Oil And Gas Water Management Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

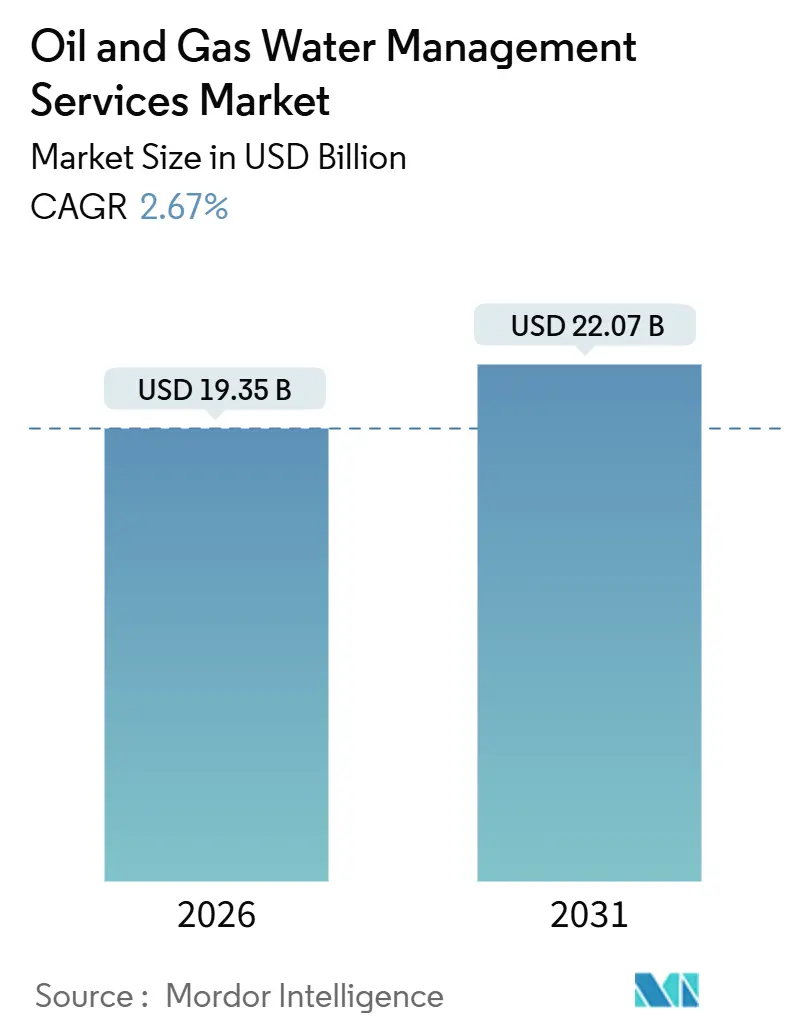

| Market Size (2026) | USD 19.35 Billion |

| Market Size (2031) | USD 22.07 Billion |

| Growth Rate (2026 - 2031) | 2.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oil And Gas Water Management Services Market Analysis by Mordor Intelligence

The Oil And Gas Water Management Services Market size is estimated at USD 19.35 billion in 2026, and is expected to reach USD 22.07 billion by 2031, at a CAGR of 2.67% during the forecast period (2026-2031).

The Oil & Gas Water Management Services market is moving from volume-based disposal toward treatment-and-reuse models as operators react to stricter discharge rules, water scarcity in shale basins, and ESG-linked financing incentives. Membrane costs fell 18% between 2024 and 2025, allowing advanced reverse-osmosis and nanofiltration units to displace legacy physical separators in the Oil & Gas Water Management Services market.[1]Baker Hughes, “Annual Report 2025,” bakerhughes.com Produced water already contributes 47.5% of total handled volumes, and flowback water is expanding at 5.8% annually, underscoring the reliance on unconventional drilling even as well designs become more efficient in the Oil & Gas Water Management Services market.[2]U.S. Energy Information Administration, “Tight Oil Production Analysis 2025,” eia.gov Deepwater projects in Brazil and West Africa, where salinity frequently exceeds 200,000 mg/L, are catalyzing offshore demand for high-specification desalination systems, further diversifying revenue streams for the Oil & Gas Water Management Services market.[3]Petrobras, “Procurement Notice October 2025,” petrobras.com.br

Key Report Takeaways

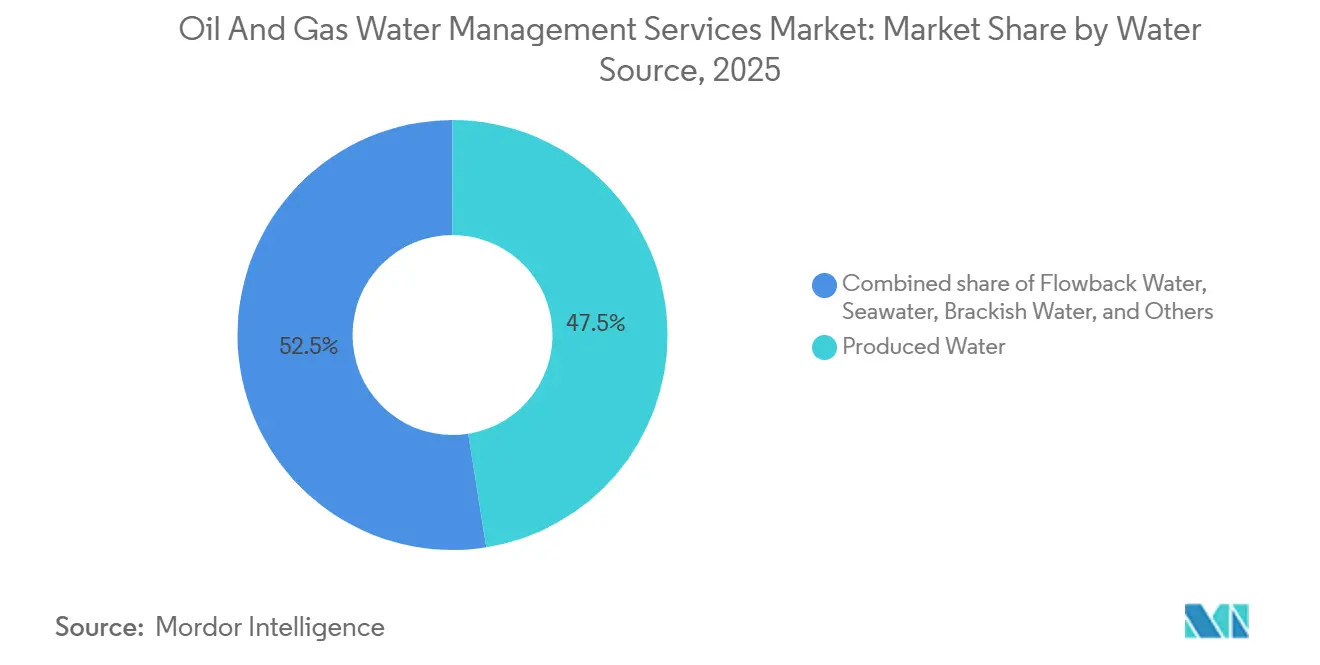

- By water source, produced water held 47.5% of the Oil & Gas Water Management Services market share in 2025, while flowback water is forecast to post the fastest 5.8% CAGR through 2031.

- By treatment technology, membrane filtration captured 35.1% revenue share in 2025; evaporation and crystallization is the fastest growing category at a 3.2% CAGR.

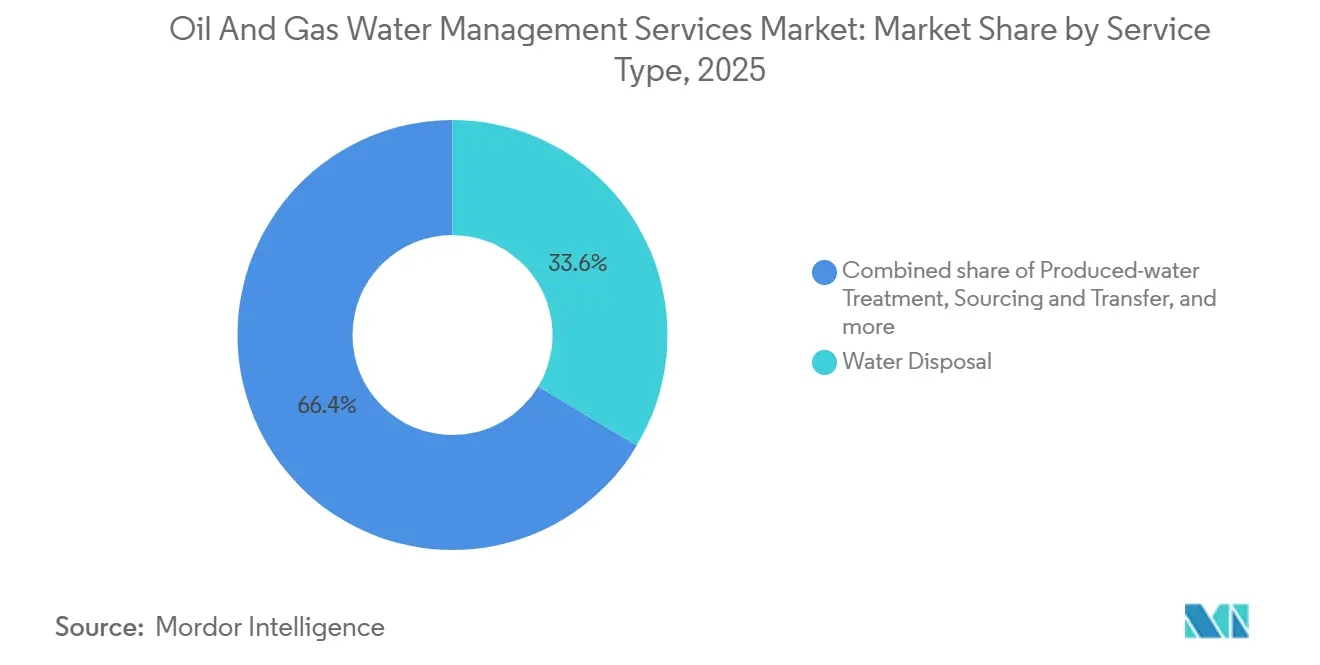

- By service type, water disposal accounted for 33.6% of the Oil & Gas Water Management Services market size in 2025, whereas produced-water treatment is projected to expand at a 3.7% CAGR to 2031.

- By location, onshore operations generated 65.9% revenue in 2025; offshore services are advancing at a 3.9% CAGR on the back of deepwater developments.

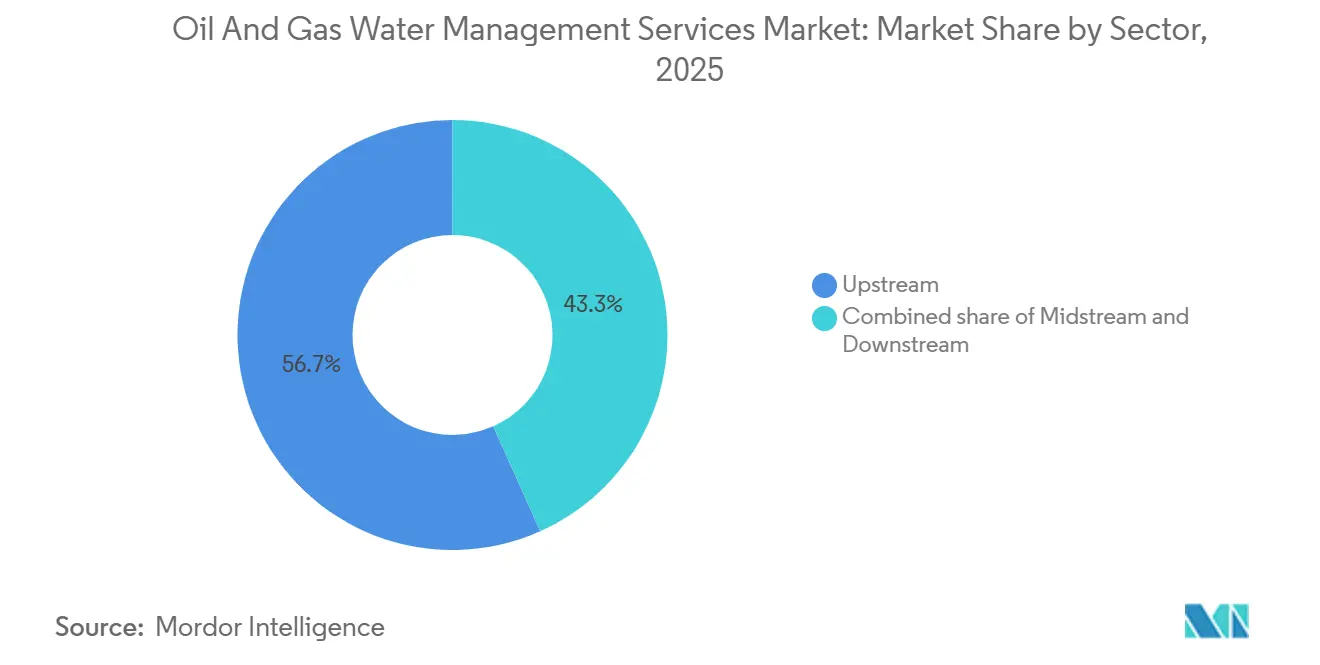

- By sector, the upstream segment commanded 56.7% of demand in 2025 and is expected to maintain a 3.0% CAGR through 2031.

- By geography, North America led with 39.4% in 2025, while Asia-Pacific is set to advance at a 4.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oil And Gas Water Management Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Produced-water surge from shale & tight formations | +0.9% | North America core, spillover to Argentina Vaca Muerta and China Sichuan | Medium term (2-4 years) |

| Stricter discharge & injection regulations | +0.7% | Global, with acute pressure in EU, California, and ASEAN coastal zones | Long term (≥ 4 years) |

| Water-stress pushing reuse & recycling mandates | +0.6% | North America Permian, Middle East onshore, India offshore | Medium term (2-4 years) |

| Digital water-operations platforms enable real-time optimization | +0.4% | Global, early adoption in North America and Norway | Short term (≤ 2 years) |

| Mobile "plug-and-play" treatment units for remote basins | +0.3% | North America unconventional plays, Argentina, Australia Cooper Basin | Short term (≤ 2 years) |

| ESG-linked financing rewarding high-efficiency water programs | +0.3% | Global, concentrated in North America and Europe with ESG-focused capital markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Produced-Water Surge From Shale & Tight Formations

Unconventional extraction generated 25 billion barrels of produced water in North America during 2025, up 14% year-on-year, as extended laterals and high-intensity completions became standard practice.[4]U.S. Geological Survey, “Water Resources Report 2025,” usgs.gov Permian volumes reached 11 billion barrels with water-to-oil ratios climbing to 6:1, lifting logistics costs to USD 0.85 per barrel and pushing operators toward centralized treatment hubs able to process 150,000 barrels per day, cutting transport expenses 40%. Argentina’s Vaca Muerta followed a similar trajectory, posting daily produced-water volumes above 80,000 barrels that now require new pipeline corridors. China’s Sichuan shale-gas plays added chemistry-specific hurdles, with H₂S concentrations exceeding 200 ppm, raising treatment costs by USD 0.30 per barrel. The interplay of rising volumes and challenging water chemistries is steering the Oil & Gas Water Management Services market toward modular, scalable systems that can grow alongside production.

Stricter Discharge & Injection Regulations

The U.S. EPA’s 2025 update to Underground Injection Control rules imposed quarterly seismic monitoring within 10 km of fault zones, affecting roughly 1,200 wells and accelerating demand for produced-water treatment across Oklahoma, Texas, and Kansas. California introduced a 10 mg/L total-nitrogen cap for offshore discharge, effectively eliminating direct ocean disposal without advanced biological polishing. The European Union capped BTEX concentrations at 0.1 mg/L, rendering legacy hydrocyclones insufficient for compliance. Norway recorded 14 non-compliance cases in 2024, prompting retrofits with ultrafiltration modules. This escalating regulatory stringency shortens compliance windows and channels spending toward service providers with proven performance records, thereby reshaping competitive dynamics inside the Oil & Gas Water Management Services market.

Water Stress Pushing Reuse & Recycling Mandates

Freshwater availability in Midland and Delaware counties fell to 60% of historical averages in 2025, driving operators to recycle up to 70% of completion fluid at costs nearly 46% lower than sourcing brackish groundwater. Saudi Aramco’s Ghawar field recycled 95% of produced water, saving USD 22 million in desalination energy. India barred freshwater withdrawal for Krishna-Godavari offshore drilling beginning January 2025, pushing operators to install shipboard reverse-osmosis units. As mandates proliferate, the Oil & Gas Water Management Services market is pivoting toward high-recovery membranes and evaporation systems capable of achieving zero-liquid-discharge in water-scarce basins.

Digital Water-Operations Platforms Enable Real-Time Optimization

Schlumberger’s DELFI platform integrated water modules at 42 sites in 2025, trimming chemical dosing by 18% and extending membrane life by nine months. Baker Hughes added edge sensors to 320 hydrocyclone units, reducing downtime by 26% through predictive maintenance. Veolia’s Hubgrade center remotely monitors 1,100 produced-water plants and has lowered electricity costs by USD 0.08 per barrel at early deployments. These productivity gains tilt competitive advantage toward firms able to bundle treatment hardware with analytics, a trend accelerating consolidation inside the Oil & Gas Water Management Services market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics & disposal costs in low-margin wells | -0.5% | North America mature fields, onshore Middle East stripper wells | Short term (≤ 2 years) |

| Oil-price volatility delaying water-infrastructure CAPEX | -0.4% | Global, acute in North America shale and Latin America | Medium term (2-4 years) |

| Fragmented basin-level water-quality specifications | -0.2% | North America state-by-state variance, EU member-state differences | Long term (≥ 4 years) |

| Uncertain permitting outlook for Class II disposal wells | -0.2% | North America (Oklahoma, Texas, Kansas seismic zones), select EU jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Logistics & Disposal Costs in Low-Margin Wells

Hauling produced water from remote Bakken wellheads cost USD 1.10 per barrel in 2025, consuming 22% of netbacks when oil traded near USD 70/bbl. Stripper wells generating high water cuts saw 1,800 temporary shut-ins in Texas and New Mexico as water-handling expenses eclipsed revenue. Pipeline transport can lower costs to USD 0.25 per barrel once daily volumes exceed 50,000 barrels, but multiyear construction timelines deter investment in declining fields. Offshore, aging Gulf of Mexico platforms barge produced water to shore at USD 2.50 per barrel due to deck-space constraints, eroding project economics when gas prices stay below USD 3/MMBtu. These structural cost pressures partly offset growth momentum in the Oil & Gas Water Management Services market.

Oil-Price Volatility Delaying Water-Infrastructure CAPEX

Brent crude’s USD 68-87/bbl range in 2025 caused the deferral of 14 large treatment projects worth USD 1.8 billion. Evaporation-crystallization systems, requiring USD 15-40 million upfront, saw order volumes drop 30% year-on-year. Operators favored short-term hauling contracts over multiyear treatment agreements, sacrificing the 25-35% life-cycle savings achievable with integrated water strategies. In Latin America, currency swings and shifting tax regimes delayed six Vaca Muerta recycling hubs and three Brazilian offshore zero-discharge projects. The stop-start investment cadence extends lead times and inflates financing costs, modestly tempering the outlook for the Oil & Gas Water Management Services market.

Segment Analysis

By Water Source: Produced Water Maintains Lead

Produced water accounted for 47.5% of handled volumes in 2025, reflecting the maturity of unconventional reservoirs and rising water-to-hydrocarbon ratios. Flowback water is expanding 5.8% annually, supported by longer laterals and higher proppant loads that generate 40% more flowback per well than 2023 designs. Seawater dominates offshore pressure-maintenance schemes, such as Johan Sverdrup’s 420,000-barrel-per-day intake that employs electrochlorination to prevent biofouling. Brackish and make-up sources are losing share as operators substitute recycled volumes, a shift accelerated by groundwater permit caps in Texas and New Mexico.

Mobile filtration is opening new revenue pools inside the Oil & Gas Water Management Services market. Baker Hughes rolled out a trailer-mounted ultrafiltration unit in 2025 that processes 15,000 barrels per day and relocates within 36 hours, ideal for short-lived flowback peaks. Produced water’s high salinity, averaging 180,000 mg/L in the Permian, requires multi-stage treatment, whereas flowback can often be polished by single-pass reverse osmosis. This divergence is segmenting service strategies: integrated providers chase long-term produced-water contracts while niche haulers target mobile flowback work. As recycled volumes rise, the Oil & Gas Water Management Services market will increasingly differentiate solutions by water chemistry, not just source.

Note: Segment shares of all individual segments available upon report purchase

By Treatment Technology: Membranes Strengthen Position

Membrane filtration captured 35.1% of spending in 2025 and is forecast to grow at 3.2% a year through 2031. Reverse-osmosis module prices fell 18% year-on-year, and energy consumption per barrel dropped 12% after the deployment of high-efficiency pressure exchangers. Physical separation remains the first-stage workhorse at 68% of onshore sites, but is now frequently paired with membrane polishing to meet discharge limits below 30 mg/L total suspended solids. Chemical pretreatment evolved as well; Veolia’s new coagulant cut dosing 25% while removing 95% of oil and grease.

Evaporation and crystallization systems are gaining ground where zero-liquid-discharge mandates prevail, although capital intensity slows uptake. Aquatech’s 20,000-barrel-per-day brine concentrator in the Marcellus became operational in 2025, transforming brine into industrial salt. Biological processes remain niche due to salinity constraints. The technology mix underscores the Oil & Gas Water Management Services market trend toward hybrid treatment trains, combining physical, chemical, and membrane steps to balance cost and compliance.

By Service Type: Treatment Advances on Disposal

Disposal still generated 33.6% of revenue in 2025 due to the prevalence of Class II injection wells, yet produced-water treatment is rising at a 3.7% CAGR as reuse economics improve. Permian operators recycled 4.8 billion barrels in 2025, saving USD 1.4 billion in freshwater costs. Hauling remains essential for remote wells; Select Energy Services ran 1,850 vacuum trucks, averaging 180 loads per month. Sourcing and transfer infrastructure is booming; WaterBridge’s 420-mile pipeline network moved 310,000 barrels per day in 2025, offering 15-year contracted cash flows.

Economics hinge on local geology: disposal costs average USD 0.40 per barrel in the Anadarko Basin, discouraging treatment, while California’s disposal ban pushes treatment rates to USD 2.80 per barrel. Fountain Quail’s integrated hauling-plus-treatment packages bridge the transition until pipelines become viable. The Oil & Gas Water Management Services industry is thus shifting from transactional disposal to asset-backed, lifecycle water solutions.

Note: Segment shares of all individual segments available upon report purchase

By Location: Onshore Scale, Offshore Complexity

Onshore operations accounted for 65.9% of 2025 revenue, propelled by North American shale well counts. Centralized Permian hubs treat up to 200,000 barrels daily, achieving per-barrel costs 60% below distributed systems. Offshore growth at 3.9% CAGR reflects deepwater projects where salinity and hydrocarbon content are extreme. Brazil’s Mero field, online in 2024, generates water with 220,000 mg/L TDS and 1,800 mg/L oil, requiring shipboard electro-coagulation and centrifugation.

Offshore constraints, weight, power, and safety favor compact solutions like Aker’s 40 m² ultrafiltration modules. Veolia’s subsea injection pilot in 2025 removed topside treatment entirely, cutting operating costs by 40%. As offshore complexity escalates, the Oil & Gas Water Management Services market bifurcates: onshore providers optimize throughput, offshore specialists engineer for reliability within tight footprints.

By Sector: Upstream Dominance Endures

Upstream activities generated 56.7% of demand in 2025 and remain on a 3.0% CAGR trajectory. Water cuts in the Bakken hit 78% as older wells mature, increasing water-handling spend. Saudi Aramco’s Ghawar field now produces six barrels of water per barrel of oil, underpinning continued infrastructure expansion. Midstream and downstream volumes are comparatively modest: Enbridge treated 14 million barrels of dehydration water in 2025, dwarfed by upstream flows.

Closed-loop cooling and zero-discharge systems are spreading through refineries, yet these upgrades are driven by municipal water scarcity rather than hydrocarbon production. Consequently, the Oil & Gas Water Management Services market will remain upstream-centric, with midstream and downstream segments offering niche but stable revenue opportunities.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America delivered 39.4% of global revenue in 2025, driven by the Permian Basin’s 35 million-barrel-per-day produced-water stream. Reuse rates are rising as ESG pressure mounts, aided by an extensive network of 180,000 Class II wells that still offer a disposal safety valve. Canada faces emulsified-bitumen challenges that add USD 0.50 per barrel in pretreatment costs. Mexico awarded four modernization contracts in 2025 to improve offshore water systems.

Asia-Pacific is the fastest-growing region at a 4.1% CAGR. Sichuan shale-gas output generated 28 million barrels of produced water in 2025, all subject to 15 mg/L total-nitrogen limits before discharge to the Yangtze watershed. India’s ONGC ordered three 80,000-barrel-per-day offshore treatment platforms to meet zero-discharge mandates. Indonesia and Malaysia commissioned floating treatment barges, while Australia piloted solar-powered evaporation ponds that cut energy costs by 35%.

The Middle East and Africa emphasize large-scale recycling projects, exemplified by Khurais’ 400,000-barrel-per-day plant, which reduces seawater intake by 22%. Nigeria’s Agbami FPSO installed a hybrid power system to keep ultrafiltration modules online despite grid unreliability. South America’s pre-salt fields require subsea separation and injection to free deck space. Europe’s North Sea retrofits compact systems to extend platform life by up to five years. These regional nuances confirm that the Oil & Gas Water Management Services market must tailor solutions to local resource, regulation, and infrastructure contexts.

Competitive Landscape

Top Companies in Oil and Gas Water Management Services Market

The Oil & Gas Water Management Services market is moderately fragmented; the top 10 players hold close to 48% of 2025 revenue. Integrated oilfield-service majors, Schlumberger, Halliburton, Baker Hughes, bundle logistics, treatment, and digital monitoring, a strategy attractive to supermajors but cost-intensive for independents. Midstream water specialists such as WaterBridge and Solaris secure long-term contracts that lock in pipeline throughput and deter greenfield entry by capital-constrained rivals.

Environmental-services leaders Veolia and SUEZ differentiate through proprietary membranes and centralized remote-operations centers, targeting jurisdictions with stringent discharge caps. White-space opportunities cluster around mobile treatment, zero-liquid-discharge, and subsea injection. Baker Hughes’ trailer-mounted units, Aquatech’s crystallizers, and Veolia’s subsea system each address these niches, respectively. Firms that master real-time analytics and predictive maintenance are winning disproportionate share, while legacy haulers relying on manual dispatch are losing ground.

Oil And Gas Water Management Services Industry Leaders

-

Halliburton Company

-

Baker Hughes Co.

-

Schlumberger Ltd.

-

Veolia Environnement SA

-

Select Energy Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Halliburton secured multiple service contracts from Petrobras to provide deepwater vessel stimulation, intelligent completions, safety valves, and related services in Brazil's offshore Búzios, Sepia, and Atapu fields. While not directly focused on water management, Halliburton's integrated stimulation and well services may involve flowback and fluid handling technologies essential for managing produced water and reservoir fluids.

- April 2025: WaterBridge completed a USD 280 million Permian pipeline expansion, adding 140 miles and boosting capacity to 310,000 barrels per day.

- April 2024: SUEZ introduced a reverse-osmosis membrane with 22% lower energy use and 98% salt rejection at <800 psi.

- January 2024: Schlumberger acquired HydroAnalytics, a cloud platform enabling real-time salinity and hydrocarbon tracking across 14 basins, integrating it into DELFI for predictive maintenance.

Global Oil And Gas Water Management Services Market Report Scope

The oil and gas water management services market encompasses technologies and services designed for sourcing, transporting, treating, recycling, storing, and disposing of water across upstream, midstream, and downstream operations. It focuses on managing water generated during drilling, hydraulic fracturing, production, and refining processes, including produced water, flowback water, and wastewater.

The oil & gas water management services market report is segmented by water source, treatment technology, service type, location, sector, and geography. By water source, the market is segmented into produced water, flowback water, seawater, brackish/make-up water, and others. By treatment technology, the market is segmented into physical separation, membrane filtration, chemical treatment, evaporation and crystallization, and biological treatment. By service type, the market is segmented into water disposal, water hauling, produced-water treatment, sourcing and transfer, and others. By location, the market is segmented into onshore and offshore. By sector, the market is segmented into upstream, midstream, and downstream. The market forecasts are provided in terms of value (USD).

| Produced Water |

| Flowback Water |

| Seawater |

| Brackish/Make-Up Water |

| Others |

| Physical Separation (Hydro-cyclones, etc.) |

| Membrane Filtration (RO, NF, UF) |

| Chemical Treatment (Coagulation, Oxidation) |

| Evaporation and Crystallization |

| Biological Treatment |

| Water Disposal |

| Water Hauling |

| Produced-water Treatment |

| Sourcing and Transfer |

| Others |

| Onshore |

| Offshore |

| Upstream |

| Midstream |

| Downstream |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Water Source | Produced Water | |

| Flowback Water | ||

| Seawater | ||

| Brackish/Make-Up Water | ||

| Others | ||

| By Treatment Technology | Physical Separation (Hydro-cyclones, etc.) | |

| Membrane Filtration (RO, NF, UF) | ||

| Chemical Treatment (Coagulation, Oxidation) | ||

| Evaporation and Crystallization | ||

| Biological Treatment | ||

| By Service Type | Water Disposal | |

| Water Hauling | ||

| Produced-water Treatment | ||

| Sourcing and Transfer | ||

| Others | ||

| By Location | Onshore | |

| Offshore | ||

| By Sector | Upstream | |

| Midstream | ||

| Downstream | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Oil and Gas Water Management Services market in 2026?

The Oil and Gas Water Management Services market size stood at USD 19.35 billion in 2026 and is projected to reach USD 22.07 billion by 2031, registering a growth of 2.67% through 2031.

Which treatment technology is gaining share the fastest?

Membrane filtration is the fastest-growing technology, expanding at a 3.2% CAGR as reverse-osmosis and nanofiltration costs decline.

Why is produced-water treatment outpacing disposal growth?

Tightening discharge rules, ESG financing incentives, and rising disposal-well seismic scrutiny make treatment and reuse more economical in several basins.

Which region offers the highest growth potential through 2031?

Asia-Pacific leads with a projected 4.1% CAGR, driven by China's Sichuan shale gas and India's offshore developments under zero-discharge mandates.

What is the competitive advantage of digital water-management platforms?

Real-time monitoring and predictive maintenance reduce chemical use by up to 18% and downtime by 26%, delivering measurable cost savings for operators.

How does oil-price volatility influence investment in water infrastructure?

Price swings defer capital-intensive projects such as crystallizers, pushing operators toward short-term hauling contracts despite higher operating costs over time.