Offshore Oilfield Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 45.46 Billion |

| Market Size (2031) | USD 63.13 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

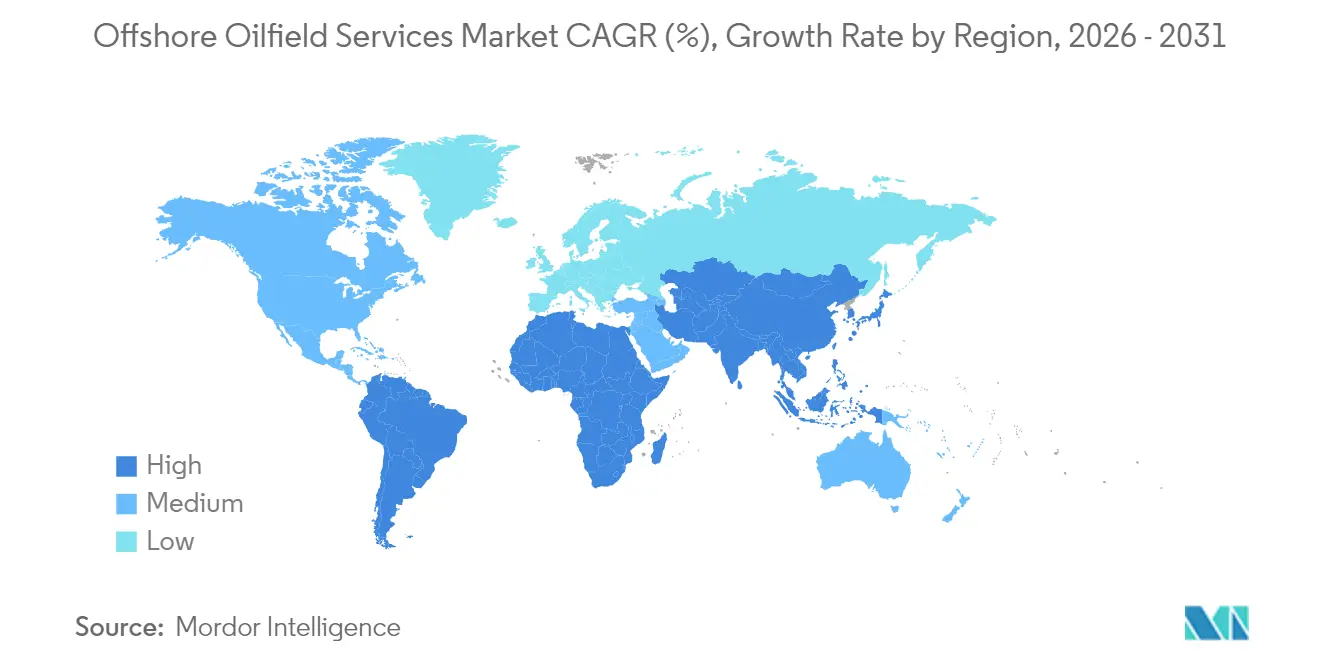

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Oilfield Services Market Analysis by Mordor Intelligence

Offshore Oilfield Services Market size in 2026 is estimated at USD 45.46 billion, growing from 2025 value of USD 42.57 billion with 2031 projections showing USD 63.13 billion, growing at 6.78% CAGR over 2026-2031.

Rebounding deep- and ultra-deepwater projects, tighter availability of premium rigs, and mandates for lower-emission operations contribute to the renewed momentum. Operators channel capital toward high-impact barrels while utilizing digital tools to enhance drilling efficiency and maintain breakeven costs below USD 50 per barrel. Contractors respond by expanding high-specification fleets, integrating real-time analytics into well delivery, and aligning with national content policies to secure long-term charters. Energy-security agendas in Asia-Pacific and the Middle East underpin multiyear drilling programs, while South American pre-salt developments anchor the next growth frontier.

Key Report Takeaways

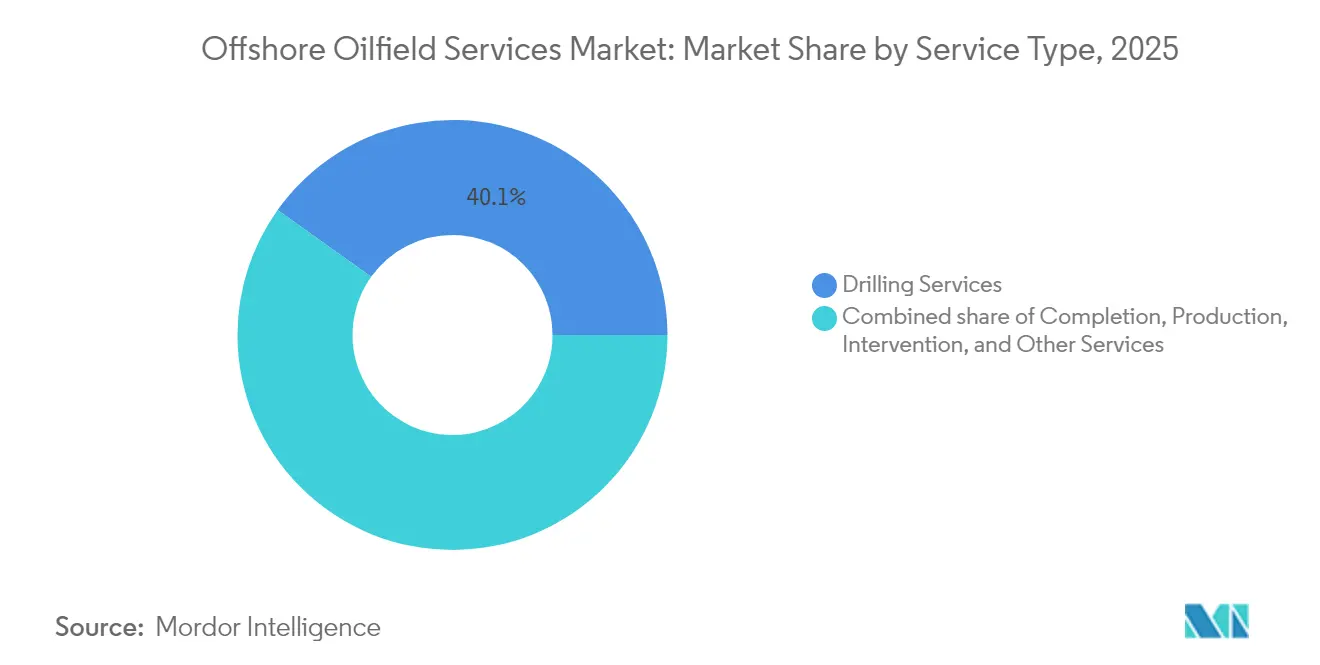

- By service type, drilling held 40.12% of the offshore oilfield services market share in 2025; production and intervention services are forecast to expand at a 7.25% CAGR through 2031.

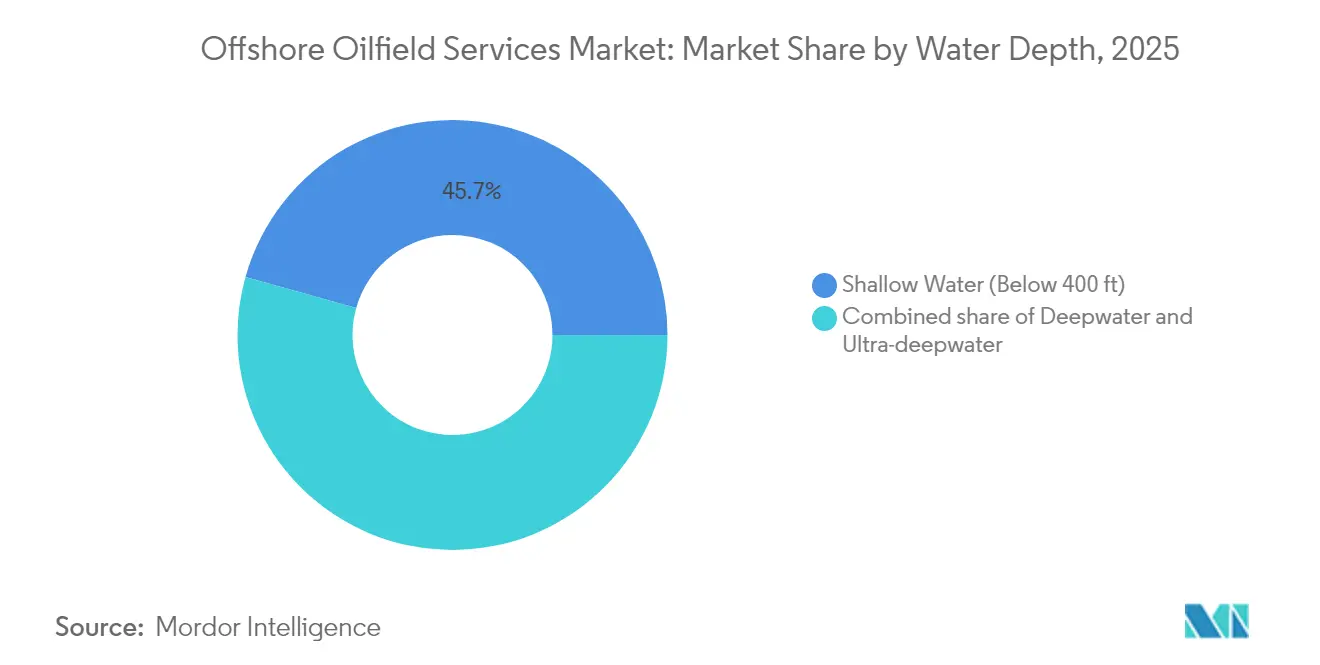

- By water depth, shallow-water operations below 400 ft led with 45.65% share in 2025; ultra-deepwater projects above 5,000 ft are set to grow at an 8.12% CAGR to 2031.

- By geography, Asia-Pacific commanded 47.15% of 2025 revenue, while South America is projected to record an 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Offshore Oilfield Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep- & ultra-deepwater drilling up-cycle | +0.9% | Gulf of Mexico, Brazil, West Africa | Medium term (2-4 years) |

| Modern jack-up and 7G drillship shortage | +0.7% | Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Energy-security charter push in Asia & MENA | +0.6% | Asia-Pacific core, spill-over to MENA | Long term (≥ 4 years) |

| Digital-first integrated service contracts | +0.5% | North America, Europe, global follow-on | Medium term (2-4 years) |

| Decommissioning wave in mature basins | +0.4% | UKCS, Australia, Gulf of Mexico | Long term (≥ 4 years) |

| Methane-credit rules for offshore vessels | +0.3% | Europe, North America, global enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-cycle in Deep- & Ultra-Deepwater Drilling Commitments

Drillship utilisation is on track to hit 97% in 2025, a sharp reversal from the lows of 2020, as projects such as SLB’s USD 800 million Trion contract in Mexico and BP’s Kaskida development re-enter execution phases[1]Schlumberger, “2025 Market Outlook,” slb.com. Namibia’s recent multi-billion-barrel finds add fresh acreage to the deepwater pipeline. Contractors lean on dual-BOP drillships, dynamic positioning, and subsea processing to unlock once uneconomic resources. Operators, confident in long-run demand, accept longer lead times in exchange for scalable barrels and inject digital twins to keep well costs predictable. Ultra-deepwater reservoirs above 5,000 ft therefore emerge as core acreage for future production growth.

Supply–Demand Crunch for Modern Jack-ups & 7G Drillships

Seventh-generation drillships now command day rates near USD 500,000 and secure multi-year deals, exemplified by Noble Corporation’s fleet expansion and USD 7.5 billion backlog following its Diamond Offshore purchase[2]Noble Corporation, “Noble Completes Diamond Offshore Acquisition,” noblecorp.com. Jack-up utilisation is projected to be 86% in 2025 across Southeast Asia and the Middle East, where shallow-water demand remains resilient. Limited newbuild activity since 2015, combined with the accelerated scrapping of older rigs, underpins the tightness. Operators therefore lock in rigs earlier and for longer terms, while contractors fast-track reactivations and invest in dual-activity upgrades to capture premium pricing.

National Energy-Security Push in Asia & MENA

Long-term charters are gaining traction as governments prioritize domestic output. Qatar committed more than USD 5 billion to offshore LNG and oil developments, while Kuwait extended its six-well offshore campaign to 2026. China launched the Meng Xiang deep-ocean vessel, capable of drilling 11 km, signaling its intent to reduce foreign rig reliance. These charters often include technology-transfer clauses and local-content quotas, reshaping service models and giving regional contractors larger roles.

Digital-First Integrated Service Contracts

Baker Hughes’ AI-enabled well optimisation for Saudi Aramco reduced non-productive time by double-digit percentages, demonstrating real-time optimisation at scale[3]Baker Hughes, “AI-Enabled Drilling Optimisation Case Study,” bakerhughes.com. Oceaneering International’s connected ROV fleet shows similar gains in subsea inspection. Operators are increasingly bundling drilling, completions, and production monitoring into outcome-based contracts, shifting risk to service providers that can deliver data-driven execution. This digital shift is especially valuable in deepwater, where real-time alerts prevent high-cost downtime and improve safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SEMI-sub day-rate compression amid fleet over-capacity | -0.5% | Global, particularly North Sea and Gulf of Mexico | Short term (≤ 2 years) |

| FX-driven cost inflation for crew & consumables | -0.4% | Global, with acute impact in emerging markets and cross-border operations | Short term (≤ 2 years) |

| ESG-driven capital rationing by Western lenders | -0.3% | North America & EU, with spillover to global projects | Medium term (2-4 years) |

| Chronic shortage of HPHT-graded BOP spare parts | -0.2% | Global deepwater operations, concentrated in Gulf of Mexico, Brazil, West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semi-Sub Day-Rate Compression Amid Fleet Over-Capacity

Fifth- and sixth-generation semi-submersibles face muted demand as deepwater clients pivot to more versatile drillships. Several Gulf of Mexico units roll off contract in 2025 without timely follow-up work, pulling regional utilisation below fleet averages. Operating costs for semi-submersibles remain higher than those of drillships at comparable water depths, limiting their competitiveness outside specific harsh-environment niches. Contractors defer upgrades and, in some cases, recycle ageing units to stabilise supply. The imbalance weighs on profitability and acts as a drag on new technology investment.

ESG-Driven Capital Rationing by Western Lenders

Banks in Europe and North America are attaching stricter emissions criteria to upstream funding, thereby rerouting some capital toward renewables. Smaller independents struggle to secure project finance and often look to national oil companies or specialised energy lenders willing to accept higher carbon footprints. The funding gap accelerates asset divestitures, prompting consolidation in the offshore oilfield services industry as larger players use balance-sheet strength to acquire distressed assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Drilling Dominance Amid Production Growth

Drilling services continued to lead the offshore oilfield services market with 40.12% revenue share in 2025, supported by capital-intensive rigs that remain indispensable for field development. The offshore oilfield services market size tied to drilling is driven by long-cycle deepwater projects that require high-specification assets for several years. High day-rates improve contractor margins and enable reinvestment in dual-activity and automation upgrades. Completion and workover scopes expand as designs become more complex, while data-rich logging guides stimulation programs that enhance recovery factors.

Production and intervention services are poised for a 7.25% CAGR through 2031 as operators maximise output from existing wells using coiled-tubing, wireline, and hydraulic intervention packages. This pivot aligns with capital discipline, offering shorter payback windows compared with new field developments. Ancillary services—such as seismic, aviation, offshore support vessels, and decommissioning—add resilience to the offshore oilfield services market, broadening contractor portfolios. Seadrill’s merger talks with Transocean exemplify the sector’s consolidation drive, aiming for operating synergies and balanced exposure across drilling and production services.

By Water Depth: Shallow Foundations, Ultra-Deep Frontiers

Shallow-water campaigns below 400 ft accounted for 45.65% of 2025 revenue, as jack-ups delivered cost-effective solutions in the Middle East, Southeast Asia, and Mexico. Established pipelines, processing hubs, and shorter development cycles keep operating costs low, enabling national oil companies to secure rapid production additions. The offshore oilfield services market size associated with shallow-water rigs remains sizable, yet growth moderates as easy barrels decline.

Ultra-deepwater projects above 5,000 ft are expected to register the fastest 8.12% CAGR to 2031, driven by pre-salt Brazil, frontier Namibia, and resource-rich US Gulf prospects. Floating production units, long-distance tiebacks, and next-generation blowout preventer systems increase service complexity and value per well. China’s Meng Xiang vessel, capable of drilling to a depth of 11 km, underscores the technology race to reach deeper reservoirs. Contractors that combine rig capability with integrated well services capture larger work scopes and higher margins, reinforcing a two-track market where shallow-water volume supports stability and ultra-deepwater innovation propels premium growth.

Geography Analysis

Asia-Pacific accounted for 47.15% of 2025 revenue, a leadership position anchored by China’s drive for supply security, Southeast Asia’s mature brownfields, and Australia’s emerging USD 60 billion decommissioning opportunity. CNOOC plans to exceed 2 million BOE per day in 2025, backed by RMB 125–135 billion (USD 17.4–18.8 billion) capital expenditure focused on Bozhong 26-6, Kenli 10-2, and Yellowtail. New Chinese rigs, such as Meng Xiang, lift domestic capability and reduce reliance on foreign units, while long-term charters secure drilling capacity for LNG-expansion projects.

South America is the fastest-growing region, projected to grow at a 7.62% CAGR. Petrobras has earmarked USD 111 billion for the 2025–2029 period, with the Búzios 7 and Mero phases requiring extensive subsea, FPSO, and well-construction services. Guyana is expected to reach an output of 800,000 bpd by 2025, creating significant demand for subsea trees, support vessels, and topside modifications. Suriname and Trinidad add exploration upside, sustaining multi-rig campaigns that feed the regional project queue.

North America’s Gulf of Mexico retains a deepwater core of high-productivity assets, benefiting the offshore oilfield services market through steady appraisal wells and brownfield redevelopments. Europe balances the decline in the North Sea with a growing decommissioning backlog that requires plug-and-abandonment expertise. The Middle East and Africa see diversified growth: Qatar, UAE, and Saudi Arabia invest in gas capacity, while Namibia, Angola, and Nigeria court exploration budgets for frontier plays.

Competitive Landscape

The offshore oilfield services market exhibits moderate concentration, as integrated majors such as Schlumberger, Halliburton, and Baker Hughes combine digital platforms with global asset bases to secure outcome-based contracts. Drilling contractors such as Transocean, Valaris, and Noble Corporation differentiate themselves on fleet capability, safety metrics, and execution track record; the latter now commands the largest set of 7G dual-BOP drillships following its acquisition of Diamond Offshore.

Helmerich & Payne’s USD 1.97 billion purchase of KCA Deutag rebalanced its land-rig exposure by adding 88 offshore units and asset-light management contracts in the North Sea and Africa. Consolidation delivers scale, broader geographic reach, and cost synergies in procurement and maintenance. Smaller specialists remain competitive in niches—such as subsea intervention, wellbore cleanup, and FPSO maintenance—where proprietary tools or certifications create high entry barriers.

Technology adoption now sits at the centre of differentiation. AI-based drilling parameter optimisation reduces stuck-pipe incidents, while predictive maintenance slashes unplanned downtime on critical rotating equipment. ESG credentials also influence tender outcomes: contractors that certify lower-carbon rigs, electrify support vessels, or integrate methane-capture kits gain scoring advantages during bid evaluations.

Offshore Oilfield Services Industry Leaders

Transocean LTD

Schlumberger Limited

Baker Hughes Company

Halliburton Company

TechnipFMC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Helmerich & Payne closed its USD 1.97 billion acquisition of KCA Deutag, boosting the Middle East rig count from 12 to 88.

- November 2024: China launched the Meng Xiang deep-ocean drilling vessel, capable of drilling wells up to 11 km in depth. This vessel is China's first domestically designed and built deep-sea drilling ship, designed to explore the Earth's mantle.

- July 2024: KCA Deutag completed its acquisition of Saipem's onshore drilling business, securing six rigs in Argentina, Kazakhstan, and Romania.

- May 2024: Expro Group bought UK-based Coretrax for USD 75 million to expand well-construction and intervention services.

Global Offshore Oilfield Services Market Report Scope

The offshore oilfield services (OFS) market includes services offered to upstream oil and gas operating companies at different stages of an oilfield, such as drilling, completion, production, and intervention services. The services include drilling, completion, production, and intervention, as well as other services such as offshore helicopter services, seismic data acquisition and processing, offshore supply vessels, and decommissioning.

The offshore oilfield services market is segmented by service type and geography(North America, Asia-Pacific, Europe, South America, the Middle East, and Africa). By service type, the market is segmented into drilling services, completion services (cementing services, hydraulic fracturing services, and other completion services), production and intervention services (logging services, production testing, well services, and other production and intervention services), and other services. The report also covers the market size and forecasts for the offshore oilfield services market across the major regions. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

| Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) |

| Production and Intervention Services |

| Other Services (OSV, seismic, decomm., aviation) |

| Shallow Water (Below 400 ft) |

| Deepwater (400 to 5,000 ft) |

| Ultra-deepwater (Above 5,000 ft) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Trinidad and Tobago | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| Angola | |

| Namibia | |

| Rest of Middle East and Africa |

| By Service Type | Drilling Services | |

| Completion Services (Cementing, Hydraulic Fracturing) | ||

| Production and Intervention Services | ||

| Other Services (OSV, seismic, decomm., aviation) | ||

| By Water Depth | Shallow Water (Below 400 ft) | |

| Deepwater (400 to 5,000 ft) | ||

| Ultra-deepwater (Above 5,000 ft) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Trinidad and Tobago | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| Angola | ||

| Namibia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the offshore oilfield services market?

The market is valued at USD 45.46 billion in 2026 and is expected to reach USD 63.13 billion by 2031.

Which service segment leads revenue generation?

Drilling services top the revenue chart with 40.12% share in 2025, reflecting the capital-intensive nature of offshore exploration.

Which region is growing the fastest?

South America is projected to grow at an 7.62% CAGR through 2031, led by Brazil’s pre-salt and Guyana’s new production.

Why are ultra-deepwater projects gaining traction?

Technological breakthroughs in subsea processing and high-specification drillships enable cost-competitive access to reserves deeper than 5,000 ft.

How does digital technology affect offshore service contracts?

Real-time analytics and remote operations reduce non-productive time, prompting operators to shift toward outcome-based integrated service agreements.

What drives consolidation among drilling contractors?

Asset scarcity, the need for balanced global footprints, and the pursuit of cost synergies encourage mergers such as Noble’s purchase of Diamond Offshore and H&P’s acquisition of KCA Deutag.

Page last updated on: