers market size is expected to grow from USD 1.93 billion in 2025 to USD 2.02 billion in 2026 and is forecast to reach USD 2.54 billion by 2031 at 4.72% CAGR over 2026-2031. The current crude oil flow improvers market size reflects steady demand from shale pipeline expansions, deepwater projects, and the rising share of heavy crude production. Polymer-based drag reducing agents, multifunctional paraffin inhibitors, and low-dosage hydrate inhibitors anchor product development as operators seek cost-effective means to maintain throughput in aging or ultra-deep transport systems. Competitive intensity remains moderate because service majors and specialty chemical suppliers balance global reach with formulation expertise, while regulatory pressure on PFAS accelerates a pivot to bio-based and fluorine-free chemistries.

Key Report Takeaways

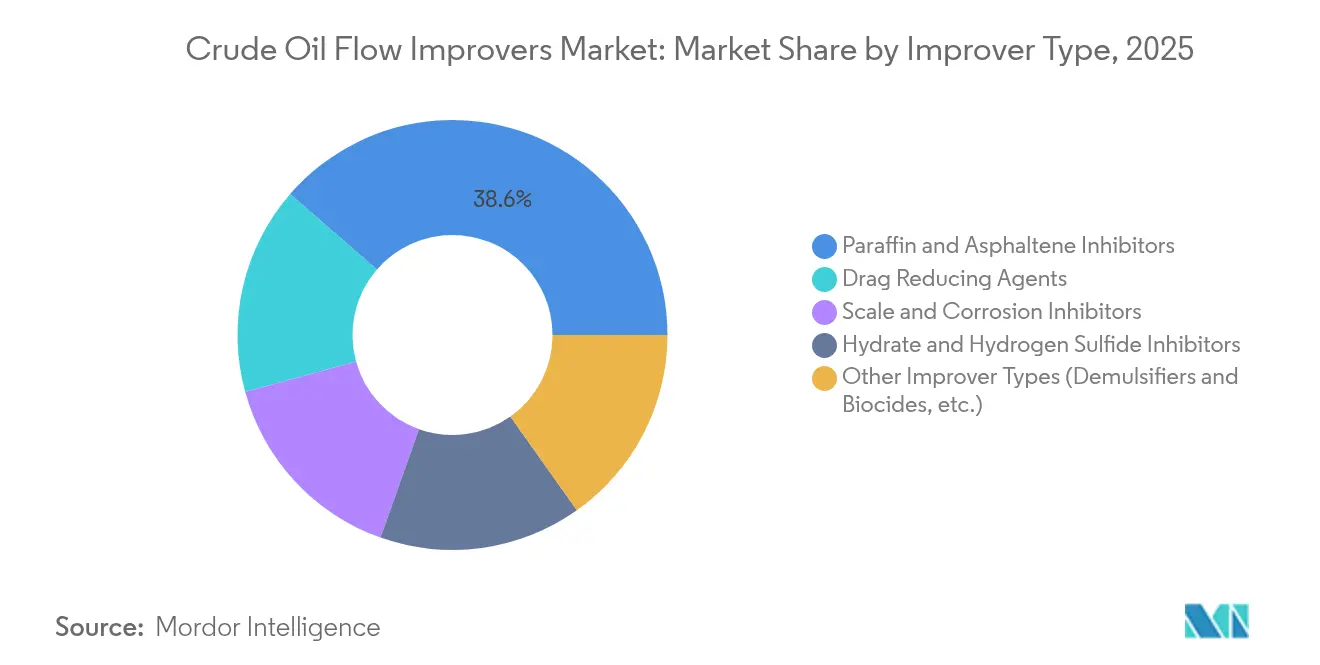

- By improver type, paraffin and asphaltene inhibitors held 38.62% of the crude oil flow improvers market share in 2025; drag reducing agents recorded the fastest 7.41% CAGR through 2031.

- By oil type, heavy and extra-heavy grades accounted for 47.02% share of the crude oil flow improvers market size in 2025 and are projected to expand at a 6.08% CAGR.

- By deployment location, onshore systems led with 54.71% revenue share in 2025; ultra-deep offshore sites advance at a 7.35% CAGR through 2031.

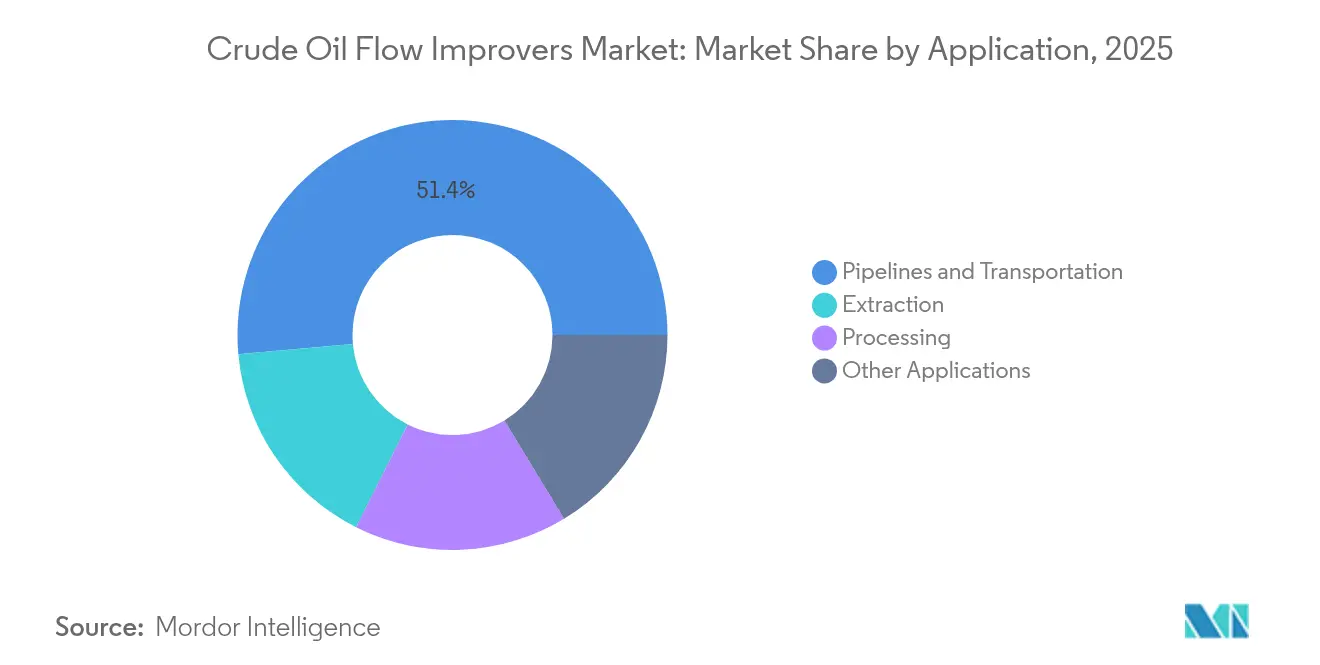

- By application, pipeline and transportation commanded a 51.42% share of the crude oil flow improvers market size in 2025; offshore pipelines are forecast to grow at 6.21% CAGR to 2031.

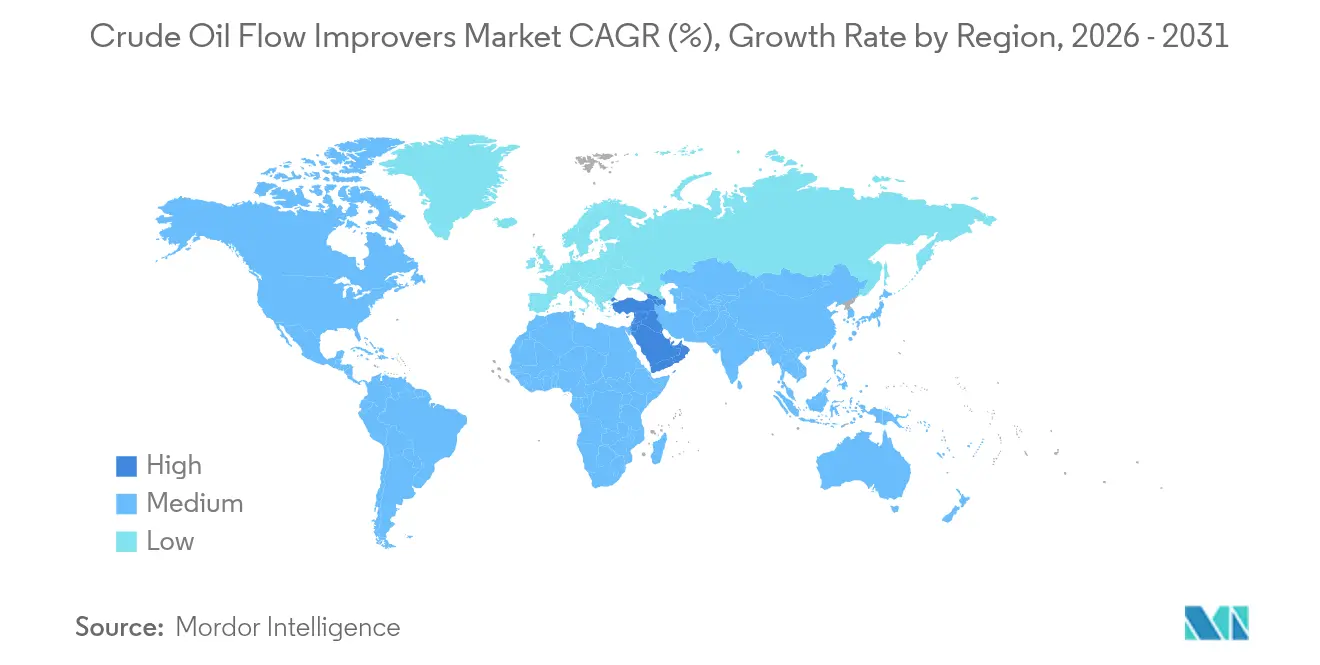

- By geography, North America held 33.28% of the crude oil flow improvers market share in 2025, while the Middle East and Africa registered the quickest 5.84% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Crude Oil Flow Improvers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased shale and tight-oil pipeline mileage | +1.2% | North America core, spill-over to Argentina | Medium term (2-4 years) |

| Surge in deep-water FPSO projects requiring hydrate inhibitors | +0.8% | Global offshore, West Africa and Brazil | Long term (≥ 4 years) |

| Growing demand for paraffin and asphaltene inhibitors | +0.9% | Global heavy crude regions | Short term (≤ 2 years) |

| Growing adoption of polymer-based DRAs in aging trunk lines | +1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing Demand for Petroleum Based Products | +0.6% | Global, with concentration in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Shale and Tight-Oil Pipeline Mileage

North American shale output lifts viscosity and wax load in gathering networks, compelling operators to dose drag-reducing agents that keep flow above economic thresholds[1]OnePetro, “Advances in Drag Reducing Agents for Shale Pipelines,” onepetro.org. Ultra-high-molecular-weight polyolefins enhance low-temperature performance, supporting lines in Canada and the Dakotas where sub-zero seasons degrade legacy chemistries. Digital injection skids now modulate treatment in real time, aligning dosage with crude blend variability to trim chemical cost without throttling capacity. These efficiencies are scaling as shale wellhead pipelines grow in mileage and interconnect existing trunk lines, reinforcing momentum in the crude oil flow improvers market.

Surge in Deep-Water FPSO Projects Requiring Hydrate Inhibitors

Ultra-deep developments past 1,500 m water depth intensify hydrate formation risk. Low-dosage kinetic and anti-agglomerant inhibitors outperform bulky methanol campaigns, easing topside storage and cutting carbon footprints. Sour-gas-compatible packages show stability at hydrogen sulfide levels above 70,000 ppm, unlocking pre-salt wells in Brazil and new finds off Angola. Operators deploy umbilical chemical lines that synchronize with subsea boosting units, driving sustained uptake of specialized formulations across the crude oil flow improvers market.

Growing Demand for Paraffin and Asphaltene Inhibitors

Higher wax appearance temperatures plague heavy crudes from Canadian oil sands, Venezuelan Orinoco blends, and deepwater Indian plays. Multifunctional polymer additives disperse wax crystals and curb asphaltene precipitation more effectively than solvent blends. Pipeline capacity drops of up to 50% are avoided when treatment begins at the wellhead and continues through export lines. Field pilots of bio-based paraffin inhibitors demonstrate parity with petro-derived analogues, answering environmental scrutiny while nurturing growth in the crude oil flow improvers market.

Growing Adoption of Polymer-Based DRAs in Aging Trunk Lines

Trunk lines averaging 40 years in service confront flow friction that erodes throughput. Polymer DRAs restore 10-40% capacity with minimal CAPEX compared to looping or pump upgrades. Shear-stable poly-alpha-olefin variants persist across 1,000 km lengths without molecular degradation, protecting marginal barrels that sustain refinery supply. Automated dosing tied to supervisory control and data acquisition platforms bolsters predictive maintenance strategies, aligning with operator priorities to keep legacy assets productive inside the crude oil flow improvers market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter PFAS bans limiting fluorinated flow improver chemistries | -0.6% | North America and EU, expanding globally | Short term (≤ 2 years) |

| Volatility in upstream CAPEX cycles post-energy transition pledges | -0.5% | Global, with emphasis on Western markets | Medium term (2-4 years) |

| Supply bottlenecks for high-molecular-weight poly-alpha-olefins | -0.4% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter PFAS Bans Limiting Fluorinated Flow Improver Chemistries

Widening PFAS regulation compels rapid reformulation. Fluorinated surfactants that long served extreme temperature applications face phase-out, prompting manufacturers to invest in silicone, hydrocarbon, or bio-based alternatives[2]United States Environmental Protection Agency, “PFAS Strategic Roadmap,” epa.gov. DIC Corporation’s PFAS-free antifoam technology reached commercial readiness in 2024, but interim supply gaps elevate costs and prolong qualification cycles. Equipment components made of fluoro-elastomers also require substitution, extending disruption beyond pure chemicals and tempering near-term growth in the crude oil flow improvers market.

Volatility in Upstream CAPEX Cycles Post-Energy Transition Pledges

Oil majors’ net-zero roadmaps flatten exploration budgets, squeezing multiyear chemical contracts that underpin research pipelines. Offshore megaprojects progress selectively, postponing some hydrate inhibitor demand. Operators pivot toward short-cycle tiebacks and brownfield debottlenecking, shrinking flow improver order volumes during price troughs. Suppliers counter by bundling products and integrating digital support, yet cash-flow irregularity still weighs on the crude oil flow improvers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Improver Type: Paraffin Solutions Drive Market Leadership

Paraffin and asphaltene inhibitors generated the largest revenue, delivering 38.62% market share in 2025 as operators battled wax deposition in cooler pipelines. The crude oil flow improvers market size for these additives is forecast to expand steadily because heavy-crude output rises and deepwater fluids cool rapidly during seabed transit. Drag reducing agents, though smaller by revenue, advance fastest at 7.41% CAGR, mirroring the need to lift throughput in aging lines without capital expansion. Multifunctional packages that merge wax control, asphaltene dispersion, and anti-foul properties reduce chemical SKUs onsite, pushing integrated solutions to the forefront of the crude oil flow improvers market.

By Oil Type: Heavy Crude Challenges Drive Innovation

Heavy and extra-heavy feeds secured a 47.02% share in 2025 and outpace lighter grades with a 6.08% CAGR because the global production mix tilts toward viscous resources as conventional reservoirs mature. Shear-stable polymers cut pressure drop and stave off paraffin crystallization, supporting cross-border pipelines such as Trans Mountain and Andean links. Laboratory trials demonstrate over 60% viscosity reduction when mechanical cavitation technologies partner with tailored additive packages. Such hybrid methods bolster confidence that existing rights-of-way can carry denser barrels, sustaining investment in the crude oil flow improvers market.

Medium crudes still need flow support in frigid climates, keeping demand broad-based. Light blends also benefit from hydrate suppression in ultra-deep environments, confirming that chemical demand grows across the crude grade spectrum rather than relying solely on the heaviest cuts.

By Deployment Location: Onshore Operations Lead Market

Onshore systems represented 54.71% of 2025 revenue owing to extensive North American and Eurasian pipeline grids. Yet the most robust 7.35% CAGR stems from ultra-deep offshore projects where high hydrostatic pressure and low seabed temperature amplify flow risks. Umbilical chemical delivery marries convenience with safety, sparking new orders for hydrate inhibitors and drag reducers tailored for 10,000-psi service. As regional gas projects progress, sour service additives join standard packages, layering further value into the crude oil flow improvers market.

By Application: Pipeline Transport Dominates Flow Assurance

Transport pipelines absorbed 51.42% of 2025 revenue, illustrating how flow assurance drives bottom-line economics along continental networks. This application portion of the crude oil flow improvers market size will continue to outrank others because any fractional loss in pipeline rate multiplies across thousands of barrels per day. Offshore pipelines, especially insulated tiebacks beyond 30 km, post a 6.21% CAGR as deepwater fields proliferate. Extraction sites use chemicals at wellhead to dilute viscosity, but volumes remain modest compared with continuous pipeline dosing.

Real-time dosage optimization platforms now ingest fluid analytics and calibrate injection on the fly. The union of software and chemistry curbs overtreatment and demonstrates tangible cost savings, a key selling point in the crude oil flow improvers market. Integrated service contracts coupling chemical supply, monitoring hardware, and data dashboards build stickier customer relationships and sharpen supplier competitiveness.

Geography Analysis

North America controlled 33.28% of worldwide revenue in 2025, underwritten by shale pipelines and Gulf of Mexico infrastructure. Automation and high-load polymers buttress performance in below-freezing territories, sustaining replacement demand across the crude oil flow improvers market.

The Middle East and Africa surge at 5.84% CAGR through 2031, buoyed by national plans to monetize sour crudes and fast-track West African deepwater hubs. Asia-Pacific growth tracks refinery expansions and new transnational lines feeding coastal import terminals. Europe maintains replacement demand in North Sea networks and adheres to strict PFAS curbs that accelerate fluorine-free chemistry adoption.

Recent breakthroughs in sour-gas compatible inhibitors in Oman and hybrid wax-control pipelines in India exemplify the localized engineering that vendors must master to deepen geographic penetration. Government directives urging domestic refining self-sufficiency further amplify the call for robust flow assurance programs across developing regions.

Competitive Landscape

The market remains moderately fragmented. Integrated service firms such as Baker Hughes and SLB bundle flow chemistry with downhole and surface services, locking in multi-year packages that protect share. Sustainability rises to board-level priority as PFAS bans loom. Strategic collaboration intensifies. Service majors tie chemical contracts to data analytics platforms, assuring measurable performance and forging switching barriers. Meanwhile, regional players sign distribution agreements with global formulators to blend locally, cutting freight costs and fulfilling local-content rules.

Crude Oil Flow Improvers Industry Leaders

Baker Hughes

Dorf Ketal

BASF

Clariant

SLB (Schlumberger)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: BASF announced capacity expansion for its Basoflux paraffin inhibitors at Tarragona, Spain, to meet growing demand for next-generation wax control solutions.

- June 2023: Clariant Oil Services launched PHASETREAT WET demulsifier line, introducing a more efficient, sustainable treatment for complex production fluids.

Global Crude Oil Flow Improvers Market Report Scope

The Crude Oil Flow Improvers Market Report include:

| Paraffin and Asphaltene Inhibitors |

| Drag Reducing Agents |

| Scale and Corrosion Inhibitors |

| Hydrate and Hydrogen Sulfide Inhibitors |

| Other Improver Types (Demulsifiers and Biocides, etc.) |

| Light and Medium (Less than 25 wt% wax) |

| Heavy and Extra-Heavy (Greater than 25 wt% wax) |

| Onshore |

| Offshore (Shallow, Deep, Ultra-Deep) |

| Extraction |

| Pipelines and Transportation |

| Processing |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Improver Type | Paraffin and Asphaltene Inhibitors | |

| Drag Reducing Agents | ||

| Scale and Corrosion Inhibitors | ||

| Hydrate and Hydrogen Sulfide Inhibitors | ||

| Other Improver Types (Demulsifiers and Biocides, etc.) | ||

| By Oil Type | Light and Medium (Less than 25 wt% wax) | |

| Heavy and Extra-Heavy (Greater than 25 wt% wax) | ||

| By Deployment Location | Onshore | |

| Offshore (Shallow, Deep, Ultra-Deep) | ||

| By Application | Extraction | |

| Pipelines and Transportation | ||

| Processing | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the crude oil flow improvers market?

The crude oil flow improvers market size stands at USD 2.02 billion in 2026 and is forecast to reach USD 2.54 billion by 2031 at a 4.72% CAGR.

Which improver type accounts for the largest revenue share?

Paraffin and asphaltene inhibitors lead with 38.62% share in 2025 owing to widespread wax deposition challenges in heavy and waxy crude streams.

Why are drag reducing agents growing faster than other products?

Polymer DRAs lift pipeline throughput 10-40% without capital upgrades, making them attractive for aging trunk lines and new shale gathering systems that face capacity limits.

How are PFAS regulations affecting flow improver supply?

Expanding PFAS bans force manufacturers to shift away from fluorinated surfactants, which raises reformulation costs and temporarily constrains certain high-performance chemistries.

Which region will grow the fastest through 2031?

The Middle East and Africa post the highest 5.84% CAGR as new pipelines, deepwater developments, and sour crude treatment projects accelerate flow improver demand.

Page last updated on: