Occupational And Physical Therapy Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

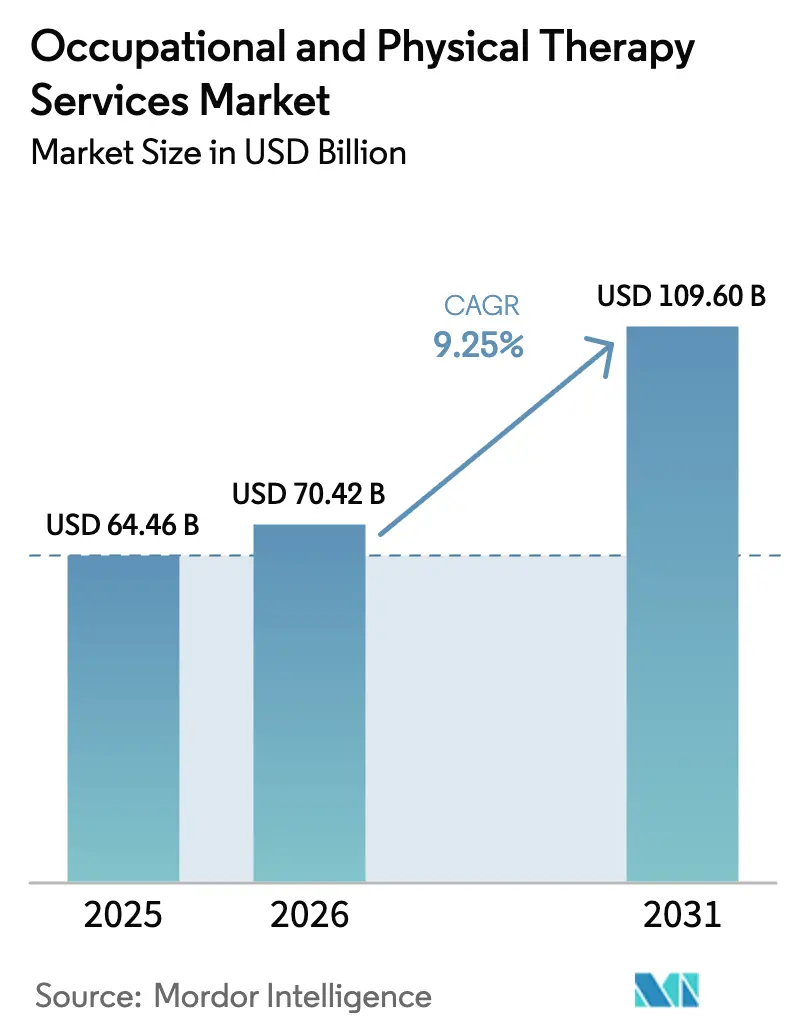

| Market Size (2026) | USD 70.42 Billion |

| Market Size (2031) | USD 109.60 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

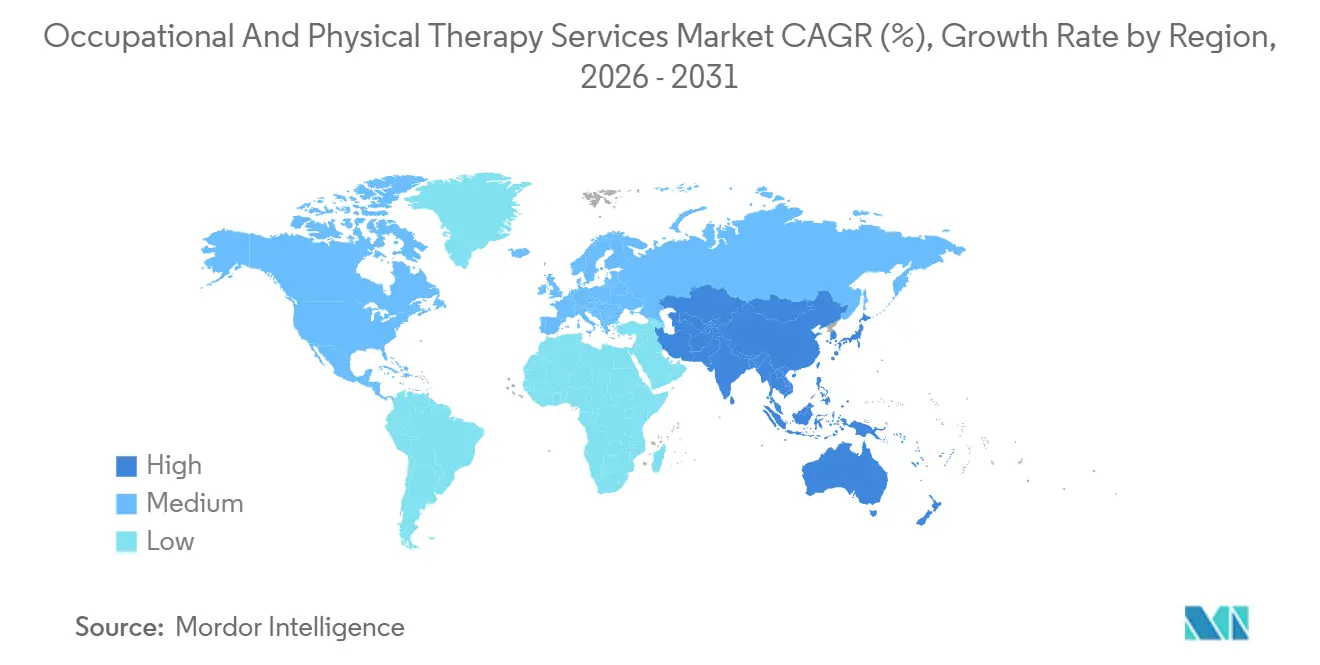

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Occupational And Physical Therapy Services Market Analysis by Mordor Intelligence

The Occupational And Physical Therapy Services Market size was valued at USD 64.46 billion in 2025 and is estimated to grow from USD 70.42 billion in 2026 to reach USD 109.60 billion by 2031, at a CAGR of 9.25% during the forecast period (2026-2031).

Structural spending is tilting toward preventive and rehabilitative care as payors try to curb downstream surgical costs, while permanent tele-rehabilitation reimbursement, artificial-intelligence triage, and employer-sponsored musculoskeletal programs keep the occupational and physical therapy services market on a fast-growth trajectory. The U.S. Bureau of Labor Statistics projects 14% employment growth for physical therapists and 11% for occupational therapists from 2023-2033, confirming that labor supply is expanding in tandem with demand. Hybrid care that blends in-person visits with virtual coaching is gaining traction after a 2025 randomized controlled trial showed non-inferior outcomes at 35% lower cost. At the same time, an aging population, rising sports-injury incidence, and rapid clinic expansion in Asia-Pacific position the occupational and physical therapy services market for durable, geographically balanced growth.

Key Report Takeaways

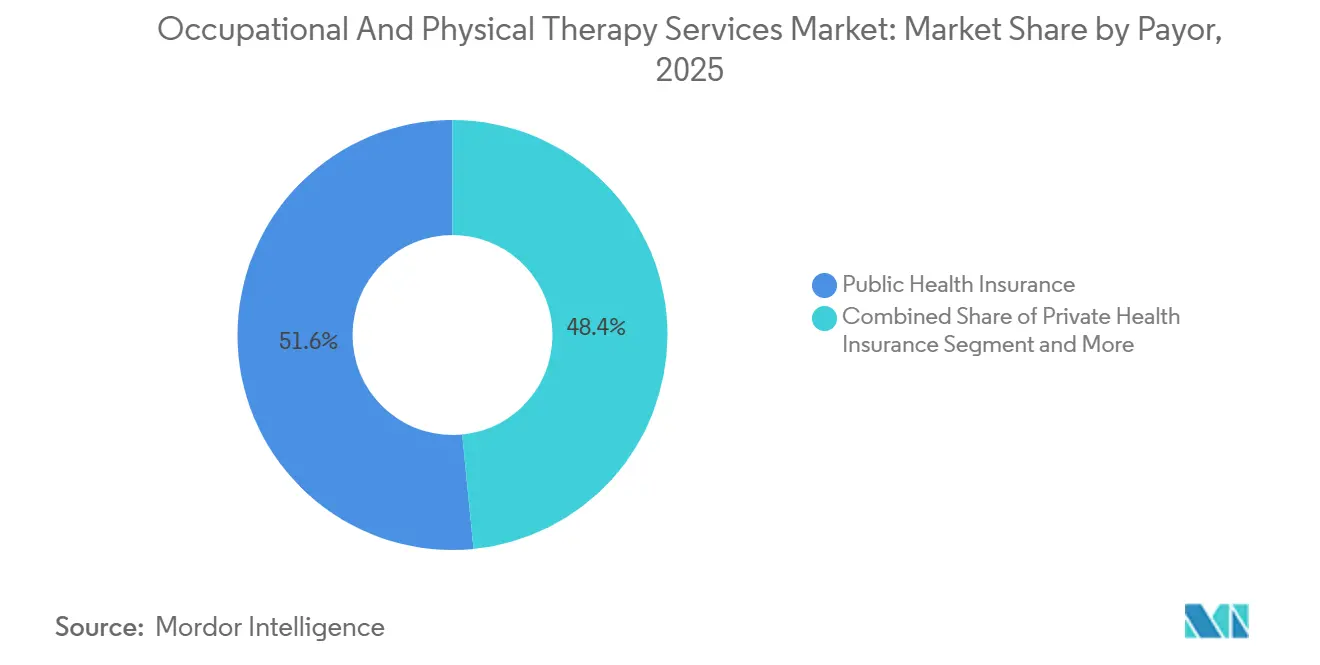

- By payor, public health plans captured 51.56% revenue in 2025, while private health insurance is advancing at a 10.25% CAGR through 2031, the fastest among funding sources.

- By application, orthopedic therapy led with 38.53% of occupational and physical therapy services market share in 2025; sports-injury therapy is on track for a 10.85% CAGR to 2031.

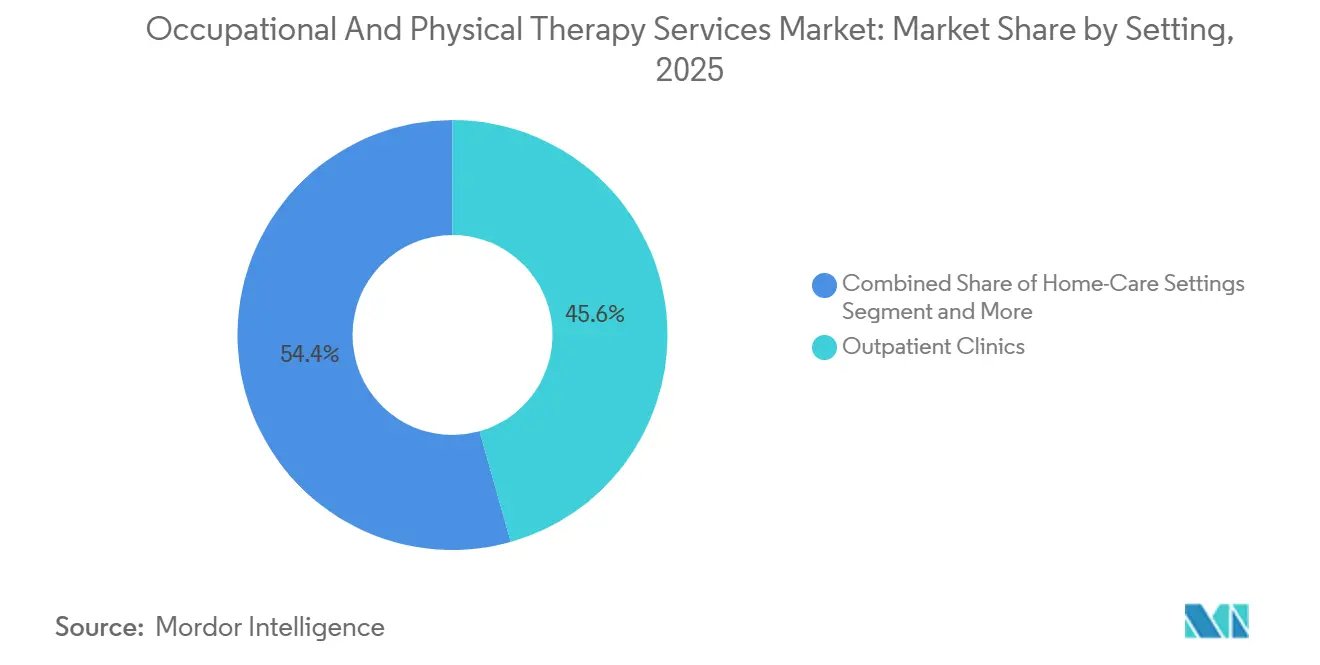

- By setting, outpatient clinics generated 45.63% revenue in 2025, but home-care venues are expanding at an 11.87% CAGR through 2031.

- By delivery mode, in-person therapy retained 68.33% revenue in 2025, yet tele-rehabilitation is scaling at a 16.7% CAGR to the end of the forecast period.

- By geography, North America contributed 40.13% revenue in 2025, whereas Asia-Pacific is projected to post the quickest regional CAGR at 10.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Occupational And Physical Therapy Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing occupational & physical-therapy workforce | +1.8% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing reimbursement coverage for rehabilitative care | +2.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising incidence of sports & recreation injuries | +1.3% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Aging-population driven musculoskeletal burden | +2.4% | Global, most acute in North America, Europe, and Japan | Long term (≥ 4 years) |

| Hybrid in-person/virtual service models | +1.2% | North America and Europe, early adoption in urban Asia-Pacific | Short term (≤ 2 years) |

| AI-enabled personalized rehab protocols | +0.9% | North America and Europe, pilot deployments in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Occupational & Physical-Therapy Workforce

The pipeline of professionals is widening: 12,400 physical therapists and 8,200 occupational therapists graduated in 2024, a 6% and 5% year-over-year increase, respectively. States such as Texas and Florida opened a combined 30 new clinics in 2024, absorbing graduates faster than legacy coastal markets. India’s 2025 skills initiative to train 50,000 therapists by 2028 aims to cut the supply lag in tier-2 and tier-3 cities. These workforce gains directly expand addressable capacity, especially in rural and suburban areas where the occupational and physical therapy services market historically suffered staffing shortages. As supply rises, wait-times shrink, bolstering adherence and recurring revenue.

Growing Reimbursement Coverage for Rehabilitative Care

CMS made pandemic-era telehealth parity permanent in its 2024 physician-fee schedule, allowing therapists to bill virtual visits at the same rate as clinic sessions[1]Centers for Medicare & Medicaid Services, “CY 2024 Medicare Physician Fee Schedule,” cms.gov. Private insurers have followed suit; UnitedHealthcare now covers up to 30 virtual sessions per year without prior authorization. Evidence supports that early, guideline-concordant therapy prevents costly surgeries: a Health Care Cost Institute study showed 28% lower lumbar-fusion rates when patients completed eight or more visits within 90 days of diagnosis. Employer adoption is also rising, with Amazon operating on-site therapy clinics in 25 fulfillment centers by 2025.

Rising Incidence of Sports & Recreation Injuries

Sports-related emergency visits climbed to 3.2 million in 2024, a 9% jump over 2023, with youth soccer and adult recreational basketball leading the surge[2]Consumer Product Safety Commission, “NEISS Data Highlights,” cpsc.gov. ACL reconstructions rose 7% in the same period, extending rehabilitation cycles to 9-12 months. School districts now embed athletic trainers and therapists in 85% of U.S. high schools. Japan echoes the trend: its 2025 plan will place therapists in 10,000 community sports clubs by 2027, targeting middle-aged “weekend warriors”. This steady inflow of active patients reinforces year-round demand in the occupational and physical therapy services market.

Aging-Population Driven Musculoskeletal Burden

Adults aged 65+ in the United States will swell to 73 million by 2030. Arthritis prevalence already exceeds 58.5 million and is projected to top 78 million by 2040. Medicare Advantage sponsors see value in home-based therapy: Humana covered in-home services for 1.2 million members in 2024 and reported a 22% fall in hip-fracture hospitalizations. Comparable demographic waves in Europe and Japan sustain long-run tailwinds for the occupational and physical therapy services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness & limited access in emerging markets | -1.2% | Asia-Pacific (excluding Japan & Australia), Middle East & Africa, Latin America | Long term (≥ 4 years) |

| High out-of-pocket cost for long treatment cycles | -0.8% | Global; acute in U.S. high-deductible plans and emerging markets without universal coverage | Medium term (2-4 years) |

| Data-privacy concerns around tele-rehab platforms | -0.6% | North America and Europe; spillover to urban Asia-Pacific | Short term (≤ 2 years) |

| Fragmented outcome-tracking standards | -0.5% | Global, especially cross-border digital platforms and multi-state providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Awareness & Limited Access in Emerging Markets

Only 15% of people in low-income nations who need rehabilitation actually receive it, versus 65% in high-income countries. Sub-Saharan Africa averages 0.04 physical therapists per 10,000 population, compared with 7.2 in North America. India maintains a 1-per-90,000 therapist-to-population ratio. Long travel distances, tuition bottlenecks, and narrow insurance benefits restrain penetration. Government workforce planning and benefit-design reforms are prerequisites for closing this gap, otherwise demand will remain latent.

High Out-of-Pocket Cost for Long Treatment Cycles

Patients in U.S. high-deductible health plans average 6.2 therapy visits per episode, versus 9.8 for low-deductible enrollees, even though guidelines call for 10-12 visits. In Brazil, a private session costs USD 40-60, or up to 20% of monthly minimum wage, curtailing adherence. Tele-rehab trims per-session fees but cannot replace hands-on manual techniques. California’s 2024 subsidy caps Medicaid co-pays at USD 10, a model other states may emulate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payor: Public Plans Anchor, Private Accelerates

Public coverage held 51.56% revenue in 2025, underpinned by Medicare and Medicaid utilization, yet private health insurance is forecast to expand at a 10.25% CAGR through 2031. This acceleration derives from employers bundling musculoskeletal benefits with primary care to mitigate absenteeism. A 2024 National Business Group on Health survey showed 68% of large employers offering virtual physical therapy as a standard benefit. Meanwhile, CMS launched the Rehabilitation Therapy Alternative Payment Model in 2024, enabling shared-savings contracts that reward cost control and functional-outcome gains.

Value-based contracting tilts the competitive field toward data-literate groups able to document functional gains. Anthem now pegs 20% of therapy reimbursement to patient-reported outcome measures. This outcome-linked orientation favors larger platforms with robust analytics and positions the occupational and physical therapy services market for further consolidation.

By Application: Orthopedic Dominates, Sports Injury Surges

Orthopedic therapy generated 38.53% of revenue in 2025, benefiting from 1.2 million knee and hip replacements that each trigger 8-12 weeks of rehab. Sports-injury therapy, bolstered by increasing youth participation, is projected to post a 10.85% CAGR through 2031. Neurological therapy gains momentum as hospitals adopt early-mobilization pathways; initiating therapy within 24 hours of stroke lowered average inpatient stay by 2.3 days.

Pediatric therapy growth follows rising autism diagnosis: 1-in-36 U.S. children required specialty services in 2024. Texas Medicaid now funds up to 40 early-intervention sessions yearly, expanding demand. Specialty niches such as pelvic-floor and vestibular programs are emerging add-ons that raise visit frequency and diversify the occupational and physical therapy services market.

By Setting: Outpatient Leads, Home Care Gains

Outpatient clinics produced 45.63% of 2025 revenue thanks to convenient access and equipment breadth. Yet home-based therapy is slated for an 11.87% CAGR, buoyed by Medicare Advantage incentives and technology that enables remote supervision. MedPAC found home-based rehab following hip fracture costs 35% less per episode with comparable outcomes.

To defend share, major chains now dispatch mobile units; Athletico outfitted vans with portable ultrasound and e-stim devices in 15 metro areas by 2024. Hospitals gain some relief from the 3.2% reimbursement boost for complex therapy in the 2024 Outpatient Prospective Payment System rule.

By Service-Delivery Mode: Virtual Scales, In-Person Endures

In-person visits still commanded 68.33% revenue in 2025, underscoring the enduring need for manual techniques. Tele-rehabilitation, however, is tracking a 16.7% CAGR through 2031 after CMS locked in parity and interstate licensure compacts reduced regulatory friction. A 2024 BMJ Open meta-analysis of 42 trials confirmed non-inferior outcomes for chronic musculoskeletal cases managed virtually.

Hybrid therapy blends the best of both worlds: the American Physical Therapy Association endorsed hybrid pathways for low-back pain and knee osteoarthritis in its 2024 guidelines. As clinics optimize in-person-to-virtual ratios, the occupational and physical therapy services market is likely to shift toward outcome-priced episode bundles rather than visit-count billing.

Geography Analysis

North America contributed 40.13% revenue in 2025, with Medicare spending on outpatient therapy hitting USD 9.8 billion, a 6.2% annual rise driven mainly by volume. Canada’s single-payer system covers post-surgical rehab but leaves chronic care largely out-of-pocket, fostering a parallel private clinic sector. Mexico’s federal clinics now provide basic therapy, yet most demand remains private, centered in affluent urban corridors. The U.S. Department of Veterans Affairs embedded therapists in 150 community clinics in 2024 to cut veteran wait times.

Asia-Pacific is projected to advance at a 10.51% CAGR through 2031, the fastest worldwide. China’s 2024 policy permits therapists to open independent practices, supporting rapid clinic proliferation. India’s Apollo Hospitals will introduce 50 rehabilitation centers across tier-2 cities by 2027. Japan confronts labor shortages as its therapist vacancy rate reached 15%, spurring investment in robotic-assist devices. Australia’s National Disability Insurance Scheme added AUD 2.1 billion in 2024 funding, enlarging pediatric and neuro-rehab capacity.

Europe maintains steady growth. Germany’s statutory plans reimburse up to six sessions per prescription, underpinning predictable outpatient volumes. NHS England’s physiotherapy wait times stretched to eight weeks in 2024, propelling private digital alternatives.

Competitive Landscape

The market remains moderately fragmented: the top players control a significant percentage of outpatient revenue. Encompass Health operated 1,350 outpatient clinics and generated USD 1.8 billion in 2024 outpatient revenue, up 7.4% year-over-year[3]Encompass Health Corporation, “Form 10-K 2024,” sec.gov. Select Medical managed more than 1,900 clinics and booked USD 2.1 billion, aided by a 4.2% same-store visit rise. Both have built proprietary tele-rehab platforms to defend share and have begun partnering with retail pharmacies to co-locate services.

Digital entrants, empowered by permanent reimbursement and employer demand, are scaling quickly. One leading virtual provider secured long-term contracts with the U.S. Department of Veterans Affairs in 2024 to supply home-based musculoskeletal programs, widening its payer mix beyond commercial employers. Another AI-centric platform earned FDA clearance for motion-tracking software and is active in five European countries. Traditional chains are responding: Select Medical committed USD 25 million to a virtual-care build-out in 2024, and Encompass Health integrated AI-guided tools into its post-acute pathways in early 2025.

White-space expansion continues in pediatric therapy and rural outreach. Mobile units, franchise networks, and school-based contracts are proliferating. With technology reducing geographic barriers, the occupational and physical therapy services market is likely to see accelerated consolidation as investors favor companies that can document outcome superiority across modalities.

Occupational And Physical Therapy Services Industry Leaders

ATI Holdings, LLC

Athletico Physical Therapy

Encompass Health Corporation

Upstream Rehabilitation Inc.

Select Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: U.S. Physical Therapy, Inc. acquired a management services firm overseeing eight clinics that log 66,000 annual visits and USD 8 million in revenue, expanding its footprint in the Midwest.

- May 2025: Kelly added Children’s Therapy Center, a Minnesota-based pediatric occupational, physical, and speech therapy specialist, broadening its developmental-services portfolio.

Global Occupational And Physical Therapy Services Market Report Scope

As per the scope of the report, occupational and physical therapy services are healthcare interventions aimed at enhancing an individual's functional abilities and overall well-being. Occupational therapy focuses on helping individuals develop, recover, or maintain the skills necessary for daily activities, such as dressing, cooking, and working, by improving fine motor skills, coordination, and adaptive strategies. Physical therapy, on the other hand, is centered on restoring movement, reducing pain, and increasing physical strength and mobility through exercises, manual techniques, and various modalities, often to treat injuries, musculoskeletal conditions, neurological disorders, and other health issues impacting physical function.

The occupational and physical therapy services market is segmented by payer, application, setting, service delivery mode, and geography. By payer, the market is divided into public health insurance, private health insurance, and out-of-pocket payments. By application, it includes orthopedic therapy, neurological therapy, sports injury therapy, general therapy, geriatric therapy, pediatric therapy, and other applications. By setting, the market is segmented into hospitals, outpatient clinics, home care settings, and other settings. By service delivery mode, it is classified into in-person therapy, tele-rehabilitation/virtual therapy, and hybrid therapy. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Public Health Insurance |

| Private Health Insurance |

| Out-of-Pocket |

| Orthopedic Therapy |

| Neurological Therapy |

| Sports-Injury Therapy |

| General Therapy |

| Geriatric Therapy |

| Pediatric Therapy |

| Other Applications |

| Hospitals |

| Outpatient Clinics |

| Home-Care Settings |

| Other Settings |

| In-person Therapy |

| Tele-rehabilitation / Virtual Therapy |

| Hybrid Therapy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Payor | Public Health Insurance | |

| Private Health Insurance | ||

| Out-of-Pocket | ||

| By Application | Orthopedic Therapy | |

| Neurological Therapy | ||

| Sports-Injury Therapy | ||

| General Therapy | ||

| Geriatric Therapy | ||

| Pediatric Therapy | ||

| Other Applications | ||

| By Setting | Hospitals | |

| Outpatient Clinics | ||

| Home-Care Settings | ||

| Other Settings | ||

| By Service-Delivery Mode | In-person Therapy | |

| Tele-rehabilitation / Virtual Therapy | ||

| Hybrid Therapy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected global value of occupational and physical therapy services in 2031?

Spending is projected to reach USD 109.60 billion by 2031.

How quickly is tele-rehabilitation revenue expanding through 2031?

Tele-rehabilitation is forecast to grow at a 16.7% CAGR, the fastest pace among delivery modes.

Which geographic region is anticipated to record the strongest growth through 2031?

Asia-Pacific is on track for a 10.51% CAGR, outpacing all other regions over the forecast period.

What share of 2025 revenue came from public health insurance plans?

Public payors accounted for 51.56% of global revenue in 2025.

Which application area is poised for the fastest growth over the next five years?

Sports-injury therapy is projected to expand at a 10.85% CAGR through 2031.

Page last updated on: