Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

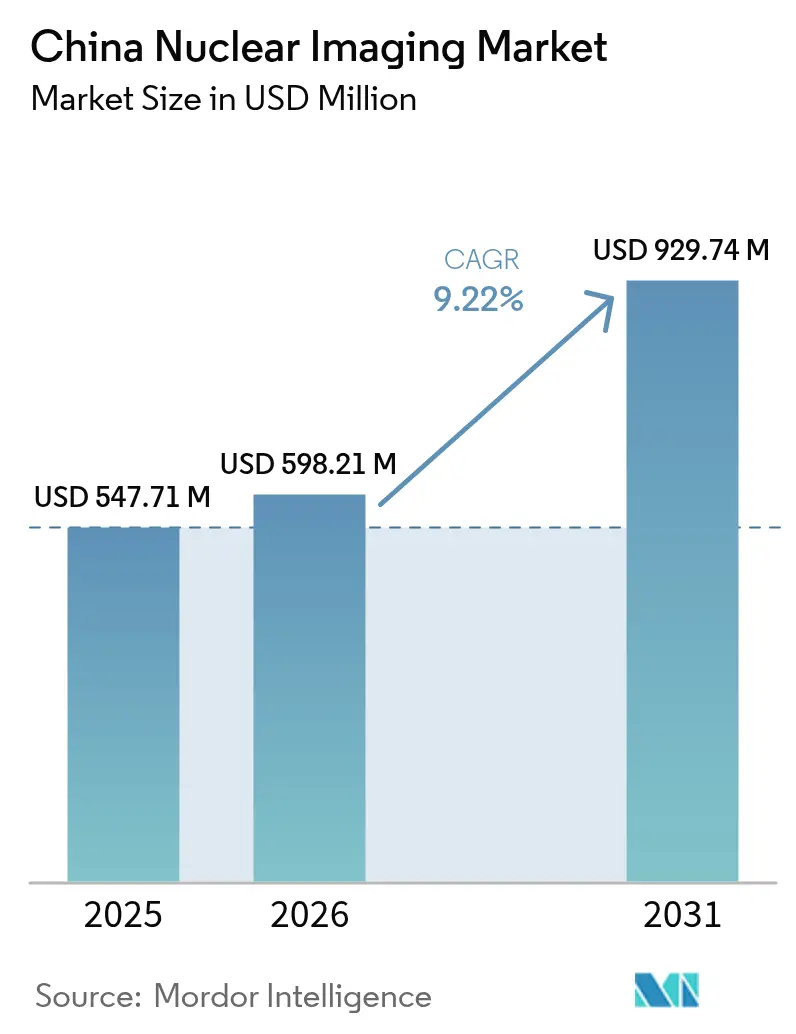

| Base Year Market Size (2025) | USD 547.71 Million |

| Market Size (2026) | USD 598.21 Million |

| Market Size (2031) | USD 929.74 Million |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

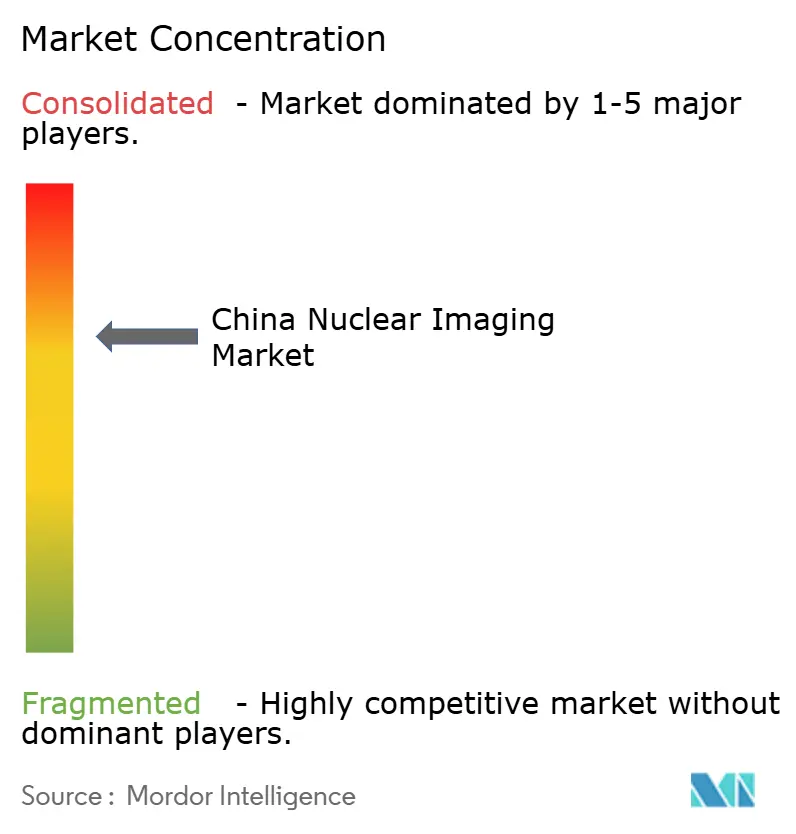

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Nuclear Imaging Market Analysis by Mordor Intelligence

The China Nuclear Imaging Market size is expected to grow from USD 547.71 million in 2025 to USD 598.21 million in 2026 and is forecast to reach USD 929.74 million by 2031 at 9.22% CAGR over 2026-2031.

China's nuclear imaging market is experiencing robust growth, driven by policy-backed advancements in isotope manufacturing, rapid adoption of total-body PET technology, and the anticipated commercial launch of radioligand therapies by late 2025. Over the past two years, the market has transitioned from hardware-centric revenue streams to a focus on consumables, supported by the establishment of domestic production lines for Lu-177, Mo-99, and Y-90. This shift has reduced import costs and stabilized tracer supply. Larger provincial hospitals are upgrading from ≤26 cm axial PET/CT systems to full-body systems to manage increasing patient volumes, while tier-2 imaging centers are addressing service gaps in regions underserved by tertiary hospitals. Additionally, provincial reimbursement pilots prioritizing cost-effectiveness over budget constraints are accelerating the approval of innovative equipment and tracers. Competitive dynamics are intensifying, with nearly 100 radiopharmaceutical start-ups leveraging RMB 5 billion in 2025 venture funding to explore untapped opportunities in neurology and cardiology imaging.

Key Report Takeaways

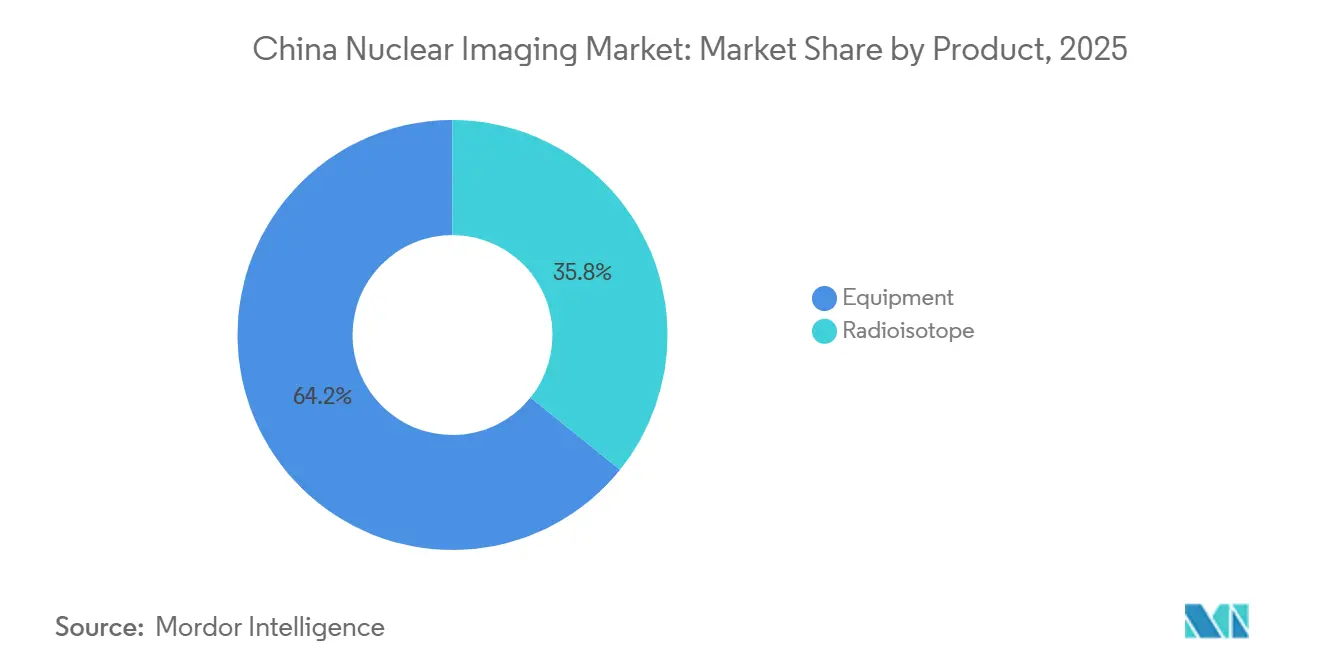

- By product, equipment commanded 64.23% of the China nuclear imaging market share in 2025, yet radioisotopes are forecast to expand at an 11.54% CAGR to 2031, overtaking hardware revenue.

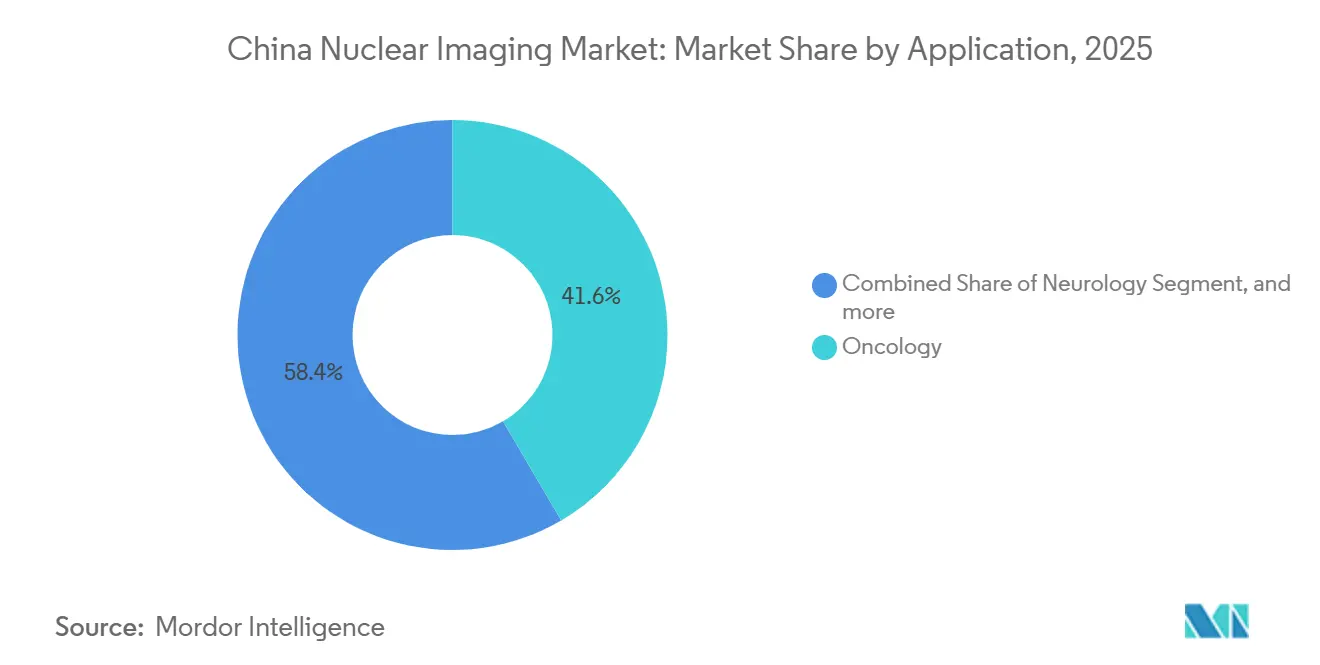

- By application, oncology led with 41.56% revenue share in 2025, while neurology is projected to advance at an 11.67% CAGR through 2031.

- By end user, hospitals accounted for 65.43% of the China nuclear imaging market size in 2025; diagnostic imaging centers recorded the fastest growth at 10.54% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Nuclear Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing oncology and cardiology disease burden | +2.1% | Eastern provinces | Medium term (2-4 years) |

| National healthcare reform and policy support | +1.8% | Pilot provinces, national roll-out | Long term (≥ 4 years) |

| Demographic aging and rising healthcare expenditure | +1.5% | Tier-1 cities | Long term (≥ 4 years) |

| Expansion of domestic radioisotope production capacity | +2.3% | National hubs (Qinshan, Mianyang) | Medium term (2-4 years) |

| Technological advancements in nuclear imaging modalities | +1.2% | Top-tier academic centers | Short term (≤ 2 years) |

| Export-oriented government incentives for radiopharmaceuticals | +0.3% | Manufacturing belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Oncology and Cardiology Disease Burden

China registered 4.82 million new cancer cases and 2.57 million deaths in 2022, reshaping demand for the China nuclear imaging market[1]Journal of Nuclear Medicine, “Nationwide Cancer Incidence 2024,” jnm.org . Lung cancer alone contributed 1.06 million diagnoses, ensuring sustained PET/CT utilization for thoracic oncology. A 2024 trial showed that the nectin-4 tracer [68Ga]Ga-N188 matched 18F-FDG sensitivity while improving specificity for triple-negative breast cancer, signaling the diversification of tracers. Cardiology imaging remains nascent, yet autopsy data indicating 68.2% latent coronary disease in HFpEF patients position SPECT and PET perfusion protocols for growth. Clinical guidelines that endorse SPECT myocardial perfusion imaging as a first-line diagnosis, plus the emergence of 68Ga-FAPI for cardiac fibrosis, add incremental volume. Combined, these disease trends are expected to lift annual nuclear medicine exam penetration above the 0.28% baseline recorded in 2024.

National Healthcare Reform and Policy Support

The December 2024 Circular No. 53 cut clinical-trial review windows to 30 days in pilot provinces and shifted reimbursement assessment toward cost-effectiveness[2]Journal of Nuclear Medicine, “Circular No. 53 Policy Update,” jnm.org . As a result, NMPA approvals for radiopharmaceuticals rose from ≈30 agents in 2022 to >40 by 2025. Fast-track licensing for Class IV user facilities also eased hospital entry barriers, although only 65 institutions held these permits in 2025. The Mid- and Long-Term Development Plan for Medical Isotopes (2021-2035) mandates nuclear medicine departments across all 2,749 Class 3 hospitals plus 2,000 additional sites, effectively doubling the addressable footprint for the China nuclear imaging market. While fragmented, reimbursement now accommodates cost-utility metrics, encouraging provinces to pilot coverage for expensive modalities such as total-body PET.

Demographic Aging and Rising Healthcare Expenditure

Adults aged≥65 years will account for 27% of China’s population by 2040, up from 14% in 2024, intensifying demand for neurodegenerative imaging [JNM.ORG]. A 1,073-patient amyloid-PET cohort at Huashan Hospital altered diagnoses in 19.3% of Alzheimer’s workups, demonstrating clinical utility. Total-body PET enables dual-tracer scans—11C-CFT and 18F-FDG—in 600 seconds, doubling daily throughput and aligning with elderly patients’ tolerance limits. Despite 0.305 PET scanners per million residents in 2024, versus 7.2 in the United States, provincial budgets earmark incremental capex for PET/CT as part of aging-care initiatives. These demographic and fiscal shifts add 1.5 percentage points to the forecast CAGR of the China nuclear imaging market.

Expansion of Domestic Radioisotope Production Capacity

CNNC launched Lu-177 lines at Qinshan in June 2025, with an annual output of≥10,000 curies, slashing import dependence for 177Lu-DOTATATE and 177Lu-PSMA treatments [JNM.ORG]. China Isotope & Radiation Corporation began building a Mo-99/Tc-99m reactor in January 2024, targeting 100,000 curies by 2027, sufficient for national SPECT demand. First-in-China production of Y-90 glass microspheres and C-14 in 2025 and 2024, respectively, diversifies tracer supply, while Eckert & Ziegler’s Ac-225 license agreement moves alpha-therapy precursors in-country. Improved isotope self-reliance stabilizes input costs, explains the 2.3 percentage-point CAGR uplift, and pivots the China nuclear imaging market toward consumables-led revenue.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and reimbursement constraints | -1.4% | Tier-2 and tier-3 cities | Medium term (2-4 years) |

| Logistical challenges of short-half-life isotopes | -0.9% | Western provinces | Short term (≤ 2 years) |

| Regulatory bottlenecks for cyclotron commissioning | -0.6% | Nationwide | Medium term (2-4 years) |

| Shortage of skilled nuclear medicine workforce | -0.8% | Tier-2 hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Reimbursement Constraints

Total-body PET units cost RMB 70-100 million (USD 9.8-14 million), roughly triple the cost of conventional PET/CT, straining hospital capex cycles when provincial reimbursement lists still price scans at RMB 6,000-9,000. Volume-based purchasing further squeezed 18F-FDG tariffs by 33% between 2022 and 2024, stretching equipment payback to eight-plus years. Catastrophic out-of-pocket ceilings of RMB 400,000-450,000 discourage multi-cycle 177Lu therapies, muting consumable pull-through. Independent imaging centers navigate multi-agency licensing that may take 18 months, delaying revenue realization and trimming the CAGR of the China nuclear imaging market by 1.4 percentage points.

Logistical Challenges of Short-Half-Life Isotopes

China’s 148 cyclotrons in 2024 clustered in the east, leaving Xinjiang and Qinghai reliant on air freight that adds RMB 2,000-5,000 per 18F-FDG dose. Only 10 sites run 82Rb generators versus >200 in the U.S., curbing cardiac PET expansion. Technetium shortages following 2024 European reactor outages forced appointment rescheduling, exposing supply fragility until China Isotope’s Mo-99 reactor comes online in 2027. These logistical frictions shave 0.9 percentage points off the China nuclear imaging market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Domestic Isotope Push Reshapes Revenue Mix

Equipment generated 64.23% of the China nuclear imaging market share in 2025, buoyed by ≈20 total-body PET installations and photon-counting CT launches. However, radioisotopes are on track for an 11.54% CAGR through 2031 as Qinshan’s Lu-177 and future Mo-99 reactors underpin supply. Consequently, the China nuclear imaging market size for consumables is expected to surpass equipment sales by 2029. Competitive dynamics favor state-owned CNNC and growing private players that secure long-term supply contracts with academic centers.

The projected shift toward a consumables-driven model supports recurring revenue streams, stabilizing profitability despite price compression in scanners. Y-90 glass microsphere rollouts and Ac-225 partnerships add high-margin therapy isotopes that deepen the moat for early movers. United Imaging’s strategy now pairs hardware with tracer-agnostic service bundles, a logical hedge as the China nuclear imaging market transitions to isotope-led growth.

By Application: Oncology Dominance Masks Neurology’s Velocity

Oncology contributed 41.56% of 2025 revenue, underpinned by lung-cancer prevalence and November 2025 approval of Pluvicto. Novel PET tracers such as nectin-4 and CLDN18.2 are widening the diagnostic funnel, and FAPI theranostic pairs promise procedure upsell. Even so, neurology will log the highest CAGR at 11.67%, supported by 600-second total-body PET dual-tracer protocols. By 2031, neurology’s share of the China nuclear imaging market size could advance 3-4 percentage points, fueled by tau-PET approvals and reimbursement expansion.

Cardiology remains a low-volume niche today, but guideline revisions and 68Ga-FAPI’s superior uptake in fibrosis position it for catch-up growth. Thyroid and infection imaging stay steady yet undifferentiated, offering limited incremental upside. Collectively, application diversification cushions the China nuclear imaging market from oncology reimbursement risk.

By End User: Imaging Centers Exploit Tier-2 White Space

Hospitals accounted for 65.43% of 2025 revenue, reflecting their lock on Class IV tracer licenses and established radiopharmacies. Diagnostic imaging centers, however, are expanding at 10.54% CAGR as private operators rush into tier-2 locales where nuclear medicine coverage remains under 35%. This segment’s agility—free from multispecialty hospital bureaucracy—allows targeted high-margin oncology scans that lift average revenue per unit.

Mid-term policy pledges to equip every Class 3 hospital plus 2,000 additional facilities by 2035 equate to 3,000-4,000 new scanners, but staffing and isotope supply will dictate the pace. Imaging-center growth hedges against hospital procurement lulls, ensuring the China nuclear imaging market retains demand momentum across diverse care settings.

Competitive Landscape

Roughly 100 radiopharmaceutical entrants since 2019 created a fragmented field, yet fewer than 10 organizations hold Class IV licenses, consolidating advanced-tracer synthesis among elite centers. United Imaging commands the premium scanner niche with 20 total-body PET systems and the photon-counting uCT Ultima, edging overseas brands on installed base. CNNC and China Isotope dominate isotope manufacture, while private players like Sinotau build GMP lines to chase export upside under new policy incentives.

Strategic plays include Novartis’s local Lu-177 facility and Eckert & Ziegler’s Ac-225 pact, which target scarcity isotopes poised for alpha-therapy expansions. Technology bets focus on AI dosimetry and high-sensitivity SPECT prototypes, raising competitive stakes for data science capabilities. With hospitals in tier-1 cities nearing equipment saturation, white-space capture in tier-2 geographies and isotopes offers the clearest growth runway for incumbents and challengers in the China nuclear imaging market.

Blue Sail Medical’s patent on a cooled nuclear-tomography system and Tsinghua University’s clinical-grade gamma cameras demonstrate a flourishing innovation ecosystem that erodes historical technology gaps. Overall, the China nuclear imaging industry exhibits moderate consolidation with active domestic-innovation forces reshaping competitive hierarchies.

China Nuclear Imaging Industry Leaders

Bracco Imaging SpA

Canon Inc.

Koninklijke Philips NV

Cardinal Health Inc.

General Electric Company (GE HealthCare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Curium established a legal entity in China, marking a significant step in its global expansion to improve cancer diagnosis and treatment. This new presence will strengthen collaborations and support the development of advanced radiopharmaceuticals in Asia.

- June 2025: CNNC launched Y-90 glass microsphere and Lu-177 production at Qinshan, removing reliance on European imports for key therapy isotopes

- January 2025: Eckert & Ziegler signed an Ac-225 license deal with a Chinese joint venture, enabling domestic alpha-emitter supply for targeted radionuclide therapy.

China Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear imaging is a medical imaging technique that uses radioactive tracers to visualize and diagnose abnormalities within the body. It provides functional information about organs and tissues by detecting radiation emitted from the tracers.

The China Nuclear Imaging Market Report is Segmented by Product (Equipment and Radio-isotope [SPECT Radio-isotopes and PET Radio-isotopes]), Application (Cardiology, Neurology, Thyroid, Oncology, and Other Applications), and End User (Hospitals, Diagnostic Imaging Centres, and Academic & Research Institutes). Market Forecasts are Provided in Terms of Value (USD). The report offers values in USD million for all the above-mentioned segments.

By Product

| Equipment | ||

| Radio-isotope | SPECT Radio-isotopes | Technetium-99m (TC-99m) |

| Thallium-201 (TI-201) | ||

| Gallium (Ga-67) | ||

| Iodine (I-123) | ||

| Other SPECT Radioisotopes | ||

| PET Radio-isotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (RB-82) | ||

| Other PET Radioisotopes | ||

By Application

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radio-isotope | SPECT Radio-isotopes | Technetium-99m (TC-99m) | |

| Thallium-201 (TI-201) | |||

| Gallium (Ga-67) | |||

| Iodine (I-123) | |||

| Other SPECT Radioisotopes | |||

| PET Radio-isotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (RB-82) | |||

| Other PET Radioisotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

Ow fast is the China nuclear imaging market expected to grow between 2026 and 2031?

It is projected to expand from USD 598.21 million in 2026 to USD 929.74 million in 2031, at a 9.22% CAGR.

Which segment will outpace overall growth?

Radioisotopes are set to grow 11.54% annually as domestic Lu-177 and Mo-99 output ramps up.

What is driving neurology imaging demand?

Total-body PET cut Parkinson's scan time to 600 seconds and amyloid PET altered dementia diagnoses in 19.3% of cases.

Why are diagnostic imaging centers expanding in tier-2 cities?

Fewer than 35% of tertiary hospitals in those areas host nuclear medicine departments, creating unmet demand for oncology PET.

What policy reform had the biggest market impact recently?

State Council Circular No. 53 in December 2024 shortened device and drug review cycles and introduced cost-effectiveness in reimbursement decisions.

Which companies lead isotope production?

State-owned CNNC and China Isotope drive Lu-177, Y-90, and future Mo-99 supply, while private Sinotau expands GMP capacity.

Page last updated on: