Assistive Technologies For Visually Impaired Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

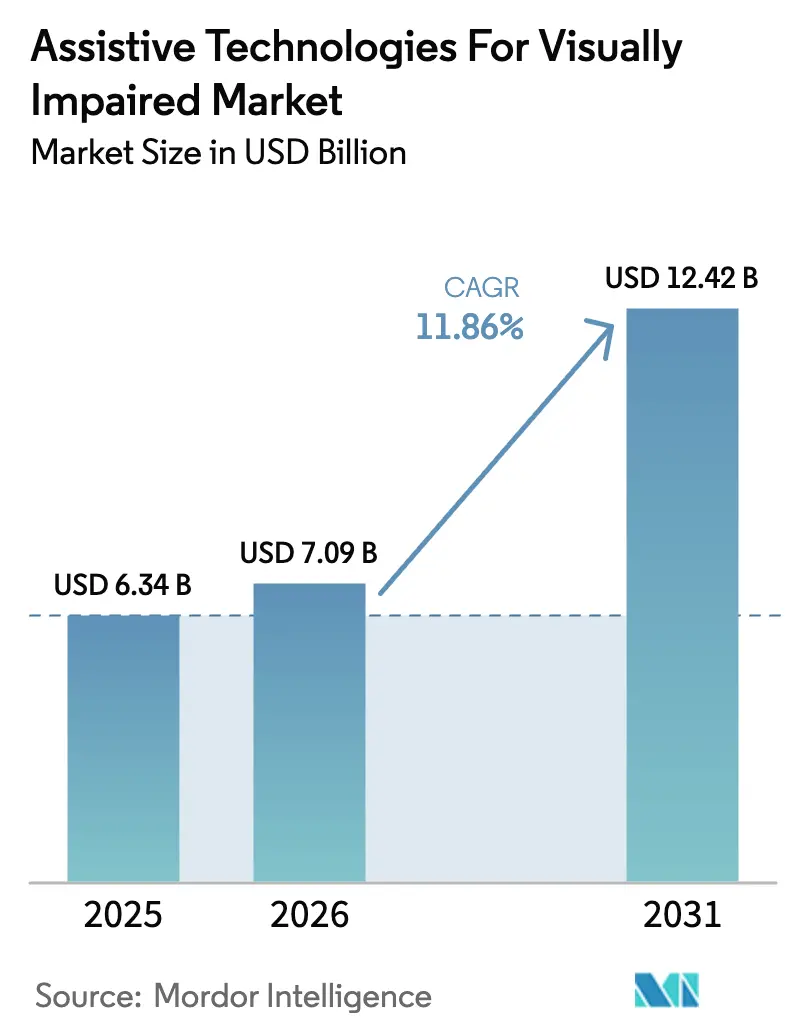

| Market Size (2026) | USD 7.09 Billion |

| Market Size (2031) | USD 12.42 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

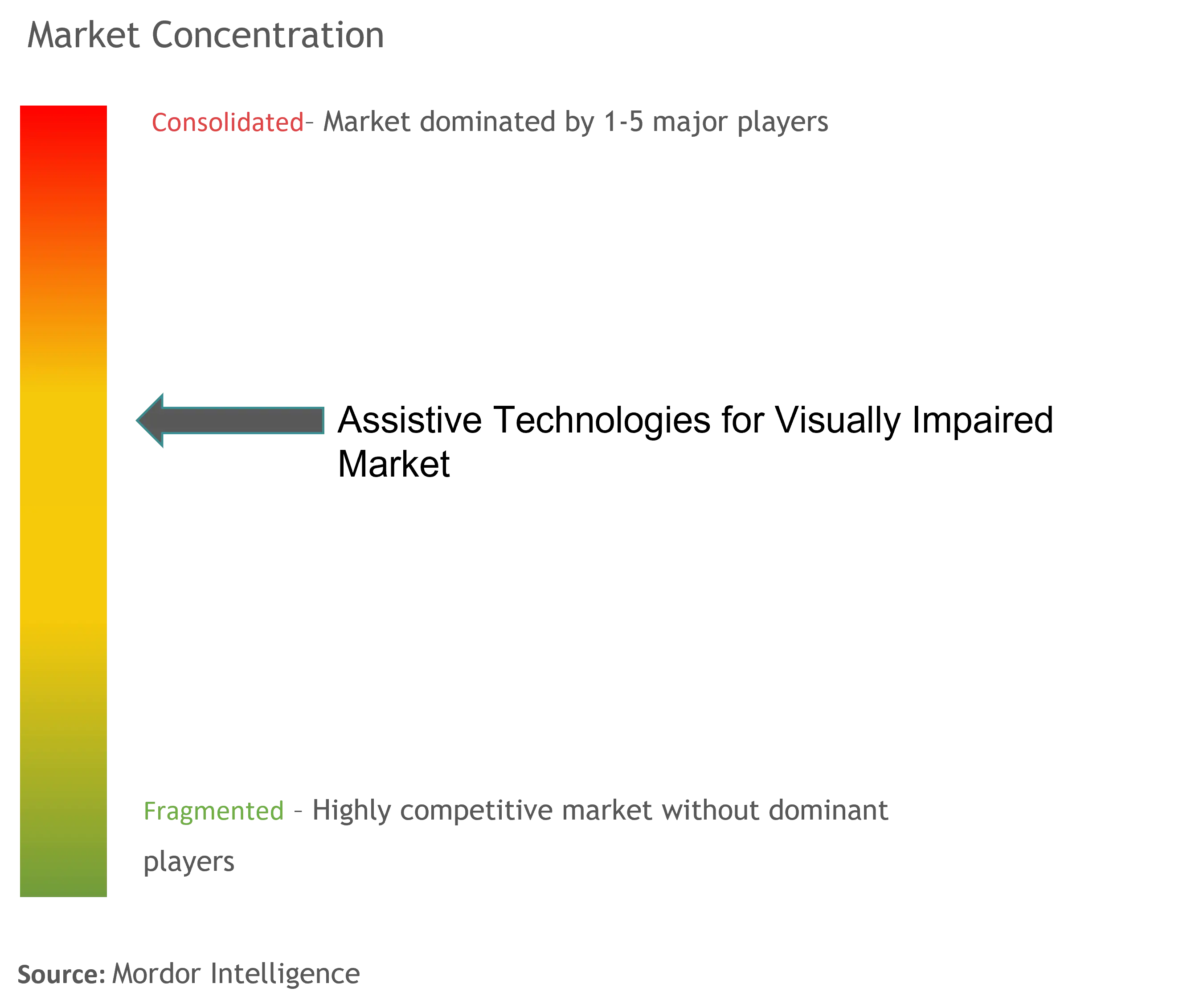

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Assistive Technologies For Visually Impaired Market Analysis by Mordor Intelligence

Assistive Technologies For Visually Impaired market size in 2026 is estimated at USD 7.09 billion, growing from 2025 value of USD 6.34 billion with 2031 projections showing USD 12.42 billion, growing at 11.86% CAGR over 2026-2031. Demographic ageing, widening regulatory coverage, and rapid AI-driven product innovation are converging to lift adoption rates across all major end-user groups. Growing vision-loss prevalence—13.2 million Americans aged 65+ already report impairment, a figure projected to double by mid-century—is sharpening the commercial urgency of inclusive design. Mandated accessibility under the European Accessibility Act (EAA) from June 2025 and the United States’ WCAG 2.1-based rules for public digital services are accelerating procurement cycles and standardizing compliance pathways. Competitive intensity is rising as platform vendors embed native accessibility tools, compelling specialist suppliers to pivot toward hybrid, cloud-connected ecosystems. As a result, the Assistive Technologies For Visually Impaired market is moving from hardware-centric point solutions to software-first service models that promise recurring revenue, lower upfront costs, and continuous feature updates.

Key Report Takeaways

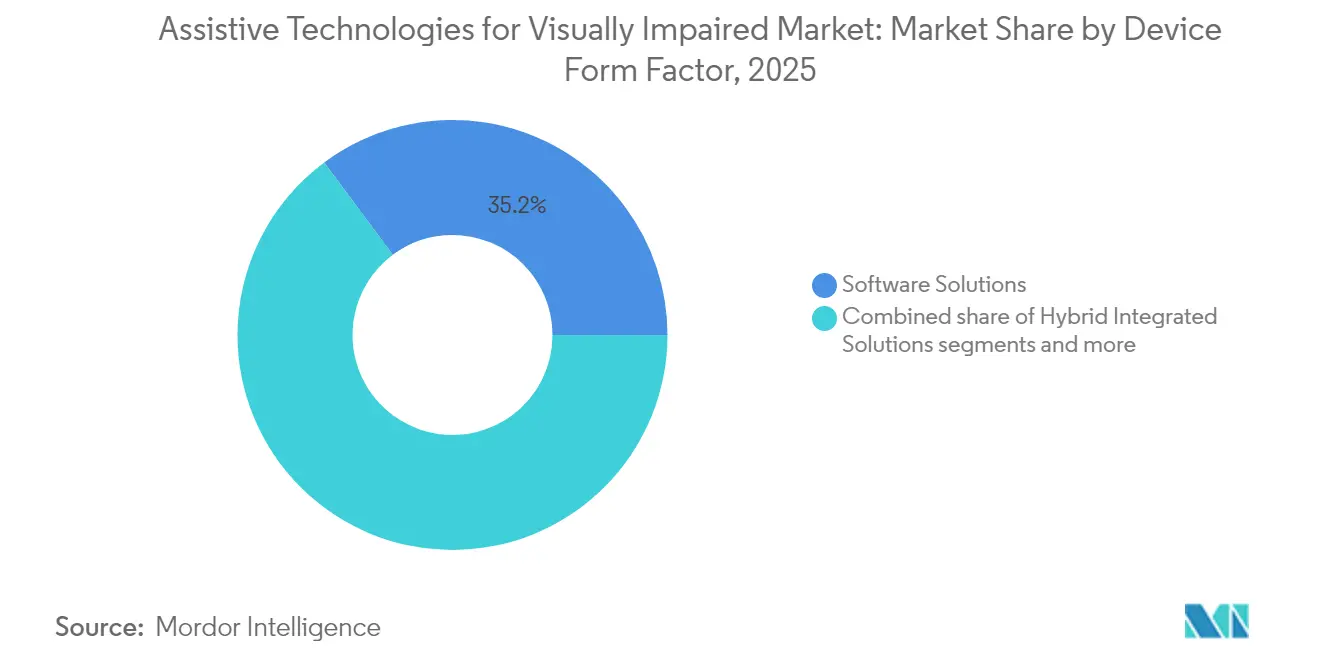

- By device form factor, Software Solutions held 35.18% of Assistive Technologies For Visually Impaired market share in 2025, while Hybrid Integrated Solutions are projected to expand at a 13.67% CAGR to 2031.

- By end user, Educational Institutions commanded 38.02% share of the Assistive Technologies For Visually Impaired market size in 2025 and Rehabilitation Centers are advancing at a 14.82% CAGR through 2031.

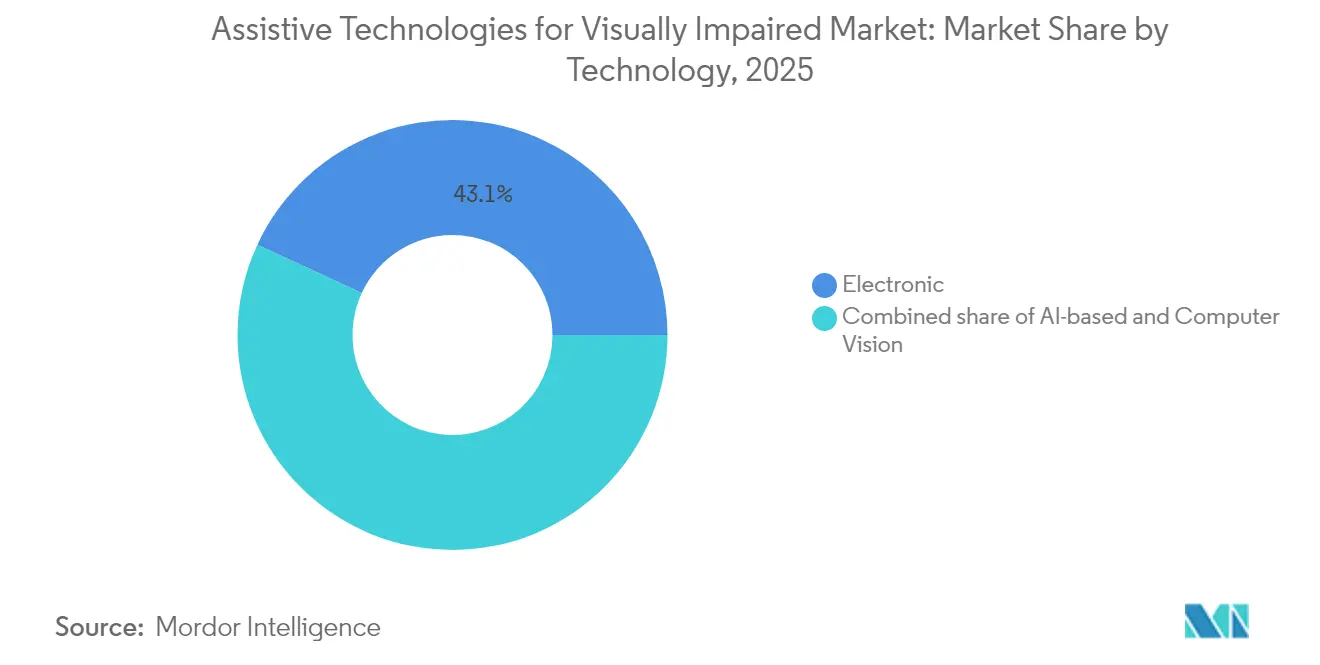

- By technology, Electronic platforms accounted for 43.10% of the Assistive Technologies For Visually Impaired market size in 2025; AI-based & Computer Vision solutions are forecast to grow at a 16.07% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Assistive Technologies For Visually Impaired Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & rising prevalence of visual impairment | +2.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| AI & computer-vision breakthroughs enabling smarter aids | +3.2% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Stronger accessibility regulations & public funding | +2.1% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Inclusive education & workplace mandates | +1.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Integration with mainstream consumer-electronics ecosystems | +1.8% | Global, technology-forward regions leading | Short term (≤ 2 years) |

| Open-source low-cost hardware emerging in developing nations | +0.9% | APAC, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Rising Prevalence of Visual Impairment

The Assistive Technologies For Visually Impaired market draws sustained momentum from global ageing trajectories that are pushing vision-loss incidence upward in every major region. Two-thirds of legally blind adults are seniors, and prevalence triples between the 45-64 and 75-plus cohorts. Age-related macular degeneration alone affects 1.85 million people with blindness and another 6.23 million with moderate or severe impairment worldwide. Retirees’ growing life expectancy is stretching independent-living needs well beyond previous planning horizons, prompting insurers and governments to explore technology subsidies that delay costlier institutional care. Vendors are prioritizing intuitive voice interfaces, simplified haptics, and low-maintenance designs that accommodate declining dexterity. These design choices broaden appeal across older users while positioning suppliers to capture healthcare-system cost-avoidance budgets. Consequently, the Assistive Technologies For Visually Impaired market is increasingly viewed as a core enabler of healthy ageing strategies across OECD economies.

AI & Computer-Vision Breakthroughs Enabling Smarter Aids

Machine-learning advances are transforming assistive devices from passive reading or magnification tools into proactive co-pilots that analyze complex environments in real time. Apple’s research prototype SceneScout achieves 72% scene-description accuracy using Street View imagery, letting blind users virtually rehearse unfamiliar routes. In China, university-developed smart glasses pair bone-conduction audio with AI object identification to guide users through crowded urban settings without canes. Multimodal large-language models such as Audo-Sight personalize output in real time, filtering inappropriate content and adapting to ambient noise conditions. These capabilities expand the Assistive Technologies For Visually Impaired market by unlocking navigation, social-interaction, and employment use cases that legacy products could not address. They also blur competitive boundaries as cloud-AI providers enter what was once a hardware-dominated niche. The upshot is an acceleration in feature expectations that lowers the relevance of basic magnifiers while boosting demand for connected, updateable platforms.

Stronger Accessibility Regulations & Public Funding

Statutory mandates are turning accessibility from a discretionary extra into a non-negotiable product attribute. The European Accessibility Act covers roughly 101 million disabled citizens and binds businesses with at least 10 employees or EUR 2 million turnover to offer perceivable, operable, understandable, and robust products from June 2025. In the United States, new Title II rules oblige state and local governments to reach WCAG 2.1 Level AA compliance by 2026-2027, with estimated annual benefits exceeding costs by USD 1.7 billion. Procurement officers now embed accessibility clauses in tender documents, guaranteeing baseline demand for certified solutions. Public grants and tax incentives further encourage early migration, expanding the Assistive Technologies For Visually Impaired market beyond consumer channels into civic infrastructure, libraries, and transit. These mechanisms compress adoption timelines, favor suppliers with documented compliance, and marginalize laggards unable to retrofit legacy designs within mandated deadlines.

Inclusive Education & Workplace Mandates

Academic institutions’ bulk purchases create early-life exposure that shapes long-term user preferences. The National Federation of the Blind’s 2024 resolutions underline the need for accessible mobile apps and electronic textbooks in classrooms. Once students enter the workforce, the Americans with Disabilities Act (ADA) obliges employers to provide reasonable accommodation, reinforcing the installed base originally seeded on campus. Because Educational Institutions already account for 38.59% of the Assistive Technologies For Visually Impaired market, their endorsement signals product maturity and reduces stigma among peers. Universities are deploying centrally managed software licences that update over the cloud and support single sign-on, lowering maintenance headaches. As hybrid study and remote work patterns persist, demand is shifting toward browser-based readers and AI note-taking that work across devices, further enlarging the Assistive Technologies For Visually Impaired market among knowledge-economy workers.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & limited reimbursement | -2.4% | Global, acute in developing markets | Medium term (2-4 years) |

| Low awareness & lack of trained instructors | -1.6% | Global, pronounced in rural & developing regions | Long term (≥ 4 years) |

| Interoperability gaps due to fragmented standards | -1.2% | Global, technology-dependent sectors | Short term (≤ 2 years) |

| Data-privacy & cyber-security concerns in AI vision aids | -0.8% | Global, heightened in privacy-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Limited Reimbursement

Despite plummeting sensor prices, premium assistive hardware often retails above USD 3,000, well beyond the means of many potential users. Half of U.S. adults with disabilities cite insurance denials or prohibitive co-pays as key reasons for delayed equipment purchases. Medicare still excludes most low-vision aids, effectively limiting uptake among retirees—the largest afflicted cohort. While cost-engineered products such as the Seika Braille Display sell for USD 2,495, they may omit advanced refresh rates or tactile-graphic rendering that enhance independence. This price-performance tension fragments the Assistive Technologies For Visually Impaired market into premium and budget tiers, slowing overall penetration. Vendors increasingly explore pay-as-you-go subscriptions and lease-to-own programmes to expand addressable demand, but reimbursement policy remains a gating factor.

Low Awareness & Lack of Trained Instructors

Technology alone does not guarantee meaningful use. Physicians and therapists often struggle to match device features with patient abilities, citing scarce comparative evidence and limited training. In rural counties, 65% of visually impaired respondents report transportation hurdles that prevent follow-up training visits, leading to device abandonment. Complex multi-gesture braille interfaces further raise the learning curve for seniors. As a result, knowledge gaps dampen repeat purchases and word-of-mouth referrals, slowing Assistive Technologies For Visually Impaired market growth even where funding exists. Emerging tele-rehabilitation models hold promise but require reliable broadband and multilingual curricula, both unevenly distributed. Without scaled instructor networks, technology diffusion will lag potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Form Factor: Software Scale Meets Hybrid Innovation

Software Solutions led with 35.18% share of the Assistive Technologies For Visually Impaired market in 2025, powered by cloud distribution, automatic updates, and operating-system bundling. Screen readers and text-to-speech engines now leverage AI to auto-label unlabeled buttons, minimizing developer retrofitting time. Their low marginal-cost economics allow educational districts to deploy thousands of licences under site agreements, reinforcing dominance. Yet growth curves are flattening as penetration nears saturation in high-income classrooms. Hybrid Integrated Solutions, blending smart-glasses hardware with AI edge inference, are absorbing incremental demand and are forecast to grow at 13.67% CAGR. Examples include Dot Pad, whose tactile tablet streams braille comics via a partnership with WEBTOON, broadening content horizons for younger readers. Because hybrid rigs combine radar, GPS, and camera sensors, they unlock spatial use cases unavailable to pure software, fueling cross-sell with mobility-training programs. Conversely, stand-alone Hardware Devices are facing commoditization as mainstream wearables co-opt entry-level magnifier and flashlight features. Nonetheless, niche needs such as multi-line braille graphics and low-vision video magnifiers protect a residual premium segment within the Assistive Technologies For Visually Impaired market.

The competitive stakes now revolve around firmware extensibility and API openness. Vendors shipping smart glasses increasingly expose developer kits that let third parties add scene-description engines or object-recognition plug-ins after purchase, extending lifecycle value. At the same time, procurement officers favour hardware backed by well-maintained software pipelines and over-the-air security patches. Hybrid devices therefore carry dual maintenance obligations: durable physical design plus agile cloud back ends. Suppliers able to master both disciplines will capture share as refresh cycles shorten from traditional five-year braille-display replacements to two-year subscription renewals, raising total lifetime revenue per user and enlarging the Assistive Technologies For Visually Impaired market.

By End User: Institutional Leadership and Rehabilitation Upswing

Educational Institutions accounted for 38.02% of Assistive Technologies For Visually Impaired market share in 2025, cemented by legislation that ties federal funding to accessibility compliance. Large-scale deployments of screen readers, refreshable braille displays, and digital-exam platforms reduce per-unit procurement cost, creating entry barriers for smaller vendors. Crucially, early exposure shapes lifelong brand affinity, seeding downstream enterprise adoption. Students familiar with specific key commands often request identical tools when hired, locking in institutional choices. Rehabilitation Centers, although only a mid-tier buyer today, represent the fastest-growing segment at 14.82% CAGR as health insurers increasingly reimburse technology-based vision-rehab programs shown to improve quality-of-life scores by 20% over traditional counselling.

Consumers remain the largest latent audience but face affordability barriers and fragmented retail channels. Direct-to-consumer e-commerce is expanding, yet return rates hover near 18% when onboarding support is absent. Employers, under ADA obligations, are upgrading office software to support high-contrast modes, PDF remediation, and AI-powered meeting captioning, growing enterprise demand at mid-single-digit rates. Government Organizations offer predictable contract volume, particularly for kiosk retrofits in transport hubs, although procurement cycles are lengthy. Segment-specific marketing—such as curriculum-aligned content bundles for schools or tele-rehab dashboards for clinics—will therefore differentiate winners within the Assistive Technologies For Visually Impaired market.

By Technology: Electronics Remain Bedrock as AI Surges

Electronics underpinned 43.10% of the Assistive Technologies For Visually Impaired market in 2025, spanning video magnifiers, digital braille cells, and microcontroller-driven tactile displays. Their reliability appeals where bandwidth is scarce or privacy requires offline operation. Optical approaches, including high-definition magnifiers and low-vision contact lenses, serve partial-sight users who prefer residual vision over sensory substitution. However, AI-based & Computer Vision platforms are the growth engine, set to rise at 16.07% CAGR as cloud inference costs drop and on-device neural accelerators proliferate. Apple’s on-device VoiceOver Screen Recognition exemplifies privacy-preserving machine learning that identifies unlabeled UI elements without cloud connectivity.

Mechanical/Braille technology is enjoying a renaissance through digital-actuator innovation. Devices such as Dot Watch 2 deliver 4-cell refreshable braille for under USD 400, extending tactile literacy to younger, tech-savvy audiences. Multi-line braille prototypes like Monarch offer tactile graphics for math and STEM, previously unattainable with single-line units. Converged devices are emerging that merge AI scene parsing, electronic tactile output, and optical zoom into a single package. Managing power budgets, weight, and ergonomics will be central to commercial viability. Given this convergence, suppliers that orchestrate heterogeneous technology stacks will capture premium positions as the Assistive Technologies For Visually Impaired market evolves beyond single-modality tools.

Geography Analysis

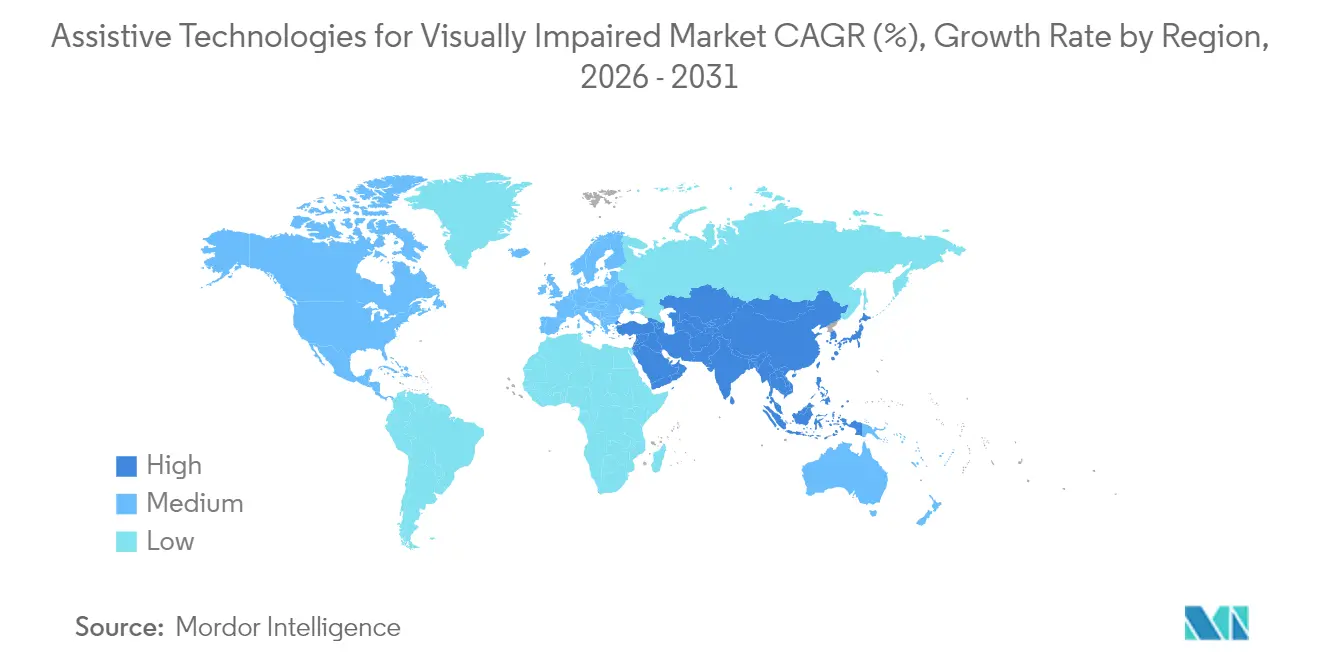

North America captured 34.86% of Assistive Technologies For Visually Impaired market revenue in 2025 thanks to entrenched disability-rights laws, sophisticated reimbursement channels, and cross-sector advocacy networks. The U.S. Department of Justice’s 2024 rule mandating WCAG 2.1 compliance for state and local digital assets creates multi-year procurement tailwinds, especially for cloud auditing and remediation software. Private insurers, however, still classify many assistive solutions as convenience devices, limiting broad subsidy coverage and preserving a two-tier adoption pattern. Canadian federal research grants are stimulating AI-powered braille R&D, while Mexico’s IMSS is piloting low-cost smart-cane deployments in urban clinics.

Asia-Pacific is the fastest-expanding contributor, forecast to post a 17.42% CAGR through 2031 as rapidly ageing populations and high myopia incidence raise demand. China demonstrates indigenous design flexibility by retrofitting low-cost smartphones with local-language screen readers, while South Korea’s Dot Corporation exports tactile displays globally. Japanese firms bundle smart-glasses training with rehabilitation insurance, creating integrated service loops. Government procurement in India and Indonesia is focusing on school-based braille laptop labs, driven by national inclusive-education mandates. These initiatives collectively swell the Assistive Technologies For Visually Impaired market across APAC, even as affordability remains a policy challenge.

Europe sits between North American maturity and Asian momentum. Harmonization under the EAA eradicates country-by-country compliance checks, encouraging pan-EU product launches and unlocking scale economies. Nordic welfare models fund personal assistive technology allowances, whereas Southern European systems lean on NGO-provided devices. Data-privacy rules spur local AI inference, making on-device processing a key selling point. The Middle East and Africa contribute smaller volumes today but hold long-run upside as multilateral donors finance inclusive digital-service roll-outs; yet political instability and limited supply chains temper near-term growth. Each region’s unique policy and cost structures will therefore dictate differentiated go-to-market models within the global Assistive Technologies For Visually Impaired market.

Competitive Landscape

Specialist incumbents and platform giants are now competing on four strategic fronts: ecosystem breadth, AI leadership, price accessibility, and regulatory credibility. Vispero, HumanWare, and HIMS continue to defend their installed base through full-stack offerings that bundle hardware, screen-reader licences, and multi-year support contracts. Their long-standing relationships with disability-services agencies still influence bulk-purchase decisions, yet contract renewal discussions increasingly include proof of WCAG 2.1 compatibility audits and cloud-security certifications. To widen reach, Vispero signed an October 2024 integration agreement with Aira that embeds remote visual-interpreter services directly inside JAWS and ZoomText.

Mainstream platforms leverage scale advantages unavailable to niche suppliers. Apple’s annual mobile OS upgrades now roll out multimodal object-recognition pipelines to hundreds of millions of devices on day one, lowering the perceived need for add-on OCR cameras or magnifier headsets. Google licenses cloud-vision APIs to third-party smart-glasses makers, accelerating time-to-market for start-ups that lack proprietary data sets. Microsoft is blending accessibility features into PowerPoint via Dot Vista, signalling deeper productivity-suite integration that could displace standalone tactile-graphics software. Because these giants already comply with GDPR and SOC 2, institutional buyers consider them low-risk anchors inside multi-vendor frameworks, a trend that pressures pure-play Assistive Technologies For Visually Impaired market suppliers to seek defensive alliances or carve out hyper-specialised niches.

Capital markets are funding next-wave challengers focused on AI personalisation and subscription economics. Eyedaptic raised follow-on capital to commercialise the EYE6 smart glasses, which run an on-device transformer model translating 99 languages for real-time scene narration. Start-ups position themselves as agile complements to mega-platforms, offering SDKs that let developers embed braille or haptic output into mainstream apps within hours. As acquisition multiples in the wider accessibility software field, consolidation is likely to intensify, reshaping the Assistive Technologies For Visually Impaired market over the next five years.

Assistive Technologies For Visually Impaired Industry Leaders

INDEX BRAILLE

American Thermoform Corp.

Amedia Networks, Inc.

Vispero

Dolphin Computer Access Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dot Corporation unveiled Dot Vista, an AI-enabled braille-graphics module for Microsoft PowerPoint, at Build 2025

- October 2022: Vispero partnered with Aira to integrate remote sighted-guide services into desktop and mobile products

Global Assistive Technologies For Visually Impaired Market Report Scope

As per the scope of the report, Assistive Technologies for the Visually Impaired consists of products that aid blind or visually impaired individuals to study/read, hear, and write, and also assist in mobility. The Assistive Technologies for the Visually Impaired Market is segmented by Product Type (Educational Devices & Software (Braille Computers/Systems, Braille Duplicators & Writers, Mathematical & Science Devices, Reading Machines, and Others), Mobility Devices, Low Vision Devices (Smart Glasses, Magnifying Lenses, Others), and Others), By End User (Blind Schools and Training Institutes, Government/Social/Non-profit organizations, and Enterprises, Federation & Hospital, and Personal Use), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Hardware Devices | Braille Displays & Note Takers |

| Braille Printers & Embossers | |

| Wearable Assistive Devices | |

| Navigation Aids | |

| Magnification Aids | |

| Others (Document Holders, Monitors, etc.) | |

| Software Solutions | Screen Readers |

| Voice Recognition & TTS Software | |

| Others (OCR, Talking Calculators, etc.) | |

| Hybrid Integrated Solutions | Smart Glasses (Wearable AI Devices) |

| Smart Canes / IoT Navigation Aids | |

| Integrated Braille Tablets & Pads | |

| Other Converged Solutions |

| Individuals / Consumers |

| Educational Institutions |

| Enterprises & Workplace |

| Rehabilitation Centers & NGOs |

| Government Organizations |

| Optical |

| Electronic |

| AI-based & Computer Vision |

| Mechanical / Braille |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Device Form Factor (integrated with Product Type) | Hardware Devices | Braille Displays & Note Takers |

| Braille Printers & Embossers | ||

| Wearable Assistive Devices | ||

| Navigation Aids | ||

| Magnification Aids | ||

| Others (Document Holders, Monitors, etc.) | ||

| Software Solutions | Screen Readers | |

| Voice Recognition & TTS Software | ||

| Others (OCR, Talking Calculators, etc.) | ||

| Hybrid Integrated Solutions | Smart Glasses (Wearable AI Devices) | |

| Smart Canes / IoT Navigation Aids | ||

| Integrated Braille Tablets & Pads | ||

| Other Converged Solutions | ||

| By End User | Individuals / Consumers | |

| Educational Institutions | ||

| Enterprises & Workplace | ||

| Rehabilitation Centers & NGOs | ||

| Government Organizations | ||

| By Technology | Optical | |

| Electronic | ||

| AI-based & Computer Vision | ||

| Mechanical / Braille | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Assistive Technologies For Visually Impaired market in 2026?

The market stands at USD 7.09 billion in 2026 and is forecast to grow at a 11.86% CAGR to USD 12.42 billion by 2031.

Which device category leads current demand?

Software Solutions hold the largest 35.18% revenue share, driven by cloud-distributed screen readers and text-to-speech tools.

Which region will grow the fastest through 2031?

Asia-Pacific is projected to expand at a 17.42% CAGR, fuelled by ageing demographics and rising myopia prevalence.

What technology is seeing the quickest adoption?

AI-based & Computer Vision platforms are forecast to grow at 16.07% CAGR as on-device neural processing becomes affordable.

What is limiting consumer uptake today?

High upfront device prices and limited insurance reimbursement remain the chief barriers for individual buyers.

Page last updated on: