Nylon Cable Ties Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

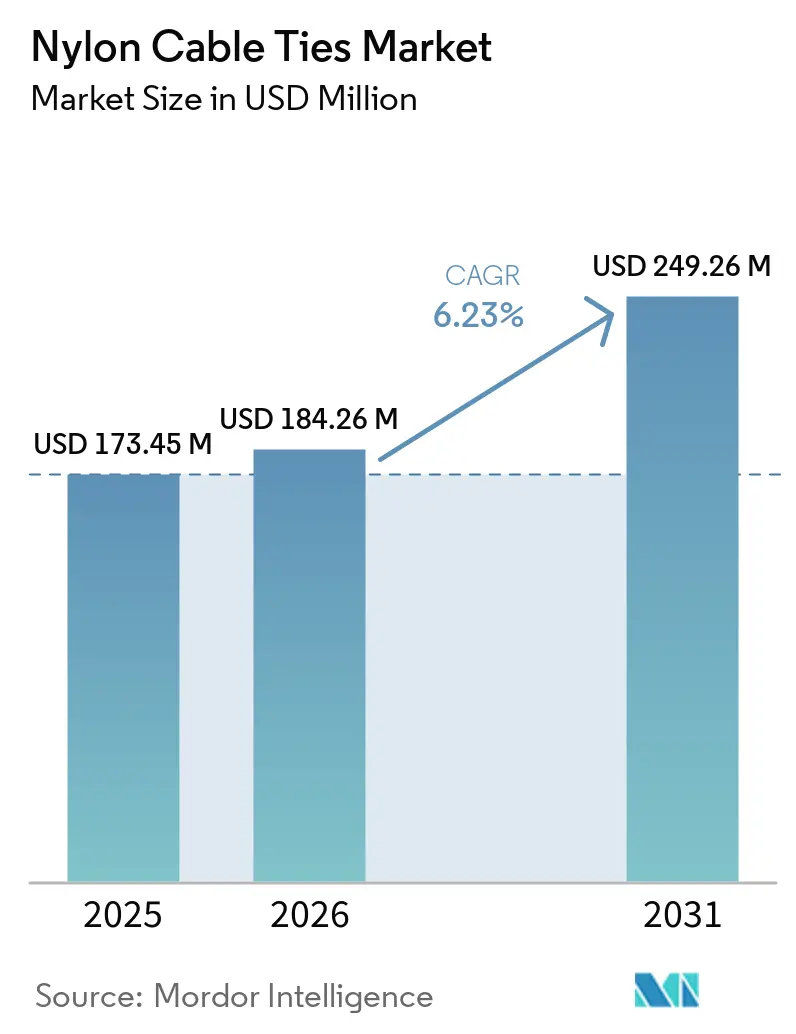

| Market Size (2026) | USD 184.26 Million |

| Market Size (2031) | USD 249.26 Million |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

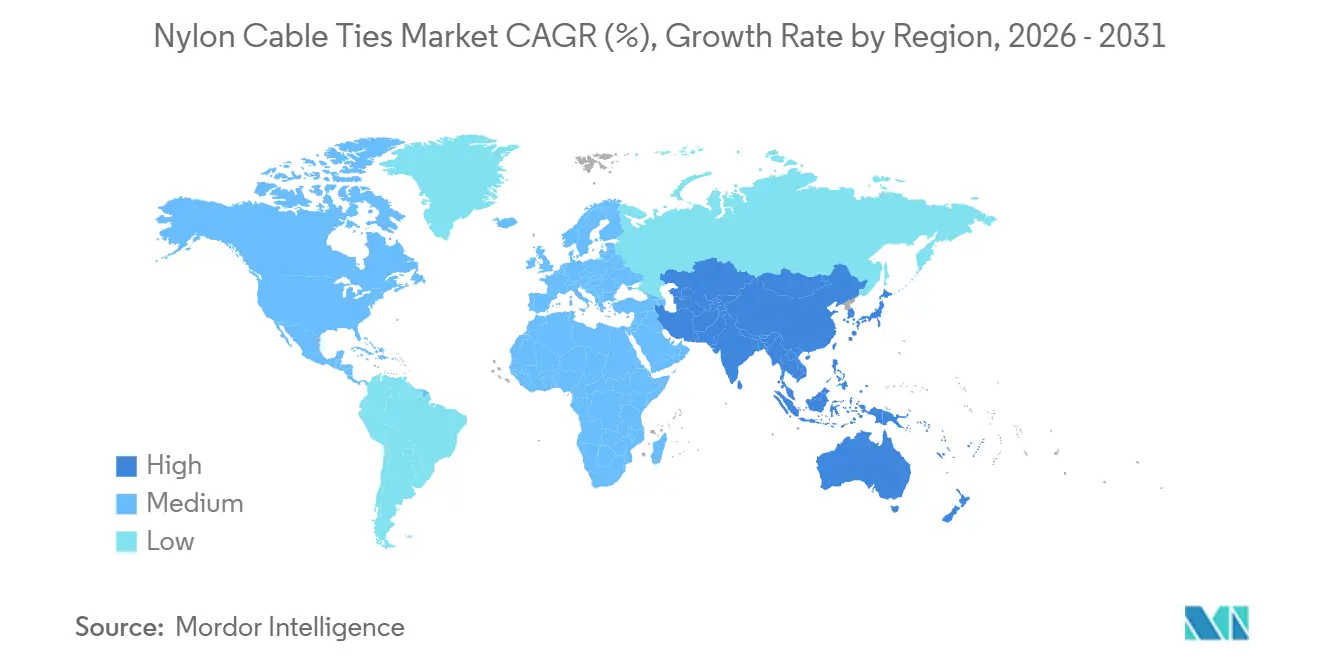

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

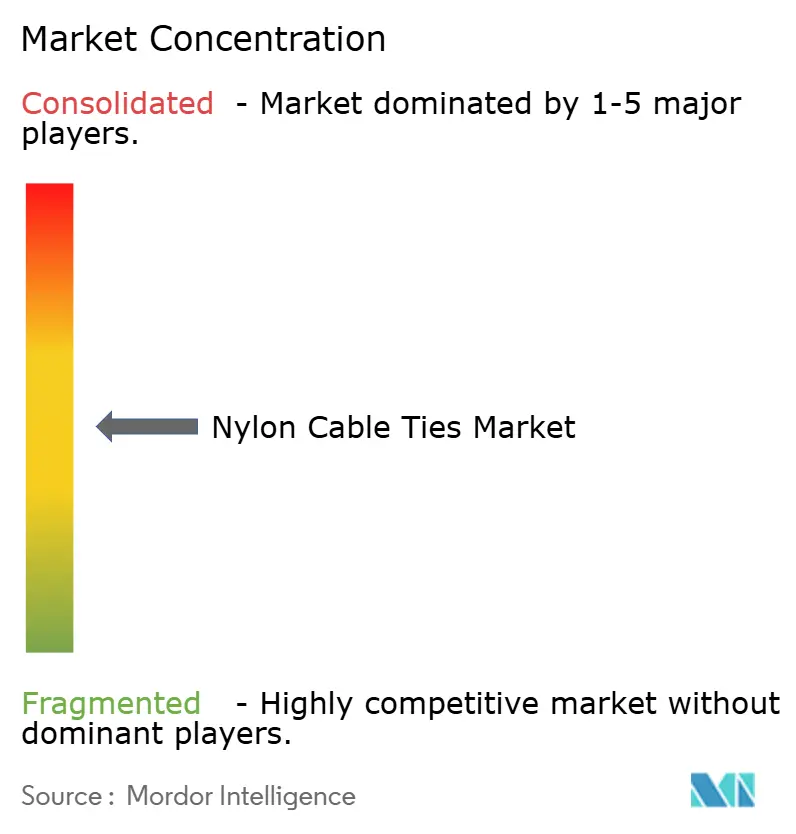

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nylon Cable Ties Market Analysis by Mordor Intelligence

The Nylon Cable Ties Market size is expected to grow from USD 173.45 million in 2025 to USD 184.26 million in 2026 and is forecast to reach USD 249.26 million by 2031 at 6.23% CAGR over 2026-2031. Product demand is shifting from legacy residential construction toward electrification programs, renewable-energy installations, and hyperscale data centers, each of which specifies higher-performance ties that withstand heat, UV radiation, and vibration. Automotive electrification lifts unit consumption per vehicle, while data-center operators drive adoption of Radio Frequency Identification (RFID)-enabled variants that streamline maintenance and asset tracking. Feedstock integration is becoming a central competitive lever as caprolactam and adipic acid price swings compress converter margins in Europe and North America. Channel dynamics are also evolving, with e-commerce platforms capturing small-order volumes that once flowed through regional distributors.

Key Report Takeaways

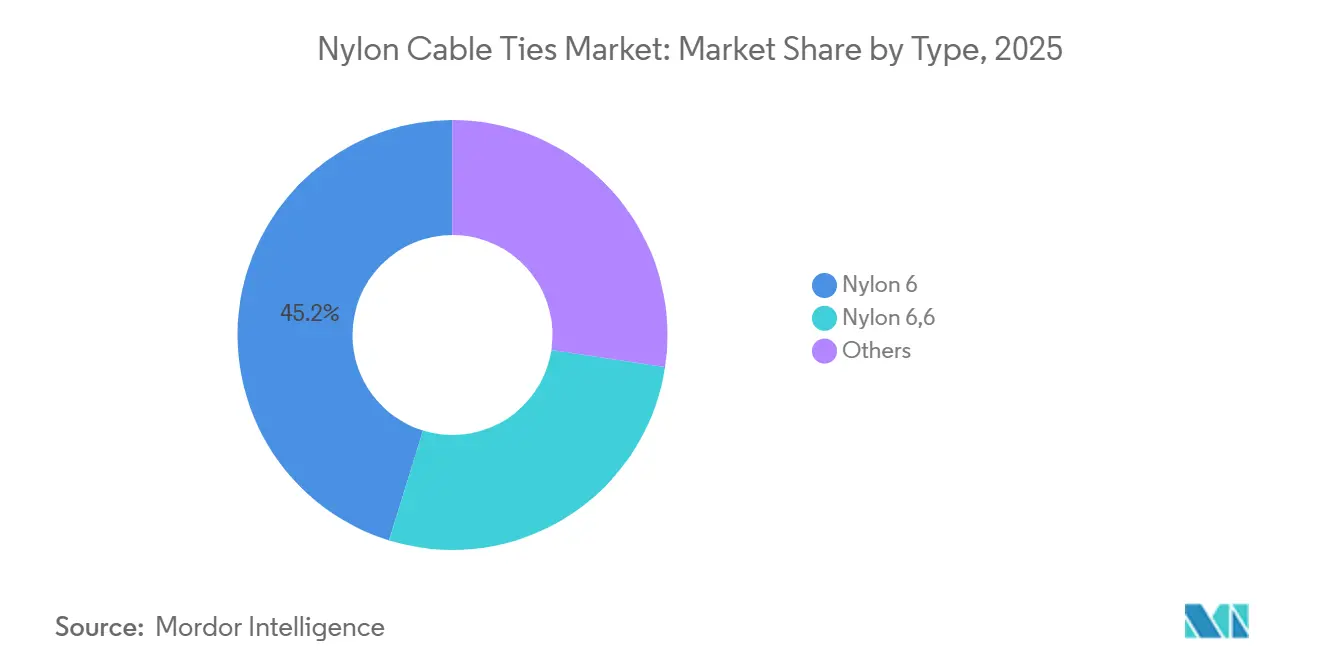

- By type, Nylon 6 held 45.23% of the nylon cable ties market share in 2025; Nylon 6,6 is projected to post the fastest 6.97% CAGR through 2031.

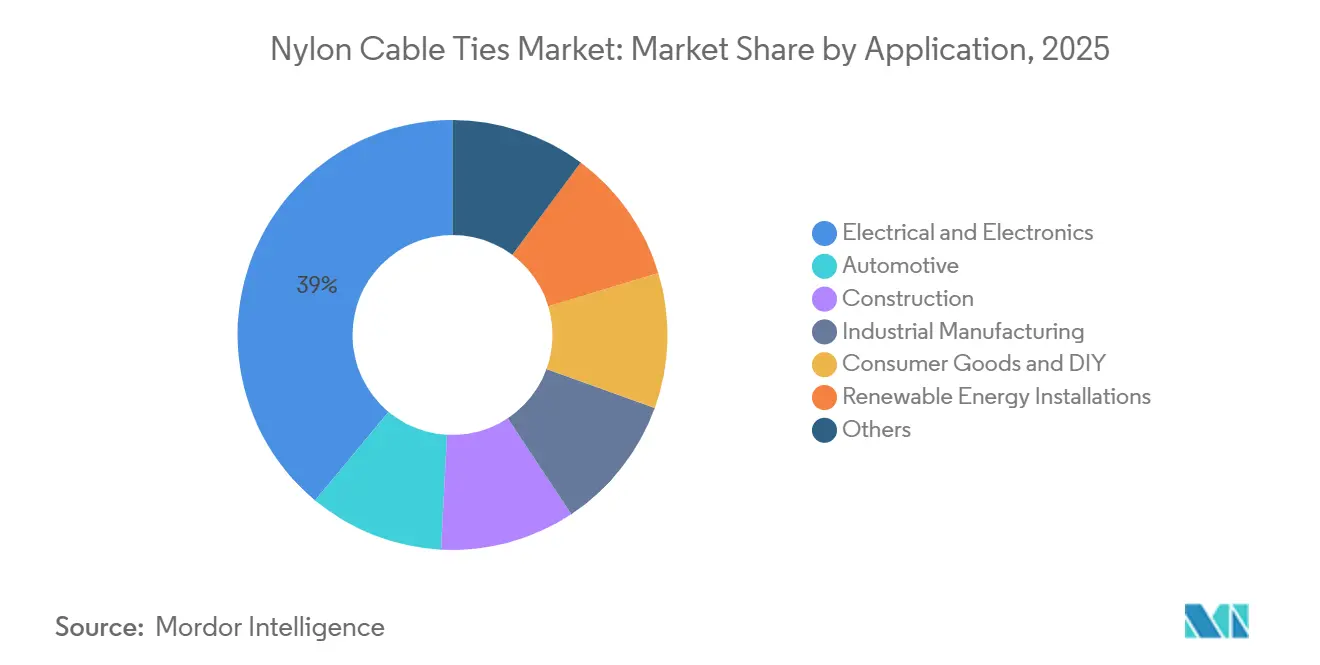

- By application, Electrical and Electronics accounted for a 38.96% share of the nylon cable ties market size in 2025, while Automotive is forecast to grow at a 6.76% CAGR to 2031.

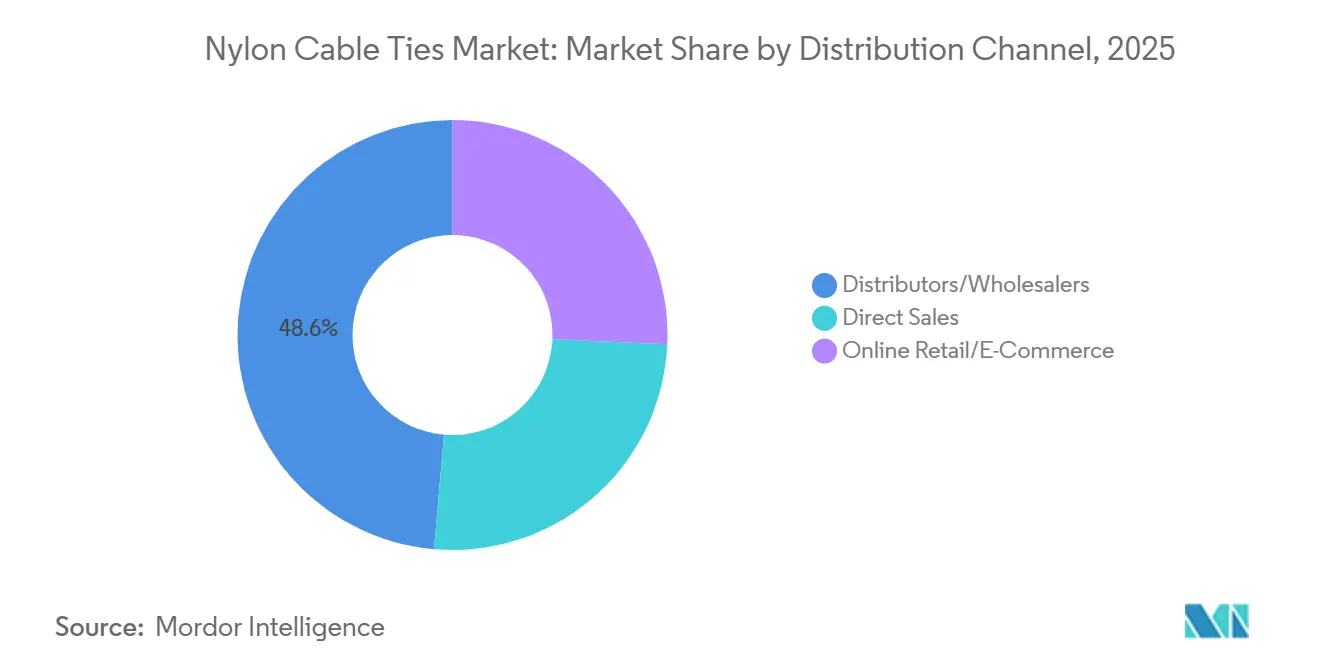

- By distribution channel, Distributors/Wholesalers led with 48.63% revenue share in 2025; Online Retail/E-Commerce is advancing at a 5.45% CAGR during the forecast period (2026-2031).

- By geography, North America captured 25.32% of 2025 revenue, whereas Asia-Pacific is on track for the highest 7.32% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nylon Cable Ties Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global construction and infrastructure pipelines | +1.2% | Asia-Pacific, Middle East, North America | Medium term (2-4 years) |

| Rising uptake in electric-vehicle wire-harness assemblies | +1.8% | Global | Long term (≥ 4 years) |

| Cost-effective and easy-install versus metallic fasteners | +0.9% | Global | Short term (≤ 2 years) |

| Offshore wind and solar farms need UV-resistant ties | +1.1% | Europe, Asia-Pacific coasts, North America offshore | Medium term (2-4 years) |

| Adoption of RFID-enabled smart ties for predictive maintenance | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Construction and Infrastructure Pipelines

Megaprojects across Asia-Pacific and the Middle East continue to specify large volumes of ties for electrical runs in transit systems, commercial towers, and utility grids. India’s National Infrastructure Pipeline targets USD 1.4 trillion of spend through 2025, creating sustained pull for commodity grades while rewarding suppliers that can stage inventory near job sites. China’s Belt and Road contractors procure ties for export builds in Southeast Asia and Africa, extending price competition beyond domestic markets. Demand often arrives in surges, forcing manufacturers to balance overtime production with the risk of post-project inventory corrections. Distributors respond by shortening purchase commitments, which raises working-capital requirements for converters. The net effect is a structurally higher safety-stock level at plants serving project business.

Rising Uptake in Electric Vehicle Wire-Harness Assemblies

Battery-electric cars require 30%-50% more ties than internal-combustion models because high-voltage cabling, sensor looms, and coolant lines occupy greater real estate. Harnesses run at 600 V to 1,000 V and heat components beyond 150°C, so automakers insist on Nylon 6,6 ties that pass ISO 19642 thermal-aging tests up to 12,000 hours[1]ISO, “ISO 19642 Road Vehicles – Electrical Wiring Harnesses,” iso.org. HellermannTyton’s swivel mount, introduced in February 2025, rotates 360 degrees, easing routing around moving parts without overstressing the tie. Tier-1 harness makers such as Yazaki and Aptiv consolidate supplier lists to ensure traceability and RoHS compliance, which tightens entry conditions for regional converters. As global EV output scales, tie suppliers able to certify materials for continuous 175°C exposure enjoy premium pricing and multiyear volume contracts.

Cost-Effective and Easy-Install Versus Metallic Fasteners

A two-gram Nylon 6 tie often replaces a 15-gram stainless clamp, trimming both material cost and assembly time in consumer electronics, DIY (Do-It-Yourself) projects, and light industrial builds. Tool-free installation and the absence of threaded hardware eliminate separate inventory lines, a benefit that resonates with e-commerce buyers who seek quick replenishment. In heavy-duty zones, stainless ties rated above 7,000 N remain essential, narrowing the cost gap versus engineered nylons. Even so, labor savings still tilt many users to plastic, especially when installers operate on ladders or within confined panels, where one-handed operation reduces fatigue. The resulting hybrid spec, plastic indoors, metal outdoors, supports SKU diversification across performance tiers.

Offshore Wind and Solar Farms Need UV/Weather-Resistant Ties

Standard nylon degrades after 18-24 months of salt spray and sustained UV exposure, prompting wind-farm and solar-park owners to shift toward coated stainless or UV-stabilized nylon blends. HellermannTyton’s MBT-Series, certified to UL 62275 in September 2025, offers SS316L variants with polyester coating that resists galvanic corrosion against aluminum frames. North Sea and Atlantic-coast wind specs now require DNV approval, favoring suppliers with in-house salt-fog test cells. Premium products fetch up to triple the unit price of commodity grades, yet owners accept the delta because field failures necessitate rope-access technicians and megawatt-hour downtime penalties. The divide between indoor commodity and outdoor engineered ties is therefore widening.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of reusable or alternative fastening systems | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Feedstock price volatility for caprolactam and adipic acid | -1.3% | Global | Medium term (2-4 years) |

| Migration to automated harness-wrapping robots | -0.5% | Automotive hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Reusable Alternative Fastening Systems

Hook-and-loop products such as VELCRO ONE-WRAP capture share in data centers and consumer electronics where cables move often, and landfill costs weigh on purchasing mandates. Operators report 40% lower consumable spending across a three-year refresh cycle, even though reusable ties carry higher upfront prices[2]Velcro Companies, “ONE-WRAP Reusable Cable Ties,” velcro.com. Color coding, adjustability, and the absence of sharp cut tails improve worker ergonomics and equipment safety. Nylon ties retain primacy in high-vibration or high-temperature environments such as under-hood automotive, yet the volume shift toward reusables in light-duty applications trims baseline growth for single-use nylon.

Feedstock Price Volatility for Caprolactam and Adipic Acid

Caprolactam spot prices swung from a 17.7% decline in December 2024 to sequential increases of 2.7%-2.9% across major regions in March 2026 as benzene tracked crude-oil spikes. Adipic acid costs also rose due to new N2O abatement rules affecting European and North American producers. Vertically integrated manufacturers hedge exposure by aligning polymerization and tie molding on the same site, while non-integrated converters face margin squeeze when cost pass-through lags distributor contract cycles. Long-term contracts with automotive OEMs (original equipment manufacturers) provide some buffer, but spot-market buyers see immediate price volatility that complicates project budgeting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Nylon 6,6 Gains on Heat Resistance

Cost-focused builders still favor Nylon 6 for indoor wiring where ambient temperatures stay below 85°C. High-volume SKUs for consumer devices, lighting fixtures, and residential panels keep Nylon 6 in the lead at 45.23% of 2025 revenue. Specialty blends and bio-based formulations occupy a niche but attract research and development spend as brands chase low-carbon materials. Regulatory moves against halogenated flame retardants accelerate the pivot to phosphorus-based systems, raising formulation complexity and rewarding compounders with accredited labs.

Nylon 6,6 accounted for a smaller share than Nylon 6 in 2025, yet is projected to grow at a 6.97% CAGR through 2031. The Nylon cable ties market size for Nylon 6,6 is forecast to climb as under-hood EV temperatures demand continuous service to 175°C. OEM engineering standards such as QC/T 1037 require thermal aging that Nylon 6 often cannot pass without additives, steering specifications toward Nylon 6,6. Recycled grades introduced by HellermannTyton in October 2024 combine circular-economy credentials with tensile strengths up to 535 N, commanding a 10%-15% premium over virgin material.

By Application: Automotive Electrification Drives Fastest Growth

Electrical and Electronics remains the largest slice at 38.96% of 2025 revenue. Data-center expansion in North America and Asia-Pacific underpins demand for RFID-enabled variants that reduce audit labor. Construction, industrial manufacturing, and DIY channels provide resilient baseline orders yet face substitution from reusable hook-and-loop ties in retrofit work. Renewable energy sites, while smaller, post double-digit gains as offshore wind farms specify UL 62275 stainless or UV-stabilized nylons for nacelle and tower cabling.

Automotive wire harnesses are set to advance at a 6.76% CAGR from 2026 to 2031, the fastest among applications. EV programs at Tesla, BYD, and legacy OEMs multiply tie counts because battery packs, inverters, and sensor suites expand wiring volume. The Nylon cable ties market size for automotive applications benefits from mandatory ISO 19642 testing, which keeps low-spec plastics out of qualified supply chains.

By Distribution Channel: E-Commerce Gains on SKU Breadth

Distributors and wholesalers held 48.63% share in 2025, but Online Retail and e-commerce are growing at 5.45% CAGR as maintenance buyers adopt just-in-time replenishment. The Nylon cable ties market share captured online rises because configurator tools help users pick tensile strength, temperature rating, and certification in seconds.

Direct sales stay relevant for automotive harness suppliers and tier-one contract manufacturers that negotiate year-long agreements tied to build schedules. Distributors pivot toward value-added services such as kitting and private labeling to defend margins. Omnichannel strategies emerge, with suppliers allowing buyers to place framework orders electronically and draw from local distributor stock for same-day pickup.

Geography Analysis

North America maintained 25.32% of 2025 revenue owing to data-center construction in Virginia, Texas, and Oregon, plus EV ramps in Michigan and Mexico. Operators increasingly specify RFID-enabled ties for real-time tracking, a niche that local suppliers fill with short lead times. Caprolactam price volatility and Asian import competition squeeze margins, pushing converters toward feedstock integration. Canadian offshore wind pilots call for marine-grade stainless ties that satisfy DNV and UL 62275 rules.

Asia-Pacific leads growth at 7.32% CAGR through 2031, powered by China’s integrated caprolactam capacity and India’s infrastructure push. Chinese converters undercut Western prices on commodity grades, yet domestic brands also move upscale with RFID-ready and UV-resistant lines as export users demand certifications. India’s metro and highway expansions consume bulk packs, but price sensitivity slows adoption of premium formulations. Japan and South Korea favor certified materials for automotive exports, reinforcing regional demand for Nylon 6,6. Southeast Asian nations such as Vietnam attract harness production relocations, supporting local stocking models.

Europe grows more slowly because natural-gas and electricity prices remain elevated post-2022, lifting polymerization costs. Buyers import more Asian resin and semi-finished ties, although stringent sustainability agendas spur interest in post-industrial recycled Nylon 6,6. North Sea wind farms, data centers in Ireland and the Nordics, and German automotive wire harnesses still anchor demand for high-spec grades. South America and Middle East-Africa remain small but gain momentum from Brazilian automation investment and Saudi Arabia’s NEOM project, where UV-stable and high-temperature certifications are mandatory despite tight budgets.

Competitive Landscape

The Nylon Cable Ties market is moderately fragmented. Mergers, backward integration into polymerization, and alliances with chip vendors reshape the landscape. Companies that document cradle-to-gate carbon footprints gain an edge with European and Japanese purchasers. The overall trajectory points to coexistence: commodity demand stays fragmented, while engineered and digital ties consolidate around a handful of certification-rich producers.

Nylon Cable Ties Industry Leaders

HellermannTyton Group

Panduit Corporation

ABB Ltd

3M

HUA WEI INDUSTRIAL CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Samsara Eco launched its first production and development facility in Jerrabomberra, New South Wales, Australia. This facility utilized its proprietary EosEco enzymatic technology on an industrial scale to recycle Nylon 6,6, a key material used in the production of nylon cable ties.

- February 2025: HellermannTyton introduced the Swivel Mount, a 360° rotatable cable-tie mount for applications with moving parts in industrial automation, robotics, and electrical enclosures. The heat-stabilized Polyamide 6.6 (Nylon 6,6) mount reduces cable stress during movement and eliminates drilling for secure mounting on high- and low-energy surfaces.

Global Nylon Cable Ties Market Report Scope

Nylon cable ties (also known as zip ties) are durable, versatile fasteners. Featuring a flexible, geared strap with a self-locking pawl in the head, they create a secure, one-way, high-strength bundle for cables, wires, and miscellaneous items. They are valued for being heat-resistant, insulating, and long-lasting.

The Nylon Cable Ties market is segmented by type, application, distribution channel, and geography. By type, the market is segmented into nylon 6, nylon 6,6, and others. By application, the market is segmented into electrical and electronics, automotive, construction, industrial manufacturing, consumer goods and DIY, renewable energy installations, and others. By distribution channel, the market is segmented into distributors/wholesalers, direct sales, and online retail/e-commerce. The report also covers the market size and forecasts for nylon cable ties in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Nylon 6 |

| Nylon 6,6 |

| Others |

| Electrical and Electronics | Consumer Electronics Wiring |

| Data-centre Cabling | |

| Automotive | ICE Vehicles |

| Electric Vehicles | |

| Construction | Commercial Buildings |

| Residential Buildings | |

| Industrial Manufacturing | |

| Consumer Goods and DIY | |

| Renewable Energy Installations | |

| Others |

| Distributors/Wholesalers |

| Direct Sales |

| Online Retail/E-Commerce |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Type | Nylon 6 | |

| Nylon 6,6 | ||

| Others | ||

| By Application | Electrical and Electronics | Consumer Electronics Wiring |

| Data-centre Cabling | ||

| Automotive | ICE Vehicles | |

| Electric Vehicles | ||

| Construction | Commercial Buildings | |

| Residential Buildings | ||

| Industrial Manufacturing | ||

| Consumer Goods and DIY | ||

| Renewable Energy Installations | ||

| Others | ||

| By Distribution Channel | Distributors/Wholesalers | |

| Direct Sales | ||

| Online Retail/E-Commerce | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Nylon cable ties market?

The market is valued at USD 184.26 million in 2026 and is forecast to reach USD 249.26 million by 2031.

Which material grade is growing fastest in cable ties?

Nylon 6,6 is expanding at 6.97% CAGR through 2031 due to higher heat resistance needed in EVs and renewable-energy gear.

Why are RFID-enabled cable ties gaining traction?

They cut inspection time by enabling non-contact scanning and asset tracking, a crucial feature for data-center and industrial owners facing high downtime costs.

How is e-commerce changing procurement of cable ties?

Online platforms let maintenance buyers order niche SKUs on demand, eroding distributor share and promoting just-in-time inventory models.

Page last updated on: