Market Overview

| Study Period | 2021 - 2031 |

|---|---|

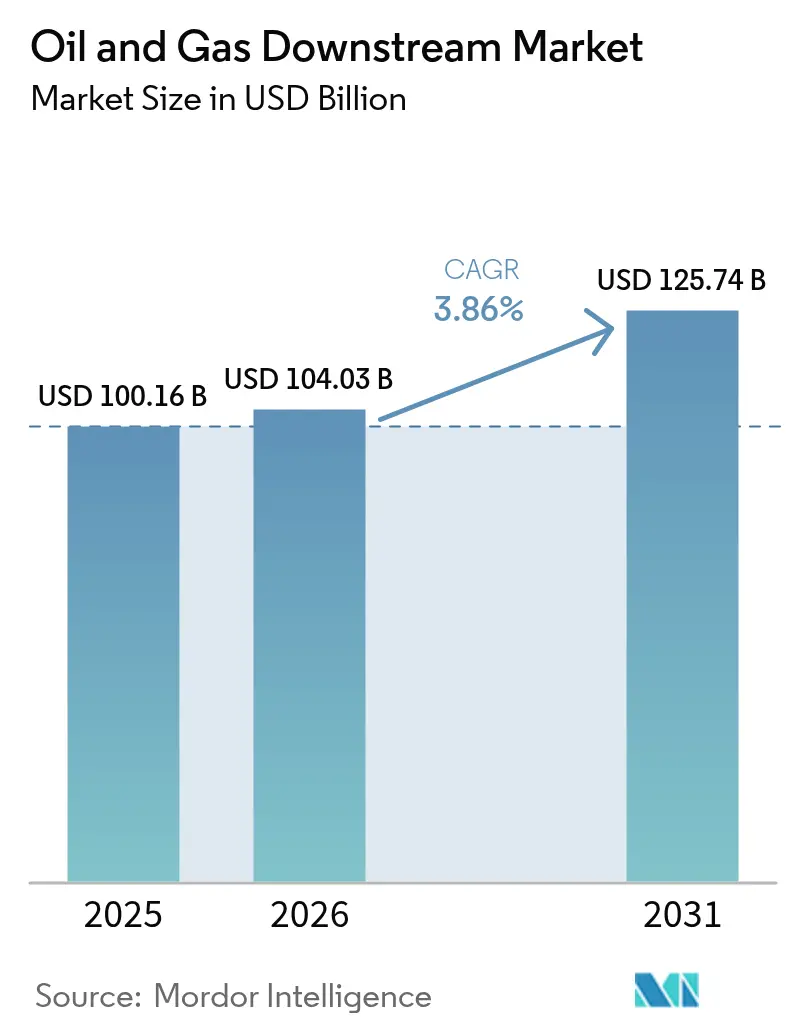

| Market Size (2026) | USD 104.03 Billion |

| Market Size (2031) | USD 125.74 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas Downstream Market Analysis by Mordor Intelligence

Oil And Gas Downstream Market size market size in 2026 is estimated at USD 104.03 billion, growing from 2025 value of USD 100.16 billion with 2031 projections showing USD 125.74 billion, growing at 3.86% CAGR over 2026-2031.

Expansion is driven by capacity additions in the Asia-Pacific region, rising petrochemical integration, and sustained demand for diesel and jet fuel, even as gasoline volumes ease in electrified transport corridors. Tight sulfur rules, aviation fuel mandates, and digital twin optimization collectively lift margins, while elevated interest rates and net-zero pledges temper greenfield spending. Competitive dynamics feature integrated operators shifting toward higher-value chemical feedstocks, leveraging hydrogen monetization, and exploiting scale advantages in refining and petrochemical complexes. Investment flows concentrate where feedstock is advantaged, regulations are supportive, and product-export routes are efficient, positioning the oil and gas downstream market for steady, if selective, growth through the decade.

Key Report Takeaways

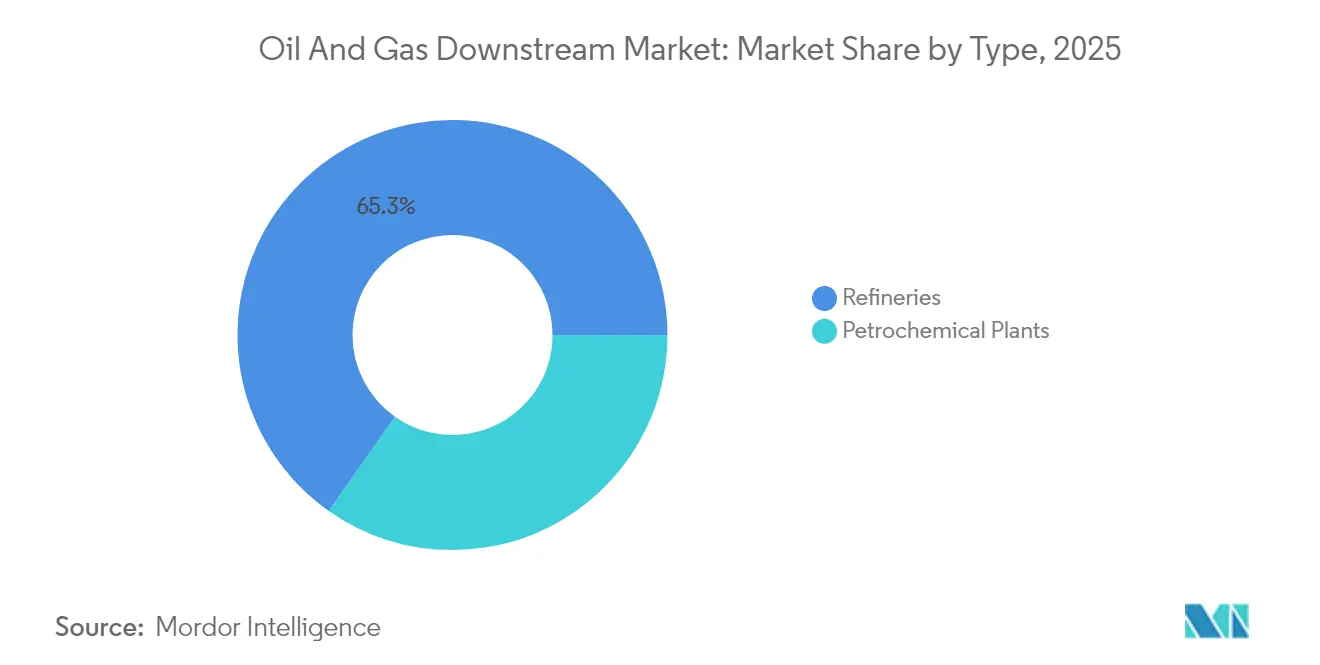

- By type, refineries captured 65.25% of the Oil & Gas Downstream market share in 2025, while petrochemical plants are set to log the fastest expansion at a 4.72% CAGR to 2031.

- By product type, refined petroleum products commanded 69.75% of the Oil & Gas Downstream market size in 2025; petrochemicals, however, are projected to advance at a 4.22% CAGR over the same horizon.

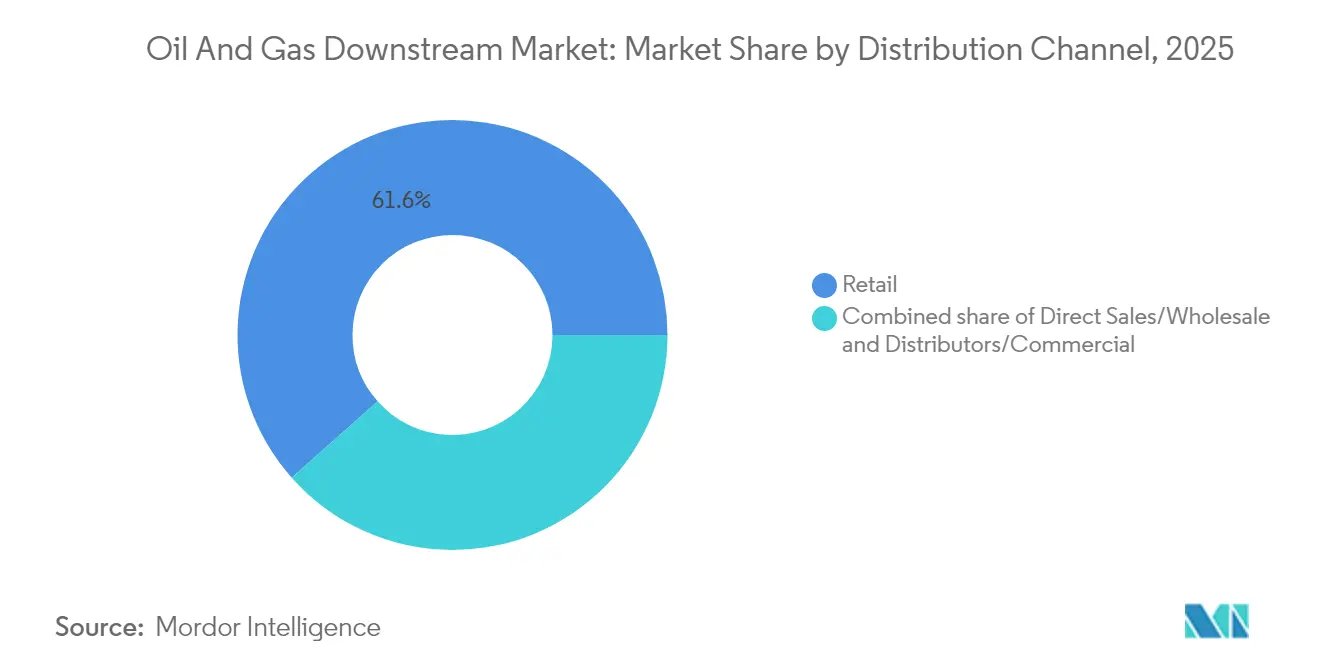

- By distribution channel, retail networks dominated with 61.55% revenue share in 2025, and this channel is projected to expand at a 4.41% CAGR through 2031.

- By geography, Asia-Pacific held 32.85% of 2025 sales and is expected to post the quickest regional growth at 4.92% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in refining capacity | 1.20% | APAC core, Middle East | Medium term (2-4 years) |

| Booming petrochemical demand | 0.90% | Global, APAC lead | Long term (≥ 4 years) |

| Stricter IMO sulfur rules | 0.60% | Global maritime | Short term (≤ 2 years) |

| Aviation-fuel rebound & SAF mandates | 0.70% | North America, EU | Medium term (2-4 years) |

| Digital-twin/AI OPEX optimization | 0.50% | Global early adopters | Long term (≥ 4 years) |

| Hydrogen co-product monetization | 0.40% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Refining Capacity Expansion Drives Regional Rebalancing

Asia-Pacific and Middle Eastern projects, totaling 4.9 million b/d between 2024 and 2028, are tilting global economics toward these hubs, giving integrated operators scale and feedstock proximity advantages while compressing European and North American margins.[1]U.S. Energy Information Administration, “International Energy Outlook,” eia.gov

Petrochemical Demand Growth Transforms Refinery Economics

Petrochemicals already account for 14% of global oil demand and are expected to rise further, prompting refiners to reconfigure their operations toward naphtha cracking and aromatics extraction in integrated complexes, as exemplified by Saudi Aramco’s Motiva and China’s coastal mega-projects.[2]International Energy Agency, “The Future of Petrochemicals,” iea.org

IMO Sulfur Regulations Drive Ongoing Compliance Investments

Very-low-sulfur fuel oil now dominates bunker sales, rewarding refiners with desulfurization units and prompting shifts in crude slate, secondary unit revamps, and new outlets for marine gas oil and methanol.

Aviation-Fuel Recovery and SAF Mandates Create New Revenue Streams

The rebound in jet-fuel demand, paired with the U.K.’s 10% SAF mandate by 2030 and U.S. capacity reaching 15.8 million gallons in 2024, opens up premium niches for HEFA and power-to-liquids pathways at refineries with feedstock flexibility.[3]UK Department for Transport, “Sustainable Aviation Fuel Mandate Consultation,” gov.uk

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV penetration eroding gasoline demand | -0.80% | North America, Europe | Medium term (2-4 years) |

| Net-zero policies curbing fossil fuels | -0.60% | Europe, North America | Long term (≥ 4 years) |

| Climate-risk downtime & insurance | -0.40% | Gulf Coast, coastal sites | Short term (≤ 2 years) |

| High interest rates limit projects | -0.50% | Global, emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle Adoption Pressures Gasoline Demand Fundamentals

Global EV sales reached 14 million units in 2024, accelerating the decline in gasoline demand in Europe and certain segments of China, prompting refiners to shift their focus toward diesel, jet fuel, and petrochemicals.

Net-Zero Climate Policies Constrain Long-Term Investment Horizons

EU Fit-for-55 measures and U.S. low-carbon standards place a price on carbon, deterring long-duration crude units and nudging capital toward renewable integration and flexible product slates.[4]European Commission, “Fit for 55 Package,” europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Integrated refineries sharpen competitive edge

Refineries accounted for 65.25% of the Oil & Gas Downstream market in 2025 and should advance at a 4.52% CAGR, a pace underpinned by asset-utilization upgrades and petrochemical add-ons. This segment benefits from a flexible configuration that toggles between transport fuels and chemical feedstocks based on real-time margin signals. Saudi Aramco’s Motiva expansion and Reliance’s Jamnagar complex exemplify the scale synergies that lower per-barrel costs and enhance hydrocracker yields. Integrated builds blur the lines with petrochemical plants, raising barriers for smaller standalone facilities.

Petrochemical plants, although holding a smaller 34.75% share, post a 4.72% trajectory as naphtha crackers and propane dehydrogenation units proliferate in the Asia-Pacific region. Operators bundle shared utilities, logistics, and hydrogen networks to exploit co-product valorization. Yet feedstock-price swings and competition from integrated mega-sites temper standalone economics. Overall, the Oil & Gas Downstream market size gains resilience from this dual-track capacity strategy.

By Product Type: Refined petroleum products sustain volume leadership

Refined petroleum products accounted for 69.75% of the Oil & Gas Downstream market size in 2025 and are expected to grow at a rate of 4.05% annually, as diesel, jet, and compliant marine fuels offset the decline in gasoline barrels. Aviation recovery and IMO sulfur rules underpin volume stability, while diesel’s role in freight and off-road machinery remains robust. Petrochemicals, although an embedded subset, outpace fuels as demand for packaging, automotive, and construction intensifies across the APAC region.

Lubricants occupy a niche but lucrative corner, leveraging longer drain intervals and industrial specialty grades that secure premium realization. As electrified drivetrains grow, automotive lubricant volumes ease, but industrial and marine sectors sustain baseline demand. Product-mix optimization, therefore, becomes a core competency for operators seeking to lift margins in the Oil & Gas Downstream market.

By Distribution Channel: Retail stations secure margin advantages

Retail outlets generated 61.55% of 2025 revenue and are projected to log a 4.41% CAGR through 2031, attesting to their pricing power, brand leverage, and data-rich customer interfaces. Loyalty apps and on-site convenience retail diversify earnings, guarding against fuel-only margin compression. Direct sales and wholesale shipments remain vital for industrial volumes and fleet contracts, but yield thinner spreads.

Digitally enabled service-station formats now bundle EV charging, food service, and parcel lockers, anchoring foot traffic while cushioning the transition from internal-combustion to low-carbon mobility. Such diversification helps the oil and gas downstream market maintain its relevance in the retail sector even as vehicle fleets electrify.

Geography Analysis

The Asia-Pacific region leads with a 32.85% share in 2025 and is expected to grow at a rate of 4.92% annually due to capacity surges in China, India, and Southeast Asia, where demographic tailwinds, industrialization, and policy support converge. China’s petrochemical pull counters peaking gasoline use, while Indian refiners chase export premiums to Africa and Latin America. Indonesia, Malaysia, and Thailand strengthen their product balance through hub-and-spoke logistics along vital sea lanes.

North America, despite a decline in gasoline demand, exploits ethane-rich shale to feed petrochemical crackers and hydrotreaters, thereby anchoring competitive cash costs. U.S. consolidators such as Phillips 66 retrofit units for renewable diesel to align with California’s LCFS and federal SAF incentives. Canada’s heavy-oil upgraders and Mexico’s government-driven builds diversify feedstock slates, though financing hurdles persist for new standalone capacity.

Europe navigates declining fuel volumes under the Fit-for-55 umbrella by converting sites into bio-hubs producing HVO and SAF, while integrating CCS clusters to mitigate residual CO₂. Middle Eastern projects, such as ADNOC’s Ruwais Phase II, leverage gas-liquids streams and subsidized utilities to serve EU and Asian importers. Africa is witnessing emerging complexes in Nigeria and Angola, but it is contending with capital scarcity. Meanwhile, Brazil’s Petrobras balances domestic demand coverage with volatility in currency and policy cycles, collectively steering the regional mosaic of the oil and gas downstream market.

Competitive Landscape

The oil and gas downstream market exhibits moderate concentration, with numerous regionally entrenched competitors. Saudi Aramco, Sinopec, Exxon Mobil, and Shell anchor the global league, yet none surpasses a 12% revenue stake, preserving competitive plurality. Strategies center on integration: combining refining, petrochemical, and power assets to unlock economies of scope and capture higher-margin chemical streams. Operators prioritizing digital-twin analytics and predictive maintenance, such as Shell and TotalEnergies, achieve throughput gains and energy-intensity reductions that widen their EBITDA spreads.

Portfolio realignment remains brisk. Chevron’s USD 53 billion Hess takeover extended feedstock access and U.S. Gulf Coast refining heft, while Energy Transfer’s WTG Midstream purchase sharpened logistics reach in Permian supply corridors. Private-equity vehicles continue cherry-picking mid-sized North American refineries, aggregating assets for scale. Meanwhile, APAC national oil companies are tilting their capital toward integrated build-outs that embed plastics and chemicals alongside fuels—a hedge against long-term gasoline erosion.

Innovation hotspots include SAF, renewable diesel, and hydrogen as key vectors for decarbonization. Phillips 66, TotalEnergies, and Valero repurpose hydrotreaters for HVO and HEFA pathways, accessing low-carbon credit revenue streams. Europe’s carbon-pricing regimes and the U.S. IRA incentives accelerate these pivots, reshaping product mixes across the oil and gas downstream market.

Oil And Gas Downstream Industry Leaders

BP PLC

Saudi Aramco

China Petroleum & Chemical Corp. (Sinopec)

Exxon Mobil Corporation

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Chevron Corporation completed its USD 53 billion acquisition of Hess Corporation, expanding downstream capacity and global reach.

- September 2025: Energy Transfer LP finalized a USD 2.3 billion buyout of WTG Midstream, reinforcing crude and product logistics in key shale basins.

- August 2025: Veren Inc. merged with Whitecap Resources in a USD 15 billion deal, bolstering heavy-oil supply for North American refiners.

- July 2025: Saudi Aramco unveiled a USD 8 billion, 250,000 b/d expansion at its Motiva Texas site, emphasizing the integration of petrochemicals.

Global Oil And Gas Downstream Market Report Scope

The oil and gas downstream sector encompasses refining crude oil into various petroleum products and processing natural gas into usable products. It includes refining crude oil into gasoline, diesel, jet fuel, and other products and producing petrochemicals such as plastics, fertilizers, and synthetic materials.

The market is segmented by type and geography. By type, the market is segmented into refinery and petrochemical plants. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa.

For each segment, the market sizes and forecasts were made based on revenue (USD).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Refineries | |

| Petrochemical Plants | ||

| By Product Type | Refined Petroleum Products | |

| Petrochemicals | ||

| Lubricants | ||

| By Distribution Channel | Direct Sales/Wholesale | |

| Distributors/Commercial | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Oil & Gas Downstream market in 2026?

It is projected to close 2026 at USD 104.03 billion, tracking the 3.86% CAGR outlined in this analysis.

Which region leads downstream growth this decade?

Asia-Pacific leads, expanding at a 4.92% CAGR on the back of Chinese and Indian integrated complex additions.

What is driving jet-fuel and SAF demand?

Post-pandemic flight recovery and mandates such as the U.K.’s 10% SAF target by 2031 are lifting jet-fuel volumes and premium SAF margins.

How are refiners mitigating gasoline demand decline?

They pivot toward diesel, jet fuel, and petrochemicals, retrofit units for renewable fuels, and monetize surplus hydrogen.

What operational technologies boost refinery margins?

Digital twins and AI-based predictive maintenance cut downtime and energy use, translating into measurable EBITDA gains.

Which product segment grows fastest through 2031?

Petrochemicals outpace fuels as global plastics, packaging, and specialty-chemical demand continues to rise.

Page last updated on: