Oil & Gas Engineering Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 62.94 Billion |

| Market Size (2031) | USD 88.47 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil & Gas Engineering Services Market Analysis by Mordor Intelligence

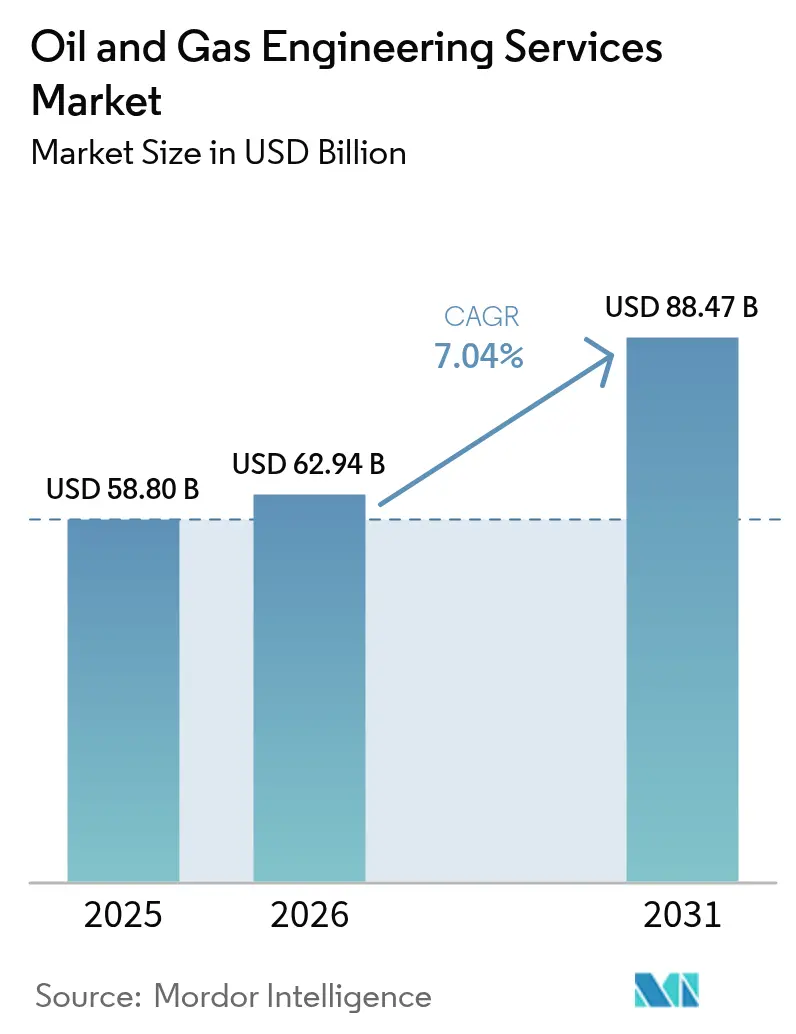

The oil and gas engineering services market size is expected to grow from USD 58.8 billion in 2025 to USD 62.94 billion in 2026 and is forecast to reach USD 88.47 billion by 2031 at 7.04% CAGR over 2026-2031. The broad adoption of digital twins, stricter decarbonization mandates, and relentless cost-optimization programs are accelerating service demand, even as operators navigate volatile commodity cycles. Upstream projects retain the largest slice of spending, yet downstream modernization and integrated petrochemical complexes are pacing the fastest growth as companies pursue higher-value product streams. Digital engineering, ranging from building information modeling to predictive analytics, is reshaping bid criteria, shortening delivery schedules, and lowering lifecycle costs. Regionally, the Asia-Pacific anchors the current demand pool, while the Middle East registers the strongest growth trajectory, driven by mega-projects tied to refining, LNG, and the NEOM industrial program.

Key Report Takeaways

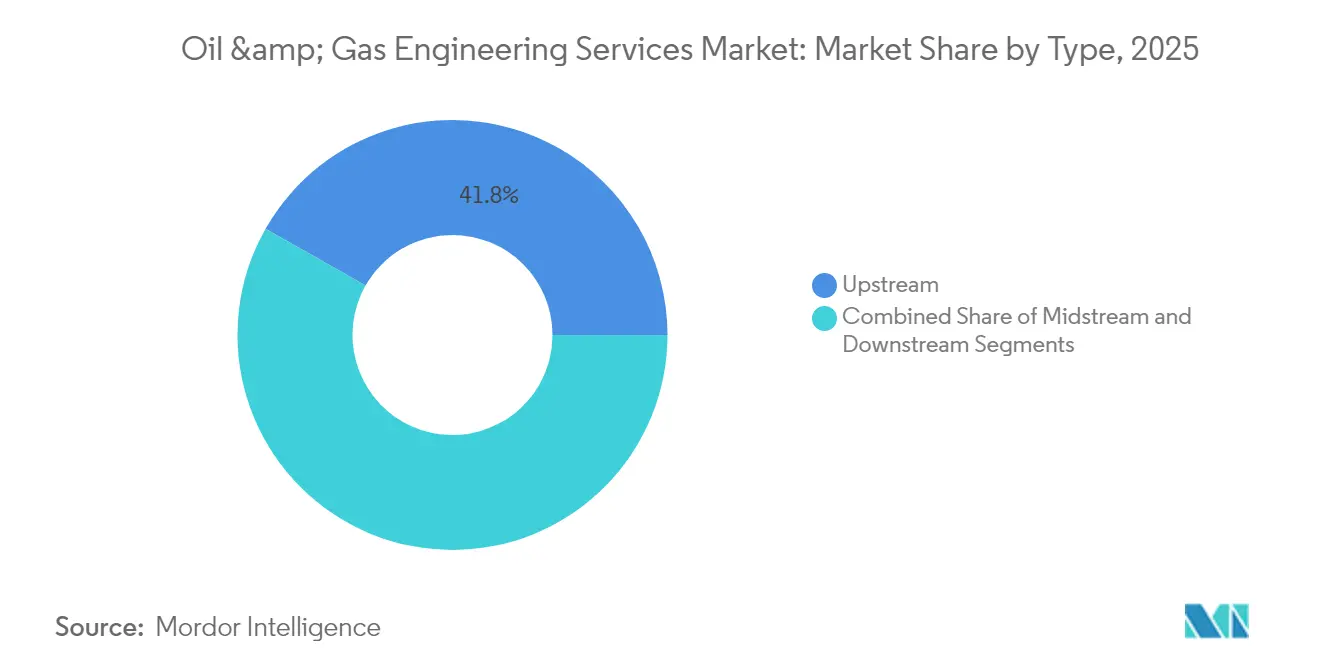

- By type, upstream services captured 41.78% of the oil and gas engineering services market share in 2025, whereas downstream services are projected to expand at an 7.82% CAGR to 2031.

- By service type, detailed engineering and EPCm commanded 30.66% of the oil and gas engineering services market size in 2025, while digital engineering is poised for the fastest 8.46% CAGR through 2031.

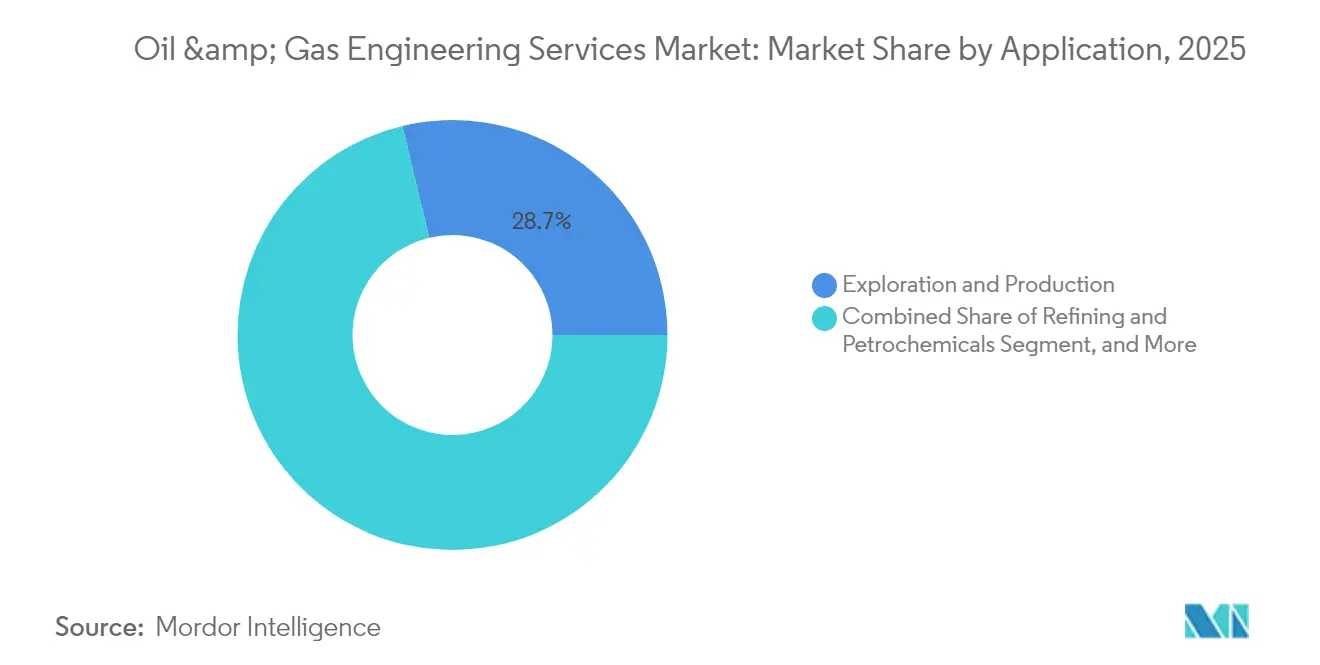

- By application, exploration and production accounted for 28.74% of the oil and gas engineering services market size in 2025; refining and petrochemicals are expected to advance at a 8.91% CAGR through 2031.

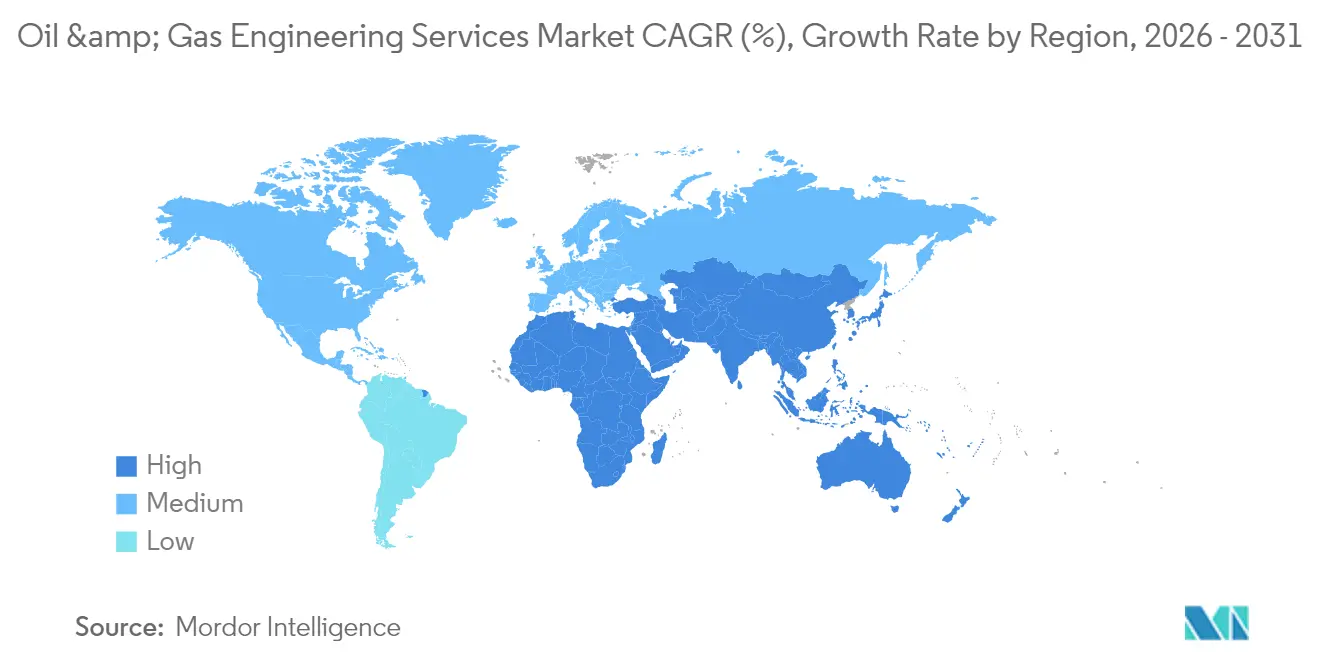

- By geography, Asia-Pacific led with 20.95% revenue share in 2025; the Middle East is forecast to expand at a 8.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oil & Gas Engineering Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing adoption of automation and digital twins | +1.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Industry-wide cost optimisation imperatives | +0.8% | Global | Short term (≤ 2 years) |

| Rising brownfield asset life-extension projects | +1.0% | North America, Europe, mature Asia-Pacific fields | Long term (≥ 4 years) |

| LNG capacity build-out in emerging markets | +1.5% | Africa, the Middle East, Southeast Asia | Medium term (2-4 years) |

| Decarbonisation mandates (CCUS and methane abatement) | +1.8% | Global, spill-over from Europe to the Asia-Pacific | Long term (≥ 4 years) |

| Surge in private upstream investment in Africa | +1.1% | Africa, early gains in Nigeria, Angola, Mozambique | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of automation and digital twins

Shell’s digital twin for its Prelude FLNG facility reduced project execution time by 18% and saved USD 45 million annually in maintenance, demonstrating the business case for real-time data integration. [1]Source: Royal Dutch Shell plc, “Annual Report 2024,” shell.com Asset owners are increasingly specifying digital-twin deliverables at the bidding stage, shifting the service scope toward predictive maintenance and scenario-based optimization. Alignment with API and ISO 55000 standards speeds board approvals and unlocks capital for larger transformation programs. Service providers that have invested in integrated data platforms now win higher-margin outcome-based contracts. This momentum directly feeds into the expanding demand for advanced analytics professionals within the oil and gas engineering services market.

LNG capacity build-out in emerging markets

Africa and Southeast Asia together have more than USD 180 billion in committed LNG projects that require specialized engineering over the next five years.[2]Source: Technip Energies Investor Relations, “Investor Presentation 2024,” technipenergies.com Qatar’s North Field expansion alone has issued over USD 25 billion in engineering contracts covering detailed design, fabrication support, and digital integration. Harsh-environment locations increase per-unit engineering intensity by 40% compared to legacy plants, according to the International Energy Agency.[3]Source: International Energy Agency, “World Energy Outlook 2024,” iea.org Higher complexity translates into premium billing rates, sustaining double-digit growth for LNG-focused service portfolios. The trend anchors robust order backlogs that cushion providers against cyclical dips in upstream spending.

Decarbonisation mandates (CCUS and methane abatement)

Carbon capture projects are projected to generate USD 12 billion in annual engineering expenditures by 2030, creating new revenue streams for multidisciplinary firms.[4]Source: ExxonMobil Corporation, “Form 10-K 2024,” sec.gov European Union methane rules and U.S. EPA standards require retrofits that only seasoned process safety engineers can execute, thereby lifting demand for scarce expertise. Service packages now bundle emissions quantification, technology selection, and permitting support, commanding premium pricing. Operators pay up because daily non-compliance penalties can exceed USD 100,000 for large facilities. Providers with a track record in CO₂ transport and injection infrastructure secure repeat business and strengthen client lock-in across the oil and gas engineering services market.

Industry-wide cost optimisation imperatives

Commodity-price swings drove operators to pursue modular design, lean engineering, and digital collaboration that lower engineering hours by up to 25%. Outcome-based pricing ties fees to realized savings, aligning incentives and reducing change-order disputes. Providers offering standardized equipment catalogs reduce procurement cycles, enabling operators to cut project lead times by four to six months. Competitive tendering now favors firms able to guarantee double-digit cost reductions without compromising safety. As a result, cost-optimization capability has become a core differentiator within the oil and gas engineering services market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Crude-price cyclicality and capex pull-backs | -0.9% | Global | Short term (≤ 2 years) |

| Skilled-labour shortages in specialised disciplines | -0.7% | North America, Europe, Australia | Medium term (2-4 years) |

| Escalating ESG-driven compliance costs | -0.5% | Global, early impact in Europe and North America | Long term (≥ 4 years) |

| Cybersecurity and IP-theft concerns in remote delivery | -0.4% | Global, affecting cross-border projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-price cyclicality and cap-ex pull-backs

Oil prices oscillating between USD 70 and USD 95 per barrel in 2024 forced multiple project deferrals, slicing ConocoPhillips’ capital budget by USD 1.2 billion and shrinking associated engineering awards by 15%. Operators now stipulate flexible scope clauses that shift risk onto contractors. Firms heavily exposed to mega-projects face lumpy cash flows and must maintain idle capacity during downturns. Smaller, regionally diversified workloads help mitigate revenue volatility; however, balance-sheet resilience remains critical for weathering short-cycle pullbacks within the oil and gas engineering services market.

Skilled-labour shortages in specialised disciplines

Vacancy rates exceed 25% for process-safety, subsea, and digital-integration engineers, inflating subcontractor premiums by 35% at Wood Group in 2024. Aging workforces in North America and Europe exacerbate the gap as seasoned experts retire faster than universities can replenish their talent. Competition from renewables adds wage pressure and lengthens hiring cycles. Providers invest in apprenticeship pipelines, but the requisite four- to seven-year skill curve prolongs capacity constraints. Persistent scarcity threatens project timelines and can cap annual revenue growth for the oil and gas engineering services industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Upstream Dominance Drives Market Foundation

Upstream services held a 41.78% market share of the oil and gas engineering services market in 2025, underscoring the capital-intensive nature of deep-water exploration, unconventional resource development, and enhanced recovery programs. Continuous reservoir appraisal and complex well architectures demand integrated subsurface and surface engineering that few competitors can execute at scale. Upstream workloads also include digital field life-cycle modeling, which informs production optimization and extends contract duration across the development horizon.

The downstream arena, although smaller, is growing faster at 7.82% CAGR as refiners modernize and integrate petrochemicals to maximize margins. Saudi Aramco’s USD 20 billion Jazan complex exemplifies the high-value projects driving downstream momentum. Stricter environmental rules raise technology requirements for sulfur removal, flare reduction, and energy efficiency, boosting consulting and execution revenues. Midstream, anchored by LNG facilities and pipelines, captures roughly 27.65%, providing steady income from long-dated infrastructure programs. Together, these dynamics reinforce a balanced opportunity set across the oil and gas engineering services market.

By Service Type: Digital Engineering Accelerates Traditional Services

Detailed engineering and EPCm accounted for 30.66% of the oil and gas engineering services market size in 2025, reflecting their indispensability for end-to-end project execution. The scope encompasses 3D modeling, procurement support, construction supervision, and commissioning. Clients prize vendors that can compress schedules without quality tradeoffs, sustaining healthy margins despite competitive tendering.

Digital engineering, though a smaller base, is expanding at an 8.46% CAGR. Worley’s deployment of digital twins across 150 projects cut engineering hours by 20% and boosted construction productivity by 15%. These gains, combined with richer life-cycle insights, position digital deliverables as table stakes in upcoming bids.

By Application: Refining and Petrochemicals Drive Growth Acceleration

Exploration and production projects accounted for 28.74% of the oil and gas engineering services market size in 2025, encompassing reservoir characterization, well design, and the development of production facilities. High-pressure, high-temperature wells and deep-water tie-backs prolong service involvement across decades, ensuring durable revenue streams. LNG and gas processing capture a significant share, driven by energy security and preferences for lower-carbon fuels.

Refining and petrochemicals, however, chart the fastest path at 8.91% CAGR to 2031, supported by China’s 1.6 million barrels-per-day capacity additions and India’s multi-billion-dollar petrochemical self-sufficiency push. Complex feedstock slats and circular-economy imperatives create specialized engineering needs in catalytic cracking, aromatics production, and polymer recycling. Meanwhile, pipeline and storage applications round out the mix by enabling crude evacuation and strategic reserve builds, particularly in emerging economies.

Geography Analysis

The Asia-Pacific region led with 20.95% of global revenue in 2025, driven by massive investments in refining, petrochemicals, and LNG, exceeding USD 150 billion through 2030. China’s carbon-neutrality pledge stimulates CCUS engineering demand, while India’s downstream build-out drives the design of complex process units.

North America contributed a significant share in 2025. Shale optimization, LNG export terminals, and refinery upgrades, each of which focuses on energy efficiency, remain key drivers. EPA methane rules sharpen demand for emissions-control engineering, and the Permian Basin sustains sizeable brown-field enhancement programs. Canada’s oil sands drive carbon-intensity reduction projects that require novel solvent-based extraction methods.

The Middle East and Africa jointly register the sharpest expansion at 8.74% CAGR. Saudi Arabia’s NEOM initiative, ADNOC’s Ruwais expansion, and Qatar’s LNG megaprojects form a multi-year workload pipeline surpassing USD 200 billion. Africa’s Coral Sul FLNG and Nigerian deep-water fields open premium opportunities for remote-environment specialists. Europe sustains stable demand through decarbonization retrofits, North Sea field life extension, and renewable integration projects under the European Green Deal framework.

Competitive Landscape

The top five players together hold a significant share of the oil and gas engineering services market, among regionally focused firms and digital specialists. Consolidation continues as incumbents acquire niche digital or sustainability assets to deepen value propositions. Wood Group’s 2025 acquisition of Cognite for USD 850 million enhanced its AI and digital-twin portfolio, while Worley’s diversification into renewable engineering broadened its energy-transition revenue mix.

Competitive advantage increasingly stems from proprietary data platforms, emissions-reduction expertise, and outcome-based pricing. Technip Energies leverages a deep LNG reference list to secure USD 3.2 billion for Saudi Aramco’s Jafurah project, illustrating the impact of domain credibility on mega-project awards. Fluor’s integrated EPC management on ExxonMobil’s Baytown modernization highlights the premium attached to compliance-driven refinery upgrades.

Emerging challengers utilize cloud collaboration, AI-guided design, and modular work-sharing to execute projects with lower overhead, capturing a share in cost-sensitive bids. In response, legacy giants upgrade their cybersecurity, invest in remote delivery centers, and pilot no-code automation for repetitive design tasks. Specialists offering CCUS, methane abatement, and bio-refinery conversions unlock high-margin niches. Overall, the oil and gas engineering services market balances scale efficiencies with agile innovation, rewarding firms that master both dimensions.

Oil & Gas Engineering Services Industry Leaders

Wood Group PLC

Worley Limited

Technip Energies N.V.

Fluor Corporation

Saipem S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Technip Energies obtained a USD 3.2 billion EPC contract for Saudi Aramco’s Jafurah gas-processing facilities.

- August 2025: Wood Group purchased digital-engineering firm Cognite for USD 850 million to bolster AI and digital-twin offerings.

- July 2025: Worley completed a USD 1.8 billion engineering and design mandate on Chevron’s Tengiz expansion in Kazakhstan.

- June 2025: Fluor secured a USD 2.1 billion integrated engineering and construction management contract for ExxonMobil’s Baytown refinery modernization.

Global Oil & Gas Engineering Services Market Report Scope

| Upstream |

| Midstream |

| Downstream |

| Design and Front-End Engineering |

| Detailed Engineering and EPCm |

| Asset Integrity and Maintenance |

| Digital Engineering (BIM, XR, Analytics) |

| Consulting and Advisory |

| Exploration and Production |

| Refining and Petrochemicals |

| LNG and Gas Processing |

| Pipeline and Storage |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Upstream | ||

| Midstream | |||

| Downstream | |||

| By Service Type | Design and Front-End Engineering | ||

| Detailed Engineering and EPCm | |||

| Asset Integrity and Maintenance | |||

| Digital Engineering (BIM, XR, Analytics) | |||

| Consulting and Advisory | |||

| By Application | Exploration and Production | ||

| Refining and Petrochemicals | |||

| LNG and Gas Processing | |||

| Pipeline and Storage | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the oil and gas engineering services market?

The oil and gas engineering services market size is USD 62.94 billion in 2026.

How fast is spending on engineering services expected to grow over the next five years?

Aggregate spending is projected to rise at a 7.04% CAGR, taking the market to USD 88.47 billion by 2031.

Which segment is expanding the quickest?

The downstream segment leads growth with an 7.82% CAGR, driven by refinery modernization and petrochemical integration.

Why are digital twins important for engineering services?

Digital twins cut project execution time up to 18%, slash maintenance costs, and enable predictive asset management.

Which region exhibits the strongest growth momentum?

The Middle East shows the highest forecast CAGR at 8.74% through 2031 due to large gas, LNG, and industrial mega-projects.

Page last updated on: