Nuclear Power Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

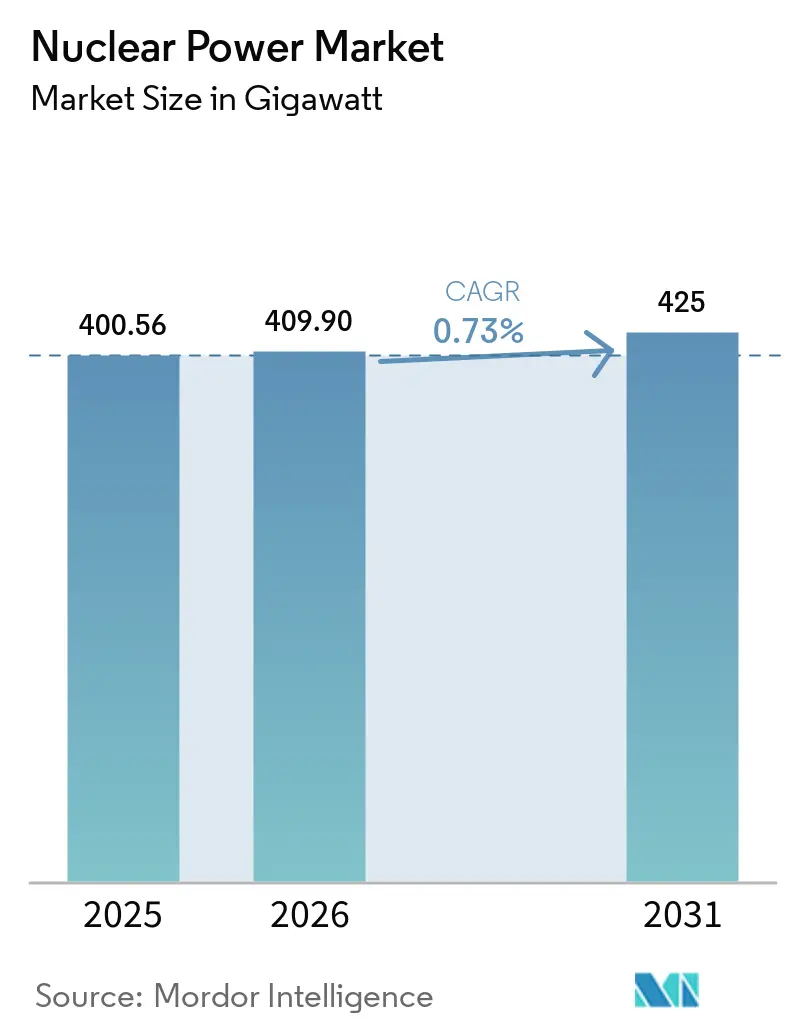

| Market Volume (2026) | 409.90 gigawatt |

| Market Volume (2031) | 425 gigawatt |

| Growth Rate (2026 - 2031) | 0.73% CAGR |

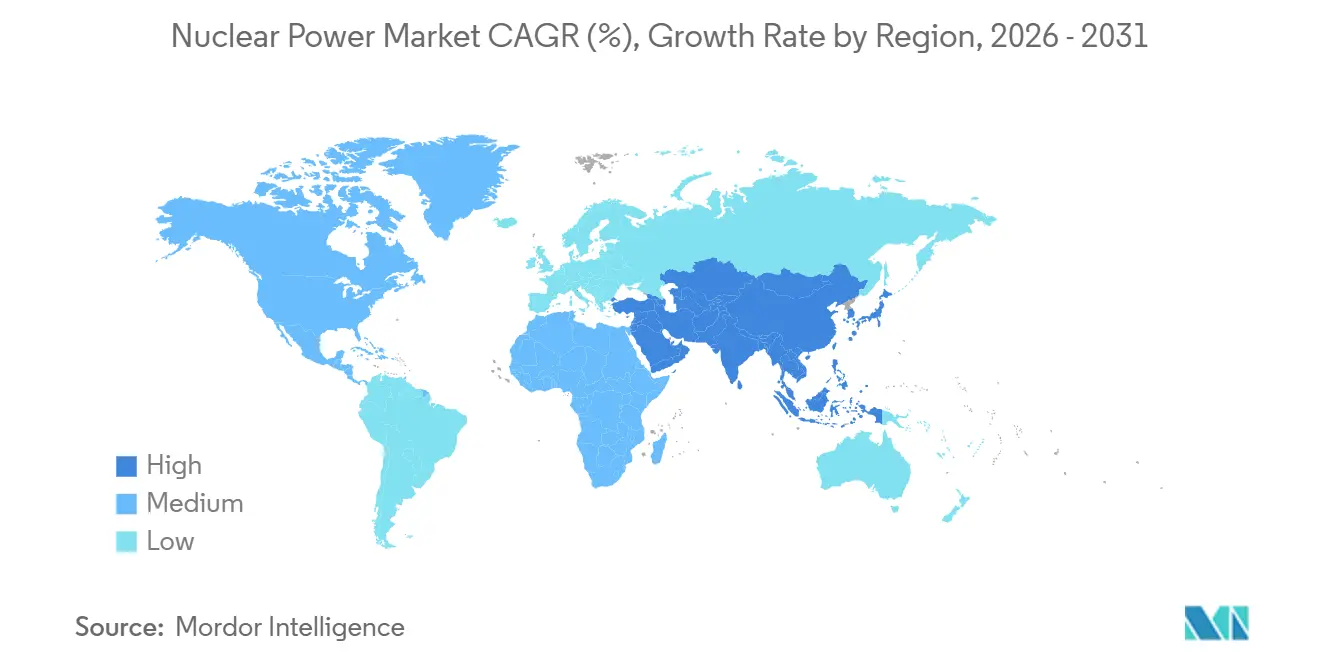

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuclear Power Market Analysis by Mordor Intelligence

The Nuclear Power Market size is projected to expand from 400.56 gigawatt in 2025 and 409.90 gigawatt in 2026 to 425 gigawatt by 2031, registering a CAGR of 0.73% between 2026 to 2031.

Capacity growth remains modest, yet momentum is strengthening around advanced reactor designs that promise shorter construction schedules and lower financing risk. Industrial buyers are emerging as a second demand pillar alongside utilities, drawn by the need for high-temperature, zero-carbon process heat. Rapid policy support in the United States, France, and China is offsetting cost pressures that still hinder large gigawatt-scale builds. Meanwhile, shifting fuel-cycle strategies, especially the move toward high-assay low-enriched uranium (HALEU), are redrawing supply chains and enlarging the addressable market for compact plants.

Key Report Takeaways

- By reactor type, pressurized light-water technology led with 72.8% of installed capacity in 2025, while fast breeder reactors are projected to expand at a 21.4% CAGR through 2031.

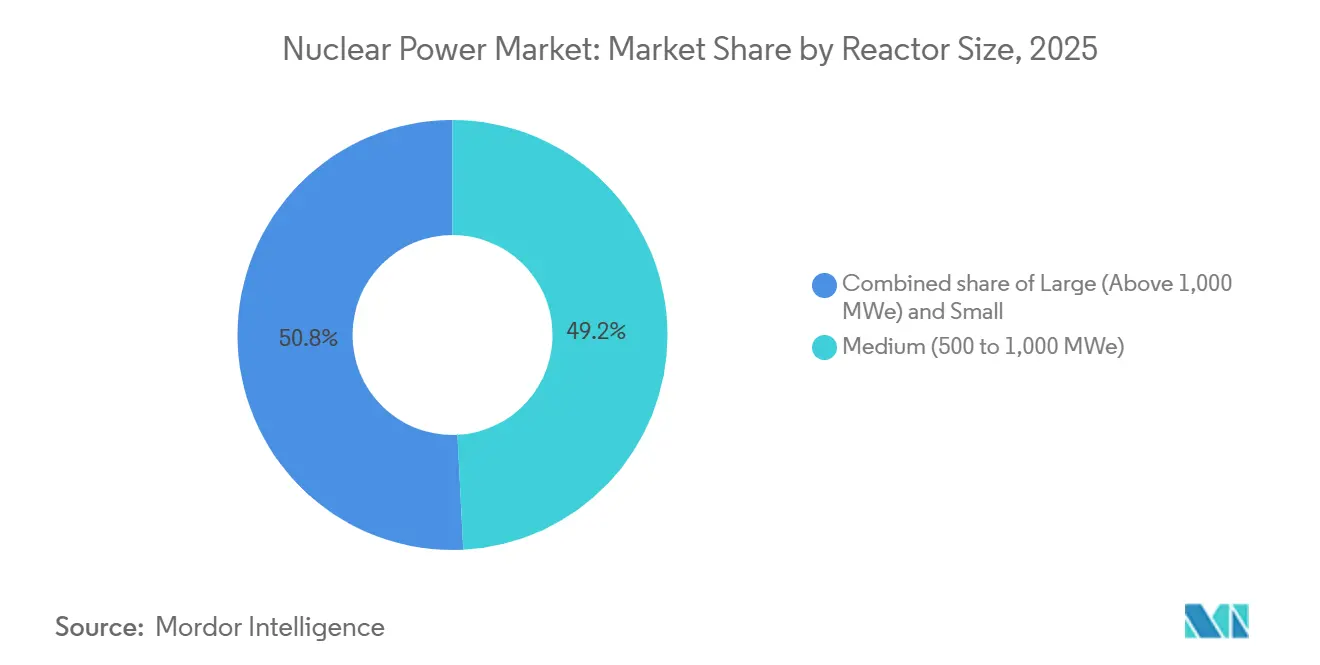

- By reactor size, the medium-sized category (500-1,000 MWe) held 49.2% of the Global nuclear power market share in 2025, whereas small reactors below 500 MWe are forecast to grow at 20.1% CAGR to 2031.

- By fuel type, low-enriched uranium accounted for 87.5% of capacity in 2025; HALEU is projected to expand at a 10.9% CAGR through 2031.

- By application, utilities and IPPs represented 87.7% of demand in 2025, while industrial and petro-chemical is projected to expand at a 12% CAGR to 2031.

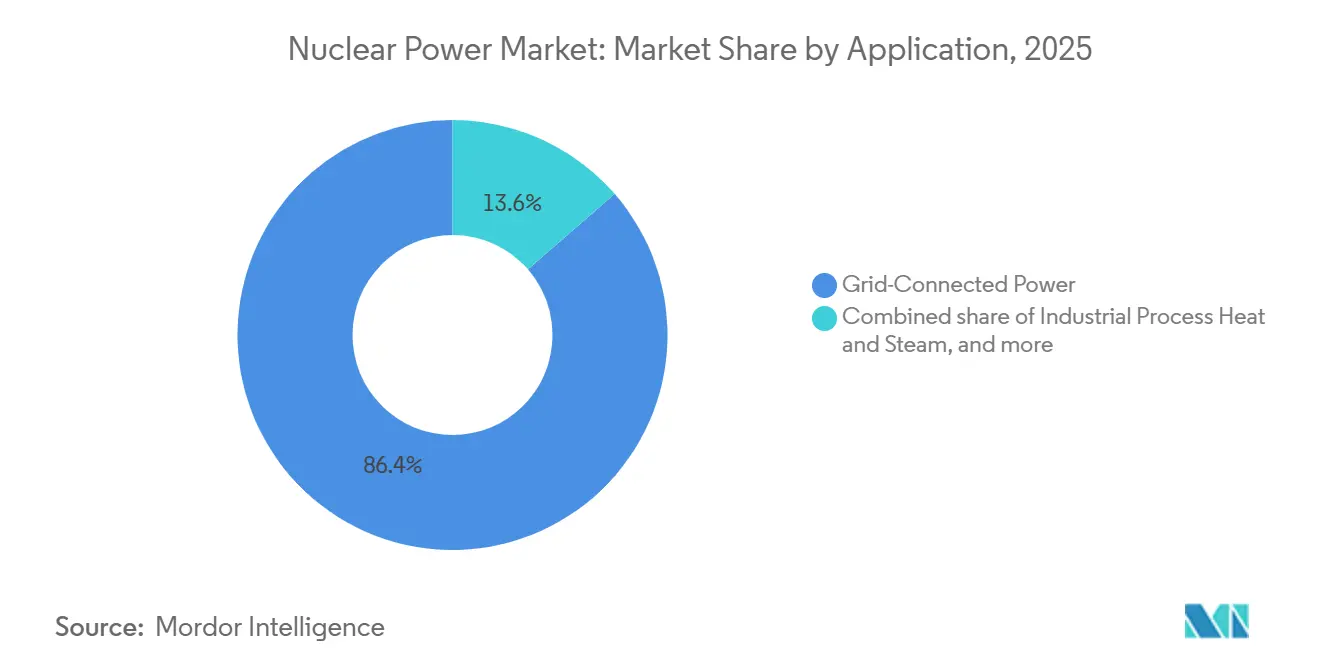

- By end-user, grid-connected power represented 86.4% of demand in 2025, while industrial process-heat use is projected to expand at a 14.7% CAGR to 2031.

- By geography, Europe held 39.1% of capacity in 2025; Asia-Pacific is the fastest-growing region at 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nuclear Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in demand for clean baseload power | +0.15% | Global, with concentration in Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Lifetime extension & uprate programs | +0.08% | North America, Europe, Russia | Short term (≤ 2 years) |

| Commercialization of advanced SMRs | +0.12% | North America, UK, Eastern Europe, Middle East | Long term (≥ 4 years) |

| Industrial decarbonization process-heat demand | +0.10% | Europe, China, North America industrial corridors | Medium term (2-4 years) |

| Nuclear-produced hydrogen & ammonia initiatives | +0.09% | North America, Europe, Japan, Middle East | Long term (≥ 4 years) |

| Emergence of nuclear-powered data-center & marine applications | +0.11% | North America, Europe, Asia-Pacific tech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Demand for Clean Baseload Power

Governments tightening carbon budgets now view nuclear as the only dispatchable zero-emission source that can scale quickly enough to back up intermittent renewables. France’s 2024 energy law mandates six new EPR2 units, the United Kingdom’s Great British Nuclear program targets 24 GW by 2050, and U.S. production tax credits under the Inflation Reduction Act improve project economics in deregulated markets.[1]International Energy Agency, “Net Zero Roadmap 2025 Update,” iea.org These measures collectively restore an investment thesis that had eroded after a decade of retirements outpacing new builds. Investor sentiment is also improving because modern policy instruments, such as U.K. regulated asset-base models, lower borrowing costs that previously drove project cancellations. As a result, the Global nuclear power market is regaining relevance in national decarbonization roadmaps, particularly where storage costs for high-renewables scenarios remain prohibitive.

Lifetime Extension & Uprate Programs

Extending the operating life of existing reactors from 40 to 60 or even 80 years defers multi-billion-dollar replacement builds. The U.S. Nuclear Regulatory Commission approved 11 subsequent license renewals in 2024-2025, lifting the average remaining life of the domestic fleet to 28 years.[2]U.S. Nuclear Regulatory Commission, “Subsequent License Renewal 2025,” nrc.gov France’s EUR 49.4 billion Grand Carénage upgrades similarly add decades of output at a fraction of new-build cost. Uprate projects boost generation by 5-20% through equipment replacements that avoid greenfield permitting, achieving levelized costs below USD 30 per MWh versus more than USD 70 per MWh for new large reactors.[3]Électricité de France, “Grand Carénage Programme 2025 Progress Report,” edf.fr This strategy, however, concentrates fleet-age risk, making operational excellence and predictive maintenance critical to avoid unplanned outages that erode cost advantages.

Commercialization of Advanced SMRs

Factory-built SMRs promise shorter build times and smaller financing tickets, tackling the two biggest hurdles of conventional nuclear. NuScale won the first U.S. design certification for a light-water SMR and has firm orders for data-center applications, while Rolls-Royce SMR closed GBP 700 million of funding to progress its U.K. demonstrator. X-energy’s Xe-100 high-temperature gas reactor secured a construction permit in 2025, opening a path for non-light-water designs. These milestones de-risk technology, yet bankability still depends on serial production volumes that reduce per-module costs. Governments are therefore bundling multiple orders, such as the U.K.’s competitive SMR selection, to create a pipeline large enough for vendors to realize economies of scale.

Industrial Decarbonization Process-Heat Demand

Hard-to-abate sectors emit almost 7 gigatons of CO₂ each year. High-temperature reactors can supply steam above 500 °C or low-carbon hydrogen, cutting emissions where electrification is uneconomic. In 2025, ArcelorMittal and Nucor launched feasibility studies to integrate SMRs into steel mills, and Dow partnered with X-energy to decarbonize a chemicals plant in Texas. These projects value firm heat more than lowest-cost electricity, enabling reactors to capture premium tariffs. The driver’s impact intensifies as industrial-sector emission caps tighten across Europe and North America in the late 2020s.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost overruns & financing challenges | -0.18% | Global, acute in liberalized Western markets | Short term (≤ 2 years) |

| Competition from low-cost renewables | -0.12% | Europe, North America, Australia, parts of Asia | Medium term (2-4 years) |

| HALEU fuel-supply bottlenecks | -0.06% | North America, Europe (advanced reactor markets) | Medium term (2-4 years) |

| Export-control & proliferation scrutiny | -0.05% | Global, concentrated in emerging nuclear markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Overruns & Financing Challenges

High capital costs and construction delays continue to erode investor confidence. Vogtle 3-4 entered service at USD 35 billion, more than double the budget, while France’s Flamanville 3 consumed EUR 19.1 billion over 17 years. These overruns led to credit downgrades and forced governments to backstop utility balance sheets. First-of-a-kind engineering risk, supply-chain fragmentation, and evolving safety regulations all drive cost blowouts. Unless serial builds improve project delivery, the Global nuclear power market risks ceding ground to cheaper renewables in deregulated markets where levelized cost parity remains elusive.

HALEU Fuel-Supply Bottlenecks

Advanced reactors rely on uranium enriched to 5-20% U-235, but commercial enrichment plants rarely produce it. Centrus Energy’s Ohio demonstration cascade delivered just 20 kg in 2024, far below multi-ton annual demand forecasts. While the U.S. Department of Energy allocated USD 2.7 billion to scale domestic capacity, commercial output is unlikely before 2028. Export restrictions on Russia’s dominant HALEU supplier further tighten availability. Developers are therefore redesigning cores for conventional fuel or delaying projects, constricting the pace at which the Global nuclear power market can adopt compact, high-performance reactors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reactor Type: PWR Dominance Faces Breeder Renaissance

Pressurized light-water reactors captured 72.8% of the Global nuclear power market share in 2025, underpinned by standardized supply chains and decades of operational data.[4]International Atomic Energy Agency, “Nuclear Power Reactors in the World 2025 Edition,” iaea.org Fast breeder reactors, although a minor base, are forecast to grow at 21.4% CAGR, driven by Russia’s BN-800 and China’s CFR-600 programs that validate closed fuel cycles. Pressurized heavy-water designs remain strategically important for India and Canada, offering natural-uranium autonomy. Boiling water reactors lag due to post-Fukushima retrofits that extend outages and inflate O&M costs.

Fast breeder momentum signals a structural pivot for the Global nuclear power market. Breeders extract up to 60 times more energy per kilogram of uranium, easing resource constraints as demand climbs. Their ability to burn plutonium stockpiles also aligns with non-proliferation objectives. However, complex sodium-cooling systems pose fire-safety challenges, and high capital costs deter adoption without sovereign backing. Consequently, light-water designs will preserve scale advantage through 2031, but breeders introduce competitive tension that could reshape vendor landscapes after 2035.

By Reactor Size: Modular Units Disrupt Gigawatt Paradigm

Medium-sized plants between 500 and 1,000 MWe represented the largest slice of the Global nuclear power market size in 2025, balancing economies of scale with grid integration flexibility. Yet small reactors below 500 MWe are projected to surge at 20.1% CAGR, propelled by factory fabrication that slashes onsite labor and financing risk.

Capital-light modules appeal to emerging economies with weaker balance sheets, while industrial buyers need only a few hundred megawatts for captive loads. NuScale’s 77 MWe module and GE-Hitachi’s 300 MWe BWRX-300 anchor the commercial pipeline. Large reactors above 1,000 MWe retain a cost-per-kilowatt edge where policy guarantees long-term offtake, but decade-long build times expose sponsors to demand uncertainty. The size segmentation, therefore, emphasizes contrasting business models rather than mere engineering: incremental capacity for distributed demand versus bulk baseload for centralized grids.

By Fuel Type: HALEU Unlocks Compact Cores

Low-enriched uranium powered 87.5% of capacity in 2025, reflecting entrenched enrichment infrastructure and familiar regulatory regimes. HALEU adoption, forecast at 10.9% CAGR, unlocks higher power densities that lower capital cost per megawatt and support longer refueling cycles, a strong value proposition for remote or industrial sites where outages are costly. Mixed oxide fuel remains limited to France, Russia, and Japan, constrained by high fabrication costs.

Thorium’s pathway stays aspirational despite India’s progress, largely because global supply chains and licensing frameworks are unprepared. The Global nuclear power market, therefore, hinges on whether HALEU supply can scale fast enough to satisfy early SMR fleets. If bottlenecks persist, utilities may revert to conventional LEU designs, dampening the technology diversification anticipated for the 2030s.

By Application: Industrial Heat Gains Traction

Grid power dominated demand at 86.4% in 2025, yet industrial process heat is expanding at 14.7% CAGR as steel and chemical producers look beyond electrification for deep decarbonization. Off-grid micro-reactors target mining camps and Arctic communities where diesel exceeds USD 0.30 per kWh, while desalination projects such as the UAE’s Barakah cogeneration plant showcase water-energy integration.

Defense installations emerge as a niche where energy resilience outweighs cost, with the U.S. Department of Defense studying micro-reactors for Alaskan bases. Collectively, these non-electric applications re-price nuclear energy as an integrated heat-and-power solution, allowing the Global nuclear power market to diversify revenue beyond wholesale electricity.

By End-User Sector: Industrials Challenge Utility Dominance

Utilities and independent power producers controlled 87.7% of installed capacity in 2025. Industrial and petrochemical buyers, however, are set to expand at 12.0% CAGR, driven by Scope 1 emission reduction mandates and the economics of avoided transmission fees. Mining companies in Canada are evaluating SMRs to power off-grid extraction where diesel costs hit USD 0.40 per kWh.

Government and defense demand is also rising for strategic resilience, evidenced by Microsoft’s 20-year PPA to restart Three Mile Island for data centers. These shifts indicate a broader decentralization trend, where the Global nuclear power market evolves from utility-centric generation toward multi-industry service models.

Geography Analysis

Europe retained 39.1% of capacity in 2025, anchored by France’s 56-unit fleet that supplied 65% of national electricity. New builds in the United Kingdom, Poland, and the Czech Republic offset retirements in Germany and Belgium, stabilizing the region’s capacity through 2031. France started civil works on its first EPR2 at Penly in 2026, while Hinkley Point C in the U.K. targets a 2031 start to replace aging AGR reactors.

Asia-Pacific is the growth engine, expanding at 7.2% CAGR as China connected 22 reactors in 2024-2025 and India commissioned two indigenous 700 MWe heavy-water units. Japan’s phased restarts and South Korea’s policy reversal also add incremental capacity. The region’s regulatory agility and sovereign financing structures underpin bigger project pipelines than in liberalized Western markets.

North America’s outlook hinges on SMR demonstrations. Vogtle’s two AP1000 units added 2.2 GW, but future scale depends on cost-shared pilots such as TerraPower’s Natrium and Ontario Power Generation’s BWRX-300. The Middle East and Africa are early-cycle adopters: the UAE’s Barakah delivers 5.6 GW of baseload power, and Saudi Arabia has pre-qualified vendors for a 2.8 GW tender. South America’s pipeline centers on Brazil’s Angra 3 and Argentina’s CAREM-25, signaling a cautious but persistent regional interest.

Competitive Landscape

Nuclear Power Market is fragmented. Rosatom’s vertically integrated model secures export contracts in Tnal financing. China National Nuclear Corporation leverages its Hualong One reference builds at Karachi and Changjiang to court Southurkey, Egypt, and Bangladesh with concessioeast Asian buyers. Westinghouse’s AP1000 wins in Poland and Ukraine capitalize on geopolitical realignment that favors non-Russian technology.

SMR competition is more fragmented. GE-Hitachi’s BWRX-300 secured Canada’s first deployment, while Rolls-Royce and NuScale vie for the U.K. and U.S. market share. Balance-of-plant services remain contested by engineering giants such as Bechtel, Framatome, and Korea Hydro & Nuclear Power. Corporate PPAs, exemplified by Microsoft’s deal with Constellation, are introducing new corporate buyers who prize reliability over vendor nationality. Consequently, incumbents face erosion of their regulatory moats as smaller entrants exploit risk-informed licensing pathways to shorten time-to-market.

Nuclear Power Industry Leaders

GE-Hitachi Nuclear Energy

KEPCO Engineering & Construction

China National Nuclear Corporation

Westinghouse Electric Company LLC

SKODA JS AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Russia and Uzbekistan have initiated the construction of a nuclear power plant in Uzbekistan, marking the first such project in post-Soviet Central Asia. The plant is situated in Uzbekistan's central-eastern Jizzakh Region, which shares borders with Tajikistan and Kazakhstan. The design incorporates two types of nuclear reactors: two large units, each with a capacity of approximately 1,000 megawatts, and two small modular reactors, each generating around 55 megawatts.

- October 2025: Land acquisition for the Chutka nuclear power plant in Mandla, Madhya Pradesh, has been approved, and construction is expected to begin soon. Companies are identifying sites for small reactors as private participation is now permitted, with NPCIL supporting construction and operations.

- October 2025: NANO Nuclear has finalized the acquisition of Global First Power Ltd from USNC, securing key Canadian licensing assets. This acquisition facilitates the deployment of the KRONOS micro-modular reactor and strengthens a unified North American strategy for construction and regulatory advancements.

- September 2025: NTPC is preparing to acquire overseas uranium assets to secure fuel for future nuclear projects. The company has received board approval to conduct joint due diligence with UCIL, aligning with initiatives like ASHVINI to support the long-term growth of clean energy through nuclear power.

- September 2024: EDF announced a EUR 52 billion (USD 57 billion) investment program to construct 6 new EPR reactors in France, representing the largest nuclear expansion commitment in Europe since the 1980s.

Global Nuclear Power Market Report Scope

Nuclear power is derived from nuclear fission, nuclear decay, and nuclear fusion reactions. Most electricity produced by nuclear power is currently produced by nuclear fission in nuclear power plants using uranium and plutonium. Electricity derived from nuclear reactors, which generate heat by fission, is nuclear power. A nuclear power plant resembles a large coal-fired power plant in that it has pumps, valves, steam generators, turbines, electric generators, condensers, and other equipment similar to the reactor, which functions as a boiler in a fossil-fuel power plant.

The report also covers the installed capacity and estimates for the nuclear power market across the major regions. The report offers the installed capacity and forecasts for nuclear power capacity for all the above segments. The global nuclear power market report includes:

| Pressurized Light-Water Moderated and Cooled Reactor (PWR) |

| Pressurized Heavy-Water Moderated and Cooled Reactor (PHWR) |

| Boiling Light-Water Cooled and Moderated Reactor (BWR) |

| Gas Cooled, Graphite Moderated Reactor (GCR) |

| High-Temperature Gas-Cooled Reactor (HTGR) |

| Light-Water Cooled, Graphite Moderated Reactor (LWGR) |

| Fast Breeder Reactor (FBR) |

| Others |

| Large (Above 1,000 MWe) |

| Medium (500 to 1,000 MWe) |

| Small (Below 500 Mwe; includes SMRs and Micro-reactors) |

| Low-Enriched Uranium (Below 5% U-235) |

| High-Assay LEU (5 to 20% U-235) |

| Mixed Oxide (MOX) |

| Thorium-based Fuels |

| Grid-Connected Power |

| Off-grid/Remote Electrification |

| Industrial Process Heat and Steam |

| Desalination and District Heating |

| Defense and Military Bases |

| Utilities and IPPs |

| Industrial and Petro-chemical |

| Mining and Remote Operations |

| Government/Defense |

| Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| France | |

| Sweden | |

| Spain | |

| Ukraine | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Reactor Type | Pressurized Light-Water Moderated and Cooled Reactor (PWR) | |

| Pressurized Heavy-Water Moderated and Cooled Reactor (PHWR) | ||

| Boiling Light-Water Cooled and Moderated Reactor (BWR) | ||

| Gas Cooled, Graphite Moderated Reactor (GCR) | ||

| High-Temperature Gas-Cooled Reactor (HTGR) | ||

| Light-Water Cooled, Graphite Moderated Reactor (LWGR) | ||

| Fast Breeder Reactor (FBR) | ||

| Others | ||

| By Reactor Size | Large (Above 1,000 MWe) | |

| Medium (500 to 1,000 MWe) | ||

| Small (Below 500 Mwe; includes SMRs and Micro-reactors) | ||

| By Fuel Type | Low-Enriched Uranium (Below 5% U-235) | |

| High-Assay LEU (5 to 20% U-235) | ||

| Mixed Oxide (MOX) | ||

| Thorium-based Fuels | ||

| By Application | Grid-Connected Power | |

| Off-grid/Remote Electrification | ||

| Industrial Process Heat and Steam | ||

| Desalination and District Heating | ||

| Defense and Military Bases | ||

| By End-User Sector | Utilities and IPPs | |

| Industrial and Petro-chemical | ||

| Mining and Remote Operations | ||

| Government/Defense | ||

| Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Sweden | ||

| Spain | ||

| Ukraine | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is capacity in the Global nuclear power market expected to grow through 2031?

Installed capacity is projected to rise from 409.90 gigawatt in 2026 to 425 gigawatt by 2031, a 0.73% CAGR that masks faster growth in Asia-Pacific and advanced SMRs.

Which reactor type will expand the quickest?

Fast breeder reactors lead with a 21.4% CAGR through 2031, driven by Russia, China, and India commercializing closed fuel cycles.

Why are small modular reactors attracting attention now?

Factory fabrication lowers construction risk and capital outlay, enabling small reactors below 500 MWe to grow at 20.1% CAGR while serving industrial and remote sites.

What is the main bottleneck for advanced reactor deployment?

Limited HALEU enrichment capacity, with commercial-scale output unlikely before 2028, is delaying several U.S. and European projects.

Which region adds the most new capacity?

Asia-Pacific leads with a 7.2% CAGR to 2031, thanks to China's aggressive build program and India's indigenous heavy-water fleet expansion.

How are industrial buyers using nuclear energy?

Steel and chemical companies plan to integrate high-temperature reactors for process heat and hydrogen, cutting on-site emissions without relying on grid electricity.

Page last updated on: