NVH Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

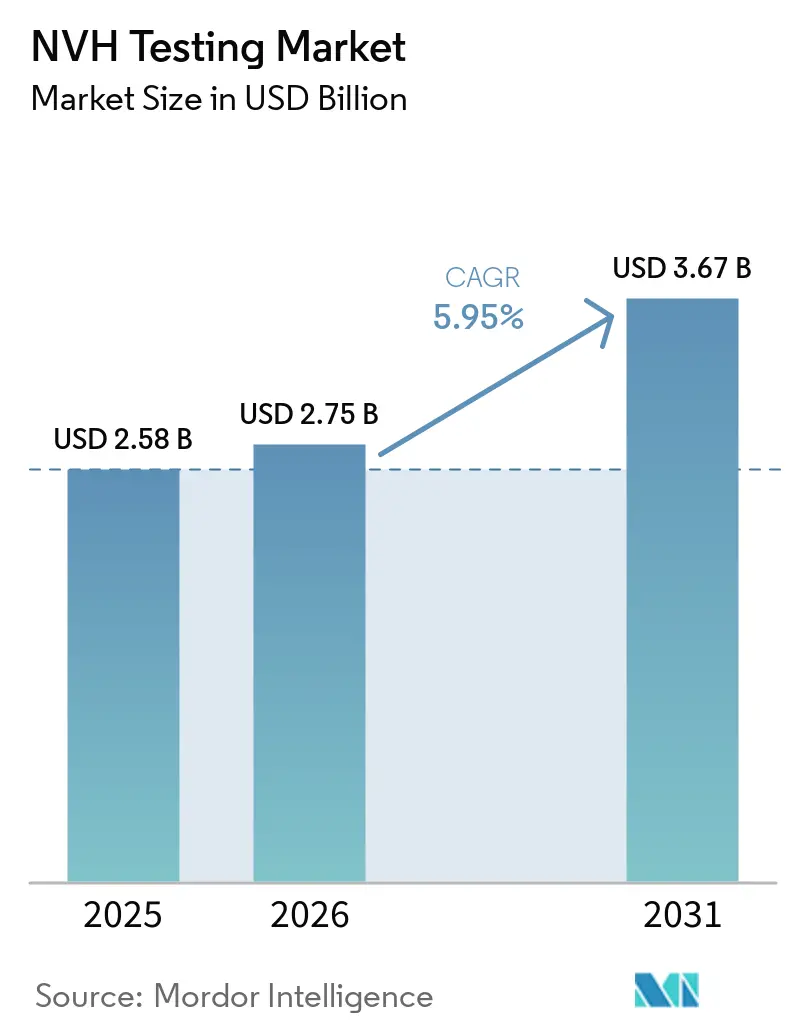

| Market Size (2026) | USD 2.75 Billion |

| Market Size (2031) | USD 3.67 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NVH Testing Market Analysis by Mordor Intelligence

The NVH testing market size is projected to expand from USD 2.58 billion in 2025 and USD 2.75 billion in 2026 to USD 3.67 billion by 2031, registering a CAGR of 5.95% between 2026 and 2031. Cabin-quiet expectations in battery-electric cars, falling micro-electro-mechanical-systems (MEMS) sensor prices, and stricter exterior-noise regulations combine to raise test-bench hours, boost software licenses, and extend regional lab footprints. Vehicle programs that once treated noise, vibration, and harshness as a compliance checkbox now budget for psychoacoustic metrics, real-time cloud analytics, and predictive-maintenance dashboards, reshaping procurement from discrete instruments to integrated platforms. Rising adoption of Industry 4.0 digital twins accelerates feedback loops between physical tests and computer-aided engineering, while the shortage of certified NVH engineers prolongs project timelines and elevates demand for turnkey consulting. Competitive intensity remains moderate because highly specialized hardware portfolios, regional service capacity, and emerging software-only entrants prevent any single supplier from capturing a dominant share.

Key Report Takeaways

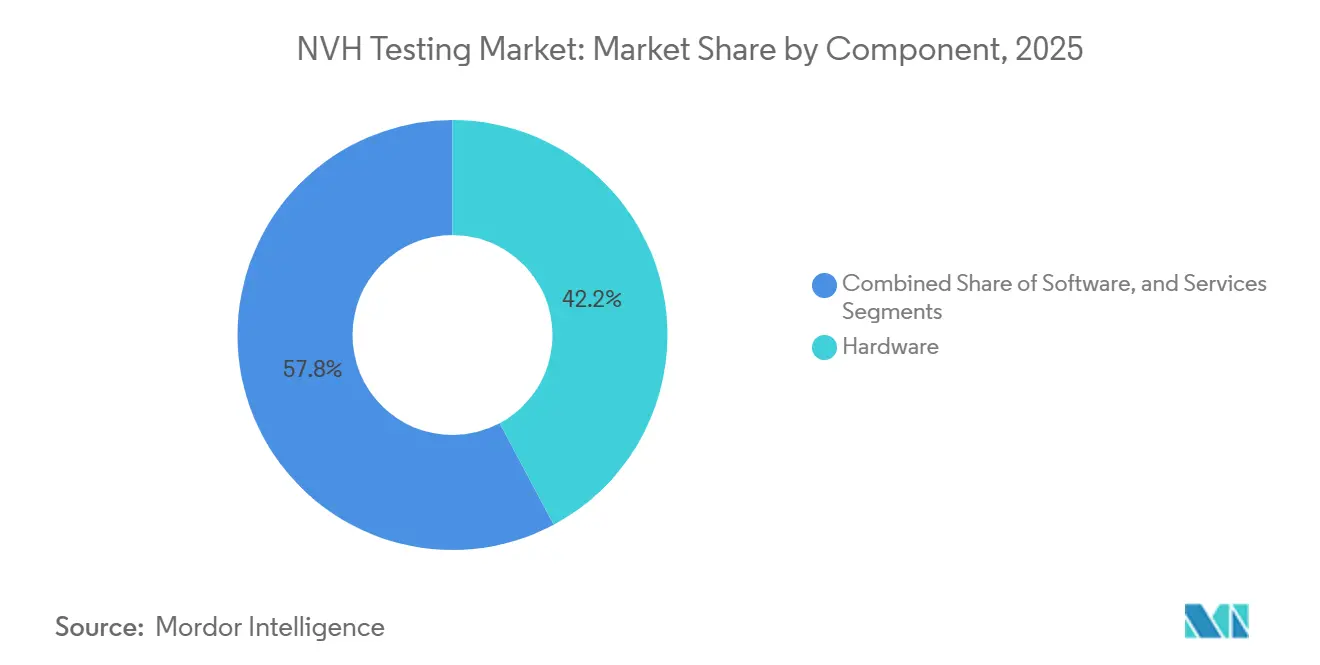

- By component, hardware captured 42.19% of the NVH testing market share in 2025; software is projected to expand at a 6.83% CAGR through 2031.

- By testing type, powertrain NVH led with 29.06% revenue share in 2025, while environmental-chamber NVH is forecast to register a 6.55% CAGR to 2031.

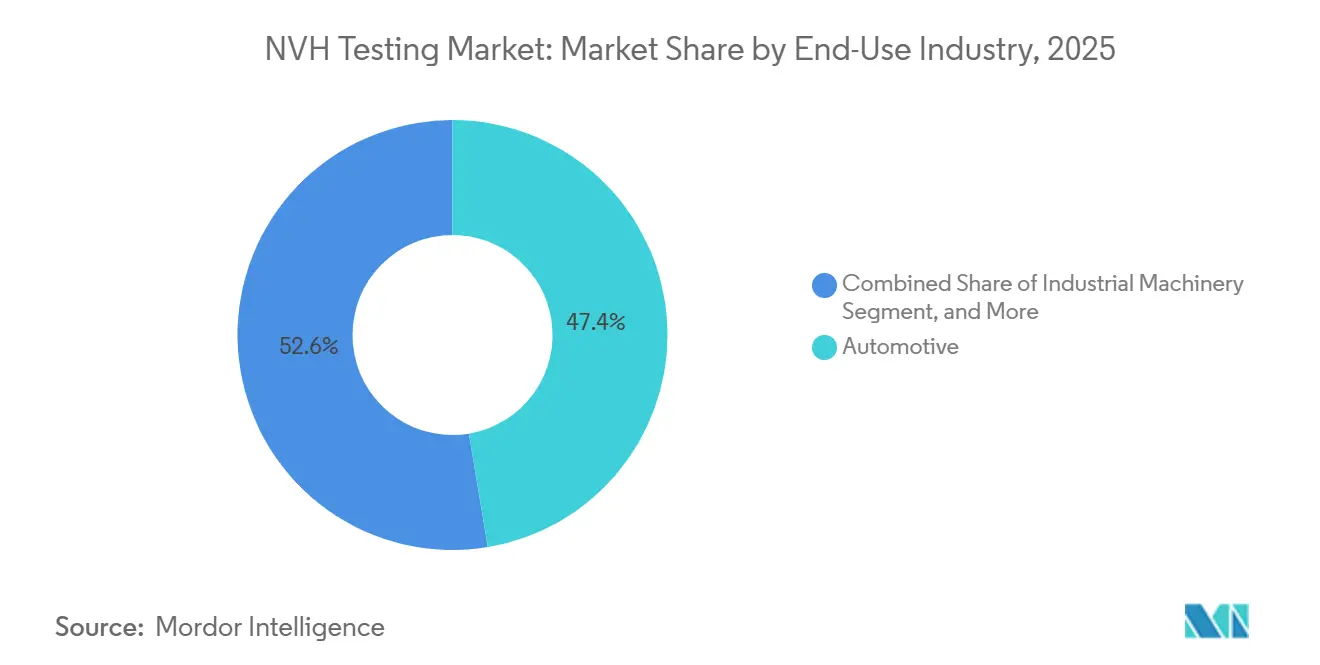

- By end-use industry, automotive accounted for 47.37% of 2025 spending, yet electric and hybrid vehicle programs inside the sector are climbing at a 6.78% CAGR and outpacing internal-combustion testing.

- By application, powertrain validation represented 34.28% of 2025 revenue, whereas electric and hybrid components are set to grow at a 6.91% CAGR.

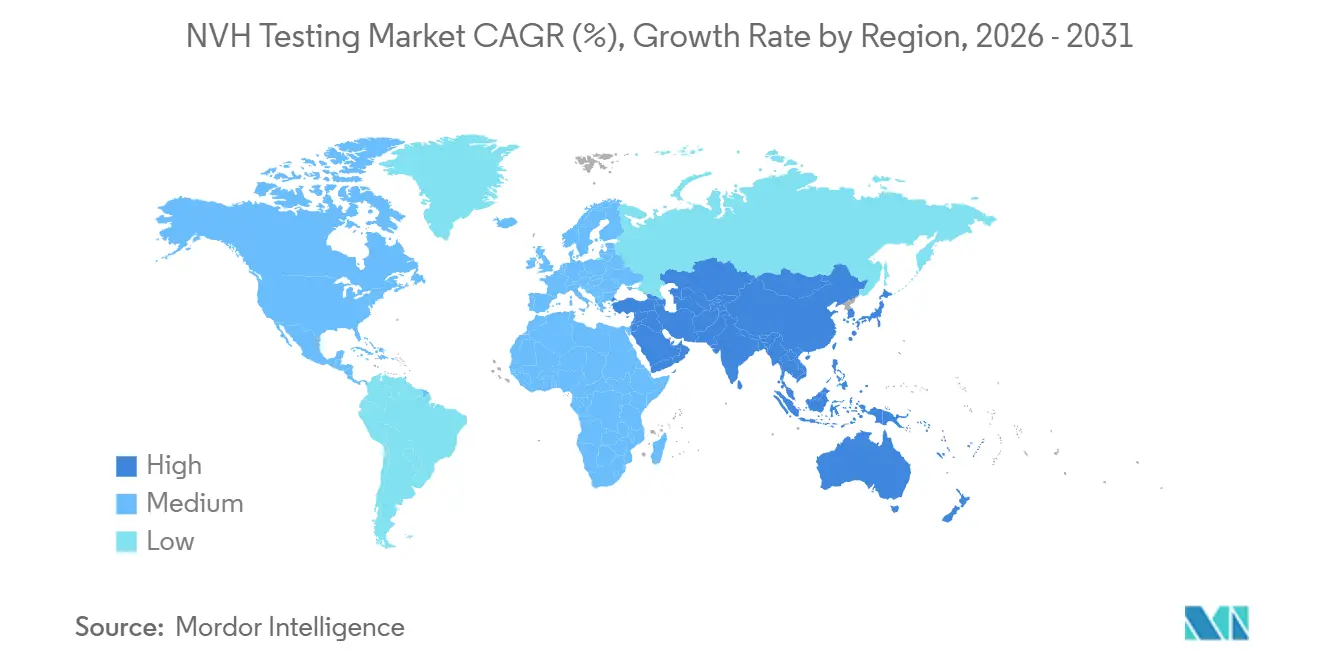

- By geography, Asia-Pacific captured 38.33% of 2025 turnover, and the Middle East is projected to deliver the fastest 6.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global NVH Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrified-Powertrain NVH Requirements | +1.5% | Global, strongest in China, Europe, North America | Medium term (2-4 years) |

| Miniaturized MEMS Sensor Cost Declines | +0.9% | Asia-Pacific manufacturing hubs and global integrators | Short term (≤ 2 years) |

| Stricter UNECE Exterior-Noise Rules | +0.8% | Europe and UNECE-aligned markets | Short term (≤ 2 years) |

| Predictive-Maintenance Adoption in Industry 4.0 | +0.7% | Industrial corridors in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth of Urban Air-Mobility Prototypes | +0.6% | Select cities in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Real-Time Cloud-Based NVH Analytics | +0.5% | North America and Europe early adopters, global diffusion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrified-Powertrain NVH Requirements

Battery-electric and plug-in hybrid models expose inverter pulse-width-modulation tones, gear-mesh whine, and tire-road interaction once masked by combustion engines, steering programs toward order-tracking analysis and psychoacoustic annoyance metrics between 1 kHz and 10 kHz. Luxury automakers saw customer NVH complaints rise to 78% of total quality issues in 2025, prompting validation budgets to climb by one-third. The European Automotive Research Partners Association has published methodologies that separate structure-borne and airborne paths, while UNECE R138 mandates sound-pressure levels of 56 dB(A) to 75 dB(A) below 20 km/h, merging customer comfort and pedestrian-safety objectives into a single compliance stream. As a result, electrified-powertrain NVH remains the primary catalyst for incremental test-bench hours through 2031.

Miniaturized MEMS Sensor Cost Declines

Unit prices for MEMS accelerometers and microphones fell roughly 15% year-on-year between 2024 and 2025, enabling 64- and 128-channel arrays that democratize operational modal analysis for mid-tier suppliers. DewesoftX 2026.1 introduced native Ethernet-linked MEMS support with sub-microsecond synchronization, and National Instruments’ FieldDAQ FD-11634 extended ruggedized coverage to outdoor rocket-test scenarios. Lower acquisition cost also opens the door to continuous condition-based monitoring that can cut unplanned downtime by up to 40 % in manufacturing plants, making sensor affordability a short-cycle demand accelerator.

Stricter UNECE Exterior-Noise Rules

UNECE Regulation 51-03 lowered passenger-car limits to 68 dB(A) effective July 2024, extending compliance complexity from open-air tracks to climate-controlled chambers that reproduce hot, cold, and wet pavement acoustics. TÜV AUSTRIA responded with a 1.2-kilometer ISO 10844:2021 test track opened in April 2025, while automakers now invest in environmental NVH chambers that lengthen validation cycles by roughly 25%. Countries such as India, Brazil, and South Korea have signaled intent to adopt similar limits by 2027, creating a near-term construction surge for exterior-noise facilities.

Predictive-Maintenance Adoption in Industry 4.0

Hybrid machine-learning models combining convolutional neural networks and support vector machines achieved 94.2% fault-classification accuracy in a 2025 study, prompting upgrades to turbines, compressors, and gearboxes with cloud-connected vibration sensors. ISO 20816 baselines are moving from annual audits to real-time dashboards, multiplying sensor counts across petrochemical plants and wind farms.[1]ISO, “ISO 20816 Mechanical Vibration,” iso.org Siemens Simcenter’s May 2026 AI master class in Leuven underlines the shift from traditional frequency-domain plots to data-science workflows, compressing root-cause analysis cycles and linking shop-floor anomalies to digital-twin simulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled NVH Engineers | -0.4% | Global, acute in China, North America, Europe | Medium term (2-4 years) |

| High Capex for Modular Hemi-Anechoic Chambers | -0.3% | Global, more severe for SMEs and emerging markets | Long term (≥ 4 years) |

| Absence of Global Test-Protocol Harmonization | -0.2% | Global friction between UNECE, SAE, ISO | Long term (≥ 4 years) |

| Data-Security Concerns in Remote Testing | -0.1% | Global, highest sensitivity in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled NVH Engineers

CohanHR’s 2025 workforce audit revealed a deficit of 120,000 to 150,000 NVH professionals, with China carrying roughly 50,000 to 60,000 unfilled roles. Ninety-five percent of postings require CAE fluency, yet few university curricula integrate Actran, MSC Nastran, or AVL EXCITE, forcing employers to extend hiring lead times by 6-12 months. Competition from artificial-intelligence roles siphons talent, while hands-on test-cell skills remain irreplaceable, delaying product launches and inflating external consulting spend.

High Capex for Modular Hemi-Anechoic Chambers

Vehicle-scale chambers equipped with chassis dynamometers and ±1 dB free-field uniformity demand investment of several million USD, a threshold demonstrated by Hyundai’s EUR 150 million (USD 165 million) Square Campus facility in November 2025. Smaller markets in South America and Africa must rely on outdoor tracks that introduce wind and temperature variability, complicating model correlation. Capital intensity centralizes capacity in Germany, Japan, Michigan, and South Korea, stretching certification lead times by up to eight weeks during peak launch seasons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Integration Reshapes Validation Workflows

Software claimed the fastest growth rate at a 6.83% CAGR, even though hardware held 42.19% of the NVH testing market share in 2025. Artificial-intelligence modules in Actran, AVL X-ion, and Siemens Simcenter TestLab automate transfer-path analysis and reduce post-processing labor by up to 70%, shrinking design loops and increasing license renewals.[2]AVL List, “NVH Testing Solutions,” avl.com Services from HEAD acoustics and NVH Consulting LLC offset the talent shortfall by bundling turnkey validation, while cloud subscriptions blur hardware-software boundaries and commoditize front-end data acquisition.

Hardware remains irreplaceable for precision capture, so Kistler’s March 2026 jBEAM Lab satellite test update and Dewesoft’s MEMS-enabled platforms underline the hybrid future. As subscription models spread, vendors will tie analytics portals to sensor ecosystems, reinforcing switching costs and nudging procurement from capital expenditure toward operating expenditure, a shift that will further influence the NVH testing market size beyond 2031.

By Testing Type: Environmental Chambers Gain Traction Amid Regulatory Pressure

Powertrain NVH retained 29.06% of 2025 sales, yet environmental-chamber NVH is outpacing the total NVH testing market, with a 6.55% run rate, as UNECE limits tighten temperature-dependent pass-by certification. Modal testing, supported by Polytec’s laser vibrometers, identifies lightweight-composite resonance in urban air-mobility airframes, while operational testing addresses regenerative-braking transients invisible to static rigs.

Ricardo’s upgraded 344 kW dynamometer underscores the need for higher-torque electric-vehicle benchmarking, and Europe’s QuieterRail project extends climate-controlled demand into high-speed rail. The widening application range means environmental chambers will narrow the revenue gap with powertrain benches by decade-end, reshaping NVH testing market share allocations across service catalogs.

By End-Use Industry: Automotive Dominance Faces Aerospace and Electronics Pressure

Automotive generated 47.37% of 2025 turnover, but internal subsegments for battery-electric and hybrid platforms are climbing at 6.78%, twice the pace of legacy programs, signaling a gradual dilution of traditional dominance within the NVH testing market. Aerospace demand accelerates as EASA’s August 2025 eVTOL proposal limits flyover noise to 65 dB(A), compelling the adoption of advanced beamforming.

Consumer-electronics plants, led by Foxconn’s Indian speaker-audit lines, move from batch inspections to 100 % inline acoustic checks, while rail operators apply ISVR-derived track dampers that shave 3-5 dB(A) off urban pass-by readings. Industrial machinery retrofits drive continuous monitoring under ISO 20816, so non-automotive revenue pools will steadily raise their combined NVH testing market share through 2031.

By Application: Electric and Hybrid Components Outpace Legacy Powertrains

Powertrain applications accounted for 34.28% of 2025 receipts, yet electric and hybrid components are surging by 6.91%, steering incremental NVH testing market size toward inverter-, charger-, and motor-centric benches. Interior-cabin programs replace mass-heavy insulation with tuned multilayer composites, while UNECE R138 artificial-warning design melds psychoacoustics with pedestrian safety.

Operational deflection-shape scanning pinpoints door-panel fringes needing stiffening, and Siemens’ virtual transfer-path solver lets engineers iterate on mount stiffness before hardware cut-in. By 2029, electric and hybrid component validation may eclipse conventional powertrain benches, a tipping point that will realign supplier roadmaps and lab-capacity planning. This pivotal shift is set to reshape supplier strategies and influence laboratory capacity planning.

Geography Analysis

Asia-Pacific accounted for 38.33% of 2025 revenue, as China produced 30% of the world’s vehicles and Japan advanced modular chamber installations. Government subsidies for domestic electric-vehicle makers translate into brisk lab utilization, while India’s Ecotone Systems expands turnkey chamber capacity to serve Tier-2 suppliers. A dense supplier base, broad manufacturing scale, and rising battery-electric penetration give the region structural advantages that will secure its leading NVH testing market share well past 2031.

Europe remains a regulatory bellwether: UNECE R51-03, ISO 362 updates, and TÜV AUSTRIA’s Bad Sobernheim track compel manufacturers to invest in local pass-by infrastructure.[3]TÜV AUSTRIA, “New Acoustic Testing Track,” tuv-austria.com Hyundai’s EUR 150 million Rüsselsheim campus spotlights premium-brand commitment, and EU-funded rail noise mitigation adds non-automotive volume. Continuous rule tightening keeps Europe’s CAGR above the global mean even as its absolute NVH testing market size trails Asia-Pacific’s larger base.

North America leverages near-shoring, channeling vehicle programs to Mexico and the U.S. Southeast, prompting AVL and HBK to expand their service offerings. Middle East infrastructure projects in Saudi Arabia and the United Arab Emirates yield the fastest 6.95% CAGR by embedding ISO 20816 vibration clauses into petrochemical and desalination tenders. South America grows from a small base through Brazil’s Sônitus Engenharia, whereas Africa’s share clusters around South Africa’s export assembly. Regional dispersion will persist, but accelerated Middle East adoption nudges its stake from low to mid-single digits by 2031.

Competitive Landscape

No vendor exceeded a 15% share of 2025 turnover, indicating a moderate concentration profile for the NVH testing market. HBK and Siemens anchor premium modal-analysis niches through large installed bases and tight integration between sensors and analytics suites. Emerson’s USD 8.2 billion purchase of National Instruments aims to pivot LabVIEW toward cloud test orchestration, though price hikes in 2024 trimmed entry-level share and signaled growing integration pains.[4]Emerson, “Completion of NI Acquisition,” emerson.com

Strategic activity clusters around vertical integration and AI expansion. Dewesoft and HBK’s Blueberry joint venture fuses real-time analytics with precision sensors, slashing system commissioning time. HBK’s EUR 133.5 million (USD 147 million) acquisition of Piezocryst extends harsh-environment coverage, while midsize consultancies such as NVH Consulting LLC fill the talent gap with flexible outsourcing. Companies are increasingly leveraging these strategies to enhance operational efficiency and market competitiveness.

Emerging threats arise from software-native start-ups that exploit machine-learning inference to classify bearing faults without frequency-domain expertise, potentially commoditizing traditional signal-processing value. Prosig, m+p international, and Signal. X retains niches in gearbox order tracking, marine torsional vibration, and acoustic holography. Expected consolidation through 2031 hinges on capital requirements for cloud platforms and AI pipelines, yet regional service density and specialized know-how will preserve a competitive long tail.

NVH Testing Industry Leaders

National Instruments Corporation

Dewesoft d.o.o.

Siemens AG

Kistler Instrumente AG

Hottinger Brüel & Kjær GmbH (HBK)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kistler introduced the jBEAM Lab update, adding satellite test modules with shock-response and pyroshock analytics for NASA and ESA launch environments.

- March 2026: Dewesoft released DewesoftX 2026.1, enabling Ethernet-linked MEMS arrays with sub-microsecond sync and secure cloud storage for distributed operational modal analysis.

- November 2025: Hyundai inaugurated its EUR 150 million (USD 165 million) Square Campus in Rüsselsheim, featuring Europe’s largest semi-anechoic chamber and a four-post rig for suspension NVH.

- August 2025: EASA issued Notice of Proposed Amendment 2025-03, setting eVTOL flyover noise caps at 65 dB(A) and mandating beamforming validation.

Global NVH Testing Market Report Scope

The NVH Testing Market encompasses tools, technologies, and services used to measure and analyze noise, vibration, and harshness across products and systems. This market primarily serves industries such as automotive, aerospace, electronics, and industrial equipment, where maintaining optimal NVH levels is critical for product performance, safety, and customer satisfaction.

The NVH Testing Market Report is Segmented by Component (Hardware, Software, and Services), Testing Type (Modal, Pass-By Noise, Operational, Environmental-Chamber, and Powertrain), End-Use Industry (Automotive, Aerospace and Defense, Industrial Machinery, Consumer Electronics, Railways, and Marine), Application (Powertrain, Interior Cabin, Exterior Noise, Electric and Hybrid Components, and Structural Components), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Data Acquisition Systems |

| Sensors and Transducers | |

| Analyzers | |

| Other Hardware | |

| Software | Signal Analysis |

| Simulation and Modelling | |

| Services | Testing Services |

| Consulting and Training |

| Modal Testing |

| Pass-By Noise Testing |

| Operational / Dynamic NVH Testing |

| Environmental-Chamber NVH |

| Powertrain NVH |

| Automotive |

| Aerospace and Defense |

| Industrial Machinery |

| Consumer Electronics |

| Railways |

| Marine |

| Powertrain |

| Interior Cabin |

| Exterior Noise |

| Electric and Hybrid Components |

| Structural Components |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | Data Acquisition Systems |

| Sensors and Transducers | ||

| Analyzers | ||

| Other Hardware | ||

| Software | Signal Analysis | |

| Simulation and Modelling | ||

| Services | Testing Services | |

| Consulting and Training | ||

| By Testing Type | Modal Testing | |

| Pass-By Noise Testing | ||

| Operational / Dynamic NVH Testing | ||

| Environmental-Chamber NVH | ||

| Powertrain NVH | ||

| By End-Use Industry | Automotive | |

| Aerospace and Defense | ||

| Industrial Machinery | ||

| Consumer Electronics | ||

| Railways | ||

| Marine | ||

| By Application | Powertrain | |

| Interior Cabin | ||

| Exterior Noise | ||

| Electric and Hybrid Components | ||

| Structural Components | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current NVH testing market size and projected growth to 2031?

The NVH testing market size was USD 2.58 billion in 2025, increased to USD 2.75 billion in 2026, and is forecast to reach USD 3.67 billion by 2031, expanding at a 5.95% CAGR during 2026-2031.

Which component segment is growing the fastest within NVH testing?

Software is the fastest-growing component, advancing at a 6.83% CAGR as artificial-intelligence modules automate fault detection.

Why are environmental NVH chambers gaining popularity?

Stricter UNECE exterior-noise limits and the need to replicate extreme climates for electric-vehicle battery systems are driving a 6.55% CAGR in environmental-chamber NVH demand.

Which geography shows the quickest NVH testing growth?

The Middle East leads with a 6.95% CAGR because large infrastructure projects in Saudi Arabia and the United Arab Emirates require vibration monitoring compliant with ISO 20816.

How is the talent shortage affecting NVH testing programs?

A global deficit of up to 150,000 qualified engineers lengthens hiring cycles by 6-12 months, pushing companies toward turnkey consulting and impacting project timelines.

What technological trend is reshaping NVH data analysis?

Real-time cloud analytics combined with machine-learning algorithms enables predictive maintenance and compresses post-processing time by up to 70 %, redefining traditional workflows.

Page last updated on: