Oat Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.68 Billion |

| Market Size (2031) | USD 11.34 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oat Ingredients Market Analysis by Mordor Intelligence

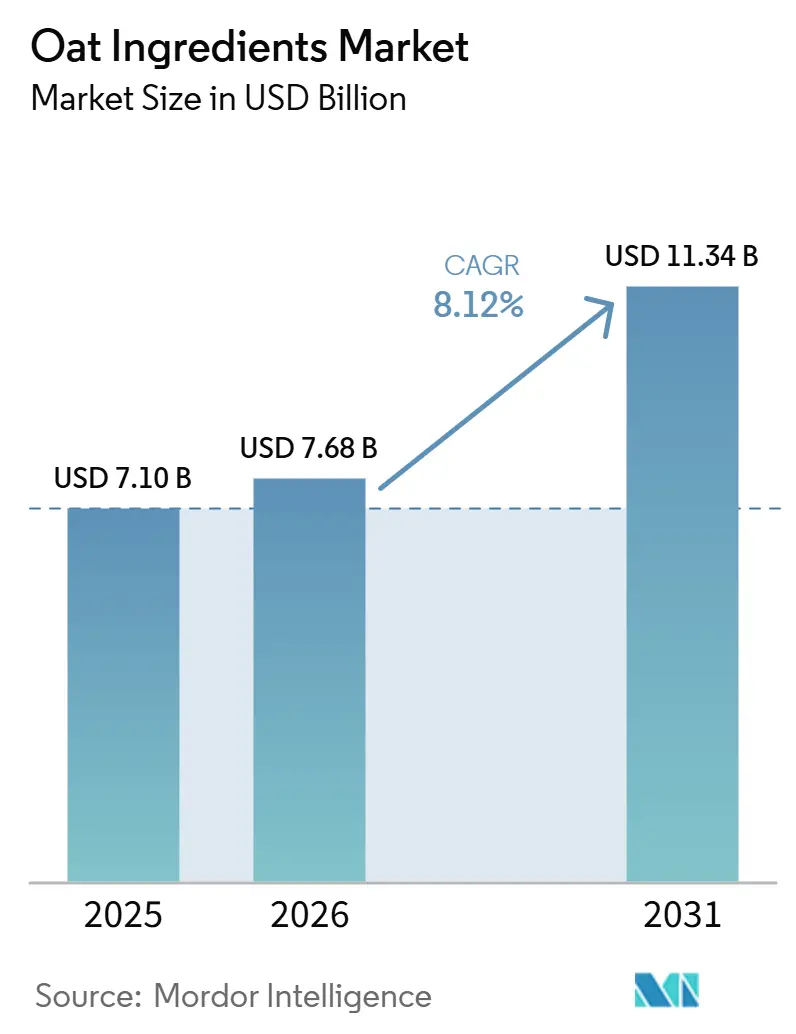

The oat ingredients market size is expected to grow from USD 7.10 billion in 2025 to USD 7.68 billion in 2026 and is forecast to reach USD 11.34 billion by 2031 at 8.12% CAGR over 2026-2031. This growth is driven by the rising popularity of plant-based diets, regulatory approvals for β-glucan's heart-health benefits, and advancements in enzymatic fractionation technology, which improve protein extraction efficiency. Major investments, such as PepsiCo’s establishment of a 160,000-ton Quaker plant in China, reflect the market's long-term growth potential. However, the market faces short-term challenges, including limited oat supplies from Canada and a newly imposed 25% tariff in the United States, which are contributing to cost volatility. Despite these obstacles, ongoing research and development efforts, coupled with premium product positioning, are expanding the use of oat ingredients in beverages, bakery products, and nutraceuticals. Furthermore, the growing focus on sustainability and the increasing demand for clean-label products are supporting attractive profit margins, particularly for organic and specialty oat fractions that command higher prices.

Key Report Takeaways

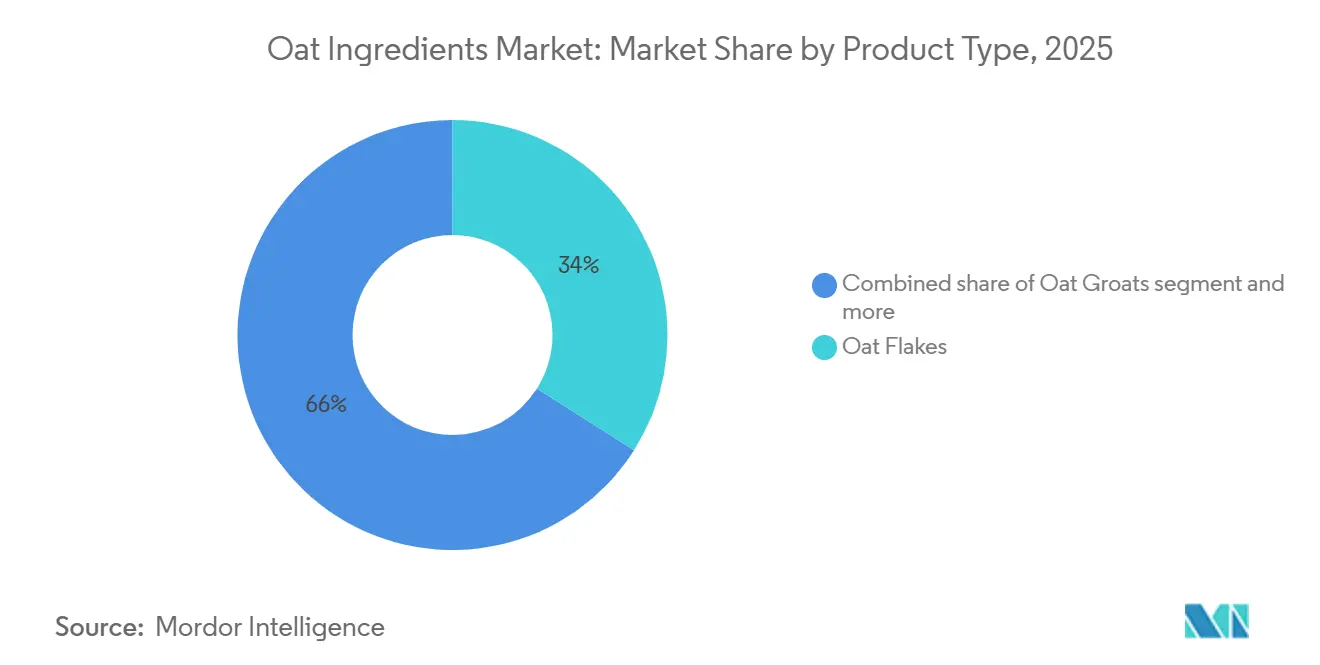

- By product type, oat flakes led with 33.98% of the oat ingredients market share in 2025, and oat protein is forecast to expand at a 12.05% CAGR through 2031.

- By nature, conventional formats held 82.74% of the oat ingredients market size in 2025, while organic oats posted the fastest growth at a 10.78% CAGR through 2031.

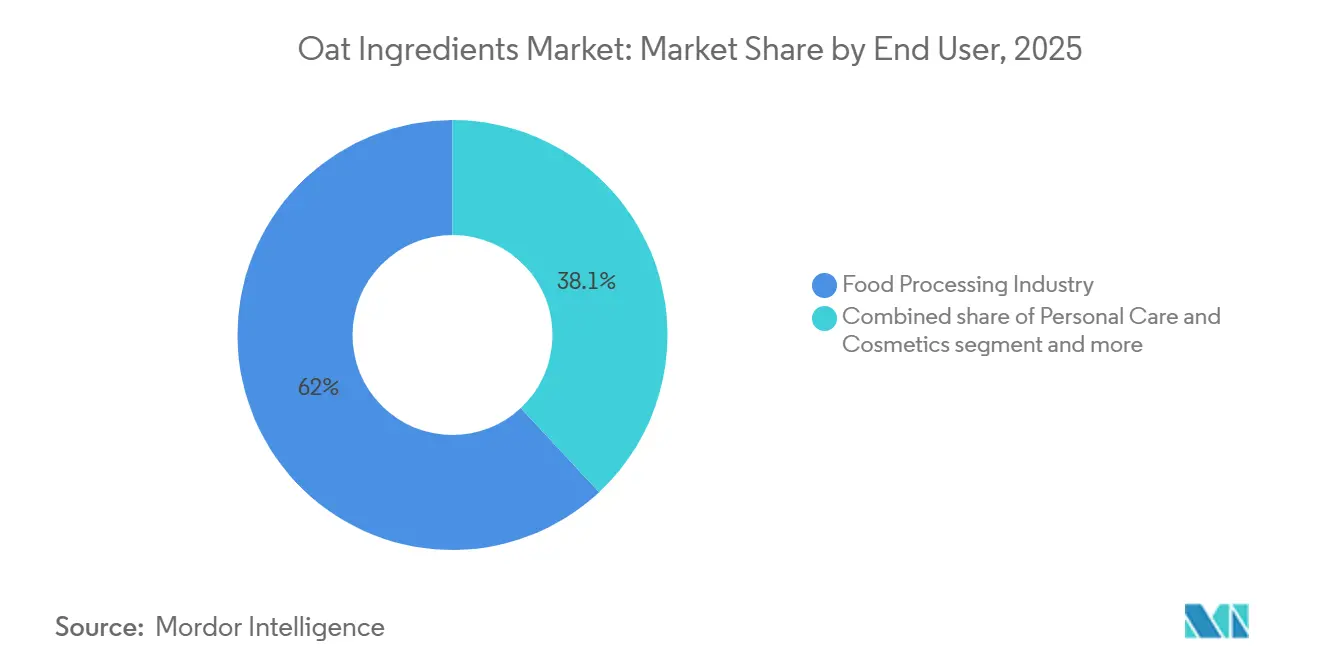

- By end-user, food processing accounted for 61.95% of revenue in 2025, and nutraceuticals are projected to grow at a 11.61% CAGR through 2031.

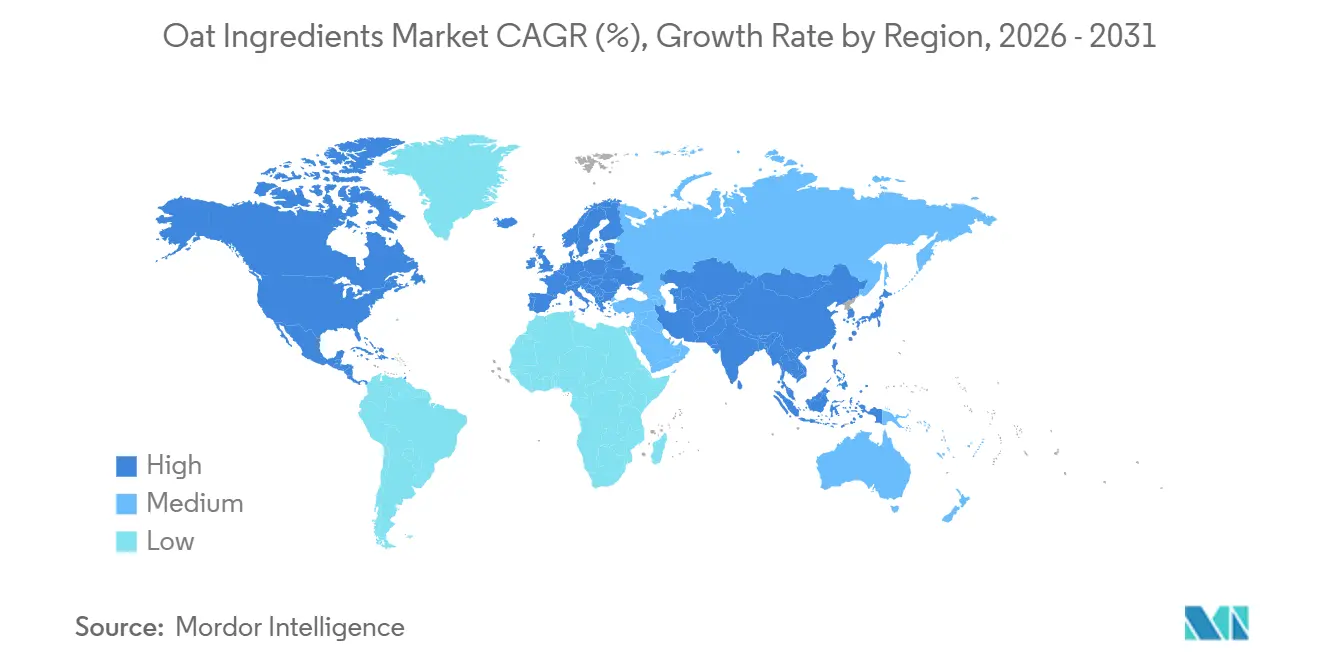

- By geography, Europe accounted for 31.88% of global revenue in 2025, and Asia-Pacific is advancing at an 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oat Ingredients Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing popularity of oat-based foods and beverages | +2.1% | Global, with strongest growth in Asia-Pacific and North America | Medium term (2-4 years) |

| Plant-based and vegan diet adoption | +1.8% | North America and Europe leading, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Increasing demand for sustainable and clean-label products | +1.5% | Europe and North America core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Growing consumer awareness of β-glucan heart-health claims | +1.3% | Global, with regulatory backing in United States, Europe, and Canada | Short term (≤ 2 years) |

| Clean label and allergen-free positioning | +1.0% | North America and Europe primarily, emerging in Asia-Pacific | Medium term (2-4 years) |

| Technological advances in oat processing and fractionation | +0.8% | Global, with innovation centers in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of oat-based foods and beverages

Consumers are increasingly shifting towards functional foods that offer both nutritional benefits and convenience, driving the popularity of oat-based products. In the United States, oat milk sales have experienced significant growth, directly boosting the demand for oat crops. This trend is not confined to beverages; it has expanded into innovative solutions like Milkadamia's Flat Pack Oat Milk, which reduces packaging waste by 94% using proprietary 2D-printing technology. Additionally, advancements in enzymatic processing are supporting this growth. For example, Novozymes' Vertera Oat biosolutions help manufacturers achieve optimal protein levels and sweetness profiles while simplifying ingredient lists. Companies are also reformulating their products to meet this rising demand. Unilever, for instance, has replaced nuts and seeds with oats in Ben & Jerry's dairy-free ice cream, as reported by Food Navigator. The growing variety of oat-based products across different categories highlights a strong and sustained growth trend that extends well beyond traditional breakfast items, supporting expansion in the broader.

Plant-based and vegan diet adoption

The plant-based protein market is projected to grow significantly by 2030, creating substantial opportunities for oat ingredients. This growth is supported by the rising adoption of meat-free diets, particularly in emerging markets. According to Vegconomist, among consumers aged 18–64 surveyed across various countries between 2023 and 2024, 4 out of 10 people in India follow a meat-free diet, highlighting the country's potential for plant-based products [1]Source: Vegconomist, "India Leads the World in Meat-Free Diets, New Statista Survey Reveals", vegconomist.com. Oats are increasingly favored for their nutritional benefits, particularly their amino acid profile. For instance, Oat Bran Concentrates contain a protein content of 21%, considerably higher than the 14% found in regular oat flakes. As the market shifts toward diversifying protein sources, oats are emerging as a strong alternative alongside lentils and chickpeas, and are often preferred over soy and pea proteins. Unlike many plant-based products that focus on mimicking meat, oat-based products emphasize complete nutrition, appealing to health-conscious consumers seeking natural, plant-based options. This growing preference for healthier dietary choices is driving demand for oats as an ingredient in the plant-based protein market.

Increasing demand for sustainable and clean-label products

Consumers are increasingly prioritizing sustainability in their purchasing decisions, driving demand for eco-friendly food products. This trend positions oat ingredients, which have a naturally low environmental impact, as a competitive option in the market. Younger consumers are willing to pay a premium for such products, with Gen Z and Millennials paying 20–30% more for products carrying claims such as organic, natural, high-protein, and no artificial ingredients [2]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. Irish oat production illustrates this advantage, achieving net carbon footprints as low as 38 kg CO₂ per ton through sustainable farming practices such as cover cropping and straw incorporation. Companies are responding to this shift to strengthen their market presence. For instance, PureOaty emphasizes its low carbon footprint across its breakfast range, differentiating itself from conventional alternatives. Similarly, Oatly has committed to reducing emissions by 89% by 2050. The growing demand for sustainable and clean-label products presents brands with opportunities to command premium pricing, allowing them to meet evolving consumer preferences while maintaining higher profit margins.

Growing consumer awareness of β-glucan heart-health claims

The FDA's recognition that consuming 3 grams of β-glucan daily can help reduce the risk of coronary heart disease, when included in a diet low in saturated fat and cholesterol, provides a strong foundation for market growth. This regulatory approval allows manufacturers to promote specific health claims, giving oat-based ingredients a competitive edge over other plant-based options[3]Source: Code of Federal Regulations Health Claims: Soluble fiber from certain foods and risk of coronary heart disease, "ecfr.gov. Additionally, approvals from Health Canada, the FDA, and EFSA for β-glucan's cholesterol-lowering benefits open up global opportunities for these enriched products. Beyond cardiovascular health, studies have shown that β-glucan can effectively regulate blood glucose levels and support the immune system. To further drive demand, ingredient suppliers and product manufacturers are actively educating consumers about these health benefits. This increased awareness not only encourages informed purchasing decisions but also supports premium pricing strategies across the value chain, enhancing the overall market potential for β-glucan-enriched products.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price volatility of raw oats | -1.2% | Global, with acute impact in North America due to Canadian supply dependence | Short term (≤ 2 years) |

| Competition from other plant-based ingredients | -0.9% | Global, with intensified competition in North America and Europe | Medium term (2-4 years) |

| Cross-contamination concerns for gluten-free claims | -0.7% | North America and Europe primarily, emerging regulatory scrutiny | Medium term (2-4 years) |

| Tariff disputes disrupting north-american trade flows | -0.5% | North America specifically, with spillover effects globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price volatility of raw oats

Canadian oat stocks are at historically low levels, highlighting significant supply chain vulnerabilities caused by production instability. These challenges have led to increased ingredient prices and limited availability, creating hurdles for the market. Over the past few years, extreme weather conditions and shifts in planting decisions have caused unpredictable variations in oat harvests, making it difficult for food manufacturers to maintain a steady supply. Despite their high nutritional value, oats remain undervalued in the market. The current pricing structure does not fully account for their nutritional benefits, with 77% of oats used for commercial food purposes and only 23% allocated for feed. Oat futures are currently trading at USD 3.09 per bushel, with a 1% decline reflecting persistent market uncertainty. This situation has forced processors to explore alternative sourcing strategies or face rising input costs that squeeze profit margins.

Cross-contamination concerns for gluten-free claims

Gluten contamination in oat products presents critical regulatory and liability concerns, which could lead to changes in labeling standards and market strategies. Testing of Trader Joe's Gluten-Free Rolled Oats revealed contamination levels ranging from below 5 ppm to 120 ppm across various lots, exposing gaps in cross-contact control during production. In the United States, there is growing pressure to introduce mandatory gluten labeling for oats, aligning with regulations already adopted in 87 other countries. Such measures could significantly increase compliance costs and restrict market access for producers who lack gluten-free certification. Implementing the Purity Protocol, a stricter standard for gluten-free oats, requires dedicated supply chains and advanced testing systems. This approach tends to favor larger, vertically integrated processors that can absorb the higher costs, while smaller regional producers may face challenges due to limited resources and infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flakes Dominate While Protein Accelerates

In 2025, oat flakes held the largest market share at 33.98%, highlighting their strong presence in traditional breakfast foods and industrial food processing. Their adaptability makes them essential ingredients in products like cereals, granola bars, and baked goods, ensuring consistent quality and functionality. This segment benefits from well-established supply chains and advanced processing systems that enable efficient and cost-effective large-scale production. For instance, Bühler Group's integrated oat production lines showcase advanced technology, managing the entire process from cleaning and grading to kilning and flaking with high efficiency and quality. Leading food manufacturers prefer oat flakes due to their reliable performance and widespread consumer acceptance, which drives steady demand across various product categories.

Oat protein is the fastest-growing segment, with a projected CAGR of 12.05% through 2031. This growth is driven by increasing scientific evidence supporting its cardiovascular benefits and the rising popularity of plant-based protein alternatives. Research from the University of Manitoba confirms that oat protein can improve heart health, lower bad cholesterol, enhance cardiac function in obese individuals, reduce blood pressure, and prevent heart-related issues in people with hypertension. Companies like Bob's Red Mill are innovating in this space, introducing high-protein oats to meet the growing demand for clean-label protein products. Oat protein stands out due to its superior amino acid profile compared to other grains, and its growth reflects a broader market trend favoring functional and health-focused ingredients over standard commodity products.

By Nature: Conventional Scale Versus Organic Premiumization

In 2025, conventional oats commanded a dominant 82.74% market share, bolstered by established supply chains, competitive pricing, and their ubiquitous presence in mainstream food applications. These oats leverage economies of scale in both production and processing, allowing manufacturers to cater to the high-volume demands of major food processors and retail outlets. Highlighting the scale advantages of the conventional segment, with Canada, as the world's leading oat producer with 3.4 million metric tonnes in 2024, as reported by the US Department of Agriculture. The conventional segment underpins mass-market staples, from breakfast cereals and snack bars to industrial food ingredients, prioritizing cost efficiency over premium branding.

Organic oats are on an upward trajectory, boasting an 10.78% CAGR through 2031. This surge is fueled by premium positioning and consumers' readiness to invest in perceived health and environmental advantages. Taking the lead, Finnish organic oats, particularly from Raisio Food Solutions, spotlight this movement. They emphasize stringent quality controls, reduced pesticide usage, and carbon-neutral production, resonating with eco-conscious consumers. Further underscoring this trend, Alpro has made headlines with a significant investment in the UK, pivoting to 100% British organic oats. This move not only underscores their dedication to local sourcing but also aligns with the industry's shift towards organic positioning and supply chain transparency. The organic segment's robust growth mirrors a broader industry trend: as consumers increasingly prioritize quality and sustainability, they're willing to pay a premium.

By End-User: Food Processing Leads While Nutraceuticals Surge

In 2025, the food processing industry dominated the market with a 61.95% share, driven by its wide range of applications. These include bakery and confectionery, breakfast cereals, dairy alternatives, snacks and bars, and beverages, all of which utilize oat ingredients for their functional benefits. Oats are valued in food manufacturing for their ability to improve texture, act as a binding agent, and enhance nutritional content across various products. Among these applications, the dairy alternatives subsegment is witnessing the fastest growth in oat crop demand, driven by the rising popularity of plant-based products. The food processing industry benefits from strong supply chain networks, standardized quality requirements, and predictable demand trends, which support efficient long-term planning and investment.

The nutraceuticals segment is the fastest-growing, with a projected CAGR of 11.61% through 2031. This growth is fueled by scientific evidence supporting the health benefits of β-glucan and regulatory approvals for health claims in multiple regions. For instance, Ceapro has successfully developed oat β-glucan for anti-aging products that help stimulate collagen production, aid skin repair, and deliver therapeutic effects through deep skin penetration. The nutraceuticals market also capitalizes on premium pricing opportunities, as consumer interest in natural remedies and functional health products continues to grow. This trend highlights a shift in consumer behavior, with increasing awareness of functional ingredients and a willingness to invest in products backed by scientific validation for health benefits.

Geography Analysis

In 2025, Europe held the largest market share at 31.88%, driven by its strong Nordic oat production and advanced processing capabilities that cater to both local and international markets. Countries like Finland, Sweden, and Ireland benefit from favorable climates and sustainable farming practices, enabling them to produce high-quality oats with strong environmental credentials. Finnish organic oats stand out due to strict quality controls, minimal pesticide use, and carbon-neutral production processes, making them highly appealing to premium market segments. Irish oat production is recognized for its sustainability, with a carbon footprint of just 207 kg CO2 equivalent per ton, significantly lower than the 1000 kg CO2/t recorded in warmer regions like Italy and Spain.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 8.92% through 2031. This growth is fueled by innovative product developments and increasing consumer acceptance of plant-based alternatives in urban areas. OATSIDE's rapid growth highlights the region's potential, driven by effective marketing and unique flavor innovations like matcha oat lattes infused with 20mg L-theanine, which offer stress relief and sleep health benefits. PepsiCo's USD 68.6 million investment in 2025 to establish a 160,000-ton Quaker oat facility in China reflects the commitment of global companies to the region's development. The region's expanding middle class, rising health awareness, and interest in functional food innovations further drive growth.

North America remains a key market despite challenges stemming from its reliance on Canadian imports, with over half of U.S. oat consumption sourced from Canada. This dependency exposes the region to trade disruptions, especially after the introduction of a 25% tariff on Canadian cereals in 2025. As a result, U.S. processors are seeking to diversify sourcing or absorb higher costs. Domestic production initiatives are gaining momentum, such as Oatly's partnerships with Midwest farmers to reintroduce oats into crop rotations, promoting both environmental and economic benefits. Meanwhile, South America and the Middle East and Africa are emerging as promising markets, driven by urbanization and growing interest in plant-based alternatives, supported by multinational brand expansion strategies.

Competitive Landscape

The oat ingredient market is moderately consolidated, with numerous small-scale players contributing to its dynamics. Major players are focusing on strategies such as product innovation, market expansion, and acquisitions to capitalize on the limited growth opportunities available. Prominent companies in the market include Lantmännen, Grain Millers, Inc., James Richardson & Sons, Limited (Richardson International), Avena Foods Ltd, and PepsiCo, Inc. (Quaker Oats Company). However, the demand for oat protein faces challenges due to the growing popularity of alternative plant-based proteins like pea and soy. Despite this, leading companies are making significant investments to sustain and grow the market.

Key strategies in the market emphasize vertical integration, sustainability, and technological advancements over price-based competition. For example, Oatly has adopted an asset-light supply chain strategy, which includes closing its Singapore facility to optimize cost structures and improve capacity utilization. This approach reflects how market leaders are enhancing operational efficiency while maintaining their global presence.

New opportunities are emerging in functional applications, such as personal care products, where β-glucan's anti-inflammatory and moisturizing properties provide unique advantages beyond traditional food applications. Technological advancements, particularly in enzymatic processing, are enabling higher protein concentration and improved functional properties. Companies like Novozymes are driving innovation by offering biosolutions that enhance protein levels and simplify ingredient formulations. Additionally, McGill University's patent filings on CRISPR-Cas9 gene editing for oats aim to improve β-glucan content and climate resilience, signaling potential technological breakthroughs that could reshape the market in the future.

Oat Ingredients Industry Leaders

-

Lantmännen

-

Grain Millers, Inc.

-

James Richardson & Sons, Limited (Richardson International)

-

PepsiCo, Inc.

-

Avena Foods Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Standard Process expanded its organic ingredients portfolio with the launch of Royal Ancient Oats Flour under its Royal Lee Organics brand. The product is a certified organic and gluten-free oat flour developed to deliver enhanced nutritional value, supporting metabolic and digestive health. Compared to conventional oat flours, it offers 150% more fiber, 25% fewer net carbohydrates, twice the iron, and ten times more avenanthramides per serving.

- February 2025: Bay State Milling has expanded its oats portfolio with the launch of PurelySown purity protocol gluten-free oats. According to the company, PurelySown Purity Protocol Gluten-Free Oats are available as conventional, organic, and Regenerative Organic Certified, going above and beyond organic standards. These oats also come in multiple forms, including groats, flakes, and rolled.

- October 2024: Flahavan's has expanded its product lineup with the relaunch of its oat bran. This oat bran is high in protein and fiber, and it contains beta-glucan, which helps lower cholesterol. Made with 100% oat bran, it will be available in a smaller 600g bag due to operational constraints, according to the brand.

Global Oat Ingredients Market Report Scope

| Oat Flour |

| Oat Groats |

| Oat Bran |

| Oat Flakes |

| Oat Starch |

| Oat Protein |

| Oat Beta-Glucan |

| Others |

| Conventional |

| Organic |

| Food Processing Industry | Bakery and Confectionery |

| Breakfast Cereals | |

| Dairy and Dairy Alternatives | |

| Snacks and Bars | |

| Beverages | |

| Others | |

| Nutraceuticals | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Others | |

| HoReCa |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Oat Flour | |

| Oat Groats | ||

| Oat Bran | ||

| Oat Flakes | ||

| Oat Starch | ||

| Oat Protein | ||

| Oat Beta-Glucan | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By End-User | Food Processing Industry | Bakery and Confectionery |

| Breakfast Cereals | ||

| Dairy and Dairy Alternatives | ||

| Snacks and Bars | ||

| Beverages | ||

| Others | ||

| Nutraceuticals | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Others | ||

| HoReCa | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of oat ingredients market?

The oat ingredients market stands at USD 7.68 billion in 2026 and is on course to reach USD 11.34 billion by 2031.

Which region is growing the fastest?

Asia-Pacific is expanding at a 8.92% CAGR as local innovators blend traditional flavors with functional oat bases.

Why is oat protein gaining traction?

Clinical research supports cardiovascular benefits, and enzymatic extraction delivers concentrates up to 21% protein, attracting sports-nutrition and dairy-alternative brands.

What drives premium pricing for organic oats?

Organic certification, lower pesticide use, and carbon-neutral farming allow producers to charge double-digit premiums while meeting rising clean-label demand.

Page last updated on: