OBGYN EHR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

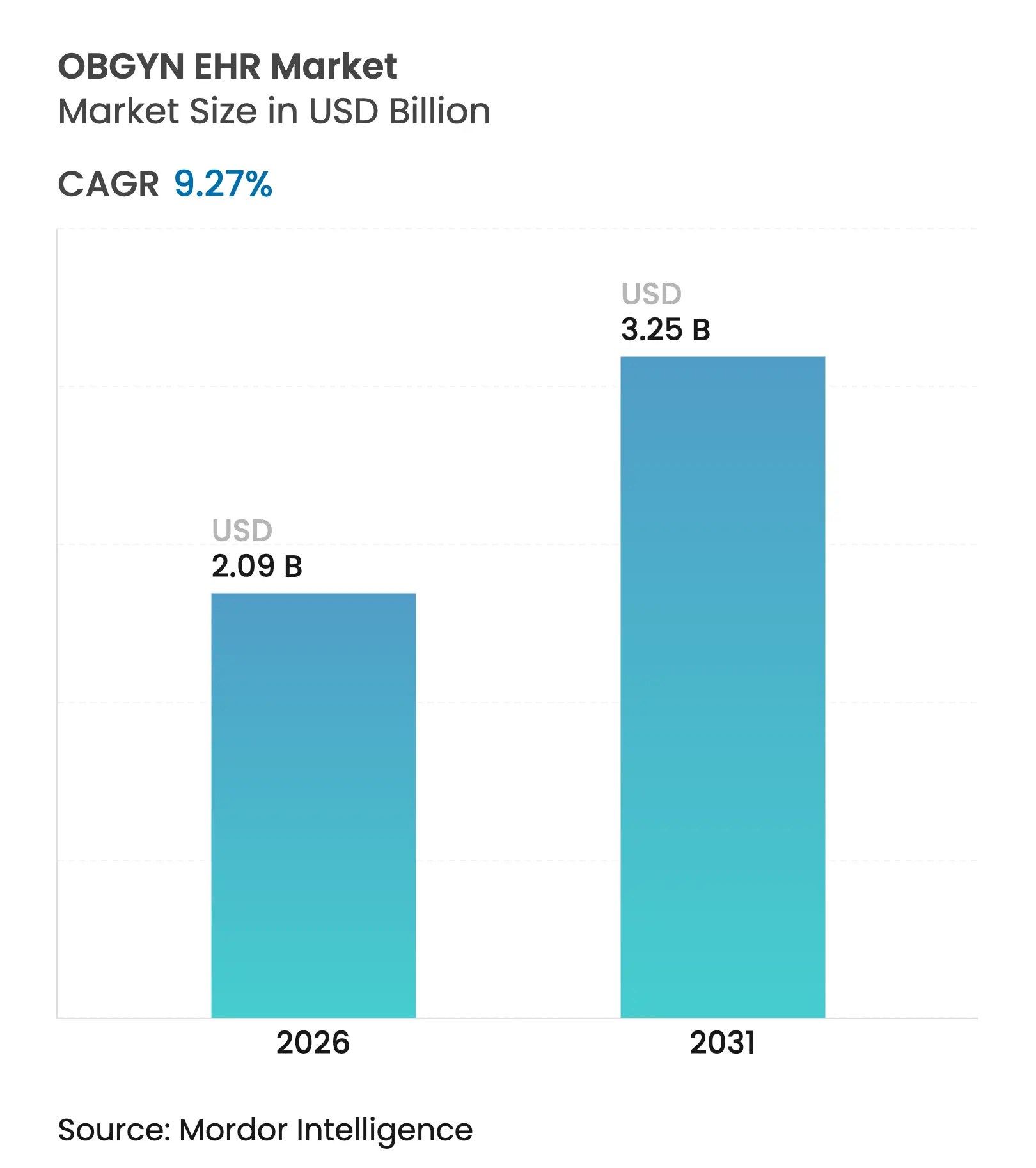

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 9.27 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

OBGYN EHR Market Analysis by Mordor Intelligence

The OBGYN EHR market size is expected to grow from USD 1.91 billion in 2025 to USD 2.09 billion in 2026 and is forecast to reach USD 3.25 billion by 2031 at 9.27% CAGR over 2026-2031. Growth is propelled by regulatory incentives that reward precise maternal-health reporting, rapid uptake of cloud deployment, and wider tele-obstetric reimbursement frameworks. Cloud platforms shorten implementation times, lower capital outlays, and streamline remote prenatal monitoring, while AI-enabled decision support further improves risk detection and documentation efficiency. Vendors that embed specialty-specific workflows now outpace generalist platforms, and emerging subscription models extend access to smaller practices.

Key Report Takeaways

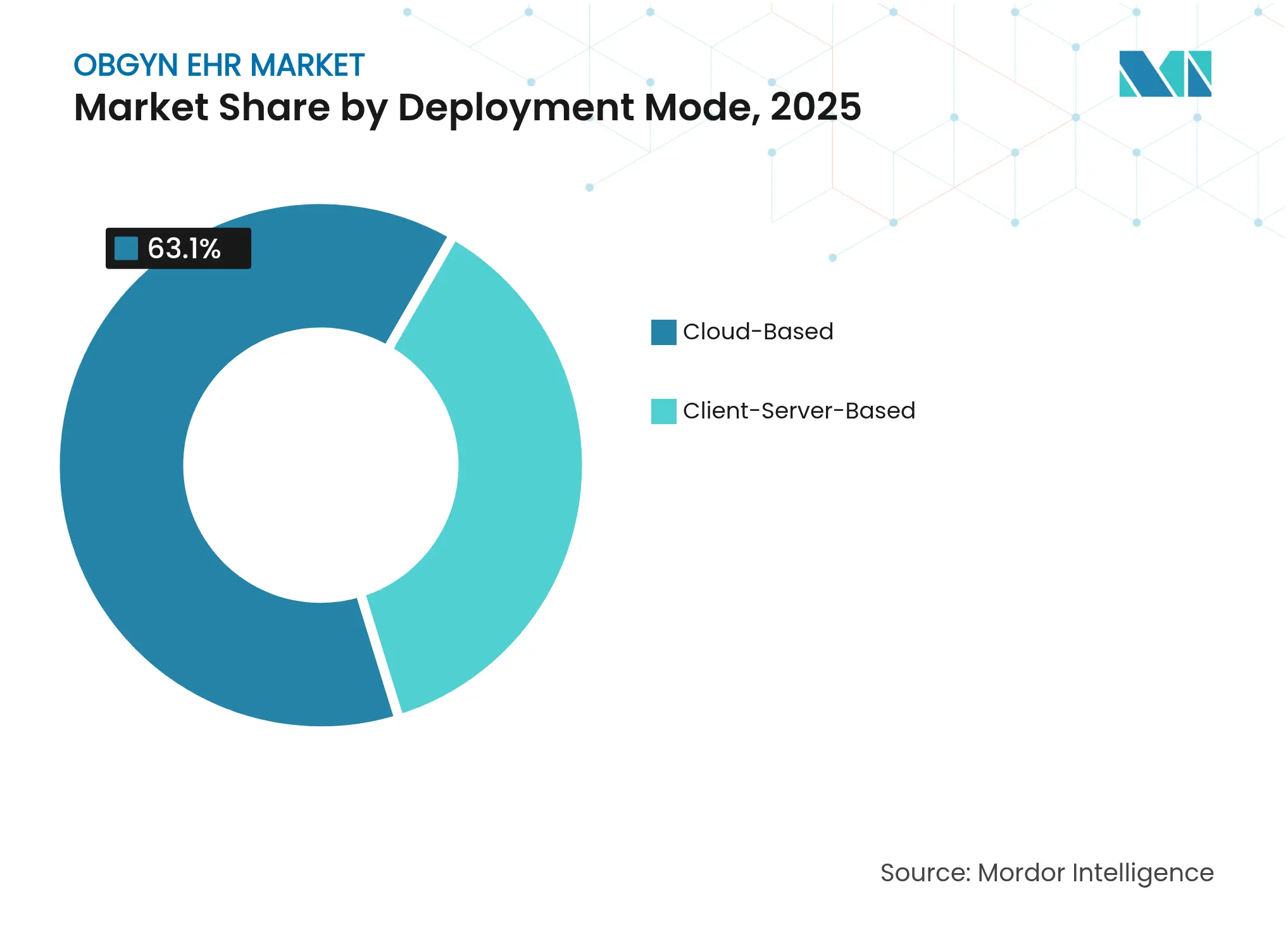

- By deployment mode, cloud-based systems captured 63.10% of the OBGYN EHR market share in 2025 and are expanding at a 9.65% CAGR through 2031.

- By application, clinical documentation led with 42.05% of the OBGYN EHR market size in 2025, while workflow management is projected to grow at 9.82% CAGR to 2031.

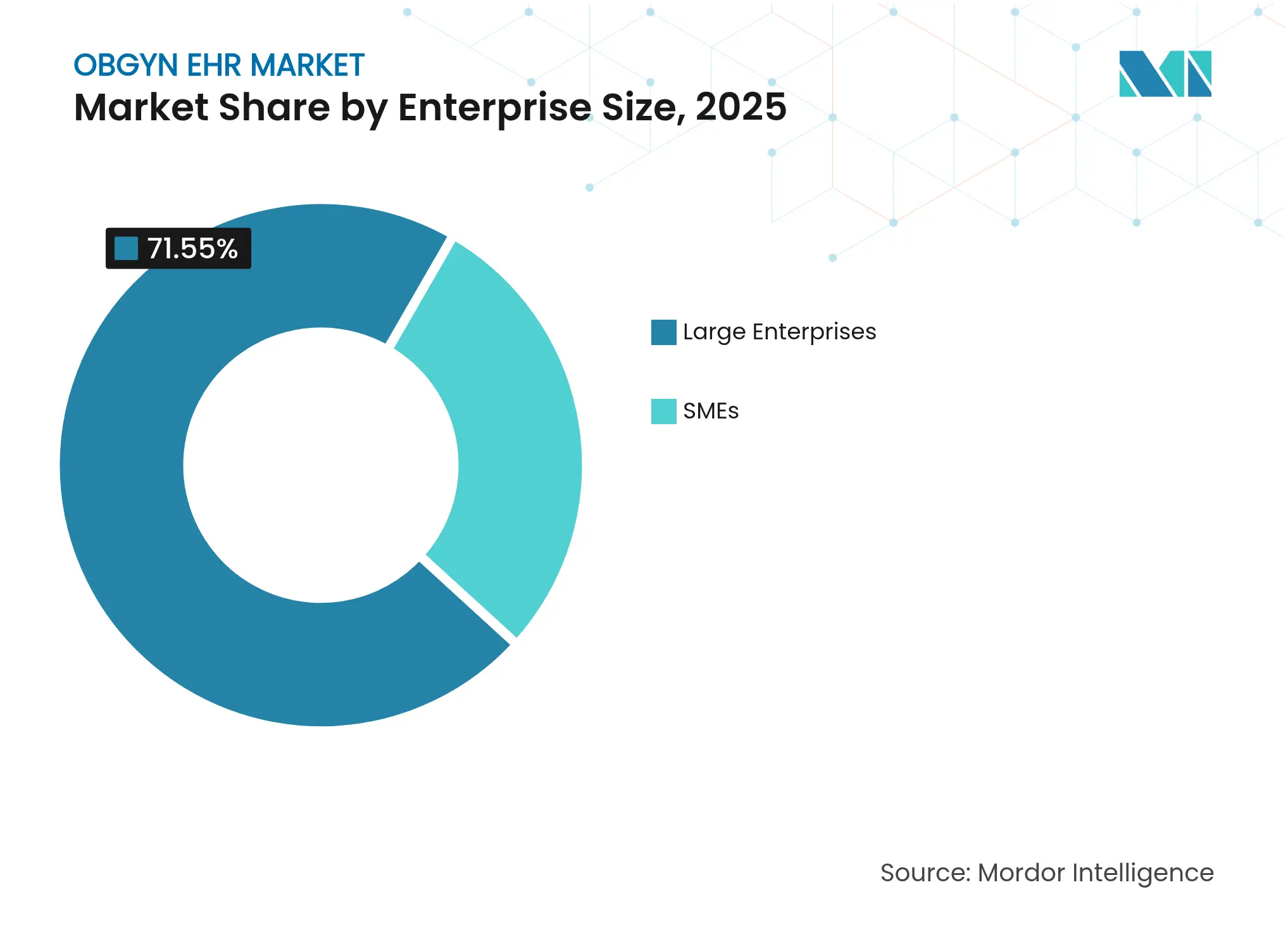

- By enterprise size, large enterprises controlled 71.55% of 2025 revenue, yet small and medium enterprises show the strongest momentum at 9.7% CAGR.

- By end-user, hospitals held 46.95% revenue share in 2025, whereas clinics and physician offices are forecast to post a 9.5% CAGR through 2031.

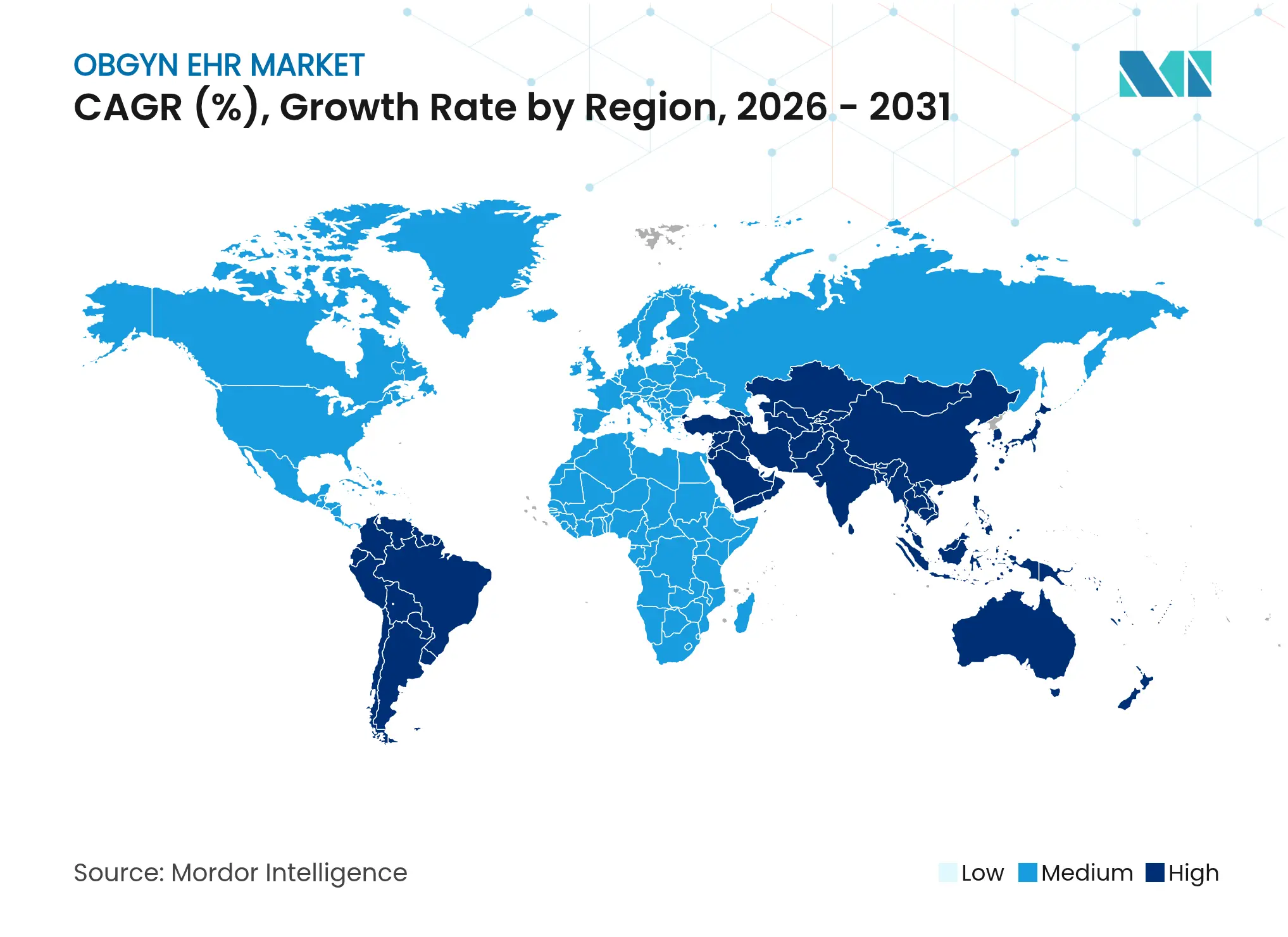

- By geography, North America maintained 41.60% revenue share in 2025; Asia-Pacific is the fastest-growing region at 11.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global OBGYN EHR Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Demand for Specialty-Specific EHRs Under

Value-Based Care

Rising Demand for Specialty-Specific EHRs Under

Value-Based Care

| +1.8% | Global with early adoption in North America & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global with early adoption in North America & Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Increasing Adoption of Cloud Deployment for Remote

Prenatal Care

Increasing Adoption of Cloud Deployment for Remote

Prenatal Care

| +1.5% | Global, accelerated in APAC & emerging markets | Short term (≤ 2 years) | |||

Regulatory Incentives for Maternal-Health Data

Interoperability

Regulatory Incentives for Maternal-Health Data

Interoperability

| +1.2% | North America & EU regulatory frameworks | Long term (≥ 4 years) | |||

AI-Driven Predictive Analytics for High-Risk Pregnancies

AI-Driven Predictive Analytics for High-Risk Pregnancies

| +1.0% | North America, Europe, select APAC | Medium term (2-4 years) | |||

Expansion of Tele-Obstetric Reimbursement Frameworks

Expansion of Tele-Obstetric Reimbursement Frameworks

| +0.9% | North America with gradual global reach | Medium term (2-4 years) | |||

Investment Surge in Women’s Digital-Health Start-Ups

Integrating with EHRs

Investment Surge in Women’s Digital-Health Start-Ups

Integrating with EHRs

| +0.7% | North America & Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Specialty-Specific EHRs Under Value-Based Care

Obstetric and gynecologic providers see measure-driven reimbursement as a catalyst for adopting purpose-built platforms that automate gestational age calculations, maternal morbidity tracking, and pregnancy-quality metrics. CMS ties bonus payments to demonstrable perinatal outcomes in the CY 2025 Medicare Physician Fee Schedule. ONC’s USCDI+ Maternal Health data[1]Office of the National Coordinator for Health IT, “Maternity Care Information Resource Guide,” healthit.gov classes further standardize obstetric information exchange, giving specialty vendors a compliance edge. Practices, therefore, favor systems that natively capture pregnancy-specific measures instead of retrofitting generic templates.

Increasing Adoption of Cloud Deployment for Remote Prenatal Care

Cloud architectures synchronize fetal-monitor readings and patient-reported vitals to clinician dashboards in real time. Remote visits gained permanent reimbursement status in CMS’s 2025 schedule, solidifying tele-obstetric workflows. Providers report 30–40% lower total cost of ownership compared with client-server-based installations, freeing capital for patient engagement tools. Scalability also supports multi-location groups seeking uniform prenatal protocols.

Regulatory Incentives for Maternal-Health Data Interoperability

The 21st Century Cures Act prohibits information blocking, compelling vendors to open APIs that share pregnancy data across care teams. New obstetrical safety standards in the 2025 Hospital Outpatient Prospective Payment System[2]Centers for Medicare & Medicaid Services, “CMS Announces New Policies to Reduce Maternal Mortality, Increase Access to Care and Advance Health Equity,” cms.gov require automatic quality reporting from EHRs. HL7 FHIR implementation guides focused on pregnancy encourage standardized exchange, rewarding compliant platforms.

AI-Driven Predictive Analytics for High-Risk Pregnancies

Cedars-Sinai validates machine-learning models[3]Cedars-Sinai, “Artificial Intelligence Can Improve OB-GYN Care,” cedars-sinai.org that flag preeclampsia earlier than legacy scoring tools. Epic embeds more than 100 AI features, including maternal-risk stratifiers, showing how large platforms leverage data scale to recreate specialty value. Practices note 15–20% time savings in documentation alongside improved diagnostic precision.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Implementation Costs & Delayed ROI

High Implementation Costs & Delayed ROI

| -1.4% | Global, heavier on SMEs & rural sites | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global, heavier on SMEs & rural sites

|

Impact Timeline

:

Medium term (2-4 years)

|

Data-Privacy & Cybersecurity Concerns Around

Reproductive Data

Data-Privacy & Cybersecurity Concerns Around

Reproductive Data

| -1.1% | North America post-Dobbs, global privacy rules | Long term (≥ 4 years) | |||

Fragmented Prenatal-Device Integration Standards

Fragmented Prenatal-Device Integration Standards

| -0.8% | Global, larger drag in emerging markets | Medium term (2-4 years) | |||

Political Restrictions on Reproductive-Health Data Sharing

Political Restrictions on Reproductive-Health Data Sharing

| -0.6% | North America state variations | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Implementation Costs & Delayed ROI

Total ownership often exceeds USD 100,000 per provider once licensing, workflow redesign, and training are tallied, extending payback periods to five years for small practices. Overruns averaging 20–30% stem from unforeseen interface work and prolonged adoption curves, prompting many independents to join larger systems to access capital and IT expertise.

Data-Privacy & Cybersecurity Concerns Around Reproductive Data

Following the Dobbs ruling, clinicians fear subpoenas for reproductive records. The April 2024 HIPAA rule seeks to block such disclosures, but ongoing legal challenges create ambiguity. Some patients, therefore, avoid digital portals, while providers demand granular consent controls that limit data sharing by jurisdiction. Vendors investing in advanced consent engines gain trust advantages but must also harden defenses against ransomware aimed at sensitive maternal information.

Segment Analysis

By Deployment Mode: Cloud Architecture Drives Remote Care Innovation

Cloud systems dominated the 2025 landscape with 63.10% of the OBGYN EHR market share in 2025 and a 9.65% CAGR outlook, anchored by pay-as-you-go pricing and seamless multi-device connectivity. This adoption wave accelerated during pandemic lockdowns, when obstetric providers needed immediate telehealth and remote-monitoring capability. Modern platforms integrate wearables, video, and AI in unified workspaces that cut infrastructure spending by up to 40%. Client-server-based installations persist inside large academic hospitals that must retain legacy interfaces or meet strict data-sovereignty statutes, but their incremental upgrades trail cloud momentum.

Migrating to software-as-a-service allows practices of every size to standardize prenatal protocols, run analytics across sites, and receive continuous feature updates without downtime. Vendors bundle disaster recovery and 24/7 patch management, lowering cybersecurity risk compared with self-hosted stacks. The OBGYN EHR market, therefore, aligns cloud roadmaps to clinical ambitions such as omnichannel scheduling and longitudinal maternal registries.

Note: Segment shares of all individual segments available upon report purchase

By Application: Documentation Efficiency Meets Workflow Automation

Clinical documentation held 42.05% of the OBGYN EHR market size in 2025 because obstetric encounters demand longitudinal data capture on vitals, fetal growth, and maternal labs at every visit. Dictation and ambient voice tools now auto-generate progress notes, freeing clinicians to focus on patient counseling. Workflow management, the fastest-growing application at 9.82% CAGR, orchestrates task routing, care-path triggers, and discharge planning, reducing staff hand-offs and error rates.

Coding and billing remain essential but are increasingly embedded inside broader revenue-cycle modules that post claims in near real time. Advanced scheduling engines apply AI to optimize provider availability against gestational timelines, cutting no-show rates and balancing labor induction slots. As automation expands, the OBGYN EHR market interlinks documentation and workflows, generating predictive task lists and compliance alerts that boost operating margin.

By Enterprise Size: SME Growth Challenges Large Enterprises’ Dominance

Large enterprises commanded 71.55% of the OBGYN EHR market share in 2025, owing to deep IT budgets and bespoke integration capacity. They pursue full-suite deployments that embed obstetrics inside network-wide platforms, ensuring unified patient records across inpatient and outpatient touchpoints. Yet, small and medium enterprises are projected to grow at 9.7% CAGR as cloud subscriptions remove hefty hardware outlays and deliver pre-configured templates.

Specialty vendors emphasize rapid go-live programs under 90 days, templated order sets, and concierge onboarding, aligning with limited SME staffing. Satisfaction scores reaching higher scores for focused platforms underscore how tailored workflows trump generic modules in lean practices. Consequently, the OBGYN EHR market sees democratization, where feature parity becomes feasible for clinics with fewer than five physicians.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospital Leadership Faces Clinic Competition

Hospitals accounted for 46.95% of the OBGYN EHR market share in 2025 because high-risk pregnancies and surgical deliveries require OR, pharmacy, and blood-bank connectivity. Massive inpatient datasets also fuel AI algorithms that predict maternal hemorrhage or neonatal distress, sustaining demand for enterprise-scale systems. Clinics and physician offices, however, lead growth at 9.5% CAGR as payers steer routine prenatal services to lower-cost sites and as wearable integration supports home-based monitoring.

Ambulatory surgical centers and freestanding maternity centers seek EHR modules that accommodate birthing-suite workflows and newborn registration without bloated acute-care functionality. Interoperability with hospital systems remains critical for emergency transfer scenarios, driving the OBGYN EHR market toward shared care-team communication tools and standardized referral summaries.

Geography Analysis

North America retained the most prominent regional position with 41.60% of the OBGYN EHR market share in 2025 and a 8.9% CAGR outlook till 2031. U.S. federal quality-reporting mandates, combined with payer incentives for maternal-safety bundles, continue to spur platform replacements. Canada invests in interoperable maternity records through provincial digital-health programmes, while Mexico’s private hospitals adopt specialty modules to differentiate obstetric service lines.

Asia-Pacific is the growth frontrunner with an 11.22% CAGR to 2031. Government-led digital-health blueprints in India, China, and Indonesia prioritized maternal mortality reduction, allocating grants for cloud EHR rollouts in rural antenatal clinics. Rising middle-class demand for premium birthing experiences fuels private-hospital investments in AI-enabled monitoring and tele-obstetric outreach.

Europe advances at 9.25% CAGR, underpinned by eHealth expansion funds and EU-wide interoperability targets. GDPR compliance shapes vendor selection, privileging offerings with native consent management and data-minimization features. Local champions such as Dedalus win tenders by localizing prenatal screening forms and integrating national registries. Middle East & Africa and South America chart 10.66% and 10.41% CAGRs respectively, building from low installed bases. Gulf states pilot cloud platforms across public maternity hospitals, while Brazil’s SUS modernization programme mandates electronic prenatal cards. Donor-funded projects in Kenya and Ghana deploy mobile EHRs to remote health posts, illustrating leap-frog adoption that bypasses legacy servers. The varied maturity levels push vendors to offer modular, language-localized OBGYN EHR market solutions.

Competitive Landscape

Market Concentration

Epic Systems deepened its leadership by adding 176 hospitals in 2024, translating cross-setting continuity and AI investments into superior clinical adoption. Its embedded decision-support tools drive physician loyalty and create switching barriers. Oracle Health lost 74 hospitals amid protracted Cerner integration work, pivoting toward voice-driven AI to regain differentiation but facing execution hurdles.

Specialty-first vendors such as ModMed thrive by aligning every screen with OB workflows, winning top user rankings for ease of use and client support. Their cloud-native cores let updates ship weekly, keeping pace with guideline changes. Ambience Healthcare illustrates a partner-eco-system route, embedding ambient documentation inside athenahealth installs to lift note accuracy and coding completeness across 100 specialties.

Investment in women’s-health startups accelerates product innovation on the periphery. Midi Health secured USD 14 million to extend virtual midlife care into EHR worklists, and Tinto integrates postpartum mental-health assessments within discharge templates. The OBGYN EHR market therefore balances incumbent scale advantages against agile niche entrants that command clinician mind-share through hyper-specialization and consumer-style usability.

OBGYN EHR Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Epic Systems unveiled a healthcare-specific ERP suite spanning workforce and supply-chain modules, aiming to cross-sell into its existing OBGYN client base.

- January 2025: Ambience Healthcare joined athenahealth’s Marketplace Program to deliver AI-assisted documentation and care-coordination across 100 specialties.

- November 2024: CMS finalized the CY 2025 Hospital Outpatient Prospective Payment System rule, embedding new obstetrical safety standards that hinge on automated EHR quality reporting.

- April 2024: The U.S. Department of Health and Human Services issued final HIPAA amendments strengthening privacy protections for reproductive-health information.

Table of Contents for OBGYN EHR Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Demand for Specialty-Specific EHRs Under Value-Based Care

- 4.2.2Increasing Adoption of Cloud Deployment for Remote Prenatal Care

- 4.2.3Regulatory Incentives For Maternal-Health Data Interoperability

- 4.2.4AI-Driven Predictive Analytics for High-Risk Pregnancies

- 4.2.5Expansion of Tele-Obstetric Reimbursement Frameworks

- 4.2.6Investment Surge in Women's Digital-Health Start-Ups Integrating with EHRs

- 4.3Market Restraints

- 4.3.1High Implementation Costs & Delayed ROI

- 4.3.2Data-Privacy & Cybersecurity Concerns Around Reproductive Data

- 4.3.3Fragmented Prenatal-Device Integration Standards

- 4.3.4Political Restrictions on Reproductive-Health Data Sharing

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Deployment Mode

- 5.1.1Client-Server-Based

- 5.1.2Cloud-Based

- 5.2By Application

- 5.2.1Billing

- 5.2.2Clinical Documentation

- 5.2.3Scheduling

- 5.2.4Workflow Management

- 5.2.5Other Applications

- 5.3By Enterprise Size

- 5.3.1Large Enterprises

- 5.3.2SMEs

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Clinics & Physician Offices

- 5.4.3Ambulatory Surgical Centers

- 5.4.4Maternity Centers

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1AdvancedMD Inc.

- 6.4.2Athenahealth Inc.

- 6.4.3ChartLogic Inc.

- 6.4.4CompuGroup Medical SE & Co. KGaA

- 6.4.5Computer Programs and Systems, Inc.

- 6.4.6CureMD Healthcare

- 6.4.7DrChrono Inc.

- 6.4.8eClinicalWorks LLC

- 6.4.9Epic Systems Corporation

- 6.4.10Greenway Health LLC

- 6.4.11Medical Information Technology, Inc.

- 6.4.12Modernizing Medicine Inc.

- 6.4.13N. Harris Computer Corporation

- 6.4.14NextGen Healthcare, Inc.

- 6.4.15Oracle Corporation

- 6.4.16Tebra Technologies, Inc

- 6.4.17Veradigm Inc.

- 6.4.18WRS Health

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global OBGYN EHR Market Report Scope

As per the scope of the report, OBGYN EHR software is electronic health record software specifically designed for obstetrics and gynecology practices to streamline patient management, record-keeping, and billing processes. This software allows healthcare providers to access patient information easily and efficiently, improving overall patient care and workflow.

The OBGYN electronic medical records (EHR) market is segmented by component, application, and geography. By component, the market is segmented into client server-based EHR and cloud-based EHR. By application, the market is segmented into scheduling, billing, clinical documentation, workflow management, and other applications (patient engagement and reporting dashboards). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across the major regions globally. The report offers market sizes and forecasts in value (USD) for the above segments.