United Kingdom Nuclear Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 417.98 Million |

| Market Size (2031) | USD 593.47 Million |

| Growth Rate (2026 - 2031) | 7.27 % CAGR |

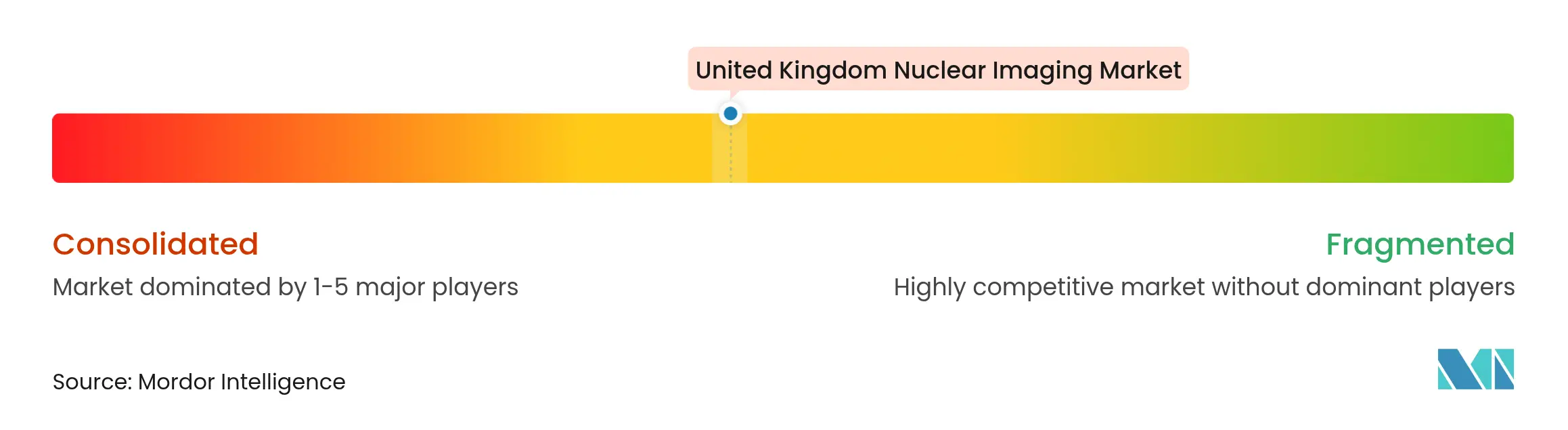

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United Kingdom Nuclear Imaging Market Analysis by Mordor Intelligence

The UK nuclear imaging market size was valued at USD 389.65 million in 2025 and estimated to grow from USD 417.98 million in 2026 to reach USD 593.47 million by 2031, at a CAGR of 7.27% during the forecast period (2026-2031). Strong NHS funding for early diagnosis, sovereign radioisotope-production projects that reduce 80% import reliance, and rapid adoption of digital detector technology collectively accelerate market expansion. Brexit-driven supply chain pressure has brought unprecedented urgency to build domestic isotope manufacturing capacity, notably through Wales’ GBP 400 million Project Arthur reactor. Novel PET and SPECT tracers are moving swiftly through MHRA approvals, while hospital Value Partnerships with equipment vendors optimize capital spending. Workforce shortages and reimbursement complexities temper growth but also create opportunities for technology-enabled efficiency gains across the UK nuclear imaging market .

Key Report Takeaways

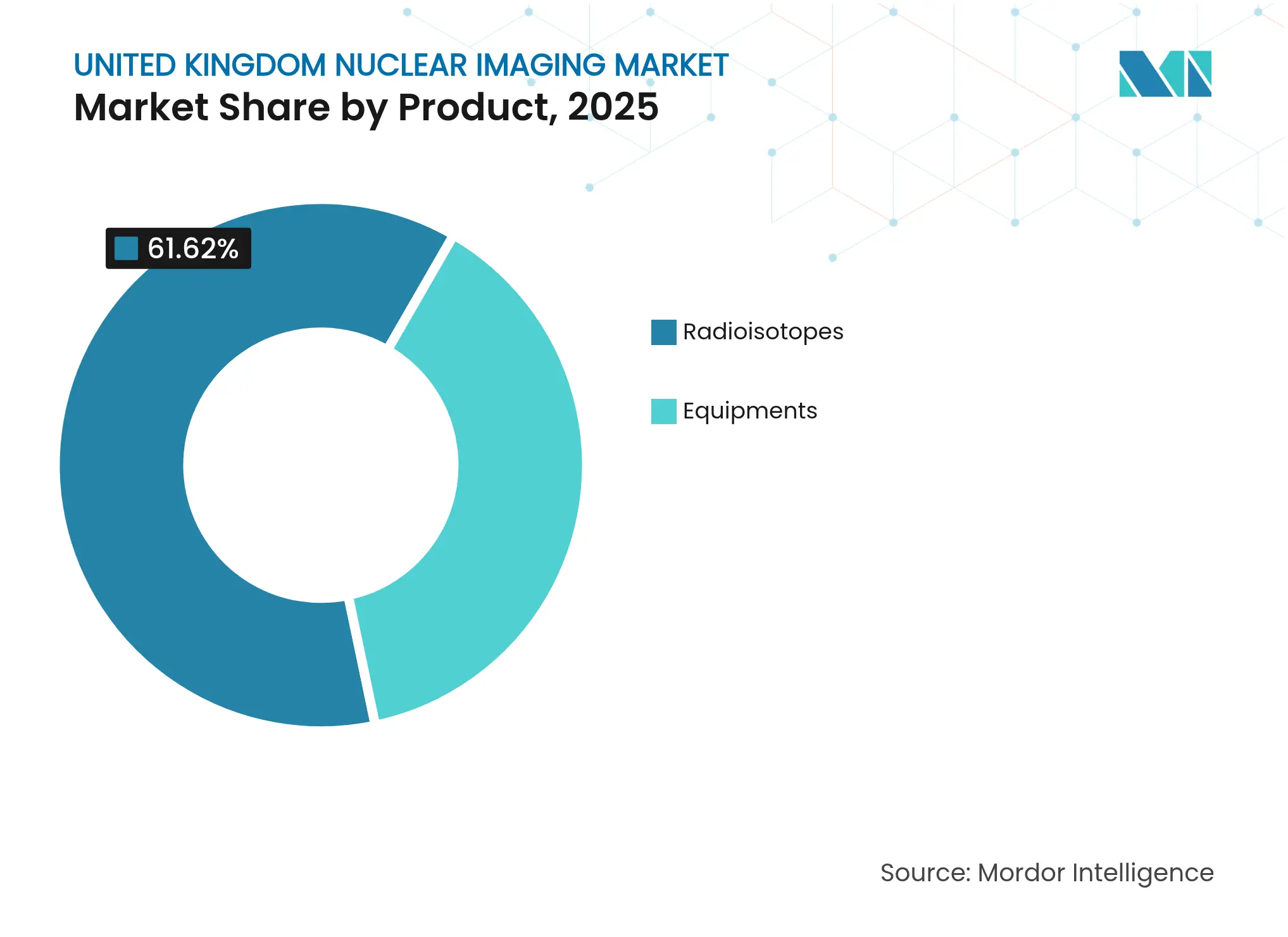

- By product, radioisotopes held 61.62% of UK nuclear imaging market share in 2025, radioisotopes are forecast to expand at a 9.42% CAGR through 2031.

- By application, oncology accounted for a 62.11% share of the UK nuclear imaging market size in 2025, neurology is projected to advance at a 9.86% CAGR between 2026-2031.

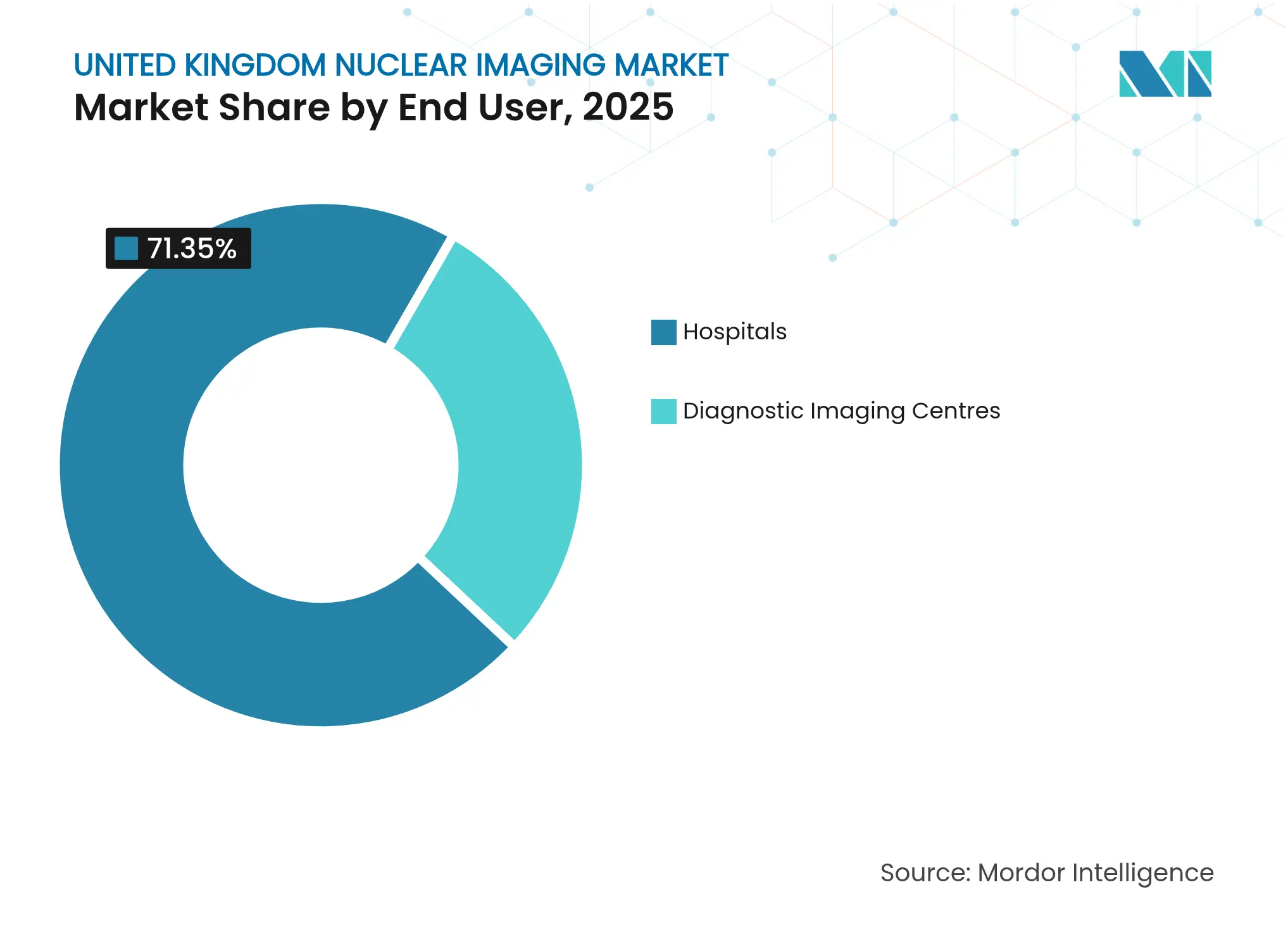

- By end user, hospitals captured 71.35% of UK nuclear imaging market share in 2025, diagnostic imaging centers are expected to post a 10.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Nuclear Imaging Market Trends and Insights

Rising Cancer Prevalence and PET-CT Adoption

Cancer diagnoses continue to climb, with 66,000 incidental cases recorded in the past year, representing one in five total diagnoses. Only 58.2% of patients received treatment within the 62-day referral-to-treatment window, well below the 85% target. NHS England responded by allocating GBP 70 million for radiotherapy equipment upgrades and launching the EDITH AI breast-cancer trial involving 700,000 women across 30 sites. Diagnostic waiting lists have swelled to 1.66 million, with nearly 500,000 patients awaiting CT or MRI, prompting wider adoption of nuclear medicine alternatives. Alliance Medical now delivers more than 50% of UK PET-CT scans through 46 static centers and 64 mobile scanners.

NHS Early-Diagnosis Funding Boosts Imaging Capacity

The National Cancer Plan prioritizes earlier detection, channeling GBP 130 million toward radiotherapy modernization that will replace 69 Linear Accelerators over three years. In November 2024, a total-body PET scanner was installed at St Thomas’ Hospital, achieving scan times below five minutes and feeding data into the National PET Imaging Platform. Siemens Healthineers has structured more than 30 Value Partnerships with NHS trusts to finance equipment and optimize workflows.

Rapid Detector Advances (Digital CZT, SiPM)

Kromek Group signed a USD 37.5 million, four-year contract with Siemens Healthineers to supply cadmium zinc telluride detectors, securing domestic manufacturing for high-resolution SPECT systems. Digital CZT and SiPM sensors shorten scan times, reduce radiation doses, and enable higher patient throughput across the UK nuclear imaging market . The British Nuclear Medicine Society reported equivalent image quality between high-sensitivity and ultra-high-sensitivity PET modes, supporting protocol optimization.

Pipeline of Novel PET/SPECT Radiotracers & Theranostics

MHRA granted a world-first approval to trofolastat (RoTecPSMA) for prostate-cancer imaging in March 2025, showing 94.2% sensitivity and 83.3% specificity. Curium closed its acquisition of Monrol to expand Lutetium-177 capacity. Blue Earth Therapeutics raised USD 77 million to fund PSMA-targeted therapy trials. GE HealthCare leads Thera4Care, a EUR 25.3 million Horizon Europe program that will standardize isotope production and deploy AI-enabled decision support.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront cost of scanners & cyclotron facilities High upfront cost of scanners & cyclotron facilities | -1.1% | UK-wide, acute in smaller NHS trusts | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:UK-wide, acute in smaller NHS trusts | Impact Timeline:Medium term (2-4 years) |

Complex UK reimbursement for new radiopharmaceuticals Complex UK reimbursement for new radiopharmaceuticals | -0.8% | England primary, devolved nations secondary | Short term (≤ 2 years) | |||

Workforce shortage of nuclear-medicine technologists Workforce shortage of nuclear-medicine technologists | -1.3% | UK-wide, severe in England | Short term (≤ 2 years) | |||

UK vulnerability to global Mo-99 supply disruptions UK vulnerability to global Mo-99 supply disruptions | -0.9% | UK-wide, critical for NHS operations | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost of Scanners & Cyclotron Facilities

The GBP 130 million Radiotherapy Modernisation Fund illustrates the scale of capital outlays confronting NHS trusts, with individual linear accelerators costing several million pounds. Siemens Healthineers’ GBP 250 million MRI factory in Oxford highlights the high expense of domestic manufacturing investments. Project Arthur’s GBP 400 million price tag represents the upper bound of infrastructure spending required for sovereign isotope production. Although NHS Supply Chain saved GBP 17.1 million through group purchasing, smaller trusts still struggle to finance state-of-the-art equipment without vendor partnerships.

Workforce Shortage of Nuclear-Medicine Technologists

The UK recorded a 30% shortfall in clinical radiologists and a 15% gap in clinical oncologists, feeding the 1.66 million patient diagnostic backlog. BNMS rebranded its practitioners group to broaden professional appeal and campaigns for mandatory Health Professions Council registration. GE HealthCare launched training grants to ease technologist shortages and secure qualified users for its installed base. The Institute of Physics and Engineering in Medicine calls for GBP 8 million annual funding to fill medical physics roles and mitigate safety risks.

Segment Analysis

By Product: Radioisotopes Drive Domestic Capability Expansion

Radioisotopes captured 61.62% of UK nuclear imaging market share in 2025, while the segment is forecast to grow at a 9.42% CAGR through 2031. The UK nuclear imaging market size for radioisotopes is on track to rise markedly as Project Arthur and private fusion initiatives bring local supply online. Technetium-99m shortages underscore dependency risks, prompting accelerated investment in PET and SPECT isotope manufacturing. Alliance Medical operates five radiopharmacies and distribution centers to stabilize supply, whereas equipment growth remains constrained by funding cycles. Nevertheless, King’s College London’s ultra-sensitive PET installation signals sustained demand for advanced scanners.

Limited capital budgets cause hospitals to stagger equipment upgrades, but the shift to digital detectors and combined PET/MRI systems will steadily lift the equipment sub-segment over the forecast. Cyclotron rollouts at major academic sites, coupled with MHRA approvals of tracers such as piflufolastat, will broaden local isotope portfolios and further enlarge the UK nuclear imaging market .

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology Leads, Neurology Accelerates

Oncology held 62.11% share of UK nuclear imaging market size in 2025 due to rising cancer incidence and priority NHS funding. Prostate-cancer imaging benefits from PSMA-targeting tracer approvals, while breast-cancer screening trials widen nuclear medicine pathways beyond symptomatic referrals. Neurology logged the fastest 9.86% CAGR outlook as quantum research hubs explore early Alzheimer’s detection. The Q-BioMed program’s GBP 19 million budget underscores public commitment to non-oncology nuclear medicine expansion.

Cardiology faces substitution from CT angiography, yet remains stable for perfusion studies, whereas thyroid applications maintain a reliable baseline driven by standardized iodine-based diagnostics. Overall, application diversification reduces reliance on single-disease demand and enhances resilience in the UK nuclear imaging market .

By End User: Diagnostic Centers Outpace Hospital Growth

Hospitals delivered 71.35% of UK nuclear imaging market share in 2025, reflecting centralized NHS pathways. However, Community Diagnostic Centres drive a 10.48% CAGR for independent imaging centers, relieving hospital backlogs and shortening patient journeys. Alliance Medical’s mobile PET-CT fleet allows flexible deployment, while Siemens Healthineers’ Value Partnerships embed long-term service contracts that stabilize hospital budgets.

Academic institutes leverage National PET Imaging Platform data repositories for drug discovery, sustaining steady scanner utilization. Updated Ionising Radiation regulations broaden practitioner licensing but add administrative workload across all end-user settings. This balanced expansion across settings supports sustainable growth for the wider UK nuclear imaging market .

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

England dominates through large-scale equipment installations and 30 NHS PET sites, benefiting from the GBP 130 million radiotherapy refresh. The region houses Siemens Healthineers’ new Oxford factory and Alliance Medical’s densest scanner network, translating into the highest regional UK nuclear imaging market size. Wales positions itself as a strategic isotope hub via Project Arthur, which could supply the entire UK upon completion and generate 200 high-skill jobs. Scotland leverages integrated health boards and research collaborations, while Northern Ireland utilizes shared procurement and cross-border referrals to maintain diagnostic access.

Persistent regional workforce gaps—most acute in England—drive adoption of tele-reporting and create opportunity for unified imaging networks. Uniform ARSAC guidance ensures consistent radiation safety, while the Civil Nuclear Roadmap targets indigenous fuel cycle capability, shaping a more self-reliant supply chain across all UK nations. Collectively, these regional dynamics foster balanced demand and resource sharing in the UK nuclear imaging market .

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The market exhibits moderate concentration. Alliance Medical supplies more than half of UK PET-CT scans via 110+ combined static and mobile units, securing multi-year NHS contracts that deter new entrants. Siemens Healthineers deepens localization with its GBP 250 million MRI plant and over 30 Value Partnerships, while GE HealthCare’s Thera4Care leadership positions it at the forefront of theranostic standardization. Emerging firms like Astral Systems pursue hospital-based fusion reactors, potentially disrupting traditional supply chains. Curium’s Monrol buyout expands therapeutic isotope reach, and Blue Earth’s funding round signals growing investor appetite.

Post-Brexit MHRA frameworks demand dual Grandfathering certificates and adherence to Windsor provisions, raising compliance costs. Vendors respond through local manufacturing footprints and joint NHS research initiatives, intensifying innovation within the UK nuclear imaging market .

United Kingdom Nuclear Imaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MHRA approved trofolastat (RoTecPSMA) for prostate-cancer imaging, marking the world’s first PSMA tracer using technetium-99m.

- February 2025: UK government launched the EDITH AI breast-cancer trial across 30 sites with GBP 11 million NIHR funding

Table of Contents for United Kingdom Nuclear Imaging Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising cancer prevalence and PET-CT adoption

- 4.2.2NHS early-diagnosis funding boosts imaging capacity

- 4.2.3Rapid detector advances (digital CZT, SiPM)

- 4.2.4Pipeline of novel PET/SPECT radiotracers & theranostics

- 4.2.5Sovereign radioisotope-production initiatives post-Brexit

- 4.2.6Integrated NHS Imaging Networks sharing scanner loads

- 4.3Market Restraints

- 4.3.1High upfront cost of scanners & cyclotron facilities

- 4.3.2Complex UK reimbursement for new radiopharmaceuticals

- 4.3.3Workforce shortage of nuclear-medicine technologists

- 4.3.4UK vulnerability to global Mo-99 supply disruptions

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product (Value)

- 5.1.1Equipment

- 5.1.1.1PET/CT Scanners

- 5.1.1.2SPECT/CT Scanners

- 5.1.1.3PET/MRI Scanners

- 5.1.2Radioisotopes

- 5.1.2.1SPECT Radioisotopes

- 5.1.2.1.1Technetium-99m (Tc-99m)

- 5.1.2.1.2Thallium-201 (Tl-201)

- 5.1.2.1.3Gallium-67 (Ga-67)

- 5.1.2.1.4Iodine-123 (I-123)

- 5.1.2.1.5Other SPECT Isotopes

- 5.1.2.2PET Radioisotopes

- 5.1.2.2.1Fluorine-18 (F-18)

- 5.1.2.2.2Rubidium-82 (Rb-82)

- 5.1.2.2.3Other PET Isotopes

- 5.2By Application (Value)

- 5.2.1Cardiology

- 5.2.2Neurology

- 5.2.3Thyroid

- 5.2.4Oncology

- 5.2.5Other Applications

- 5.3By End User (Value)

- 5.3.1Hospitals

- 5.3.2Diagnostic Imaging Centres

- 5.3.3Academic & Research Institutes

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1GE HealthCare

- 6.3.2Siemens Healthineers

- 6.3.3Canon Medical Systems Corporation

- 6.3.4Koninklijke Philips N.V.

- 6.3.5Curium Pharma

- 6.3.6Cardinal Health Inc.

- 6.3.7Bracco Imaging S.p.A.

- 6.3.8Telix Pharmaceuticals Ltd.

- 6.3.9Alliance Medical (Life Healthcare Group)

- 6.3.10Advanced Accelerator Applications S.A. (Novartis)

- 6.3.11Blue Earth Diagnostics Ltd.

- 6.3.12Eckert & Ziegler AG

- 6.3.13Theragnostics Ltd.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

United Kingdom Nuclear Imaging Market Report Scope

Nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer, and cardiac and neurological disorders. The United Kingdom Nuclear Imaging market is segmented by Product (Equipment, Diagnostic Radioisotope), and Application (SPECT Applications, PET Applications). The Report offers the value (in USD million) for the above segments.