Tall Oil Fatty Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

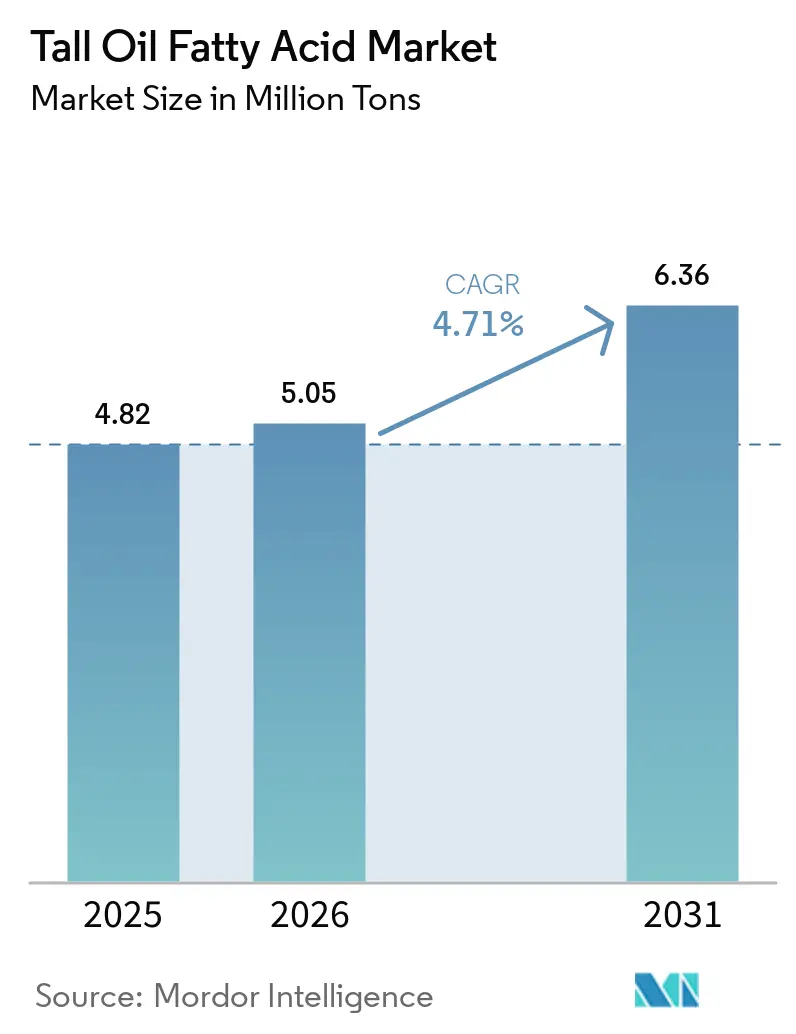

| Market Volume (2026) | 5.05 Million tons |

| Market Volume (2031) | 6.36 Million tons |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

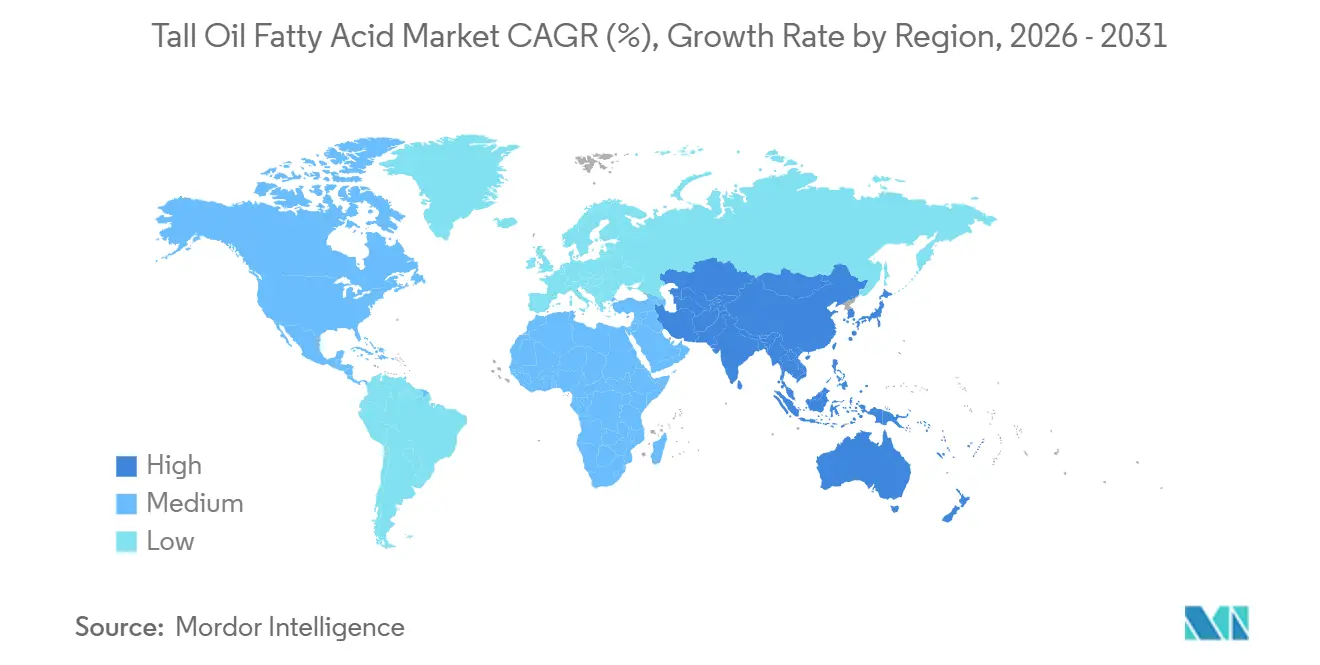

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tall Oil Fatty Acid Market Analysis by Mordor Intelligence

The Tall Oil Fatty Acid Market size is projected to be 4.82 Million tons in 2025, 5.05 Million tons in 2026, and reach 6.36 Million tons by 2031, growing at a CAGR of 4.71% from 2026 to 2031. Mounting biofuel mandates are diverting crude tall oil into renewable diesel production, pushing Tall Oil Fatty Acid market participants to out-bid energy refiners for feedstock and compressing margins. Capacity rationalization in North America, heightened sustainability certification requirements in Europe, and fresh subsidies for bio-based materials in the Asia-Pacific are reshaping competitive strategies. Large integrated pulp-chemical companies are concentrating on captive high-margin specialties, while merchant refiners expand distillation flexibility to secure fragmented CTO streams. These shifts create both supply-side volatility and demand-side momentum for Tall Oil Fatty Acid market entrants that can guarantee traceability, optimized yields, and rapid grade customization.

Key Report Takeaways

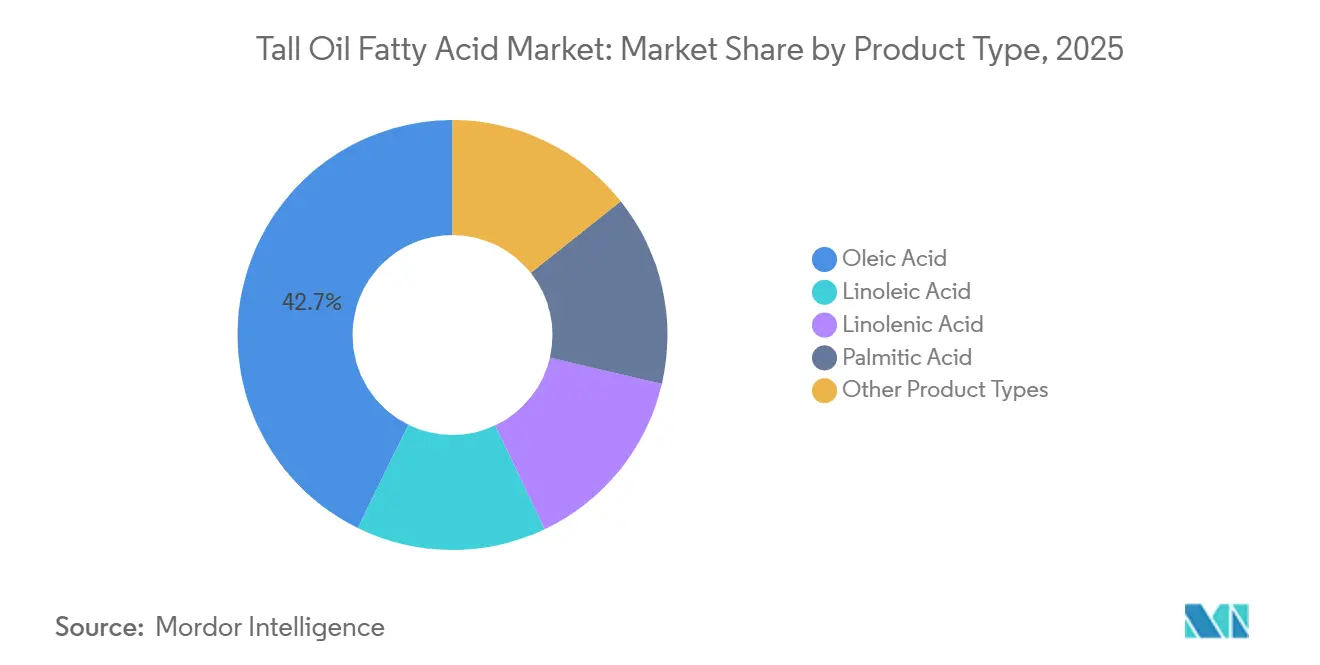

- By product type, Oleic Acid led with 42.74% of Tall Oil Fatty Acid market share in 2025, while Linolenic Acid is projected to grow at 5.92% CAGR through 2031.

- By application, Alkyd Resins captured 38.35% of volume in 2025; Dimer Acids are forecast to advance at a 6.54% CAGR up to 2031.

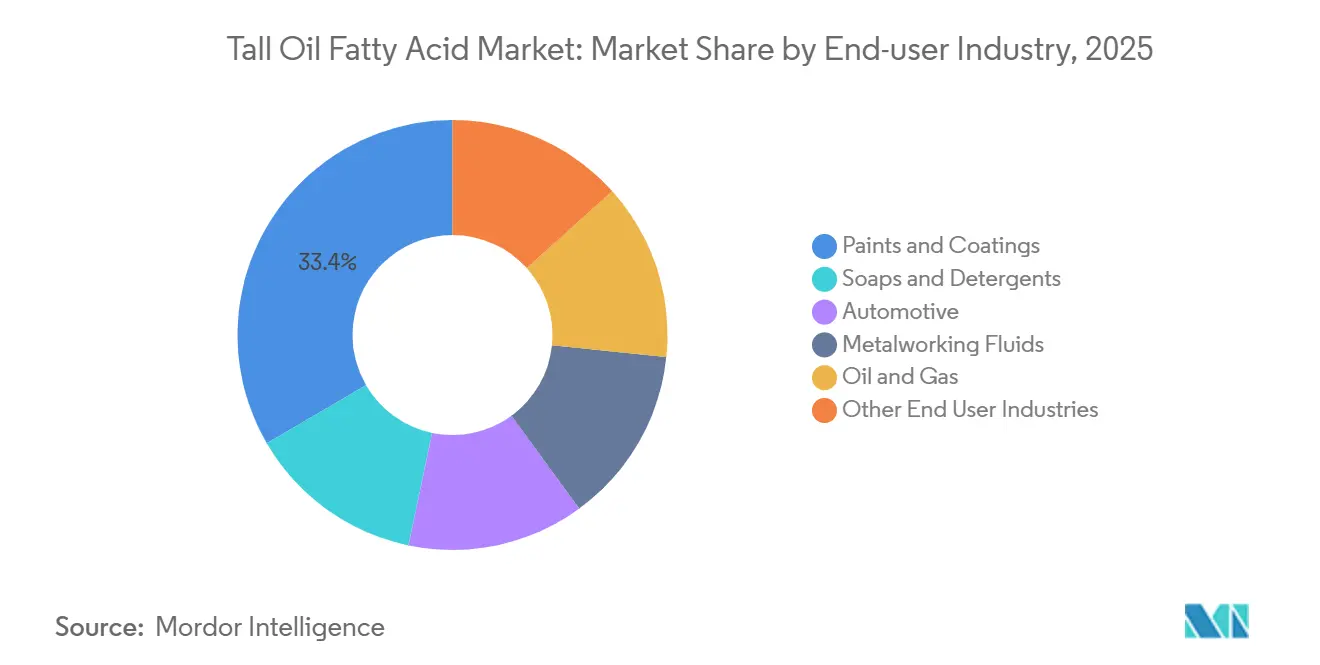

- By end-user industry, Paints and Coatings commanded 33.40% of 2025 volume, whereas Biofuels are poised for the fastest 7.38% CAGR to 2031.

- By geography, North America accounted for 35.38% of volume in 2025, yet Asia-Pacific is on track for a 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tall Oil Fatty Acid Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating demand for bio-based lubricants | +0.8% | Global, with early gains in EU and North America | Medium term (2-4 years) |

| Expanding alkyd-resin consumption in architectural coatings | +1.2% | Global, strongest in APAC (China, India, Southeast Asia) | Long term (≥ 4 years) |

| Rising use of TOFA-based dimer acids in adhesives and oil-field chemicals | +0.9% | North America shale basins, APAC automotive hubs | Medium term (2-4 years) |

| Government incentives for low-carbon feedstocks | +1.5% | EU (RED III), US (IRA, RFS), emerging in APAC | Short term (≤ 2 years) |

| Regional CTO-refinery closures driving price premiums and new capacity | +0.6% | North America, spill-over to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Demand for Bio-based Lubricants

Original equipment manufacturers in automotive and industrial equipment are switching to bio-based lubricants that satisfy stringent eco-label criteria. Tall Oil Fatty Acid market participants position TOFA esters as drop-in basestocks that offer high lubricity, rapid biodegradation, and reliable low-temperature flow[1]European Chemicals Agency, “REACH Registered Substances,” ECHA.EUROPA.EU. Elevated CTO costs temporarily prompted formulators to revert to vegetable fatty acids in 2023, but multi-year supply contracts have since stabilized pricing. New demand pockets include electric-vehicle thermal fluids and wind-turbine gearbox oils, both of which need high-purity, hydrogenated grades. Producers are upgrading hydrotreating and fractionation units to meet oxidative-stability targets. As OEM sustainability targets tighten, volume commitments for certified, traceable TOFA are growing across Europe and the United States.

Expanding Alkyd-Resin Consumption in Architectural Coatings

Architectural coatings dominate the consumption of alkyd resins, leveraging their binders for enhanced leveling, gloss retention, and a cost-effective solids content. Certification schemes like LEED and BREEAM incentivize paints with renewable carbon content, and notably, TOFA-based alkyds boast a bio-based carbon content[2]U.S. Green Building Council, “LEED v4.1 Rating System,” USGBC.ORG . The Asia-Pacific region, propelled by urban housing initiatives in India and China, witnesses growth in its coatings segment. While acrylic and polyurethane dispersions are gaining traction in premium exterior coatings, hybrid alkyd-acrylic systems are rapidly bridging the performance divide. Producers collaborating with coating companies to co-develop these hybrids stand to secure lucrative long-term offtake agreements. As a result, the Tall Oil Fatty Acid market is shifting focus towards these value-added binder applications, moving away from its traditional commodity esters.

Rising Use of TOFA-based Dimer Acids in Adhesives and Oil-field Chemicals

Dimer acids synthesized from unsaturated TOFA chains reinforce structural adhesives used in battery-electric vehicle assemblies, eliminating welds and improving fatigue resistance. Oil-field operators in North America prefer dimer-acid-based friction reducers because they meet disclosure rules and biodegradability targets. Asian adhesive makers report double-digit growth in flexible packaging, which uses polyamide resins derived from TOFA dimers. Capital requirements for high-pressure dimerization reactors constrain new entrants, concentrating supply among established refineries. Investments in yield-enhancing distillation towers by leading producers signal commitment to this high-margin niche.

Government Incentives for Low-Carbon Feedstocks

In 2024, the implementation of RED III led to a doubling of counting credits for tall oil derivatives, reducing compliance costs for European fuel blenders. The U.S. Inflation Reduction Act provides production tax credits for fuels that achieve lifecycle greenhouse gas reduction—a benchmark that tall-oil-derived HEFA pathways can attain. China's 14th Five-Year Plan highlights the importance of bio-lubricants and bio-solvents, paving the way for provincial grants aimed at pilot CTO refineries. National caps, like France's CTO blend limit, create arbitrage opportunities for suppliers, allowing them to shift feedstock to markets with more lenient regulations. Additionally, certifications such as ISCC PLUS have become essential for accessing premium market segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on softwood kraft-pulping capacity | -0.9% | Global, concentrated in North America, Nordic countries, Russia | Long term (≥ 4 years) |

| Stricter forestry regulations on logging | -0.5% | EU (EUDR), North America (FSC/SFI), emerging in APAC | Medium term (2-4 years) |

| Competition from lower-cost vegetable-oil fatty acids | -0.7% | Global, most acute in APAC and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Softwood Kraft-Pulping Capacity

Global output of softwood kraft pulp limits the availability of Tall Oil Fatty Acid (TOFA). Since 2020, a shift in digital media and packaging towards hardwood fibers has resulted in the closure of several mills across North America. Meanwhile, as renewable diesel expansions eye a larger share of CTO, competition intensifies between chemical producers and fuel customers. The TOFA market faces a persistent feedstock challenge, especially in the absence of new softwood mills emerging in South America or Southeast Asia.

Stricter Forestry Regulations on Logging

The EU Deforestation Regulation mandates geolocation proof that all wood-based inputs are deforestation-free, raising compliance costs for TOFA producers. North American mills comply with FSC and SFI standards, but patchwork state restrictions lower regional timber availability. China’s 2024 import controls on sanctioned Russian timber increased freight costs for Asian TOFA buyers. Producers with established certification infrastructure gain a cost advantage, reinforcing entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oleic Acid Dominates, Linolenic Acid Accelerates

Oleic Acid held 42.74% of volume in 2025, the largest slice of Tall Oil Fatty Acid market share, while Linolenic Acid is projected to register the fastest 5.92% CAGR through 2031. Oleic Acid’s C18:1 profile underpins metalworking fluids, surfactants, and alkyd resins. Its esters with glycerol and polyols fortify emulsifiers across personal-care and agrochemical formulations, keeping demand stable even amid feedstock fluctuations. Linolenic Acid, rich in triple unsaturation, enables rapid oxidative crosslinking, making it valuable in high-performance coatings and adhesive polyamides. Automotive lightweighting and wind-turbine blade production require such adhesives for fatigue resistance, explaining the segment’s momentum.

Growth in Linolenic Acid also reflects refiners’ move toward high-margin specialties. Investments in nitrogen-blanketed storage and antioxidant packages mitigate its oxidation sensitivity, supporting longer supply chains. Palmitic and other saturated acids fulfill soap, rubber, and fragrance niches but lack the reactivity to capture dynamic demand. SunPine’s diversification into α-Pinene and Kraton’s focus on yield optimization illustrate how Tall Oil Fatty Acid market participants are upgrading product slates to offset commodity price volatility.

By Application: Alkyd Resins Lead, Dimer Acids Surge

Alkyd Resins accounted for 38.35% of the Tall Oil Fatty Acid market size in 2025, supported by large-scale architectural coatings consumption. Demand remains buoyant because alkyds achieve gloss and flow at competitive cost, and bio-based content scores help paint brands earn green-building credits. Dimer Acids, however, are forecast to expand at a 6.54% CAGR, propelled by oil-field chemicals and automotive structural adhesives. Fracturing fluid suppliers rely on biodegradable dimer-acid polyamides to meet disclosure and toxicity thresholds in the Permian Basin, while automakers prefer dimer-acid-based hot-melts to bond multi-material battery enclosures.

Fatty Acid Esters serve biodiesel and plasticizer markets but face stiff competition from cheaper vegetable-oil esters. Smaller application pockets such as lubricity additives and corrosion inhibitors remain stable, providing a baseline offtake for second-tier refiners. Kraton’s tower installation in Florida exclusively targets higher dimer-acid yield, underscoring the strategic priority placed on this fast-growing sub-segment.

By End-user Industry: Paints and Coatings Largest, Biofuels Fastest

Biofuels, encompassing renewable diesel and sustainable aviation fuel, promise the strongest 7.38% CAGR to 2031 as RED III incentives expand.

Soap and Detergent manufacturers substitute lower-cost vegetable fatty acids when CTO prices spike, trimming their TOFA usage. Automotive producers increase TOFA demand for ester-based metalworking fluids and structural adhesives, but growth depends on global vehicle output cycles. Metalworking Fluids and Oil and Gas remain stable channels; dimer-acid-based friction reducers are standard in shale hydraulic fracturing, supporting a steady baseline of consumption.

Geography Analysis

North America contributed 35.38% of the 2025 volume, led by Southeastern United States kraft-pulp mills that supply integrated refineries. Renewable diesel mandates have escalated CTO bidding wars, lifting prices substantially between 2022 and 2023. Ingevity’s divestment of its North Charleston refinery removed integrated capacity, while Kraton’s tower upgrade aims to claw back regional share. Canada exports CTO to U.S. refiners, and Mexico’s demand sits mostly in detergents.

Asia-Pacific is forecast to post a 7.51% CAGR through 2031, bolstered by China’s bio-materials roadmap and India’s construction boom, which multiplies coatings demand. Russia-to-China timber curbs raised costs for Chinese TOFA buyers, redirecting procurement to Nordic and U.S. mills. Japan and South Korea stabilize regional demand through automotive lubricants, whereas Indonesia and Vietnam add kraft capacity, albeit mostly hardwood.

Europe benefits from Sweden and Finland’s integrated kraft complexes that feed CTO to both chemical and biofuel plants. RED III double-counting sustains refinery order books even after SunPine’s revenue dip, while UPM’s Leuna project highlights the capital intensity of backward integration. France’s CTO blend cap and Germany’s phase-out of double counting introduce cross-border arbitrage, nudging Tall Oil Fatty Acid market participants to route cargoes toward more favorable jurisdictions.

Competitive Landscape

The tall oil fatty acid market is moderately consolidated. Vertically integrated groups control significant captive CTO streams, stabilizing their input costs. Strategic realignments focus on three levers: shedding non-core plants, debottlenecking existing towers, and securing ISCC or FSC certifications. Technology differentiation revolves around advanced distillation, hydrogenation, and mass-balance traceability. Smaller European players rely on nimble logistics and specialized grades, but their lack of a captive CTO exposes them to spot-price swings. Certification costs also burden independents, tilting share toward integrated mills. Competitive intensity is further sharpened by renewable diesel refiners that can pay CTO premiums that few chemical players match. Those unable to match bids risk negative margins unless they sell premium specialties like dimer acids or fragrance terpenes. Players that unite upstream mill agreements with downstream customer co-development stand the best chance of defending Tall Oil Fatty Acid market positions in the next five years.

Tall Oil Fatty Acid Industry Leaders

Kraton Corporation

Ingevity

Forchem Oyj

Harima Chemicals Group, Inc.

Eastman Chemical Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kraton Corporation announced a general price increase of 10% or more for all Tall Oil Fatty Acids (TOFA) products in the EMEA region, effective January 1, 2026. This adjustment impacted applications such as adhesives, coatings, and sealants.

- May 2025: Kraton Corporation announced a strategic realignment, exiting its Dover, Ohio manufacturing site and discontinuing Dimer and Polyamide lines to concentrate on tall oil fatty acid supply.

Global Tall Oil Fatty Acid Market Report Scope

Tall Oil Fatty Acid (TOFA) is also called tallol or liquid rosin, which is obtained from pine and coniferous trees. It is a viscous yellow-black liquid chemical compound with an odorous smell. Tall oil fatty acid is a by-product of the wood pulp industry, belonging to the product family of Oleic Acid. The tall name is derived from a Swedish word used for pine.

The tall oil fatty acid market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into oleic acid, linoleic acid, linolenic acid, palmitic acid, and other product types (e.g., stearic acid). By application, the market is segmented into alkyd resins, dimer acids, fatty acid esters, and other applications (e.g., lubricant additives). By end-user industry, the market is segmented into soaps and detergents, paints and coatings, automotive, metalworking fluids, oil and gas, and other end-user industries (e.g., adhesives and sealants). The report also covers the market size and forecasts for the tall oil fatty acid market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of Revenue (USD).

| Oleic Acid |

| Linoleic Acid |

| Linolenic Acid |

| Palmitic Acid |

| Other Product Types (Stearic Acid, etc.) |

| Alkyd Resins |

| Dimer Acids |

| Fatty Acid Esters |

| Other Applications (Lubricant Additives, etc.) |

| Soaps and Detergents |

| Paints and Coatings |

| Automotive |

| Metalworking Fluids |

| Oil and Gas |

| Other End User Industries (Adhesives and Sealants, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Oleic Acid | |

| Linoleic Acid | ||

| Linolenic Acid | ||

| Palmitic Acid | ||

| Other Product Types (Stearic Acid, etc.) | ||

| By Application | Alkyd Resins | |

| Dimer Acids | ||

| Fatty Acid Esters | ||

| Other Applications (Lubricant Additives, etc.) | ||

| By End-user Industry | Soaps and Detergents | |

| Paints and Coatings | ||

| Automotive | ||

| Metalworking Fluids | ||

| Oil and Gas | ||

| Other End User Industries (Adhesives and Sealants, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for the Tall Oil Fatty Acid market in 2031?

It is forecast to reach 6.36 million tons by 2031, expanding at a 4.71% CAGR from 5.05 million tons in 2026.

Which product type currently dominates Tall Oil Fatty Acid demand?

Oleic Acid leads with 42.74% of the 2025 global volume.

Why are Tall Oil Fatty Acids gaining traction in bio-based lubricants?

TOFA esters deliver superior lubricity and rapid biodegradation, helping OEMs meet eco-label and sustainability targets.

How will biofuel mandates influence Tall Oil Fatty Acid supply dynamics?

Renewable diesel plants are out-bidding chemical users for CTO, tightening feedstock availability and elevating price volatility.

Which region is expected to record the fastest growth through 2031?

Asia-Pacific is set for a 7.51% CAGR, driven by China’s bio-materials policy and India’s coatings boom.

Page last updated on: