Photochromic Lenses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

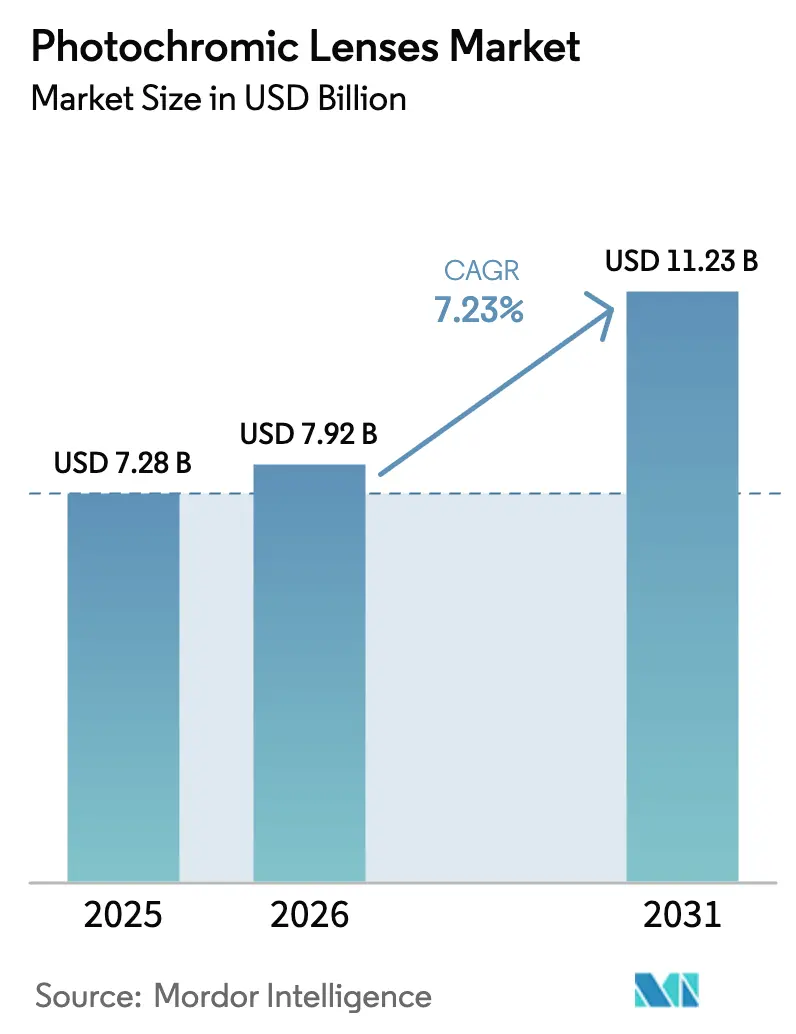

| Market Size (2026) | USD 7.92 Billion |

| Market Size (2031) | USD 11.23 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photochromic Lenses Market Analysis by Mordor Intelligence

The Photochromic Lenses Market size was valued at USD 7.28 billion in 2025 and is estimated to grow from USD 7.92 billion in 2026 to reach USD 11.23 billion by 2031, at a CAGR of 7.23% during the forecast period (2026-2031).

The growth is propelled by an aging global population that needs presbyopia correction, rising myopia prevalence in children, and the integration of adaptive-tint technology into emerging smart-glasses platforms. Plastic substrates retain the largest slice of revenue, though polycarbonate is expanding quickly on the back of its impact resistance. UV- and visible-light–activated technologies dominate current sales, yet in-mass and electronically controlled tint systems are carving out premium niches. Strong retail and e-commerce penetration, coupled with material innovation and bio-based chemistries, is widening the addressable base for the photochromic lenses market.[1]Mitsubishi Gas Chemical, “IURESIN and Episleaf Lens Monomers,” Mitsubishi Gas Chemical, mgc.co.jp

Key Report Takeaways

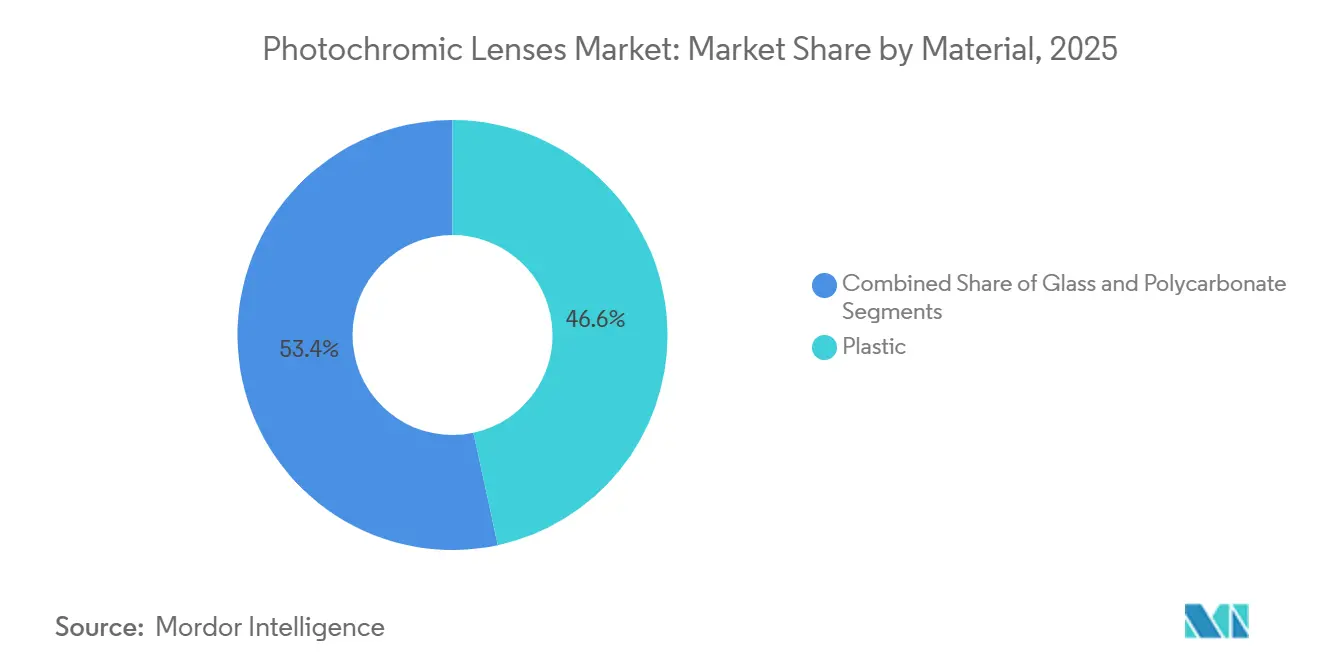

- By material, plastic lenses led with 46.62% of photochromic lenses market share in 2025. Polycarbonate substrates are projected to expand at a 10.63% CAGR through 2031, the fastest rate among materials.

- By technology, UV & visible-light-activated systems accounted for 61.57% of revenue in 2025. In-mass processes will post the highest technology-level CAGR at 8.84% through 2031.

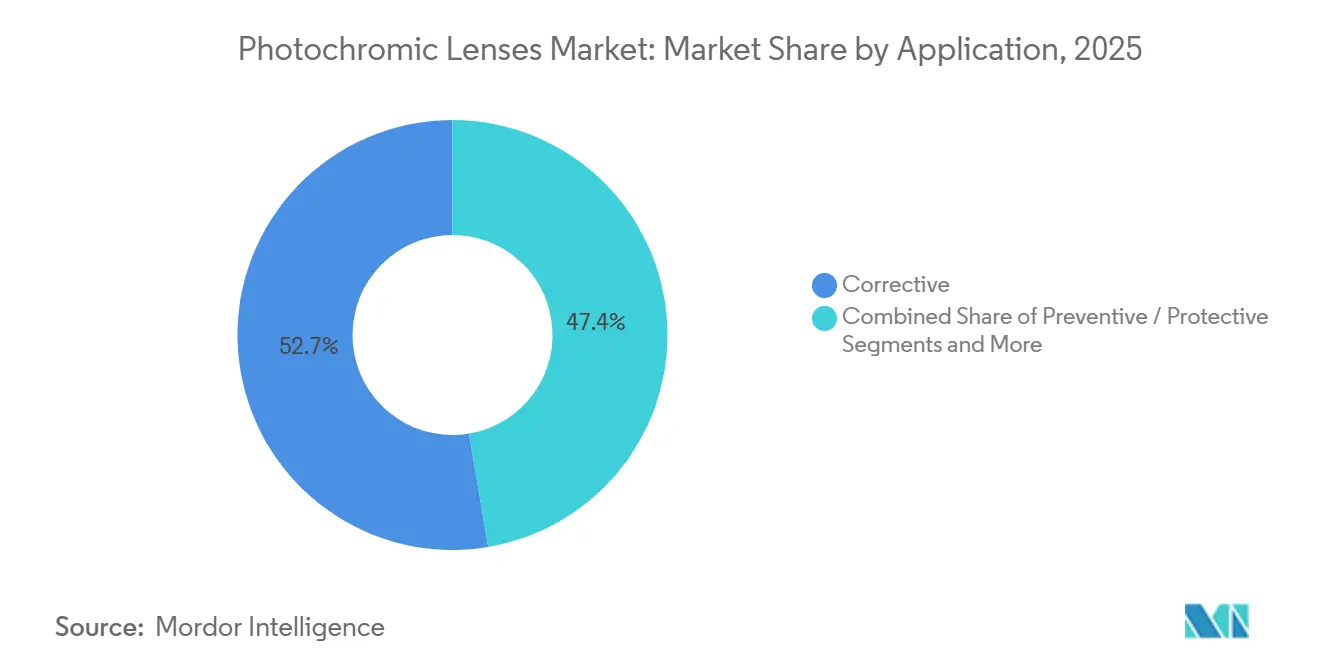

- Corrective prescription lenses held 52.65% of value in 2025; smart wearables are set to grow at 11.34% CAGR to 2031. Adults generated 47.73% of end-user demand in 2025, while children and teens represent the fastest-growing cohort at 10.02% CAGR.

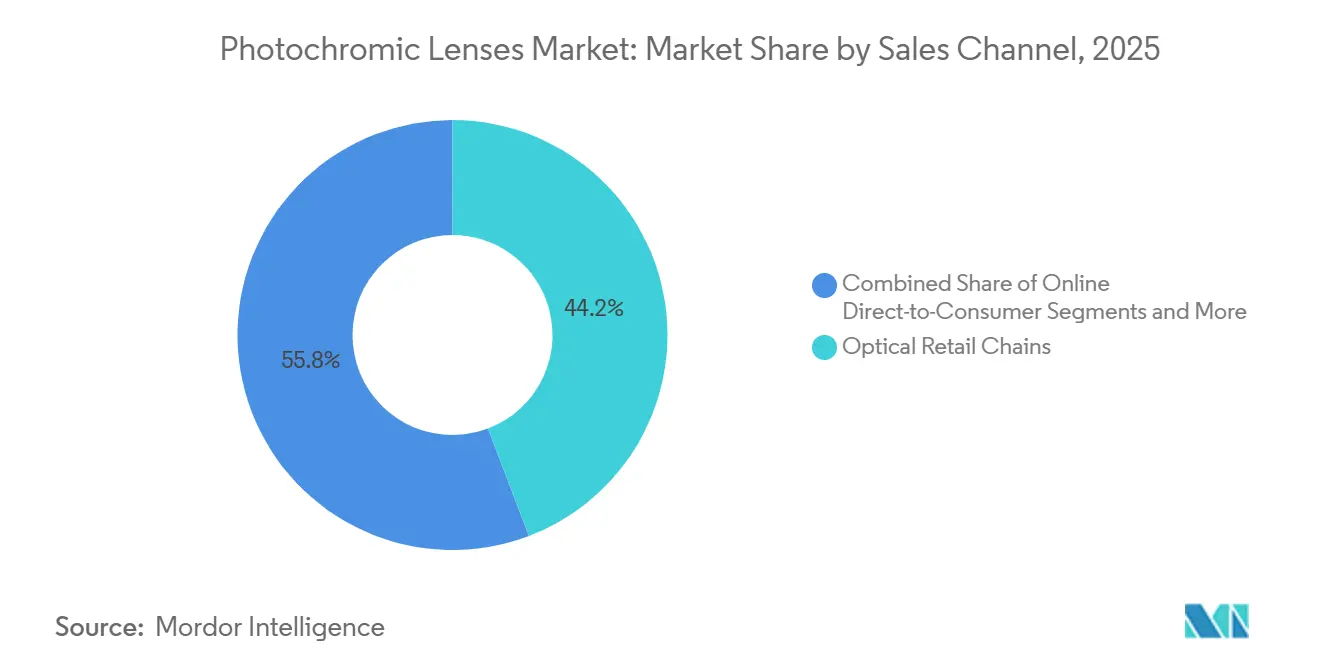

- Optical retail chains captured 44.22% of 2025 sales; online direct-to-consumer channels will advance at 11.77% CAGR through 2031.

- North America commanded 33.24% of 2025 revenue; Asia-Pacific will record the strongest regional CAGR at 10.29% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Photochromic Lenses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision disorders and an aging population | +1.2% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Multipurpose eyewear demand | +0.9% | North America, Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| E-commerce penetration of premium coatings | +0.7% | Global core markets | Medium term (2-4 years) |

| Faster activation and color clarity | +0.6% | North America, Europe | Short term (≤ 2 years) |

| AR smart-glasses integration | +0.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Bio-based eco-friendly dye development | +0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Vision Disorders and an Aging Population

More than 2.2 billion people live with visual impairment, and presbyopia affects 1.8 billion individuals worldwide.[2]World Health Organization, “Blindness and Vision Impairment,” WHO, who.int Photochromic lenses let older and presbyopic consumers combine vision correction and UV protection in one pair of glasses, which streamlines daily use. Rising myopia in children adds urgency, with prevalence already at 35% in 2023 and forecast to hit 40% by 2050. Aging markets in Japan and Italy, as well as rapidly urbanizing regions in China and India, therefore constitute strong demand pools. Manufacturers that align product lines with these demographic realities secure a durable growth runway.

Multipurpose Eyewear Demand (Prescription + Sun)

Consumers dislike switching between clear lenses and sunglasses during indoor-outdoor transitions. Modern photochromic products darken in under 30 seconds and clear within 2 minutes, delivering a seamless experience. Transitions Optical’s GEN S and ZEISS PhotoFusion X set the performance benchmark with 25-second activation and 80% faster fade-back compared with prior models. High convenience resonates in North America and Europe, where per-capita eyewear spend tops USD 150, yet demand is spreading into urban Asia-Pacific populations as disposable income climbs. Retailers are bundling adaptive-tint coatings into mid-tier packages, which accelerates uptake by positioning photochromic functionality as standard rather than luxury.

Retail and E-Commerce Penetration of Premium Coatings

Warby Parker posted USD 192.2 million in Q3 2024 revenue, up 13.3% year over year, with 2.42 million active customers using virtual try-on tools. Lenskart completed 13 million eye tests in fiscal 2025, embedding photochromic options in its omnichannel configurator. Such direct-to-consumer models trim distribution costs and narrow the price gap with clear lenses. Traditional outlets have responded by upgrading in-store demos and adopting price-match policies. The ability to personalize offers based on exposure and lifestyle data further heightens conversion rates.

Faster Activation and Color-Clarity Innovations

HOYA’s Sensity 2 doubles fade-back speed, and ZEISS PhotoFusion X curbs residual tint in cold climates. Chamelo’s Aura Rx achieves 0.1-second electronic tint change, although costs remain high. Performance improvements make adaptive-tint lenses attractive for driving and sports, where instant visual adaptation boosts safety. Color neutrality also appeals to fashion-driven buyers who want photochromic benefits without tint-shift trade-offs indoors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing over conventional lenses | -0.8% | Price-sensitive Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Counterfeit and low-quality circulation | -0.6% | Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Temperature-dependent performance limits | -0.4% | Extreme-climate geographies | Long term (≥ 4 years) |

| Regulatory scrutiny on dye chemicals | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Over Conventional Lenses

Photochromic products still cost 40-60% more than clear lenses in many emerging markets. Despite aggressive bundling, India’s penetration remains below 15% of lens sales. Retailers employ financing plans and tiered offerings to lessen sticker shock, yet the luxury perception persists and slows adoption in middle-income economies.

Counterfeit and Low-Quality Product Circulation

Safilo introduced holographic labels and blockchain authentication to combat counterfeit lenses that fail to meet ISO 8980-3 standards. Low-quality knock-offs degrade quickly, foster distrust, and suppress pricing power for authentic manufacturers. The threat is acute in markets with weaker intellectual-property enforcement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polycarbonate Gains on Impact Resistance

Plastic lenses captured 46.62% of 2025 value, yet the segment is gradually tilting toward polycarbonate because families and athletes value durability. Polycarbonate is forecast to post a 10.63% CAGR, the highest within the materials hierarchy, while retaining optical quality that meets ISO 8980-3 baselines. Mitsubishi Gas Chemical’s IURESIN plant scheduled for 2026 will introduce an ultra-high-index polycarbonate (n = 1.74), enabling thinner, lighter forms that appeal to rimless-frame enthusiasts. Trivex and other mid-index plastics are also gaining ground for ballistic and pediatric use. Meanwhile, glass lenses have fallen to single-digit share due to weight and breakage concerns, remaining mainly in luxury niches.

Mitsui Chemicals’ planned MR monomer facility for 2028 underscores the importance of continued material innovation and signals the next leap in premium-tier differentiation. CR-39 will stay relevant at the budget end, but migration toward impact-resistant and high-index options will gradually trim its share. Regulatory standards guarantee base-line transmittance performance regardless of substrate, but buyers increasingly favor the lighter weight and resilience of polycarbonate.

By Technology: UV Activation Dominates, In-Mass on the Rise

UV- and visible-light-activated coatings held 61.57% of 2025 revenue, thanks to compatibility with existing production lines and broad substrate applicability. Trans-bonding remains common, yet in-mass embedding—where dyes are mixed directly into monomers—grows rapidly for premium lines because of superior scratch resistance and color stability. Luxexcel’s additive manufacturing uses in-mass dyes to produce complex prescription lenses for AR waveguides, sidestepping traditional coating steps.

Electronic systems such as Chamelo’s liquid-crystal lenses record 0.1-second transitions but remain pricey and require power sources. Over the forecast horizon, UV-activated technology will keep the lion’s share due to cost efficiency, though in-mass and electronic variations will capture incremental high-margin demand.

By Application: Smart Wearables Surge Ahead

Corrective prescriptions represented 52.65% of 2025 revenue, anchoring the core demand. Yet smart wearables, including AR-ready frames, will climb at 11.34% CAGR as tech brands like Meta and Apple commercialize lighter, more affordable headsets. Preventive non-prescription sunglasses grow slower because an increasing share of buyers opts for dual-purpose corrective lenses.

Young tech-savvy users drive smart-wearable adoption, while presbyopic adults dominate corrective sales. The overlap between photochromic functionality and outdoor AR display readability presents a compelling value proposition that is expected to push smart-wearable penetration into double digits by 2031.

By End User: Children and Teens Accelerate

Adults contributed 47.73% of 2025 demand, but the children and teens group, bolstered by escalating myopia rates, will register a 10.02% CAGR. Pediatric product designs incorporate impact-resistant substrates and tougher coatings, and retailers often offer favorable pricing or financing to parents eager for dual-function lenses. Elderly users still rely heavily on clear lenses, yet awareness campaigns on UV-related eye damage are nudging them toward premium adaptive-tint alternatives.

By Sales Channel: Online Platforms Outpace Retail

Optical retail chains made up 44.22% of 2025 sales, but direct-to-consumer websites will grow at 11.77% CAGR through 2031. Warby Parker’s and Lenskart’s embrace of home eye tests and virtual try-ons slashes friction and showcases tint simulations in real time. Brick-and-mortar outlets respond with omnichannel strategies, while OEM bundling of prescription photochromic lenses into smart-glasses adds an additional distribution path.

Geography Analysis

North America accounted for 33.24% of 2025 revenue, backed by USD 150-plus annual per-capita eyewear spending and strong optometrist networks. The FDA’s device labeling standards reinforce consumer confidence, and direct-to-consumer leaders such as Warby Parker add momentum.[3]U.S. Food and Drug Administration, “21 CFR Part 801,” FDA, fda.govAlthough growth moderates because penetration is high, ongoing smart-wearable launches sustain a healthy pipeline.

Asia-Pacific will log the fastest 10.29% CAGR. India’s eyewear market is on track to expand from USD 9.2 billion in fiscal 2025 to USD 17.2 billion by fiscal 2030, while China’s expanding middle class buys photochromic lenses for smog and UV protection. Japan and South Korea, already premium markets, lead adoption of advanced dye blends, and Southeast Asia is catching up as e-commerce solves distribution gaps.

Europe remains a hub for high-end developments. Germany, France, and the United Kingdom maintain stringent REACH and ISO compliance, which raise entry barriers but guarantee quality. ZEISS and Rodenstock dominate innovation pipelines with fast-acting, temperature-stable products. Middle East & Africa and South America lag in penetration due to pricing sensitivities, yet rising disposable incomes and extreme UV exposure in regions such as the GCC open white-space opportunities.

Regulatory Landscape

Photochromic spectacle lenses fall under medical-device and product-safety frameworks that influence labeling, traceability, and quality-system requirements across major markets. In the United States, the FDA classifies prescription spectacle lenses under 21 CFR 886.5844 as Class I devices, generally exempt from 510(k) while still subject to applicable GMP and labeling requirements under 21 CFR Part 801.

In Europe, compliance is governed by the EU Medical Device Regulation (MDR) 2017/745 and associated guidance, with extra operational implications for highly individualized devices such as prescription lenses. Commission Delegated Regulation (EU) 2025/1920 introduced a Master UDI-DI assignment solution for spectacle lenses to help manage UDI and Eudamed registration at scale, while ISO also updated core lens requirements through ISO 14889:2025 (approved in April 2025 and published in national adoptions such as NBN EN ISO 14889:2025 in June 2025). On the US quality side, the FDA issued technical amendments to the Quality Management System Regulation in December 2025, with key changes effective February 2, 2026, requiring manufacturers to keep global QMS alignment tight across sites and suppliers.

Value Chain Analysis

The value chain for photochromic lenses begins with specialty chemical inputs, including photochromic dyes, stabilizers, and lens polymers/monomers used in plastic and polycarbonate substrates, and then moves into lens forming and photochromic activation steps. Core manufacturing routes include in-mass (bulk) tinting, where dyes are blended into monomers, imbibition, where dyes diffuse into a finished lens surface under heat, and film or resin-layer approaches applied to pre-formed substrates. Quality control runs throughout because thickness-driven tint non-uniformity (for example, the bull-eye effect in prescriptions), high-purity dye synthesis, and batch-to-batch consistency across coating, curing, and finishing all affect end performance.

Downstream, branded lens technology providers and lens manufacturers integrate proprietary photochromic platforms into multiple designs and materials, then distribute through optical labs, distributors, and retailers, supported by digital tools that simulate tint behavior at point of sale. Integrated players such as EssilorLuxottica (including Transitions Optical), ZEISS, HOYA, and Rodenstock combine material science, manufacturing, and commercialization, while OEM and laboratory partners support private-label and rapid-turnaround supply. The sales chain ends with optical retail chains, optometrists and clinics, and online direct-to-consumer channels, where fit, coating selection, and verification against performance and standards requirements shape conversion and returns.

Competitive Landscape

Top Companies in Photochromic Lenses Market

EssilorLuxottica, Hoya, and Transitions Optical anchor the competitive map with vertically integrated supply chains and proprietary dye platforms. EssilorLuxottica’s alliance with Meta positions the group at the forefront of smart-glasses convergence. Hoya and ZEISS compete on activation speeds and temperature stability, offering differentiated premium value.

Mid-tier firms—Rodenstock, Seiko, Shamir, and Tokai—capitalize on regional strengths and niche products, such as high-index plastics and myopia-control optics. Luxexcel is a wild-card disruptor, 3D-printing lenses for AR devices and eliminating coating steps. Emerging challengers like Chamelo pursue electronically controlled tints for fashion and wearable tech, even though pricing remains a hurdle. Compliance with evolving regulations is a significant differentiator: firms with robust quality systems avoid costly recalls and can serve tightly regulated markets first.

Photochromic Lenses Industry Leaders

Corning Incorporated

Carl Zeiss AG

Hoya Corporation

EssilorLuxottica SA

Rodenstock GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One key whitespace opportunity is reducing the trial gap between a lens demo and real-world indoor-outdoor performance, especially for premium photochromics where pricing can deter consumers. HOYA's January 2026 launch of HOYA LensPreview (within the HOYA Hub ecosystem) highlights how virtual try-on and visualization tools can be embedded into the purchase workflow to make tint, reflectance, and lens-option differences more tangible for patients across retail and omnichannel settings. This supports manufacturers and retailers in standardizing photochromic education, bundling coatings more effectively, and lowering remake risk through clearer pre-purchase expectation-setting.

Product-side differentiation also remains tied to durability of activation over time, color stability, and fade-back speed across temperature conditions, which map directly to recurring user objections. In April 2026, HOYA introduced Sensity 3, emphasizing longer activation life and improved color stability, while Rodenstock introduced ColorMatic X and ColorMatic Dark in January 2026, with emphasis on performance across varying temperatures. These releases create sharper opportunities in heat- and cold-exposure geographies, in premium positioning for all-day wear, and in fashion-forward segments where expressive tint options (including newer colored photochromics) help compete against conventional sunwear and polarized alternatives.

Recent Industry Developments

- April 2026: HOYA Vision Care launched Sensity 3, its third-generation light-adaptive lens family, highlighting longer activation life and improved color stability along with faster fade-back versus prior generations. The release strengthens HOYA's premium photochromic lineup and raises the performance baseline for competing UV and visible-light activated products.

- February 2026: EssilorLuxottica introduced Transitions Color Touch, expanding photochromic lenses toward more expressive, everyday tint aesthetics. The move targets fashion-driven demand and gives retailers another premium upsell pathway beyond conventional grey and brown photochromics.

- April 2025: HOYA Vision Care launched Sensity Colours, adding six fashion-oriented color options for light-adaptive lenses in time for summer selling. Broadening the palette supports differentiation at retail and helps position photochromics as lifestyle eyewear rather than a purely functional add-on.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market includes revenue generated from photochromic ophthalmic lenses that change tint with light exposure, covering prescription and non-prescription use across major materials and activation technologies. The sizing reflects lenses sold through optical clinics, retail chains, online channels, and OEM supply across the covered geographies.

Scope exclusions: It excludes contact lenses, frames, and lens care solutions, and it also excludes conventional clear or tinted lenses that do not have photochromic behavior.

Segmentation Overview

- By Material

- Glass

- Polycarbonate

- Plastic

- CR-39 (Standard Resin)

- Trivex

- High-Index Plastics

- By Technology

- UV & Visible-Light Activated

- Imbibing & Trans-bonding

- In-Mass (Bulk)

- Other Emerging Technologies

- By Application

- Corrective (Prescription)

- Preventive / Protective (Non-Rx, Sunglass Replacement)

- Smart Wearables & Connected Eyewear

- By End User

- Adults

- Children & Teens

- Elderly (65+)

- By Sales Channel

- Specialty Clinics & Optometrists

- Optical Retail Chains

- Online Direct-to-Consumer

- OEM Partnerships (Smart-glasses Makers)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public demand and supply indicators that can be checked repeatedly across years, and then narrowed them to the photochromic lens use case. Sources used included, for example, US CDC vision health statistics, WHO vision impairment facts, US FDA and similar regulator guidance on eyewear materials, and trade data from UN Comtrade for optical lens and eyewear related categories.

To make the model realistic in pricing and channel behavior, we also reviewed company annual reports, investor presentations, and public releases from optical associations and clinical bodies, along with reputable press coverage on eyewear retail and lens technology changes. A paid subscription for company financials and intelligence, plus patent databases, helped map active manufacturing footprints and technology direction, rather than relying only on marketing claims. These desk research sources are illustrative, and we also used other public and paid inputs to cross-check, validate, and clarify the data.

Primary Interviews and Surveys

Primary work was used to stress-test the desk assumptions on adoption, pricing, and channel mix for photochromic lenses, since these factors shift by region and by customer profile. We spoke with respondents across lens manufacturing, optical retail, eye care practices, and distribution, and then rechecked inputs across APAC, EMEA, and the Americas to keep the demand pool and ASP logic consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 21% | APAC: 41% |

| Mid tier: 47% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 21% | Managers: 40% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing was built using top-down demand reconstruction, where vision-correction and eyewear use indicators were translated into an addressable lens pool and then filtered to photochromic penetration by channel and region. Once the demand pool was formed, it was converted to value using region-level average selling price ranges that were validated in interviews and adjusted for material mix.

To keep the totals realistic, we corroborated the results with selective bottom-up checks, such as sampled lens volumes by channel, supplier capacity signals, and channel mark-up patterns, which we used to adjust outliers. Key model inputs included prescription eyewear usage, aging population share, UV exposure awareness and outdoor lifestyle cues, photochromic upgrade rates within corrective lenses, and ASP movement by material (plastic, polycarbonate, glass) and coating complexity. When gaps appeared in smaller countries or online-led markets, we applied proxy ratios from comparable markets and then revalidated with local respondents.

For forecasting, we used scenario analysis supported by a light multivariate regression layer, where variables like eyewear volume growth, premiumization rate, and channel shift toward organized retail and online were projected and then translated into photochromic adoption and pricing paths. Expert feedback was used to set realistic ranges for penetration change and to avoid extending short-term trends into the outer years.

Data Validation & Update Cycle

Outputs were validated through a set of consistency checks, where market totals were compared with independent signals like eyewear volumes, trade direction, and reported capacity expansions, and then reviewed for currency and inflation impacts. Variances that looked high were traced back to the exact driver, such as penetration, ASP, or channel mix, and the assumptions were revisited before sign-off.

A second analyst review is completed to ensure definitions, math, and logic align across regions, followed by targeted re-contacts when a key assumption moves outside the expected range. The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, sharp pricing moves in lens materials, or step-changes in channel structure. Before delivery, a fresh review pass is done so clients receive the latest updated view.

Mordor Intelligence's Photochromic Lenses Market Size Versus Other Published Estimates

Published market values for photochromic lenses can look different across sources because the product boundary, the included channels, and the way pricing is averaged are not the same. Differences also show up when one study uses older base-year pricing, or when regional weights are assumed rather than validated with people who sell and prescribe lenses.

Frames and non-photochromic spectacle lenses sit outside Mordor Intelligence's scope, which narrows the revenue pool and prevents adjacent eyewear value from inflating the total. The spread against other figures also comes from how fast ASPs are assumed to rise, whether online and OEM channels are fully counted, and whether the forecast path is a base case or a more aggressive scenario built on faster penetration gains.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.28 B (2025) | |

| Global Consultancy A | USD 8.21 B (2025) | Uses a broader included revenue pool in practice by blending more preventive eyewear spend into the lens total in some regions, and it also applies higher near-term penetration gains with fewer channel-level checks on ASP ranges. |

| Industry Publisher B | USD 6.98 B (2025) | Leans more on generalized eyewear growth and earlier-year price points, which can understate premium photochromic mix and the realized ASP uplift seen in organized retail and clinic channels. |

The table highlights that most gaps are explained by what gets counted as lens-only revenue, plus the ASP and penetration assumptions behind each forecast. When scope stays tight to photochromic lenses and inputs are tied back to observable demand signals and channel realities, the resulting number is easier to trace and repeat year after year.

Key Questions Answered in the Report

How large will the photochromic lenses market be in 2031?

It is projected to reach USD 11.23 billion by 2031, growing at a 7.23% CAGR from 2026 to 2031.

Which region shows the fastest growth for photochromic lenses?

Asia-Pacific is forecast to expand at a 10.29% CAGR, driven by rising middle-class demand in China and India.

Why are polycarbonate photochromic lenses gaining popularity?

Their high impact resistance suits children’s and sports eyewear, leading to a 10.63% CAGR through 2031.

What is the main technology used in photochromic lenses today?

UV- and visible-light-activated coatings dominate, holding about 61.57% of 2025 revenue.

Which sales channel is expanding most rapidly?

Online direct-to-consumer platforms are expected to grow at 11.77% CAGR because virtual try-on and home eye tests cut purchase friction.

How are smart glasses influencing demand?

Integration of photochromic optics into devices such as Meta Ray-Ban frames is driving an 11.34% CAGR in the smart-wearables segment.

Page last updated on: