Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

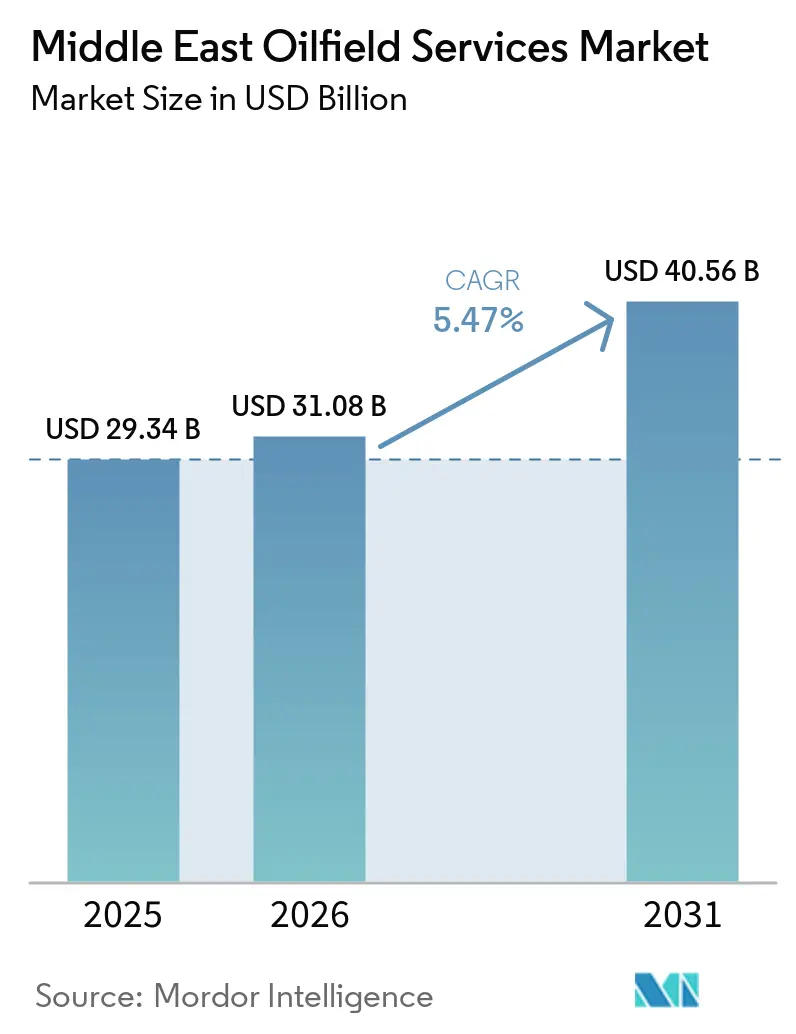

| Base Year Market Size (2025) | USD 29.34 Billion |

| Market Size (2026) | USD 31.08 Billion |

| Market Size (2031) | USD 40.56 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Oilfield Services Market Analysis by Mordor Intelligence

The Middle East Oilfield Services Market size is expected to grow from USD 29.34 billion in 2025 to USD 31.08 billion in 2026 and is forecast to reach USD 40.56 billion by 2031 at 5.47% CAGR over 2026-2031.

National oil companies are channeling capital toward mature-field optimization and unconventional gas, driving a decisive shift in service demand patterns. Drilling remains the single largest revenue stream, yet production and intervention solutions are expanding faster as operators focus on incremental barrels from existing wellbores. Offshore programs in the United Arab Emirates and Qatar are accelerating, bringing deepwater completion technologies into a region long dominated by low-cost onshore development. Digital-oilfield rollouts, from real-time geosteering to autonomous rigs, are helping offset labor shortages and compress well delivery cycles. At the same time, tighter carbon rules, water scarcity, and contract repricing pressure margins, rewarding providers able to couple technology depth with cost discipline. The interaction of these forces defines near- to medium-term opportunities across the Middle East oilfield services market.

Key Report Takeaways

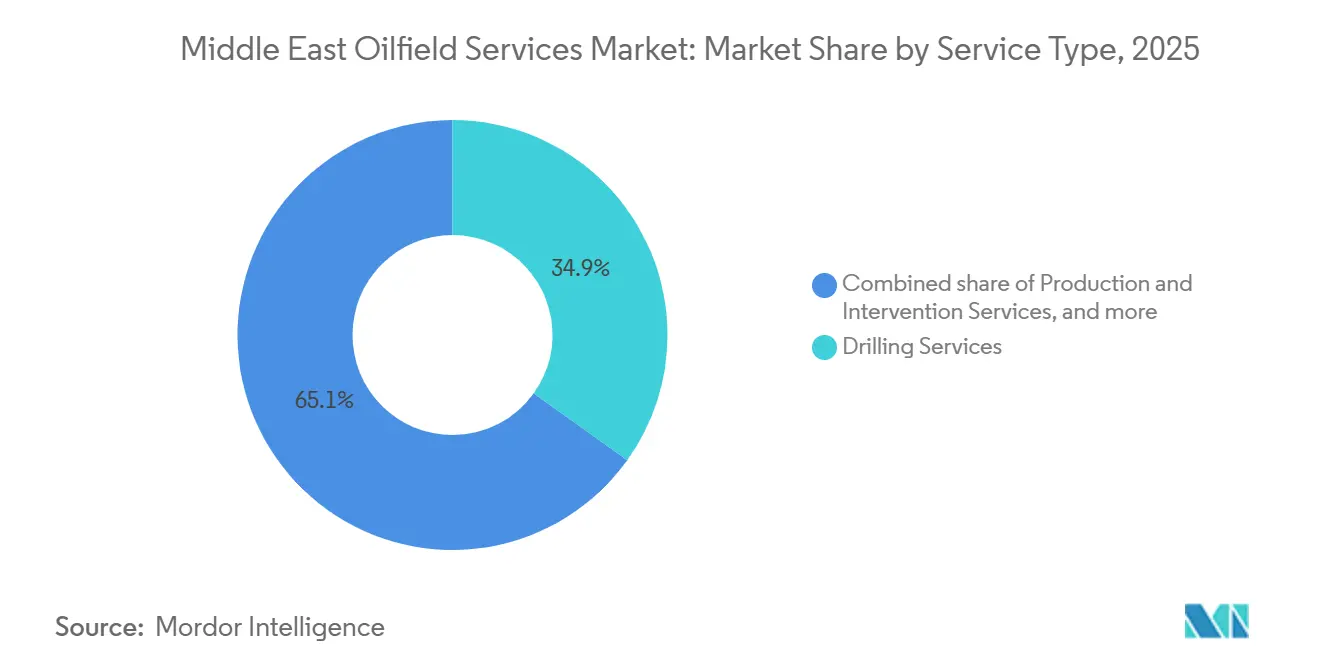

- By service type, drilling commanded 34.9% of the Middle East oilfield services market share in 2025, while production and intervention services are forecast to post the fastest 7.5% CAGR through 2031.

- By location, onshore operations accounted for 82.1% of the Middle East oilfield services market size in 2025, and offshore activity is advancing at a 9.4% CAGR to 2031.

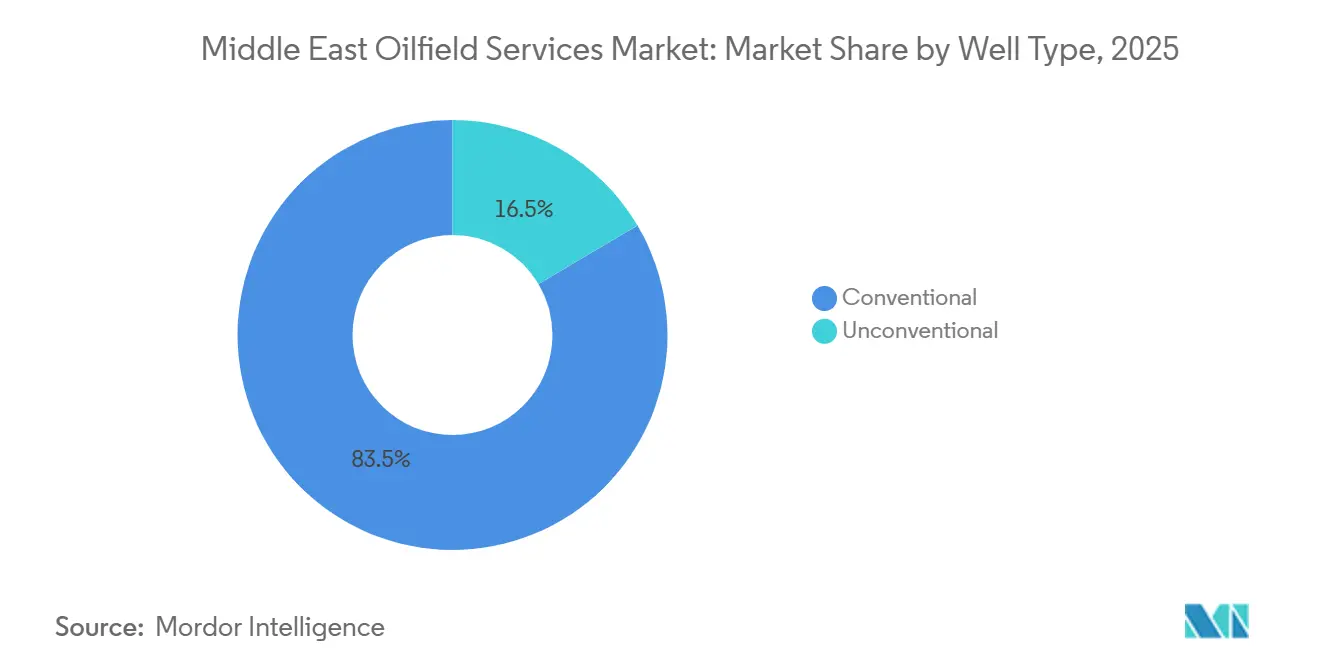

- By well type, conventional wells held an 83.5% share of the Middle East oilfield services market in 2025, and unconventional programs are projected to grow at an 8.1% CAGR through 2031.

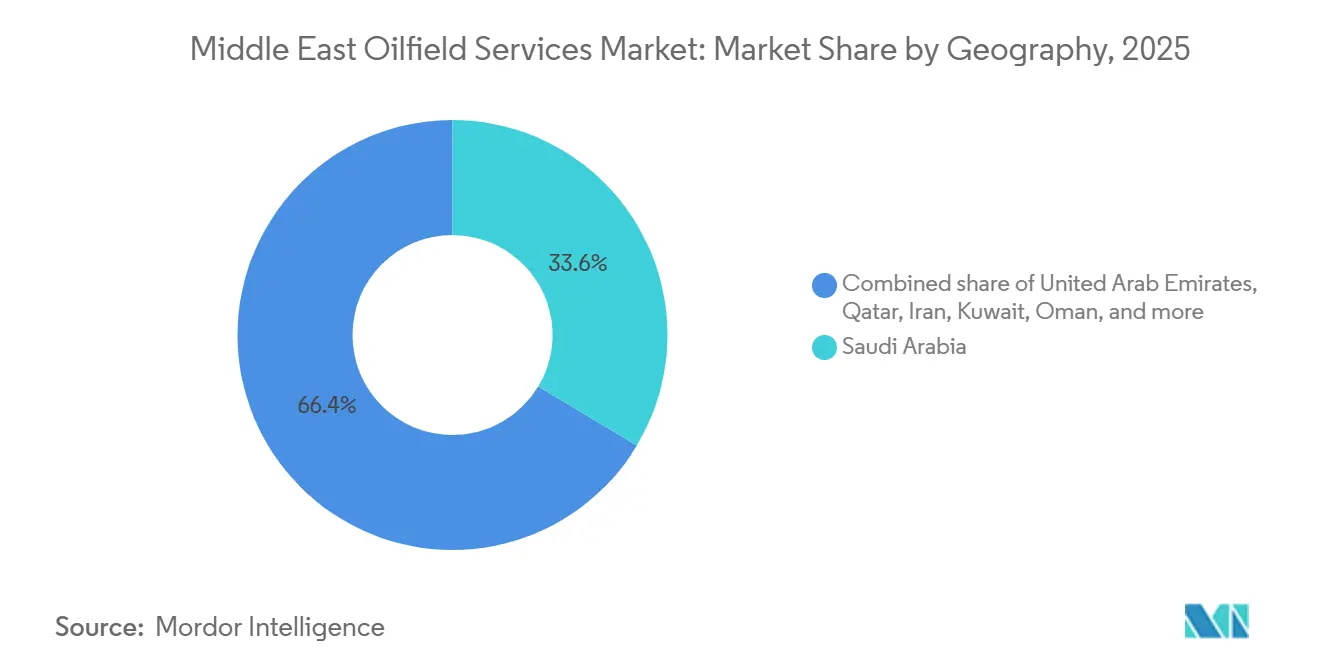

- By geography, Saudi Arabia led with 33.6% spending in 2025, while the United Arab Emirates is poised for the highest 5.9% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Oilfield Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising drilling activity across GCC fields | +1.2% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Post-COVID oil-price recovery fueling CAPEX | +0.9% | Saudi Arabia and UAE | Short term (≤ 2 years) |

| National-oil-company investment in unconventional resources | +1.5% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Local-content mandates boosting regional contracts | +0.6% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Thermal EOR projects to maximize mature-field output | +0.8% | Kuwait, Oman, Saudi Arabia | Long term (≥ 4 years) |

| Digital-oilfield adoption to offset manpower shortages | +0.5% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Drilling Activity Across GCC Fields

Active rig counts climbed to multi-year highs in 2025 as Saudi Arabia operated more than 100 rigs and the UAE exceeded 60, sustained by national oil companies determined to keep collective capacity above 12 million barrels per day.[2]Staff writers, “Gulf Rig Count Reaches Record Levels,” reuters.com Increased drilling is targeting infill locations and bypassed zones, which demand advanced rotary-steerable systems and real-time data services. Qatar’s North Field LNG build-out alone added 20 offshore rigs, sharpening demand for jack-up units and subsea completions. Kuwait is increasing well density in heavy-oil acreage to improve steam distribution, requiring corrosion-resistant tubulars and high-temperature logging. Chinese contractors, led by COSL, have entered Saudi offshore campaigns with five-year contracts, putting downward pressure on established providers’ day rates. The expansion underscores how drilling volume and well complexity together underpin the immediate growth of the Middle East oilfield services market.

Post-COVID Oil-Price Recovery Fueling CAPEX

Brent crude averaged USD 82 per barrel in 2025, restoring cash flow for Gulf majors and unfreezing projects that had been deferred during 2020.[3]Energy desk, “Higher Oil Prices Revive Gulf CAPEX,” wsj.com Saudi Aramco’s 2025 capital expenditure rose to USD 50 billion, while ADNOC committed USD 150 billion across five years, channeling much of that sum into drilling, completion, and production solutions. Higher prices have reactivated long-cycle offshore developments along with unconventional gas projects that carry larger service intensity. Yet OPEC+ supply management still introduces quarterly swings, pushing operators to negotiate performance-based pricing that shifts more risk to contractors. Integrated project-management models, where service companies assume reservoir delivery responsibility, are gaining traction, illustrated by Schlumberger’s framework in Oman’s tight-gas assets. Collectively, resilient Brent levels continue to lift the Middle East oilfield services market, even as volatility demands flexible commercial structures.

National-Oil-Company Investment in Unconventional Resources

Saudi Aramco’s Jafurah shale program moved into full development in 2026 with a plan to drill 50 horizontal wells annually, each requiring multi-stage fracturing and extensive proppant logistics. The USD 100 billion budget through 2030 is spawning fresh demand for high-horsepower frac spreads, slickwater chemistries, and downhole monitoring. ADNOC is pursuing tight-gas extraction in the Rub al Khali basin, awarding long-term completion contracts to technology majors in 2025. Oman’s Khazzan field now delivers 1.5 billion cubic feet per day, keeping a continuous queue of intervention jobs to sustain pressure. Water sourcing remains a bottleneck across inland deserts, prompting pilots that truck desalinated seawater more than 300 kilometers at material cost. Even so, unconventional momentum is set to be the single biggest structural growth lever for the Middle East oilfield services market during the next decade.

Local-Content Mandates Boosting Regional Contracts

Saudi Arabia’s IKTVA framework obliges contractors to reach 70% local value by 2030, a target mirrored by the UAE’s ICV scoring scheme. Schlumberger and Baker Hughes have opened manufacturing hubs in Dammam and Abu Dhabi, respectively, while Halliburton has teamed with Arabian Oilfield Services to cement its Saudi presence. The rules increase upfront capital and dilute equity for foreign firms, yet they create durable barriers that protect early movers. QatarEnergy, through its local-content policy, is forcing offshore contractors to base maintenance yards in Ras Laffan. Regional champions such as ADNOC Drilling and NESR leverage established footprints to outpace less integrated challengers. As a result, local-content mandates are redistributing revenue inside the Middle East oilfield services market, linking contract awards to domestic employment, technology transfer, and supply-chain localization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil prices | -0.7% | Saudi Arabia, UAE, Kuwait, Oman | Short term (≤ 2 years) |

| Tighter regional CO₂-emission regulations | -0.4% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Sanctions-driven procurement delays (Iran) | -0.3% | Iran, spillover to Iraq | Long term (≥ 4 years) |

| Water-scarcity limits on large-scale fracturing | -0.5% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil Prices

Price swings between USD 70 and USD 90 per barrel through 2025 produced uneven investment patterns and forced mid-contract repricing on several service agreements. Performance-linked structures adopted by Saudi Aramco and ADNOC transfer revenue risk to contractors, shrinking cash visibility. Smaller independents in Kuwait and Oman pause work when Brent softens, weighing on fleet utilization. Uncertainty also deters rig-new-build commitments, tightening supply and elevating spot day rates when demand rebounds. Diversified service providers now bundle maintenance annuities and digital subscriptions to smooth earnings during price troughs, helping mitigate but not eliminate volatility drag on the Middle East oilfield services market.

Water-Scarcity Limits on Large-Scale Hydraulic Fracturing

Hydraulic fracturing in arid provinces, notably Saudi Arabia’s Jafurah, consumes around 50,000 cubic meters of water per well, stressing inland aquifers and pushing operators toward desalinated seawater trucked inland. Logistics add USD 2-3 per barrel to lifting costs, challenging project economics. In the UAE, tight-gas developers recycle produced water and trial waterless fluids, though those chemistries remain premium-priced. Oman’s high recovery rates demonstrate feasibility, yet require complex treatment systems and continuous monitoring. Regulatory caps on groundwater extraction introduced in 2024 further constrain volumes available for industrial use. The combined effect slows unconventional scale-up and adds cost pressure across the Middle East oilfield services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Production Optimization Gains Momentum

Production and intervention services are projected to grow at a 7.5% CAGR to 2031, eclipsing the expansion pace of drilling despite drilling’s 34.9% Middle East oilfield services market share in 2025. Operators now favor coiled-tubing cleanouts, acid stimulations, and artificial-lift retrofits that squeeze additional barrels from mature assets. Digital well surveillance tools flag underperforming producers sooner, triggering immediate remedial activity. Completion services, especially multi-stage fracturing for tight-gas horizons, are also scaling, supported by Jafurah and Rub al Khali work programs. Drilling retains scale, yet horizontal well designs demand fewer rig days per foot, reallocating spend toward high-value downhole tools and telemetry. Layering these trends, the production-oriented segment accounts for rising contract share, illustrating how capital efficiency priorities shape the Middle East oilfield services market.

Drilling contractors respond by integrating measurement-while-drilling analytics, autonomous rotary-steerable systems, and managed-pressure kits to preserve relevance. Intervention providers further differentiate through fit-for-purpose EOR packages that combine fiber-optic diagnostics with high-temperature packers. Cementing players introduce self-healing slurries to cope with high-pressure, high-temperature wells, expanding average revenue per job. While other ancillary services, such as seismic or decommissioning, deliver steady but modest growth, the spotlight stays on production optimisation as the quickest route to uphold national output targets without massive greenfield outlays.

By Location: Offshore Activity Surges on Gas Expansion

Onshore sites still represented 82.1% of the Middle East oilfield services market size in 2025, anchored by giant carbonate fields in Saudi Arabia and Kuwait.[4]Correspondent reports, “UAE Offshore Contract Awards Accelerate,” reuters.com Yet offshore programs are forecast to log a 9.4% CAGR through 2031 as the UAE and Qatar ramp up deepwater gas developments. QatarEnergy’s North Field added 20 rigs in 2025, and ADNOC Offshore awarded USD 15 billion in drilling and completion contracts, catalyzing demand for subsea production systems, diving support vessels, and high-capacity workover units.

The offshore push accelerates technology adoption, including subsea processing modules that shrink topside scope and dual-activity rigs that drill and complete in parallel. Onshore, growth moderates amid a pivot to infill drilling and EOR, yet remains a backbone for service continuity. Providers with marine logistics capacity and integrated subsea portfolios secure the lion’s share of new awards, rebalancing revenue split toward offshore over the forecast horizon.

By Well Type: Unconventional Projects Scale Despite Constraints

Conventional wells accounted for 83.5% of activity in 2025, but unconventional programs are expected to post an 8.1% CAGR to 2031, reflecting aggressive shale and tight-gas ambitions. Jafurah’s annual 50-well schedule drives unprecedented fracturing demand in the region, requiring more than 2,000 tons of proppant per well. UAE tight-gas developers mirror the model, albeit on a smaller scale.

Extended-reach horizontals in mature carbonates blur conventional boundaries, with laterals surpassing 5,000 meters and demanding real-time geosteering. Local proppant manufacturing is underway, yet current capacity trails demand, forcing continued imports and exposing supply chains to shipping delays. Overall, unconventional acceleration introduces higher service intensity per well, lifting revenue potential even as water and cost headwinds temper rollout speed across the Middle East oilfield services market.

Geography Analysis

Saudi Arabia retained 33.6% market share in 2025 and remains the single largest spend center thanks to sustained investment in Jafurah, Marjan, and Khurais. Rig counts have grown continuously since 2024, and national content benchmarks favor contractors with Saudi manufacturing footprints. Yet the United Arab Emirates is projected to deliver the highest 5.9% CAGR between 2026 and 2031, propelled by offshore gas plays and stringent ICV scoring that rewards Emirati partnerships. ADNOC Drilling’s expanding jack-up fleet underpins this momentum.

Qatar’s North Field expansion provides a durable offshore backlog that increases subsea equipment orders and marine logistics spending. Kuwait and Oman show mid-single-digit growth, anchored by thermal EOR projects and selective unconventional pilots. Both countries face budget constraints that shape phased investment pacing. Iran remains inhibited by sanctions that limit access to high-spec equipment, while Iraq’s southern fields experience periodic step-outs tied to security conditions and contract renegotiations.

Collectively, the Gulf Cooperation Council states contribute more than 90% of current expenditure, ensuring geographic concentration of opportunities. Technology localization, workforce nationalization, and emissions compliance remain universal themes, though execution timelines and capital depth vary. This divergence offers room for specialized contractors to tailor propositions country by country, solidifying the Middle East oilfield services market as a mosaic of distinct national priorities under a shared push for production resilience.

Competitive Landscape

The market is moderately concentrated, with Schlumberger, Halliburton, and Baker Hughes still controlling significant wallet share, yet regional champions are closing the gap. ADNOC Drilling raised USD 1.1 billion in its 2024 IPO and plans to operate 140 rigs by 2027, pairing fleet scale with the highest local-content scores in the region. NESR accelerated expansion through a 40% stake in Omani contractor Abraj Energy Services, gaining high-temperature drilling capability for thermal EOR work.

International majors now bundle digital platforms such as Schlumberger’s DELFI and Baker Hughes’ Leucipa with mechanical services to secure multi-year framework agreements. Chinese entrants led by COSL and Anton Oilfield Services compete aggressively on price, winning Saudi offshore and Kuwaiti onshore slots with bids 15-20% below Western averages. Technology advantage remains decisive, yet pricing pressure intensifies, especially where local-content weighting narrows total-cost gaps.

White-space areas include decommissioning of aging offshore platforms and carbon-capture well services, both still in early regulatory stages. Weatherford’s acquisition of 30% in Arabian Oilfield Services exemplifies joint-venture paths to access closed markets while meeting localization targets. As autonomous drilling and predictive-maintenance adoption grow from pilot to mainstream, contractors unable to fuse data analytics with field execution risk erosion of relevance in the evolving Middle East oilfield services market.

Middle East Oilfield Services Industry Leaders

Halliburton Company

Weatherford International PLC

Baker Hughes Co.

Middle-East Oilfield Services

Schlumberger Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saipem has awarded EnerMech a contract for subsea pre-commissioning work on ExxonMobil's Whiptail offshore development in Guyana's Stabroek Block. The contract scope includes cleaning, hydrotesting, and monitoring of subsea infrastructure prior to production, highlighting continued investments in offshore oilfield services and deepwater project execution.

- June 2025: TotalEnergies' Tilenga project in Uganda and the East African Crude Oil Pipeline (EACOP) to Tanzania aim to develop Lake Albert's oil resources and transport crude globally. The projects include upstream field development, a 1,443 km pipeline, and social and environmental measures such as land acquisition, community consultations, and impact mitigation, adhering to international standards.

- May 2025: ADNOC Drilling has secured a USD 1.15 billion, 15-year contract for two AI-enabled jack-up rigs to support its expanding offshore operations. This initiative strengthens its offshore fleet and ensures long-term revenue. The development aligns with the broader growth of oilfield services in the Middle East, driven by technological advancements and continued investment in drilling infrastructure to meet the region's energy demands.

- November 2024: Gulf Arab states are advancing voluntary carbon markets to support emissions reduction and low-carbon transitions. Despite early-stage challenges, these markets can complement climate goals, innovation, biodiversity efforts, and regional collaboration, aligning fossil-dependent economies with Paris Agreement commitments.

Middle East Oilfield Services Market Report Scope

Oilfield services refer to a range of services that support the upstream activities of the oil and gas industry. These activities include survey, extraction, drilling, production, and abandonment. Some examples of oilfield services include casing and tubing, directional drilling, drilling, and completion fluids; floating production services; hydraulic fracturing; production testing; rig equipment; drilling rig service; offshore contract drilling; well intervention; drilling waste management services; subsea equipment; and more.

The Middle East oilfield services market is segmented by service type, location, well type, and geography. By service type, the market is segmented into drilling services, drilling and completion fluids, formation evaluation, completion and production services, drilling waste management services, and other services. By well type, the market is divided into conventional and unconventional. By location, the market is segmented into onshore and offshore, and by geography, the market is segmented into Saudi Arabia, Qatar, the United Arab Emirates, Iran, and the rest of the Middle East. For each segment, market sizing and forecasts have been done based on revenue capacity in USD billion.

By Service Type

| Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) |

| Production and Intervention Services |

| Other Services (OSV, seismic, decomm., aviation) |

By Location

| Onshore |

| Offshore |

By Well Type

| Conventional |

| Unconventional |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Iran |

| Rest of Middle East |

| By Service Type | Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) | |

| Production and Intervention Services | |

| Other Services (OSV, seismic, decomm., aviation) | |

| By Location | Onshore |

| Offshore | |

| By Well Type | Conventional |

| Unconventional | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Iran | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the projected value of the Middle East oilfield services market in 2031?

The market is forecast to reach USD 40.56 billion by 2031.

Which service segment is growing fastest in the region?

Production and intervention services are expanding at a 7.5% CAGR through 2031.

Why are offshore projects gaining importance in the Gulf?

Large gas developments in the UAE and Qatar require deepwater drilling and subsea completions, driving a 9.4% offshore CAGR.

How are local-content rules affecting contract awards?

Mandates such as Saudi IKTVA and UAE ICV favor companies with domestic manufacturing and workforce commitments, shifting share toward regional players.

What constraint most limits large-scale shale development?

Water availability poses a key challenge, increasing costs and prompting desalination and recycling solutions.

Which country is expected to post the highest spending growth?

The United Arab Emirates is poised for a 5.9% CAGR in oilfield service spending between 2026 and 2031.

Page last updated on: