Japan Nuclear Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

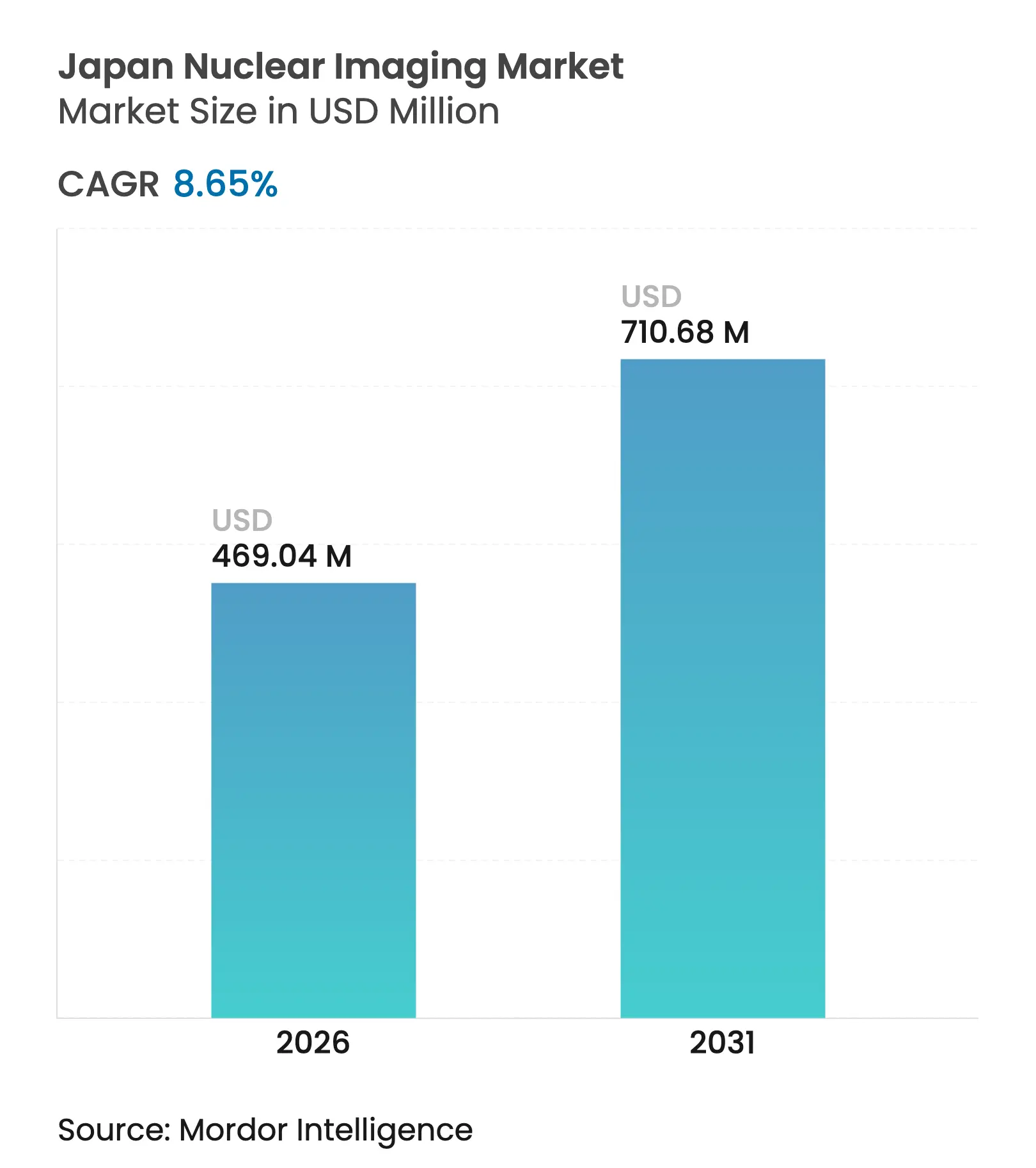

| Market Size (2026) | USD 469.04 Million |

| Market Size (2031) | USD 710.68 Million |

| Growth Rate (2026 - 2031) | 8.65 % CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Japan Nuclear Imaging Market Analysis by Mordor Intelligence

Japan nuclear imaging market size in 2026 is estimated at USD 469.04 million, growing from 2025 value of USD 431.71 million with 2031 projections showing USD 710.68 million, growing at 8.65% CAGR over 2026-2031. Japan’s well-funded universal health-insurance system, rapid population aging, and deep installed base of SPECT and PET scanners make it the world’s most densely equipped diagnostic-imaging environment. Government incentives that link green-transformation spending to domestic isotope production, combined with hospital demand for AI-enhanced workflow tools, fuel steady equipment upgrades[1]Source: Ministry of Economy, Trade and Industry, “Revision of Sector-Specific Investment Strategies,” meti.go.jp . Strategic consolidation, highlighted by GE HealthCare’s full acquisition of Nihon Medi-Physics, is reshaping supplier power and accelerating local radiopharmaceutical innovation. Simultaneously, breakthroughs in alpha-particle therapy isotopes and deep-learning reconstruction algorithms are opening precision-oncology revenue streams that offset reimbursement pressure on conventional SPECT cardiac studies.

Key Report Takeaways

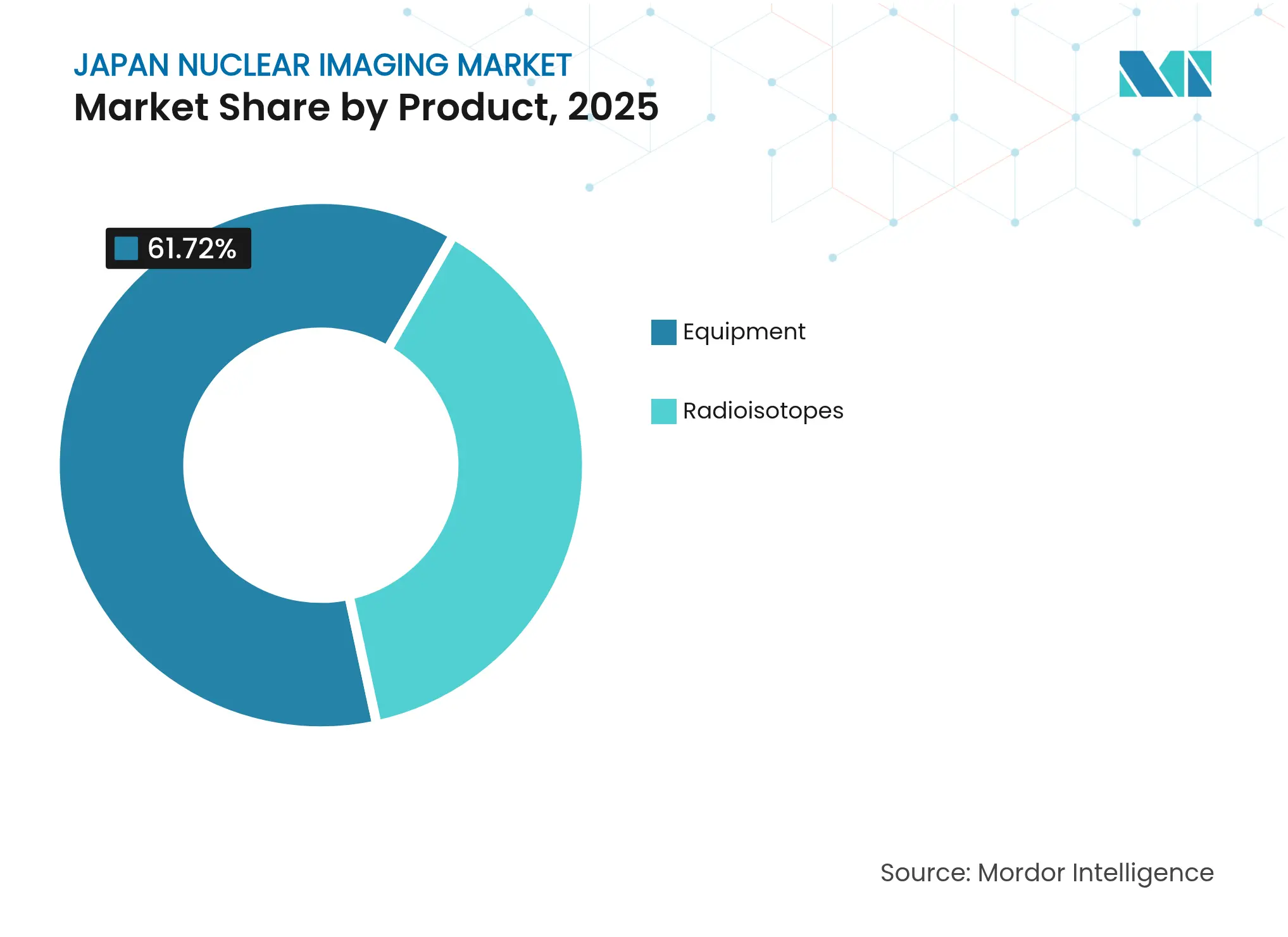

- By product, Equipment held 61.72% of Japan nuclear imaging market share in 2025, while Radiosiotopes is forecast to grow at a 9.35% CAGR through 2031.

- By application, cardiology led with a 36.35% revenue share in 2025; neurology is projected to expand at a 9.78% CAGR to 2031.

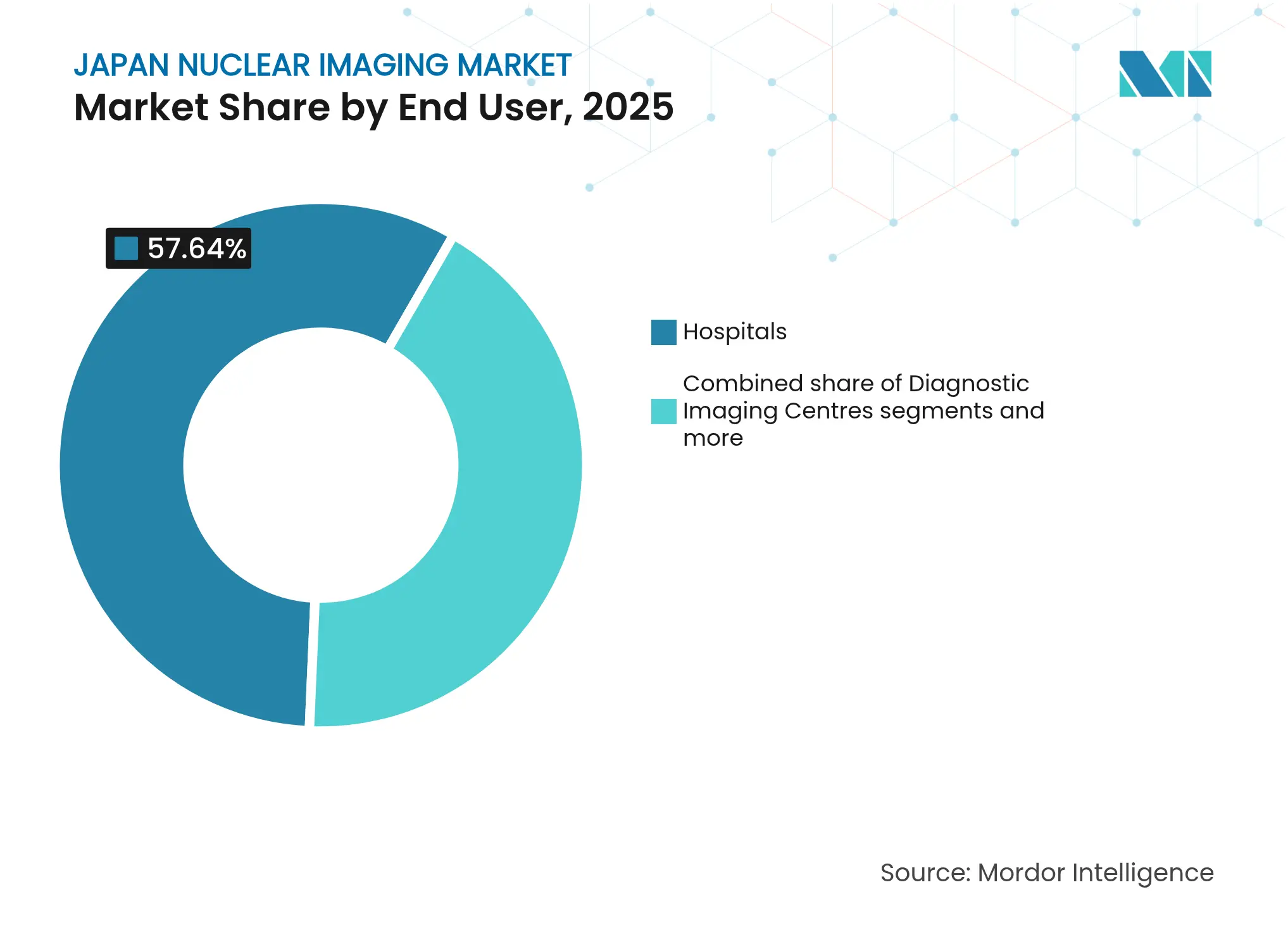

- By end user, hospitals accounted for 57.64% of the Japan nuclear imaging market size in 2025, whereas diagnostic imaging centers are advancing at a 10.38% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Nuclear Imaging Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin | |||

|---|---|---|---|---|---|---|

Rising prevalence of cardiovascular diseases in aging population Rising prevalence of cardiovascular diseases in aging population | +2.1% | National, concentrated in metropolitan areas | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:National, concentrated in metropolitan areas | Impact Timelin:Long term (≥ 4 years) |

Expanding insurance coverage for advanced imaging Expanding insurance coverage for advanced imaging | +1.8% | National, with rural prefecture benefits | Medium term (2-4 years) | |||

Government funding for theranostic isotope production capabilities Government funding for theranostic isotope production capabilities | +1.5% | National, focused on Fukushima and Osaka research hubs | Long term (≥ 4 years) | |||

Integration of AI-based reconstruction algorithms improving image quality Integration of AI-based reconstruction algorithms improving image quality | +1.2% | National, early adoption in university hospitals | Short term (≤ 2 years) | |||

Surging demand for precision oncology companion diagnostics Surging demand for precision oncology companion diagnostics | +1.4% | National, concentrated in cancer centers | Medium term (2-4 years) | |||

Rapid adoption of outpatient imaging centers Rapid adoption of outpatient imaging centers | +0.9% | Urban areas, expanding to suburban markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Cardiovascular Diseases in Aging Population

Japan now counts more than 36 million residents aged 65 years or older, driving persistent demand for nuclear cardiology examinations that evaluate myocardial perfusion with technetium-99m agents. Hospitals are prioritizing high-sensitivity SPECT/CT upgrades to identify sub-clinical ischemia in asymptomatic seniors, a shift aligned with the Japan Radiological Society database that houses roughly 500 million de-identified images for AI training. Deep-learning reconstruction tools shorten acquisition times, lowering patient dose while preserving resolution, which improves throughput in congested urban facilities. Government policy encouraging value-based radiology further cements functional imaging as a standard work-up ahead of costly interventional procedures. The demographic effect therefore establishes a long-run volume floor for SPECT cardiac services despite competitive CT angiography technologies.

Expanding Insurance Coverage for Advanced Imaging

In April 2025, the Ministry of Health, Labour and Welfare broadened reimbursement for florbetapir-18F amyloid PET from diagnostic use to post-treatment monitoring of Alzheimer’s therapy, cutting out-of-pocket costs and incentivizing facilities to install additional PET capacity. Similar coverage shifts are under review for PSMA-targeted tracers and theranostic agents, signaling a reimbursement pathway that links early detection to long-term cost containment. Rural prefectures benefit disproportionately because expanded coverage offsets travel expenses to metropolitan hospitals. Insurers also tie higher scan fees to adherence with AI-enabled dose-reduction protocols, encouraging adoption of advanced reconstruction software. As a result, payer policy increasingly guides purchasing decisions toward hybrid PET/MRI systems and AI-ready SPECT cameras.

Government Funding for Theranostic Isotope Production Capabilities

Post-Fukushima revitalization grants now subsidize domestic cyclotron and superconducting-accelerator projects that fabricate astatine-211 and actinium-225 for targeted alpha therapy. The RiSA superconducting electron accelerator achieved a 5 MV/m gradient in June 2025, a milestone toward local actinium-225 mass production by 2027. Parallel efforts at Osaka University and Hiroshima University support Phase I/II trials that aim to treat refractory thyroid and glioma tumors with alpha emitters. These investments decrease exposure to global Mo-99 volatility, strengthen supply independence, and position Japan as an exporter of high-value theranostic isotopes.

Integration of AI-Based Reconstruction Algorithms Improving Image Quality

Canon Medical’s Aquilion ONE/INSIGHT CT and GE’s Omni Legend PET/CT employ deep-learning pipelines that cut acquisition time by 50% while enhancing contrast recovery. A 50-layer 3D ResNet model now estimates Centiloid scores from amyloid PET without MRI co-registration, a step that can scale dementia screening to community clinics. AI-driven noise-reduction filters permit technologists to halve radiopharmaceutical dose, a valuable benefit amid isotope supply constraints. Early adopters—predominantly university hospitals—report throughput gains that offset software licensing fees within two years. Vendors are therefore embedding AI modules at the firmware level to appeal to cost-sensitive regional medical centers.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Chronic shortage of Mo-99 global supply chain disruptions Chronic shortage of Mo-99 global supply chain disruptions | -1.6% | Global impact, affecting Japan's import-dependent facilities | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.6% | Geographic Relevance:Global impact, affecting Japan's import-dependent facilities | Impact Timeline:Short term (≤ 2 years) |

Stringent regulatory hurdles for cyclotron installation licenses Stringent regulatory hurdles for cyclotron installation licenses | -1.1% | National, particularly affecting rural and smaller facilities | Long term (≥ 4 years) | |||

Competition from rapid CT/MRI advances reducing SPECT reimbursements Competition from rapid CT/MRI advances reducing SPECT reimbursements | -0.8% | National, concentrated in competitive urban markets | Medium term (2-4 years) | |||

High capital expenditure limiting adoption in rural prefectures High capital expenditure limiting adoption in rural prefectures | -0.7% | Rural and semi-urban areas with limited healthcare budgets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Chronic Shortage of Mo-99 Global Supply Chain Disruptions

More than 85% of Japanese nuclear-medicine scans rely on technetium-99m, yet the isotope’s parent Mo-99 is sourced mainly from aging foreign reactors that face unplanned outages. Import delays force hospitals to reschedule procedures and divert demand to CT or MRI, cutting SPECT utilization. Research cyclotrons have validated proton bombardment of natural molybdenum to make carrier-free technetium-99m, but scaling remains capital intensive. The interim risk drives bulk-purchasing alliances among major hospital chains and supports government interest in domestic isotope plants.

Stringent Regulatory Hurdles for Cyclotron Installation Licenses

PMDA’s 2024 QMS revision added documentation on radiation shielding, waste management, and ISO 13485 alignment, extending average cyclotron licensing to 24 months[2]Source: PMDA, “Revision of Japanese Medical Device QMS requirements,” pmda.go.jp . Smaller rural hospitals often abandon installation plans, reinforcing geographic concentration of nuclear imaging in large metropolitan centers. While rigorous oversight sustains public confidence, it raises entry barriers for emerging theranostic start-ups. Large healthcare groups exploit this asymmetry by negotiating volume discounts with vendors and capturing referral flows from under-equipped regions.

Segment Analysis

By Product: Equipment Dominance Faces PET Innovation

Equipment accounted for 61.72% of Japan nuclear imaging market share in 2025, underscoring the modality’s entrenched role in routine cardiology and bone procedures. The segment’s installed base benefits from comparatively low capital cost, abundant technologist expertise, and versatile isotope chemistry. Modern cadmium-zinc-telluride detectors lift energy resolution and shorten scan times, features that preserve SPECT relevance against PET challengers. Vendors bundle AI-enabled dose-optimization software to align with insurer dose-ceiling rules, reinforcing replacement sales cycles.

Radioisotopes though representing a small fraction of equipment units, is projected to post a 9.35% CAGR through 2031, the fastest in the modality mix. Clinical uptake accelerates in neurology and oncology centers where simultaneous metabolic and soft-tissue imaging improves lesion characterization. Shimadzu’s FDA-cleared BresTome time-of-flight PET device marks Japan’s innovation push into organ-specific imaging. On the radioisotope side, technetium-99m retains volume leadership, yet fluorine-18 tracers grow briskly as cyclotron capacity expands. Emerging alpha emitters such as astatine-211 promise differentiated therapeutics, positioning equipment vendors to cross-sell shielded hot-cells and theranostic workflow software. Consequently, the Japan nuclear imaging market sees a dual track: high-volume SPECT installations in regional centers and premium PET/MRI suites in tertiary hospitals.

Note: Segment shares of all individual segments available upon report purchase

By Application: Cardiology Leadership Challenged by Neurology Growth

Cardiology held 36.35% of Japan nuclear imaging market in 2025 due to long-established reimbursement codes and strong physician familiarity with perfusion protocols. New SPECT/CT cameras delivering sub-10-minute exams help cardiology labs manage growing outpatient caseloads. However, neurology applications are projected to rise at a 9.78% CAGR through 2031, propelled by amyloid and tau PET reimbursement expansions and rapidly aging demographics.

AI models now quantify beta-amyloid burden without MRI co-registration, further lowering scan cost and time. Oncology remains the most dynamic cross-cutting field as theranostic agents link imaging to therapy response; PSMA-targeted PET for prostate cancer exemplifies this tight diagnostic-treatment feedback loop. Thyroid and bone scans maintain stable share but limited growth, acting as demand ballast during isotope shortages.

By End User: Diagnostic Centers Disrupting Hospital Dominance

Hospitals commanded 57.64% of Japan nuclear imaging market size in 2025, leveraging integrated electronic-medical-record networks and surgical backup to capture complex cases. Yet independent diagnostic imaging centers will post a 10.38% CAGR to 2031, fueled by outpatient pricing reforms and patient preference for shorter wait times. Kirishima City Medical Center’s dedicated PET-CT unit illustrates the trend toward community-based cancer screening services. Hospitals respond by spinning off imaging subsidiaries and co-locating scanners in outpatient malls.

Academic institutions, while smaller in revenue terms, continue to anchor clinical trials that validate novel isotopes such as copper-64-ATSM, reinforcing Japan’s status as a translational-research hub. The coexistence of multi-scanner hospitals and nimble imaging centers diversifies procurement channels for equipment manufacturers and widens patient access.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Japan nuclear imaging market penetration is highest in the Tokyo, Osaka, and Nagoya corridors, where tertiary hospitals adopt next-generation PET/MRI scanners early and act as reference sites for regional diffusion. Metropolitan dominance reflects population density, abundant subspecialty physicians, and research funding concentration. Rural prefectures suffer limited access because capital budgets cannot absorb cyclotron and hot-lab costs; PMDA licensing hurdles further stall installation. Mobile PET-CT programs and tele-diagnosis platforms partially bridge gaps, yet scan frequency per capita still trails urban averages by 30%. Fukushima’s radioisotope-production cluster leverages reconstruction funding to become a supply-chain anchor, shipping astatine-211 and actinium-225 across the archipelago. Kansai innovation zones around Osaka drive theranostic clinical trials, solidifying the region as a talent magnet for nuclear pharmacists. Hokkaido shows rising demand for cardiac SPECT because of higher ischemic-heart-disease prevalence yet relies on weekly isotope air freight. National health-insurance parity ensures patient co-pays remain flat regardless of location, but travel cost differentials perpetuate geographic inequity. Over the forecast period, government grants tied to regional revitalization are expected to stimulate two new mid-energy cyclotron projects outside the three megacities, gradually diffusing advanced imaging capacity.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

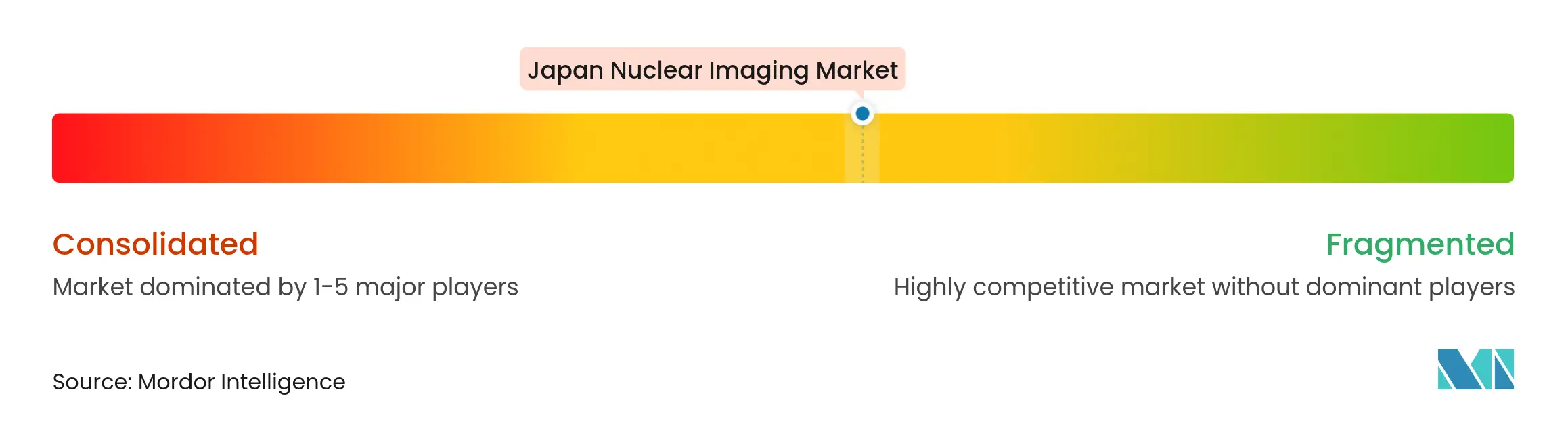

Market Concentration

The Japan nuclear imaging market contains a mix of global conglomerates and domestic specialists competing along technology, service, and supply-chain dimensions. GE HealthCare’s 100% ownership of Nihon Medi-Physics integrates reagent supply with scanner installed base, enabling bundled service contracts that lock in hospital accounts. Siemens Healthineers leverages digital twins and remote-service analytics to minimize downtime, a value proposition prized by high-volume diagnostic centers. Canon Medical differentiates through in-house AI pipelines that auto-protocol CT and PET exams, winning the 2024 Minnies award and solidifying brand loyalty among technologists.

Domestic manufacturers exploit niche strengths: Shimadzu focuses on specialized organ PET, while Neuspective pioneers generative-AI radiology-report engines that integrate smoothly with Japanese language workflows. Start-ups such as AMS Kikaku and NovAccel attract venture funding for theranostic isotope pipelines, reflecting investor confidence in long-run alpha-therapy demand. Competition is pivoting toward service ecosystems—remote scanner optimization, supply-chain resilience, and AI-based decision support—rather than pure hardware horsepower.

The Japan Medical Imaging and Radiological Systems Industries Association’s “Industry Vision 2030” promotes data-interoperable devices, pushing vendors to expose open APIs for clinical-decision-support plug-ins. Cost-of-capital advantages enjoyed by multinationals may narrow as yen-denominated financing remains cheap, enabling local firms to fund R&D for novel crystal detectors. Overall, supplier rivalry intensifies as reimbursement shifts reward image-quality gains and dose savings, not scan volume alone.

Japan Nuclear Imaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NovAccel achieved a 5 MV/m gradient in its superconducting accelerator RiSA, accelerating commercial actinium-225 manufacturing plans

- May 2025: LinkMed closed Series B funding of JPY 3 billion to advance copper-64 radiopharmaceutical clinical trials

- April 2025: GE HealthCare finalized the USD 183 million purchase of Nihon Medi-Physics, securing full control over Japan’s premier SPECT and PET tracer portfolio

Table of Contents for Japan Nuclear Imaging Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of cardiovascular diseases in ageing population

- 4.2.2Expanding insurance coverage for advanced imaging in Japan

- 4.2.3Government funding for theranostic isotope production capabilities

- 4.2.4Integration of AI-based reconstruction algorithms improving image quality

- 4.2.5Surging demand for precision oncology companion diagnostics

- 4.2.6Rapid adoption of out-patient imaging centers

- 4.3Market Restraints

- 4.3.1Chronic shortage of Mo-99 global supply chain disruptions

- 4.3.2Stringent regulatory hurdles for cyclotron installation licenses

- 4.3.3Competition from rapid CT/MRI advances reducing SPECT reimbursements

- 4.3.4High capital expenditure limiting adoption in rural prefectures

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product (Value)

- 5.1.1Equipment

- 5.1.1.1PET/CT Scanners

- 5.1.1.2SPECT/CT Scanners

- 5.1.1.3PET/MRI Scanners

- 5.1.2Radioisotopes

- 5.1.2.1SPECT Radioisotopes

- 5.1.2.1.1Technetium-99m (Tc-99m)

- 5.1.2.1.2Thallium-201 (Tl-201)

- 5.1.2.1.3Gallium-67 (Ga-67)

- 5.1.2.1.4Iodine-123 (I-123)

- 5.1.2.1.5Other SPECT Isotopes

- 5.1.2.2PET Radioisotopes

- 5.1.2.2.1Fluorine-18 (F-18)

- 5.1.2.2.2Rubidium-82 (Rb-82)

- 5.1.2.2.3Other PET Isotopes

- 5.2By Application (Value)

- 5.2.1Cardiology

- 5.2.2Neurology

- 5.2.3Thyroid

- 5.2.4Oncology

- 5.2.5Other Applications

- 5.3By End User (Value)

- 5.3.1Hospitals

- 5.3.2Diagnostic Imaging Centres

- 5.3.3Academic & Research Institutes

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1GE HealthCare

- 6.3.2Siemens Healthineers

- 6.3.3Canon Medical Systems Corporation

- 6.3.4Nihon Medi-Physics Co., Ltd.

- 6.3.5Fujifilm Healthcare Corporation

- 6.3.6Shimadzu Corporation

- 6.3.7Hitachi, Ltd. (Healthcare)

- 6.3.8Koninklijke Philips N.V.

- 6.3.9IBA (Ion Beam Applications SA)

- 6.3.10Bracco Imaging S.p.A.

- 6.3.11Cardinal Health, Inc.

- 6.3.12Eckert & Ziegler AG

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Japan Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer and cardiac and neurological disorders.

The Japanese Nuclear Imaging Market is Segmented by Product (Equipment and Radioisotope (SPECT Radioisotopes (Technetium-99m (TC-99m), Thallium-201 (TI-201), Gallium (Ga-67), Iodine (I-123), and Other SPECT Radioisotopes) and PET Radioisotopes (Fluorine-18 (F-18), Rubidium-82 (RB-82), and Other PET Radioisotopes), Application (SPECT Applications (Orthopedics, Thyroid, Cardiology, and Other SPECT Applications) and PET Applications (Oncology, Oncology, Neurology, and Other PET Applications). The report offers the value (in USD million) for the above segments.