Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

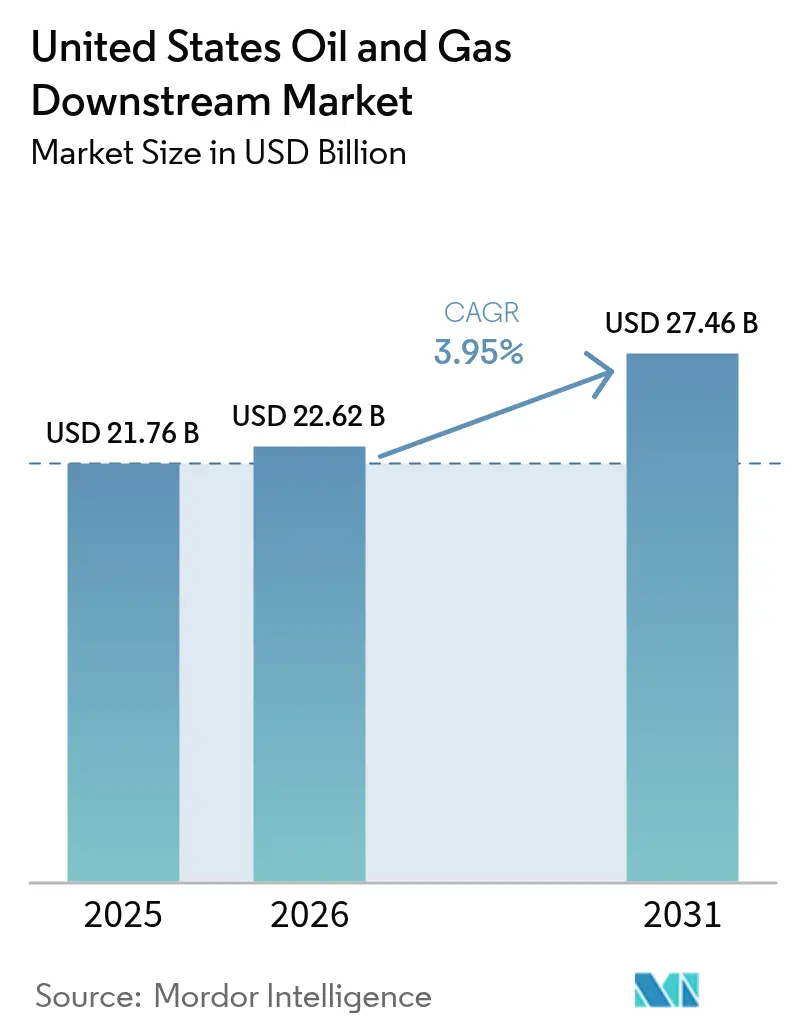

| Base Year Market Size (2025) | USD 21.76 Billion |

| Market Size (2026) | USD 22.62 Billion |

| Market Size (2031) | USD 27.46 Billion |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

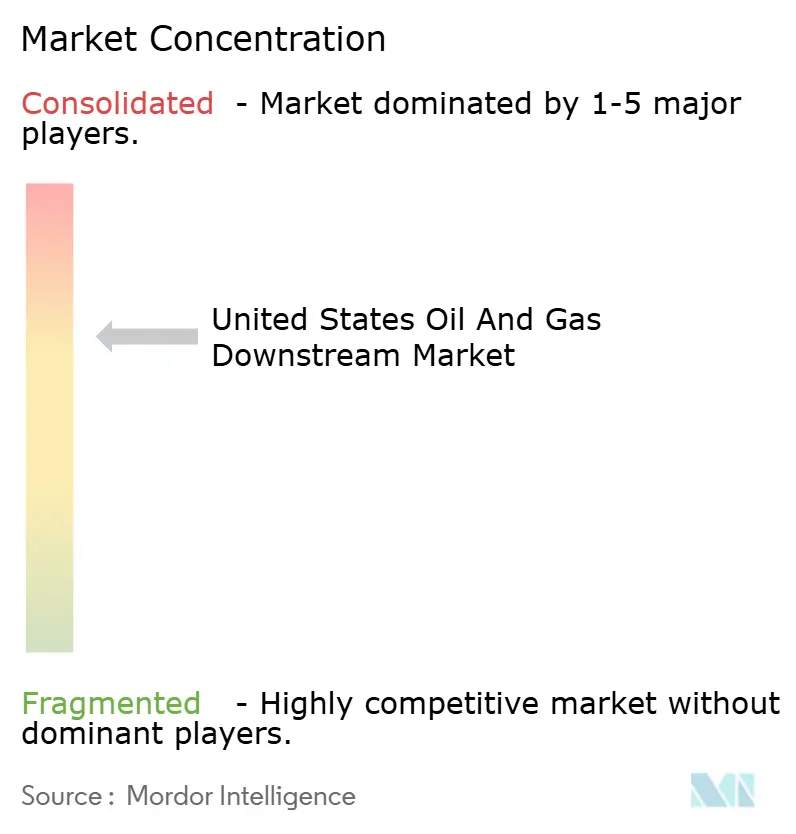

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Oil And Gas Downstream Market Analysis by Mordor Intelligence

The United States Oil And Gas Downstream Market size in 2026 is estimated at USD 22.62 billion, growing from 2025 value of USD 21.76 billion with 2031 projections showing USD 27.46 billion, growing at 3.95% CAGR over 2026-2031.

Refinery modernization outlays exceeding USD 15 billion annually, a steady 2.1% rise in national vehicle-miles traveled (VMT) during 2023, and new petrochemical capacity anchored to advantaged ethane feedstock keep the United States' oil and gas downstream market on a growth footing despite intensifying energy-transition pressures. Operators are blending traditional fuels with renewable diesel and sustainable aviation fuel, installing digital twin platforms that raise utilization by up to 15%, and leveraging USD 85-per-ton carbon-capture tax credits to defend margins. Strategic investments in Gulf Coast complexes continue to draw capital toward integrated refining and petrochemical hubs, while West Coast facilities shift toward low-carbon products to offset stricter environmental mandates.

Key Report Takeaways

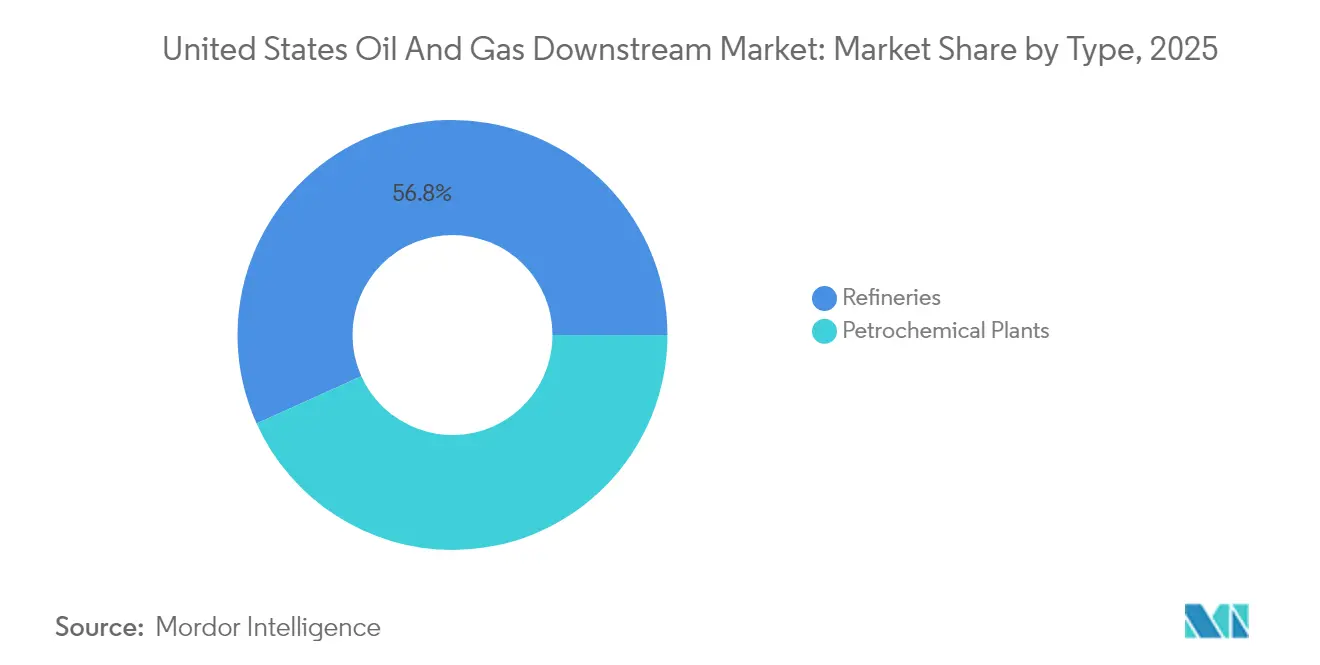

- By type, refineries led with a 56.75% revenue share of the United States' oil and gas downstream market size in 2025; petrochemical plants are projected to post the fastest growth at a 4.12% CAGR through 2031.

- By product category, refined petroleum products held 54.05% of the United States oil and gas downstream market share in 2025, whereas petrochemicals are poised to grow at a 4.25% CAGR to 2031.

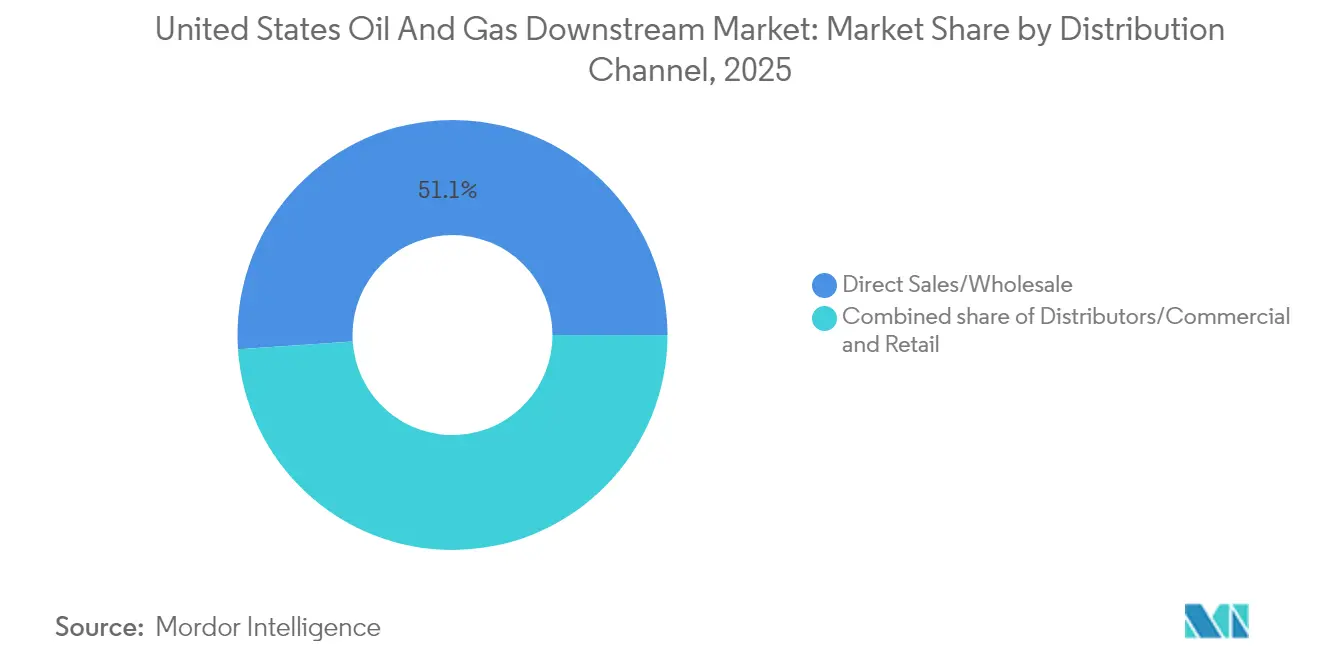

- By distribution channel, direct and wholesale sales controlled 51.05% of revenue in 2025, while retail outlets integrating EV charging are forecast to register the steepest 4.45% CAGR through 2031.

- By geography, Gulf Coast facilities represented nearly 49.60% of national capacity in 2025, and the region is expected to outpace other PADDs with a 4.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising gasoline demand from sustained VMT growth | +0.80% | National; highest expansion in Sun Belt states | Medium term (2-4 years) |

| Planned refinery modernization & capacity additions | +1.20% | Gulf Coast PADD 3 and select Midwest assets | Long term (≥ 4 years) |

| Surging petrochemical feedstock demand | +0.90% | Gulf Coast and emerging Appalachian sites | Medium term (2-4 years) |

| Expansion of renewable diesel & SAF projects | +0.70% | Early adopters on West Coast and Gulf Coast | Long term (≥ 4 years) |

| Carbon-capture tax-credit-driven projects | +0.30% | Industrial corridors in Texas and Louisiana | Long term (≥ 4 years) |

| AI-based refinery optimization & margin gains | +0.50% | Nationwide, quickest uptake in integrated complexes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Gasoline Demand from Sustained VMT Growth

U.S. VMT reached 3.26 trillion miles in 2023, a 2.1% year-over-year increase, and this momentum anchors the baseline transportation fuel demand even as EV penetration accelerates. E-commerce fulfillment and last-mile logistics are lifting diesel and gasoline consumption at a pace that counterbalances slower passenger-car volumes. Sun Belt states lead with annual VMT increases above 3%, propelled by population inflows and construction activity. The U.S. Department of Transportation projects that commercial-vehicle mileage will grow at double the pace of passenger travel through 2027, providing refiners with a reliable user base for gasoline, diesel, and jet fuel production.(1)U.S. Department of Transportation, “Freight Analysis Framework Version 5,” transportation.gov The predictable demand profile aids capacity-planning decisions and undergirds the 4.00% CAGR outlook for the United States oil and gas downstream market.

Planned Refinery Modernization & Capacity Additions

More than USD 15 billion in announced projects are revamping U.S. plants, with the Gulf Coast absorbing the largest share. ExxonMobil’s USD 2 billion Beaumont expansion adds 250,000 barrels per day (b/d) of throughput, while Chevron’s USD 475 million Pasadena revamp lifts capacity by 15% and equips the site to process heavier crudes.(2)Exxon Mobil Corporation, “Beaumont Refinery Expansion Fact Sheet,” exxonmobil.com Marathon Petroleum’s USD 2.5 billion renewable-diesel build-out exemplifies the dual path of investing in both legacy and low-carbon fuel lines. New hydrocrackers and fluid catalytic crackers raise middle-distillate yields, improve energy efficiency by up to 8%, and future-proof plants for shifting crude slates. The modernization cycle expands the installed base that feeds the United States oil and gas downstream market while nudging average operating costs downward.

Surging Petrochemical Feedstock Demand

Ethane demand increased by 9% in 2022, driven by both domestic and export-driven ethylene production. Refiners are integrating petrochemical units into existing operations to capitalize on this trend; ExxonMobil’s USD 2 billion Baytown upgrade and Chevron Phillips Chemical’s ethylene additions capture scale synergies and enhance cash margins.(3)Chevron Phillips Chemical, “U.S. Gulf Coast Petrochemical Project Overview,” cpchem.com Integrated complexes benefit from shared utilities and lower transport costs, allowing them to shift between fuels and chemicals as market signals dictate. Petrochemical-grade propylene has commanded premiums of 15-25% over refinery-grade supply, an incentive that accelerates investment in propylene recovery systems. These dynamics channel capital toward integrated energy and chemicals models that stabilize earnings across demand cycles.

Expansion of Renewable Diesel & SAF Projects

Diamond Green Diesel earmarked USD 315 million to retrofit Port Arthur for sustainable aviation fuel (SAF), and USA BioEnergy intends to spend USD 2.8 billion on a Texas SAF complex.(4)Valero Energy Corporation, “Diamond Green Diesel Investor Presentation February 2025,” valero.com Shell redirected USD 1.5 billion to convert its Convent site into a 340,000 b/d renewable-diesel hub, signaling a decisive strategic shift. The Renewable Fuel Standard and California’s Low Carbon Fuel Standard underpin margins through RIN credits and carbon-credit premiums. Phillips 66’s Rodeo conversion retires 120,000 b/d of gasoline capacity but installs an equivalent volume of renewable diesel, illustrating portfolio rebalancing toward low-carbon output. Such projects expand the product palette available to the United States oil and gas downstream market and open high-value export lanes to regions with SAF mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV adoption curbing gasoline demand | -0.60% | West Coast early adoption, national expansion | Medium term (2-4 years) |

| Federal & state decarbonization compliance costs | -0.40% | California, Northeast states with strict standards | Long term (≥ 4 years) |

| Water-stress-driven effluent restrictions at refineries | -0.30% | Texas, California drought-prone regions | Medium term (2-4 years) |

| Skilled labor shortages for turn-arounds & projects | -0.20% | Gulf Coast, Midwest refining centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Adoption Curbing Gasoline Demand

Electric-vehicle (EV) sales crossed 1.4 million units in 2023, taking 9.1% of total U.S. light-duty registrations. California leads with a 25% share, while Washington and Oregon account for over 15%, creating localized dips in gasoline demand. The USD 7.5 billion national charging-network rollout under the Infrastructure Investment and Jobs Act compresses adoption timelines, and purchase credits valid through 2032 keep consumer interest high. Fleet operators in dense urban corridors are electrifying vans and step-trucks to capture lifecycle savings, reducing diesel demand on specific routes.

Federal & State Decarbonization Compliance Costs

California’s Cap-and-Trade system and the Northeast’s Regional Greenhouse Gas Initiative impose carbon costs of USD 20-30 per metric ton, adding 3-5 cents per gallon to refinery operating expenses. EPA effluent-rule revisions will require USD 200 million upgrades at large facilities, while water-stress restrictions in Texas and California elevate utility charges. Annual compliance outlays between USD 50-100 million per plant erode margins and influence shutdown or conversion decisions, particularly at smaller West Coast sites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rising Petrochemical Integration Strengthens Earnings

Plants classified as refineries generated 56.75% of 2025 revenue inside the United States oil and gas downstream market, but petrochemical facilities are expected to advance at a 4.12% CAGR to 2031, the fastest pace among asset types. ExxonMobil's USD 2 billion Baytown investment underscores the strategic migration toward integrated footprints that share utilities, lower feedstock transport costs, and unlock high-margin chemical streams.

Integrated complexes can divert naphtha, butane, and ethane toward ethylene or propylene production when crack spreads narrow, cushioning cash flow. Historical data indicate that petrochemical plants are expected to grow at a rate of 2.8% annually from 2019 to 2024; the acceleration to 4.12% is attributed to the advantages of North American natural-gas liquids and expanding exports to Asia. Independent refineries must decide whether to pursue similar upgrades or risk compressing profitability in fuel-only models. The shift bolsters the long-term competitiveness of diversified operators and enhances the depth of the United States' oil and gas downstream market.

By Product Type: Chemicals Earn Premium Margins

Refined petroleum products accounted for 54.05% of overall revenue in 2025; however, petrochemicals are projected to grow at a 4.25% CAGR from 2026 to 2031, outperforming fuels. Ethylene, propylene, and benzene derived from refinery streams trade at 15-25% premiums to fuel-grade equivalents, giving integrated sites a defensible advantage. In contrast, middle-distillate profits increasingly track renewable-diesel credit pricing, injecting volatility.

Traditional lubricants maintain a stable customer base in industrial equipment, even as synthetics gain popularity, supporting a USD 15 billion sub-segment that delivers predictable cash flow. Renewable diesel and SAF, while still a fraction of total output, now earn RIN and LCFS credits that narrow the cost gap with petroleum jet and diesel grades. A growing emphasis on "margin per barrel" rather than volume is shaping investment and operating decisions across the United States' oil and gas downstream market.

By Distribution Channel: Retail Sites Reinvent for Electrification

Direct and wholesale channels held a 51.05% share of revenue in 2025, achieved through long-term contracts with distributors, fleets, and industrial end-users. Their scale enables refiners to capture a significant downstream margin, but retail outlets, comprising both branded and unbranded service stations, are forecast to expand revenue at a 4.45% CAGR through 2031.

Roughly 145,000 retail stations remain, down from more than 150,000 a decade earlier, yet surviving sites post higher per-store volumes and differentiated services. Shell and BP are installing fast chargers alongside gasoline dispensers, monetizing dwell time through convenience retail and maintenance services. Retail’s ability to serve both combustion and EV customers positions it as a growth lever inside the United States oil and gas downstream market and illustrates how downstream infrastructure adapts to a mixed-energy future.

Geography Analysis

Gulf Coast facilities accounted for nearly 49.60% of the 2025 national capacity, benefiting from access to onshore shale crude, offshore imports, and natural gas liquids suitable for petrochemicals. Integrated refinery-petchem complexes in Texas and Louisiana generate economies of scope, reinforcing the region’s central role in the United States' oil and gas downstream market. Refiners here also capture export premiums by shipping diesel and gasoline to Latin America and Europe via deep-water ports.

West Coast sites confront elevated compliance costs, restricted local crude supply, and tougher air-quality rules. Valero’s planned Benicia closure and Phillips 66’s Rodeo conversion will remove sizable petroleum processing capacity, yet add renewable diesel and SAF output that captures California LCFS and Cap-and-Trade credits. Although these changes shrink traditional volume, they diversify revenue streams.

Midwest refineries act as swing suppliers, balancing Gulf Coast imports with demand in the Mid-Continent region. Pipeline connectivity to Cushing and Chicago ensures a stable supply of crude and efficient evacuation of products. East Coast facilities rely increasingly on waterborne product imports due to constrained local capacity, while Rocky Mountain plants operate as isolated mini-systems with regional pricing power.

Overall, regional revenue is expected to rise at a 3.66% CAGR to 2031, lifted by Gulf Coast expansions and tempered by West Coast conversions.

Competitive Landscape

The top five operators—Marathon Petroleum, Valero Energy, Phillips 66, ExxonMobil, and Chevron—control about 40% of domestic refining capacity, signifying moderate concentration. Marathon leads with 3.0 million barrels per day (b/d) across 13 plants and complements this footprint with a retail network exceeding 6,000 branded stations. Valero operates 15 refineries that process 3.2 million barrels per day and co-owns the Diamond Green Diesel joint venture, which is scaling up renewable-diesel and SAF output.

Strategic focus increasingly rests on technology deployment and low-carbon offerings. Chevron’s alliance with Microsoft targets USD 500 million of AI-driven efficiency gains, while Phillips 66 allocates USD 850 million to repurpose Rodeo for renewable products. Independent players such as PBF Energy and HF Sinclair concentrate on niche geographies or specialty products to remain competitive.

Consolidation remains a plausible option as compliance costs rise and smaller plants struggle to fund necessary upgrades. Capital-intensive carbon-capture installations and renewable conversions favor operators with robust balance sheets. Public disclosures indicate that majors are steering 15-20% of their annual capital expenditures toward energy-transition projects, underscoring strategic hedging amid policy uncertainty.

United States Oil And Gas Downstream Industry Leaders

Marathon Petroleum Corp.

Chevron Corporation

Valero Energy Corporation

Exxon Mobil Corporation

Phillips 66

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ExxonMobil announced the completion of its USD 2 billion Beaumont refinery expansion, adding 250,000 barrels per day of processing capacity with advanced hydrocracking units that improve heavy crude processing capabilities and increase diesel yield by 12%.

- December 2024: Marathon Petroleum completed its USD 2.5 billion renewable diesel capacity expansion across multiple facilities, adding 1.2 billion gallons of annual production capability and positioning the company as the largest renewable diesel producer in North America.

- November 2024: Valero Energy and Darling Ingredients announced a USD 315 million investment in Diamond Green Diesel's Port Arthur facility to add sustainable aviation fuel production capability, targeting 470 million gallons of annual SAF capacity by 2026.

- October 2024: Phillips 66 completed the USD 850 million conversion of its Rodeo refinery to renewable fuels production, eliminating 120,000 barrels per day of traditional refining capacity while adding equivalent renewable diesel and sustainable aviation fuel production.

United States Oil And Gas Downstream Market Report Scope

The downstream sector includes processing, moving, and selling refined goods made from crude oil. Industry segments downstream include product marketing, supply and trading, and oil refining.

The US oil and gas downstream market is segmented by sector into refining and petrochemical. The report also covers the market size and forecasts for the US oil and gas downstream market. For each segment, the market sizing and forecasts have been done based on refining capacity (in a million barrels per day).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the projected value of the United States oil and gas downstream market by 2031?

The United States oil and gas downstream market is forecast to reach USD 27.46 billion by 2031, supported by a 3.95% CAGR over 2026-2031.

Which segment is expected to register the fastest volume growth through 2031?

Petrochemical plants are set to expand at a 4.12% CAGR, the fastest among asset types, as refiners integrate chemical production for higher margins.

How are refiners responding to rising EV adoption?

Operators are blending renewable diesel, installing EV chargers at retail sites, and leveraging carbon-capture credits to mitigate gasoline-demand erosion.

Why is the Gulf Coast dominant in downstream capacity?

The Gulf Coast benefits from proximity to shale crude, natural-gas liquids, and deep-water ports, giving it about 49.60% of national capacity and a 4.05% CAGR outlook.

What role does artificial intelligence play in downstream operations?

AI-driven digital twins and predictive maintenance systems have reduced unplanned downtime by 20% and generated savings of up to USD 2 billion annually for leading refiners.

Page last updated on: