Robotic Endoscopy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

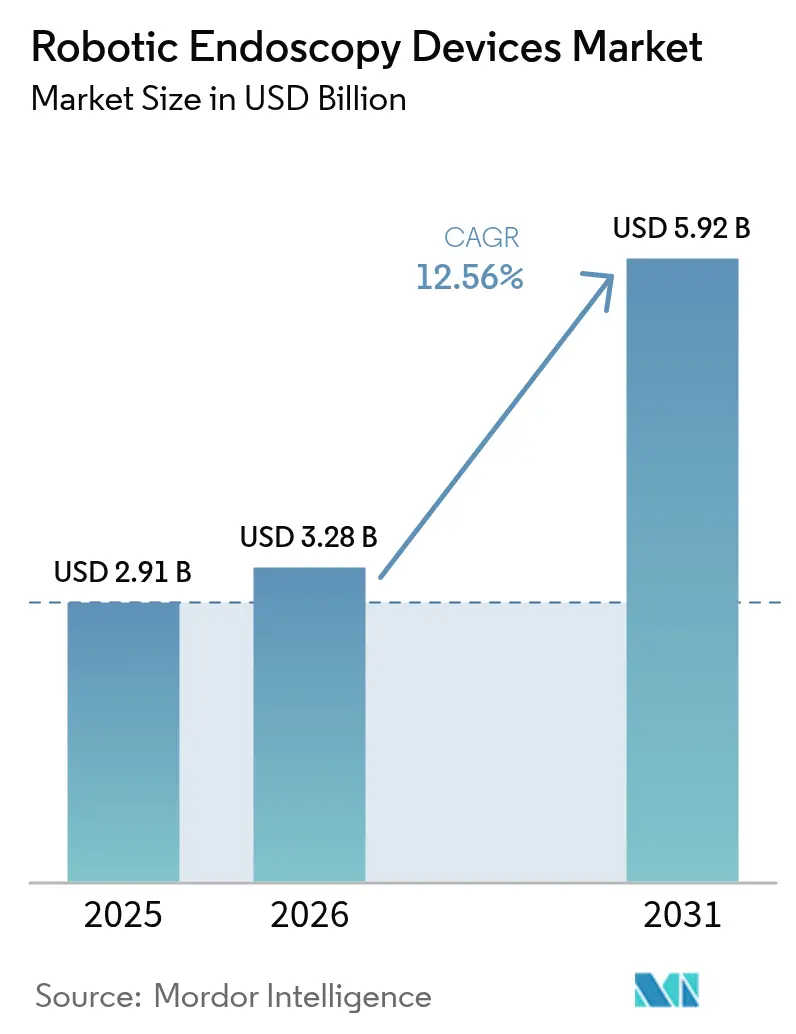

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 5.92 Billion |

| Growth Rate (2026 - 2031) | 12.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Endoscopy Devices Market Analysis by Mordor Intelligence

Robotic endoscopy devices market size in 2026 is estimated at USD 3.28 billion, growing from 2025 value of USD 2.91 billion with 2031 projections showing USD 5.92 billion, growing at 12.56% CAGR over 2026-2031. Growing adoption of minimally invasive surgery, rapid integration of artificial intelligence into imaging and navigation, and the need to curb hospital-acquired infection rates collectively propel demand. Health systems also view robotic technology as a route to shorten hospital stays and lower total procedure costs, creating favorable economics for capital investment. Competitive intensity is rising as patent cliffs democratize core technologies and modular, lower-cost platforms reach the market. Meanwhile, mounting evidence that single-use scopes eliminate cross-contamination risk strengthens the value proposition for outpatient settings. Together, these forces position the robotic endoscopy devices market for sustained double-digit expansion through the decade.

Key Report Takeaways

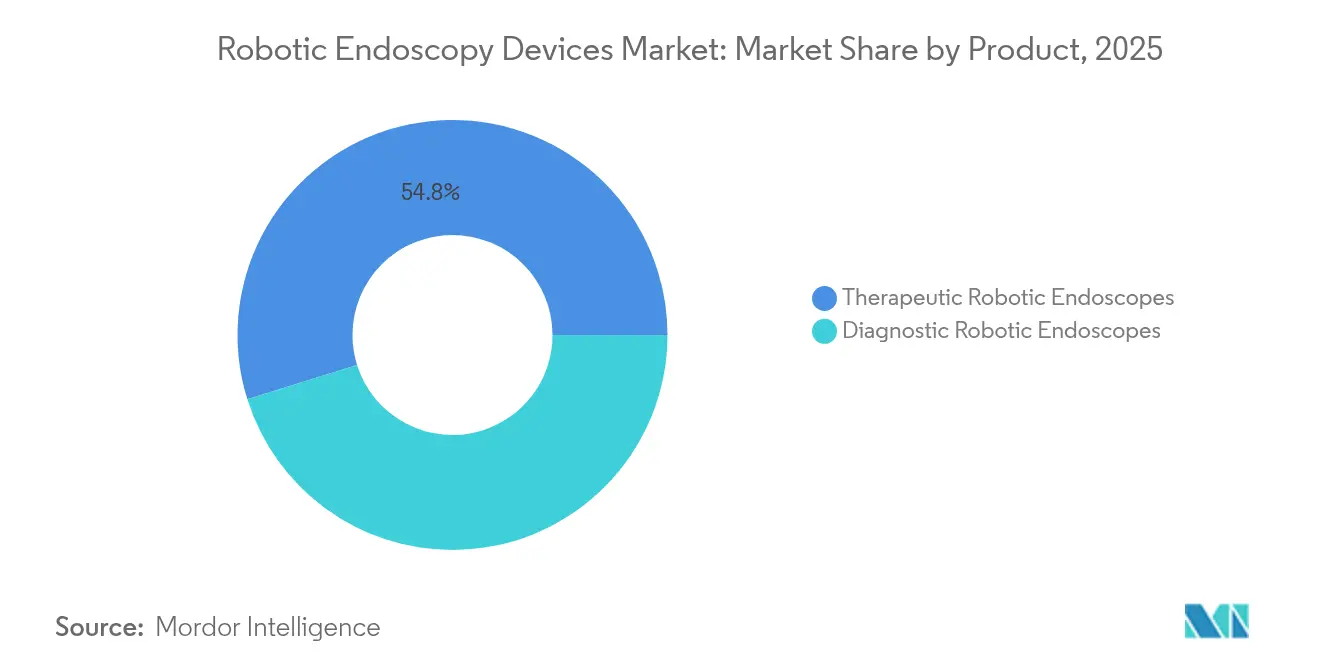

- By product, therapeutic robotic endoscopes held 54.83% of the robotic endoscopy devices market share in 2025, while diagnostic robotic endoscopes are set to expand at a 14.79% CAGR through 2031.

- By application, laparoscopy led with 45.02% revenue in 2025; bronchoscopy is advancing at a 15.6% CAGR to 2031.

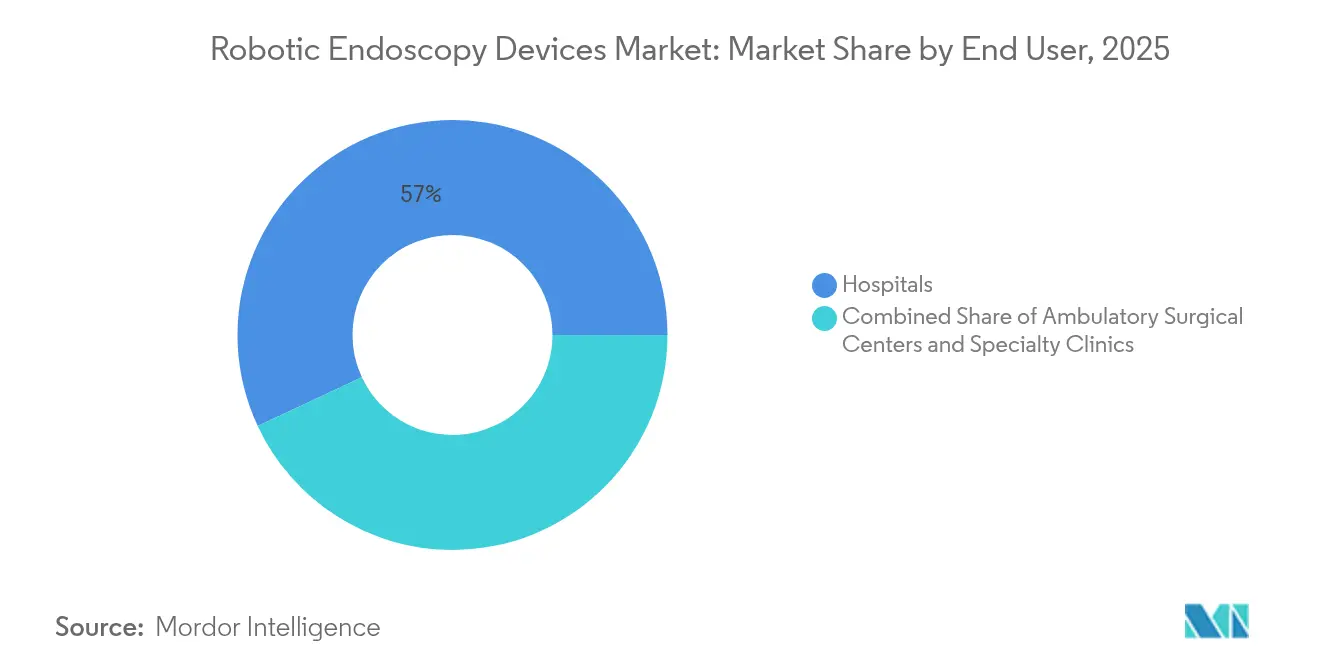

- By end user, hospitals controlled 56.95% of the robotic endoscopy devices market in 2025, yet ambulatory surgical centers (ASCs) record the highest projected CAGR at 12.9% through 2031.

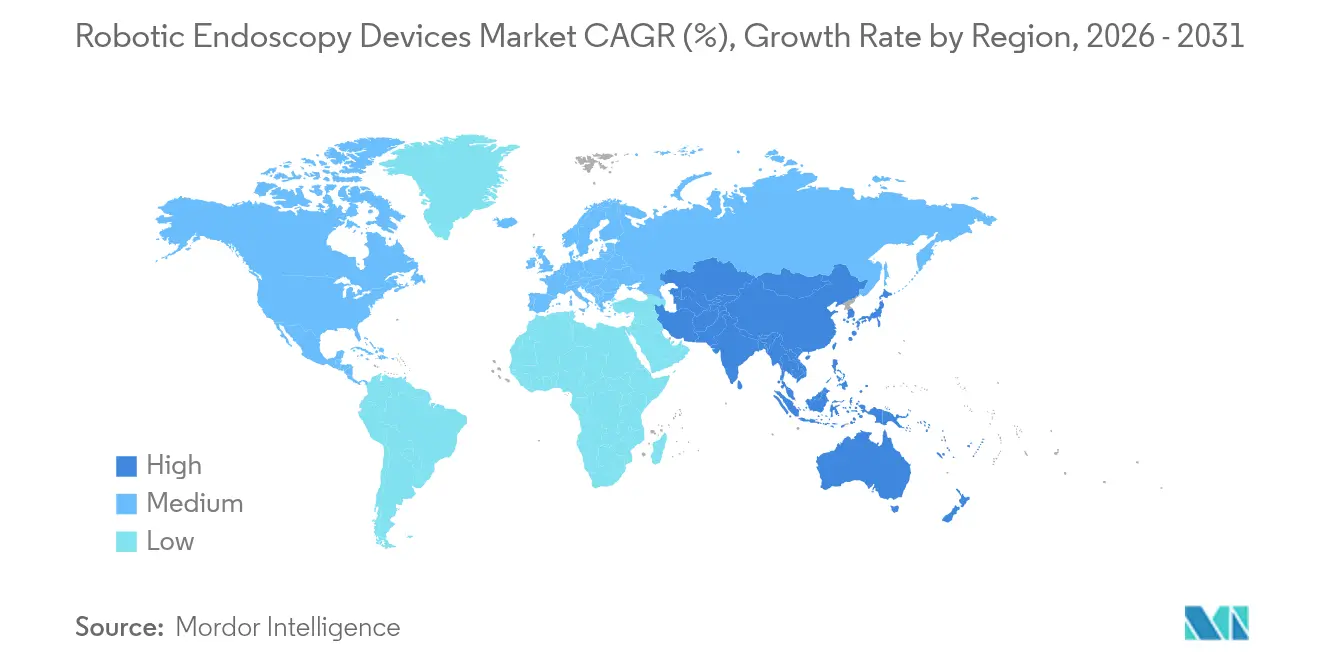

- By geography, North America captured 38.35% of 2025 revenue, while Asia-Pacific is growing fastest at 13.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotic Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Minimally-Invasive Robotic Procedures | +2.8% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| AI-Augmented Navigation & Imaging Boosts Diagnostic Yield | +2.4% | Global, spill-over to emerging markets | Medium term (2-4 years) |

| Rising Geriatric, Obese & Diabetic Population | +2.1% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Favorable Reimbursement For Robotic GI & Pulmonary Interventions | +1.9% | North America & EU core markets | Short term (≤ 2 years) |

| Surge In Dedicated Outpatient Robotic Bronchoscopy Suites | +1.6% | North America & APAC, expansion to MEA | Medium term (2-4 years) |

| Demand For Single-Use Robotic Endoscopes To Curb Infections | +1.4% | Global, accelerated in post-pandemic era | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption Of Minimally-Invasive Robotic Procedures

Clinical evidence shows robotic-assisted surgeries cut complication rates by 50% and trim recovery times by 40% compared with traditional techniques. Hospitals increasingly prioritize these outcomes to meet value-based care mandates, leading to wider platform installs and broader procedural menus. Intuitive Surgical reported 17% procedure growth in Q1 2025, underscoring global momentum[1]Investing.com, “Earnings Call Transcript: Intuitive Surgical Q1 2025,” investing.com. Enhanced 3-D vision, tremor filtration, and ergonomic consoles also mitigate surgeon fatigue, allowing longer and more complex cases in outpatient settings. Collectively, these gains expand the eligible patient pool and reinforce the economic attractiveness of the robotic endoscopy devices market.

AI-Augmented Navigation & Imaging Boosts Diagnostic Yield

Deep-learning models now lift diagnostic yield in robotic bronchoscopy to over 85%, well above the 67.8% baseline of conventional scopes[2]Anthem, “Clinical Guideline CG-MED-93,” anthem.com. Johnson & Johnson’s MONARCH QUEST platform integrates 260% more compute power with AI-driven path-planning, improving lesion targeting in real time. Cloud-based systems such as Olympus CADDIE extend similar benefits to colorectal screening, where AI raises adenoma detection without extra procedure time. Higher accuracy reduces repeat procedures and accelerates therapeutic decision-making, giving platform owners a clear competitive edge.

Favorable Reimbursement for Robotic GI & Pulmonary Interventions

Medicare’s 2025 Physician Fee Schedule added tele-supervised robotic codes and expanded coverage for advanced GI and pulmonary procedures, lowering financial barriers for providers[3]Centers for Medicare & Medicaid Services, “Medicare Physician Fee Schedule Final Rule Summary CY 2025,” cms.gov. Category I CPT codes for Olympus’s iTind therapy further legitimize robotic approaches, streamlining claims workflows. Private payers follow suit as actuarial data link fewer complications to cost savings. The resulting revenue certainty encourages health systems to accelerate capital purchases, deepening adoption across both hospital and ASC settings.

Demand for Single-Use Robotic Endoscopes to Curb Infections

Growing scrutiny of scope reprocessing drives interest in disposable designs that eliminate cross-patient contamination. Boston Scientific’s EXALT Model D duodenoscope removes all reprocessing steps while improving ergonomics. Cost analyses show total per-procedure expenses approach parity once labor, monitoring, and liability exposures are considered Ambu. Environmental trade-offs persist, but research into biodegradable polymers and recycling schemes aims to reconcile safety with sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Per-Procedure Cost Of Robotic Platforms | -2.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| Stringent Regulatory Approvals For Patient-Safety | -1.8% | Global, stricter in EU post-MDR | Long term (≥ 4 years) |

| Shortage Of Surgeons Trained On Robotic Endoscopy | -1.5% | Global, concentrated in rural areas | Long term (≥ 4 years) |

| Sustainability Push Against Disposable Robotic Scopes | -0.9% | EU & North America environmental focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Per-Procedure Cost of Robotic Platforms

System list prices between USD 1.5 million and USD 2.5 million, plus annual service fees above USD 100,000, impose steep hurdles for smaller centers. Comparative studies show robotic inguinal hernia repair costs EUR 2,810 (USD 3,242.01) versus EUR 726 (USD 837.62) for laparoscopic alternatives, underscoring payback challenges where reimbursement lags. New entrants like CMR Surgical target this gap with modular architecture priced below legacy systems, yet widespread budget constraints in lower-income regions continue to suppress uptake.

Stringent Regulatory Approvals for Patient Safety

Europe’s Medical Device Regulation demands extensive clinical evidence, extending time-to-market by up to five years and inflating compliance costs beyond USD 10 million for complex robotics. The US FDA likewise intensifies oversight of autonomous functions, compelling developers to embed robust surgeon-control safeguards. These layers of scrutiny weigh heavily on startups, slowing product cycles and tempering the pace of innovation diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutic Platforms Drive Market Leadership

Therapeutic robotic endoscopes accounted for 54.83% of the robotic endoscopy devices market in 2025, underscoring provider demand for systems that combine diagnosis and intervention in a single sitting. Leading products execute complex maneuvers such as endoscopic submucosal dissection and natural-orifice transluminal surgery, enabling scar-free outcomes that appeal to both patients and payers. Johnson & Johnson’s MONARCH platform illustrates this premium positioning, while EndoQuest pursues flexible, single-port concepts for GI procedures. Although therapeutic dominance prevails, diagnostic devices show greater headroom; AI-enhanced visualization lifts early cancer detection, pushing diagnostic unit sales at a 14.79% CAGR. Capsule systems and hybrid imaging robots widen access, hinting at future convergence where one console manages full care pathways. The robotic endoscopy devices market size for therapeutic systems is projected to broaden steadily, but diagnostic innovation is set to outpace as preventive medicine becomes policy priority.

Diagnostic platforms remain a smaller slice, yet investors funnel capital into wireless capsule robots and cloud-enabled analytics that shorten procedure times. Early-stage projects such as swallowable pump-jet cameras expand the reach of gastrointestinal screening, particularly in rural regions where full theaters are scarce. As these devices secure regulatory clearance, the robotic endoscopy devices market share for diagnostic solutions is expected to climb, narrowing the revenue gap versus therapeutic peers.

By Application: Bronchoscopy Emerges as Growth Engine

Laparoscopic cases generated 45.02% of 2025 revenue and anchor much of the installed base, thanks to decades of surgeon familiarity and mature reimbursement. Robotic assistance here drives incremental precision rather than radical workflow change, so growth rates moderate near mid-single digits. Even so, replacement cycles and emerging-market installs keep laparoscopy a critical pillar of the robotic endoscopy devices market.

Bronchoscopy adds the spark. Peripheral lung-nodule biopsies once hampered by reach limitations now achieve diagnostic yields up to 90% with robotic guidance. Cone-beam CT fusion and AI-powered airway mapping enhance target localization, driving a 15.6% CAGR through 2031. The robotic endoscopy devices market size for bronchoscopy platforms is set to more than double, elevating respiratory care as a key battleground for system vendors. Colonoscopy and ENT uses progress steadily, but their combined revenue remains secondary to the high-velocity pulmonary segment.

By End User: ASCs Reshape Service Delivery

Hospitals retained 56.95% of 2025 revenue by housing complex multidisciplinary cases under one roof. Academic centers act as early adopters, validating new workflows and training surgeons who later disseminate expertise. Yet ballooning operating costs and patient preference for same-day discharge shift momentum toward ASCs. Purpose-built robotic suites cut turnover times and enhance asset utilization, letting operators break even at lower case volumes. The robotic endoscopy devices market is thus migrating; ASCs expand at 12.9% CAGR and will account for a rising fraction of platform placements by decade’s end. Specialty clinics focused on pulmonology or bariatric care capture niche demand where high throughput justifies dedicated consoles.

Two-tier service delivery now crystallizes: hospitals manage trauma and high-acuity oncology, while ASCs command elective screenings and straightforward interventions. Vendors must cater to divergent capital budgets and workflow constraints, tailoring service contracts and per-use pricing accordingly to maximize exposure across the robotic endoscopy devices industry.

Geography Analysis

North America generated 38.35% of 2025 revenue, supported by Medicare payment clarity and a mature surgeon talent pool. Flagship centers in the United States routinely adopt next-generation consoles within months of clearance, sustaining robust upgrade cycles. Canada follows similar patterns, while Mexico’s private hospitals court medical tourists to finance advanced installations.

Europe holds significant share but confronts regulatory headwinds and green-policy scrutiny of single-use plastics. Germany, France, and the United Kingdom dominate installed bases, yet multi-year conformity assessments under the Medical Device Regulation delay market entry for new entrants. Nordic health systems investigate robotic hernia repair benefits, but cost-effectiveness questions remain open, tempering rapid scale-up.

Asia-Pacific exhibits the fastest regional CAGR at 13.2%. China anchors momentum through domestic champions offering consoles at discounts of 30%–40% relative to Western peers, spurring adoption across tertiary hospitals. Japan pioneers unique platforms and 5G-enabled telesurgery demonstrations, while South Korea emphasizes robotics in national cancer-screening protocols. Emerging ASEAN economies and India’s private chains invest aggressively, seeing robotics as a differentiator for inbound medical tourism. Consequently, the robotic endoscopy devices market size for Asia-Pacific is forecast to overtake Europe near the end of the outlook window.

Middle East & Africa record nascent but promising uptake, led by Gulf Cooperation Council projects that bundle robotics into flagship hospital build-outs. South Africa spearheads sub-Saharan adoption. Latin America witnesses steady installations in Brazil and Chile, though currency volatility constrains wider diffusion. Across these regions, vendor financing and procedure-based leasing models are critical in unlocking incremental demand.

Competitive Landscape

Competition remains moderate but intensifying as core patents expire and software differentiation eclipses mechanical exclusivity. Intuitive Surgical still commands a sizable installed base, yet Johnson & Johnson leverages NVIDIA partnerships to infuse powerful edge AI into its MONARCH and forthcoming OTTAVA platforms. CMR Surgical disrupts pricing norms with modular arms that allow tailored OR footprints, winning its first FDA clearance in 2024 and raising USD 200 million for US expansion. Chinese manufacturers such as KangDuo narrow performance gaps quickly, threatening margin compression for incumbents.

Strategic moves now hinge on ecosystem control. Vendors bundle imaging towers, disposable accessories, and data analytics into subscription bundles that shift capital cost into operating expense. Asensus Surgical secured FDA pediatric indications for Senhance, opening an underserved niche and compelling rivals to broaden age-range claims. Boston Scientific integrates single-use duodenoscopes into its endoscopy franchise, reinforcing cross-selling power while meeting infection-control mandates. Alliances between hardware makers and cloud providers aim to harvest intraoperative data for algorithm training, embedding virtuous cycles of performance improvement difficult for smaller challengers to match.

In parallel, sustainability debates ignite innovation around recyclable polymers and energy-efficient consoles, providing fresh vectors for differentiation. Vendors that navigate both infection control and environmental stewardship will likely secure preferred-supplier status in European tenders. Overall, the race tilts toward platforms offering demonstrable cost-per-case parity, advanced AI feature sets, and clear pathways to regulatory compliance across multiple jurisdictions, shaping the evolution of the robotic endoscopy devices market through 2030.

Robotic Endoscopy Devices Industry Leaders

Brainlab AG

Medrobotics Corporation

Johnson & Johnson

Intuitive Surgical Inc.

Asensus Surgical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus Corporation received FDA clearance for its EZ1500 series endoscopes with Extended Depth of Field imaging, elevating lesion-detection capability across GI procedures.

- May 2025: EndoQuest and Virtuoso Surgical began clinical trials for next-generation surgical robots targeting colorectal and ENT applications.

- March 2025: Johnson & Johnson MedTech secured FDA 510(k) clearance for MONARCH QUEST, adding AI-driven computational upgrades to its bronchoscopy platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our study counts all revenues earned from sales of motor-driven or robotically actuated flexible or rigid endoscopes and their proprietary diagnostic or therapeutic accessories that physicians guide inside the human body to visualize or treat tissue during minimally invasive procedures across hospitals, ambulatory surgical centers, and specialty clinics worldwide.

Scope exclusion: Conventional manually steered endoscopes, single-use capsule cameras lacking robotic propulsion, and stand-alone navigation software platforms are outside our remit.

Segmentation Overview

- By Product

- Diagnostic Robotic Endoscopes

- Capsule Robots

- Imaging/Visualization Robots

- Therapeutic Robotic Endoscopes

- Surgical Endoscopy Platforms

- Robotic Bronchoscopes

- NOTES & Transluminal Robots

- Diagnostic Robotic Endoscopes

- By Application

- Laparoscopy

- Bronchoscopy

- Colonoscopy

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

Our team first compiles foundational metrics from open sources such as US FDA 510(k) databases, EUDAMED notices, Medicare outpatient procedure files, WHO health-expenditure dashboards, and association reports from bodies such as the American Society for Gastrointestinal Endoscopy. Annual filings, investor decks, and patent analytics mined through Questel, plus shipment statistics from Volza, round out supply curves and regional pricing corridors that seed the initial model. The examples above illustrate the spectrum consulted, and many additional references support data capture, validation, and clarification.

Primary Research

Phone interviews and online surveys with gastrointestinal surgeons, biomedical engineers, procurement heads, and regional distributors across North America, Europe, and Asia-Pacific verify adoption triggers, price-erosion patterns, downtime costs, and capacity constraints, letting us fine-tune usage ratios and scenario sensitivities.

Market-Sizing & Forecasting

A top-down build starts with national procedure volumes and capital-equipment spend, which are then reconciled with sampled average selling price multiplied by installed-base roll-ups for leading platforms to eliminate blind spots. Key variables like robotic colonoscopy penetration, device replacement cycle, hospital capital-expenditure growth, regulatory clearance pipeline, and elective-surgery backlog feed a multivariate-regression forecast to 2030. Bottom-up manufacturer revenue snapshots and import records help adjust totals where gaps appear.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, peer review, and senior sign-off. We re-engage experts when anomalies cross preset thresholds. Figures refresh annually, with interim revisions triggered by major approvals, recalls, or reimbursement changes, so clients always receive the latest view.

Why Mordor's Robotic Endoscopy Devices Baseline Deserves Trust

Published estimates differ because each publisher selects its own product boundary, price assumptions, data year, and refresh cadence. Our disciplined scoping, primary validation, and yearly updates narrow those gaps for decision-makers.

Key gap drivers include counting hybrid visualization towers, using list prices without regional discounts, or projecting procedure booms that outpace regulatory capacity.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.91 B (2025) | Mordor Intelligence | |

| USD 2.68 B (2024) | Global Consultancy A | Includes non-robotic HD towers; no ASP adjustment |

| USD 2.49 B (2024) | Industry Publisher B | Relies on conservative device penetration and older hospital-capacity data |

These comparisons show that Mordor's transparent variable selection, frequent validation, and balanced scenario planning deliver a dependable baseline that buyers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the robotic endoscopy devices market?

The market is valued at USD 3.28 billion in 2026 and is on course to reach USD 5.92 billion by 2031.

Which product segment dominates revenue?

Therapeutic robotic endoscopes lead with 54.83% of 2025 revenue, thanks to their combined diagnostic and interventional capabilities.

Why is bronchoscopy the fastest-growing application?

Robotic bronchoscopy raises diagnostic yield for peripheral lung nodules up to 90%, supporting a 15.6% CAGR through 2031 and meeting urgent early lung-cancer detection needs.

Which is the fastest growing region in Robotic Endoscopy Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How are ambulatory surgical centers impacting market dynamics?

ASCs post a 12.9% CAGR as outpatient models lower costs and align with patient preferences for same-day discharge, shifting procedure volumes away from hospitals.

What role does AI play in next-generation platforms?

AI enhances real-time navigation and tissue characterization, pushing diagnostic accuracy above 85% and giving vendors a major differentiation lever.

Page last updated on: