Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

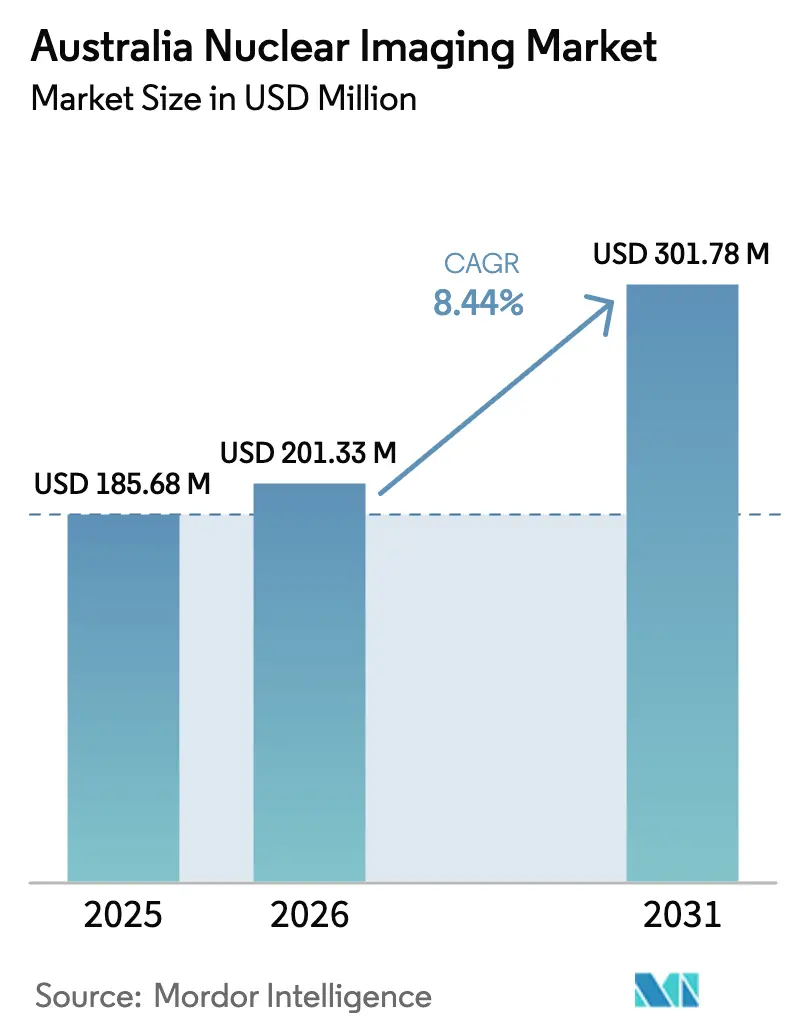

| Base Year Market Size (2025) | USD 185.68 Million |

| Market Size (2026) | USD 201.33 Million |

| Market Size (2031) | USD 301.78 Million |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

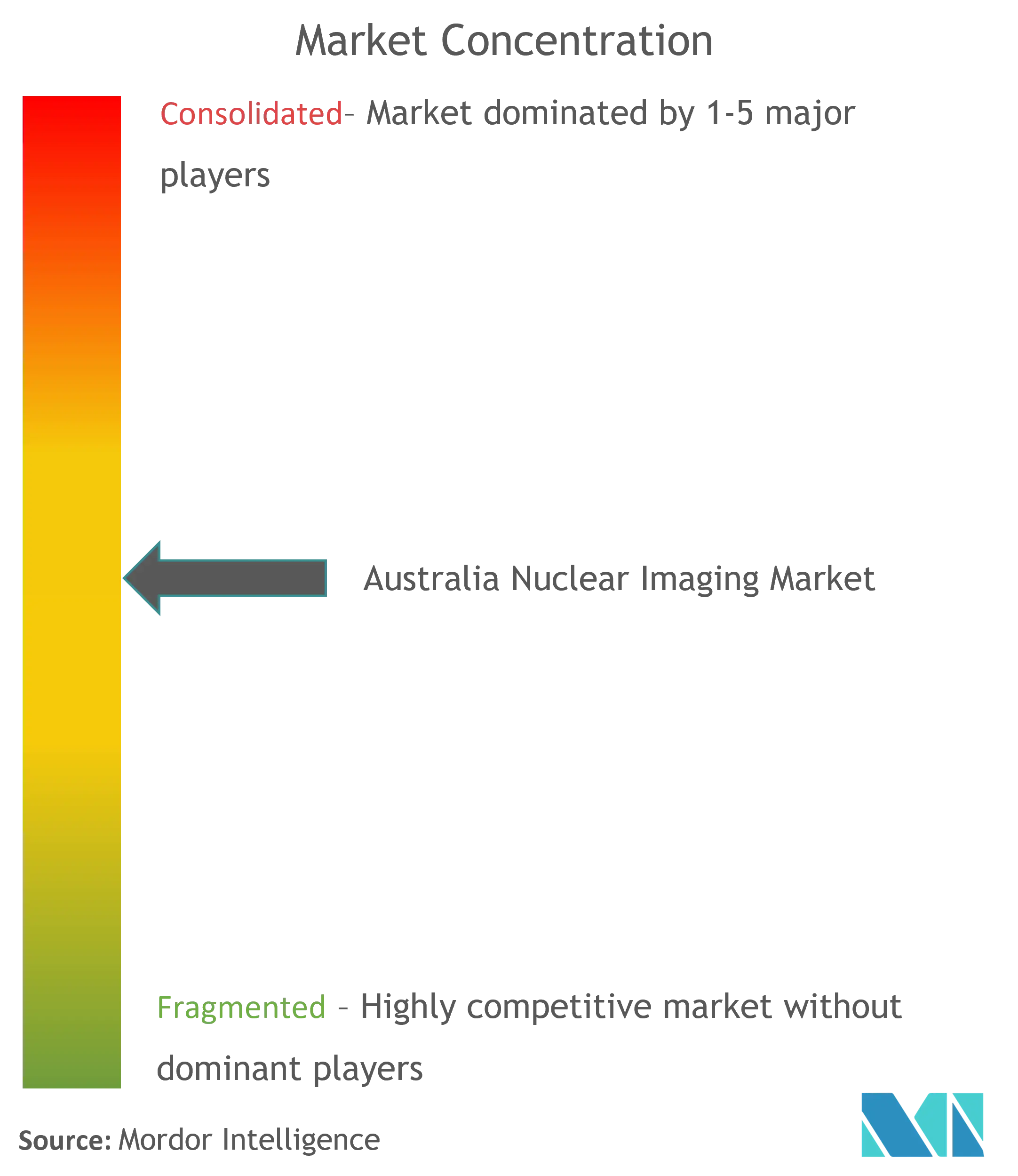

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Nuclear Imaging Market Analysis by Mordor Intelligence

The Australia nuclear imaging market size is expected to grow from USD 185.68 million in 2025 to USD 201.33 million in 2026 and is forecast to reach USD 301.78 million by 2031 at 8.44% CAGR over 2026-2031. Rising cancer incidence, expanding public-hospital replacement cycles for SPECT and PET scanners, and generous reimbursement under the Medicare Benefits Schedule are steering sustained capital investment. A sovereign isotope supply chain anchored by the Lucas Heights reactor safeguards clinical continuity, while private-sector innovation in theranostics broadens treatment pathways. Meanwhile, federal policy measures such as the PBS co-payment freeze and the March 2025 MBS update reinforce patient access and underpin procedure growth. Nonetheless, workforce shortages and occasional Mo-99 supply disruptions temper near-term expansion of the Australia nuclear imaging market.

Key Report Takeaways

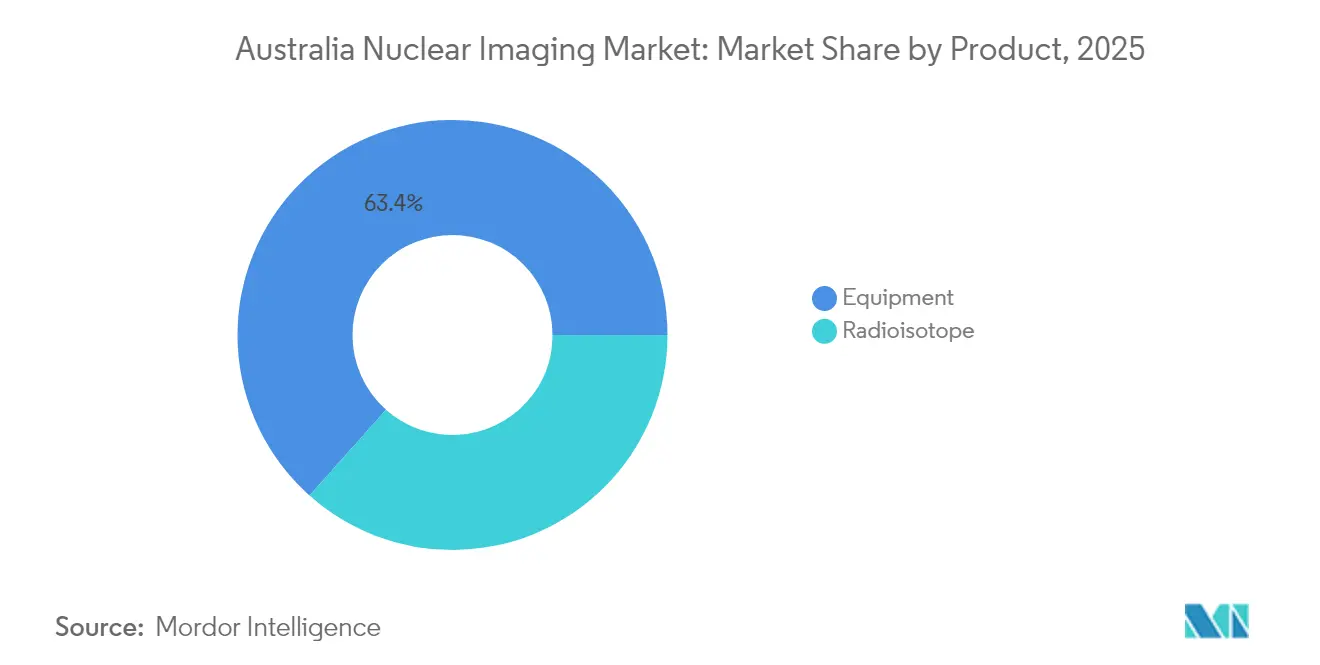

- By product, equipment led with a 63.42% revenue share in 2025; radioisotopes are projected to expand at an 8.78% CAGR through 2031.

- By application, cardiology accounted for 38.31% of the Australia nuclear imaging market share in 2025, while neurology is advancing at an 8.71% CAGR to 2031.

- By end user, hospitals controlled 68.92% of the Australia nuclear imaging market size in 2025 and diagnostic imaging centers are set to grow at a 8.86% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Nuclear Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing oncology PET-CT demand | +2.1% | National, concentrated in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Increasing public-hospital SPECT upgrades | +1.8% | National, priority in NSW and Victoria | Short term (≤ 2 years) |

| Expansion of cyclotron-based F-18 supply | +1.5% | Major metropolitan areas | Medium term (2-4 years) |

| Federal funding for Theranostics centres | +1.3% | National, early gains in major cities | Long term (≥ 4 years) |

| AI-enabled image reconstruction efficiency | +1.0% | National, technology-advanced facilities | Medium term (2-4 years) |

| Decentralised generator tech for remote sites | +0.8% | Regional Australia, remote territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Oncology PET-CT Demand

Cancer prevalence and evolving treatment algorithms continue to lift procedure volumes, with ANSTO facilitating 10,000–12,000 nuclear medicine studies every week. The recent FDA nod for Telix’s Gozellix PSMA agent intensifies focus on precision prostate imaging. Integration of theranostic protocols, highlighted by Lutetium-177 PSMA-617 trials at Peter MacCallum Cancer Centre, cements demand for high-end PET-CT scanners. Hospitals are expanding cyclotron access to ensure F-18 FDG availability, reducing delivery risk across state borders. As oncology shifts toward individualized therapy, PET-CT capacity becomes a strategic differentiator within the Australia nuclear imaging market.

Increasing Public-Hospital SPECT Upgrades

Medicare guidelines that cap scanner lifespan at 10 years trigger predictable replacement waves. State procurement clusters combine volumes to negotiate favorable pricing, accelerating adoption of AI-ready SPECT technology. Upgraded systems lower radiopharmaceutical dose and shrink scan times, allowing departments to accommodate rising referrals despite specialist shortages. The mandatory coverage rule—where outdated units lose MBS eligibility—pressures administrators to modernize and sustains revenue visibility for vendors across the Australia nuclear imaging market.

Expansion of Cyclotron-Based F-18 Supply

The 110-minute half-life of F-18 challenges long-distance distribution; localized cyclotrons in Queensland and Western Australia now complement Lucas Heights output. This hub-and-spoke network delivers same-day isotopes to secondary cities, shortening patient waitlists and unlocking incremental PET throughput. Private investors view distributed production as a hedge against reactor downtime, thereby reinforcing the resilience of the Australia nuclear imaging market.

Federal Funding for Theranostics Centres

Canberra’s targeted grants have seeded dedicated theranostic units in Melbourne, Sydney and Brisbane, enabling one-stop diagnostic-plus-therapy workflows. Early-stage trials with scandium-47 and terbium-161 show compelling tumor targeting, prompting the Therapeutic Goods Administration to accelerate review timelines. Public-private consortia straddling research and clinical care shorten commercialization cycles and position Australia as an Asia-Pacific reference site for novel radiopharmaceuticals.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mo-99 global supply-chain fragility | -1.2% | National; acute in remote areas | Short term (≤ 2 years) |

| Capital-equipment budget constraints | -0.9% | Public hospitals; regional | Medium term (2-4 years) |

| Short specialist workforce pipeline | -0.7% | National; severe in regional | Long term (≥ 4 years) |

| Radio-pharma waste-disposal compliance costs | -0.5% | Major facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mo-99 Global Supply-Chain Fragility

The February 2023 safety incident at Lucas Heights temporarily halted domestic Mo-99 output and forced emergency imports, prompting schedule backlogs nationwide. Because Mo-99 decays within 66 hours, even brief outages jeopardize cardiac imaging services that rely on 99mTc generators. Domestic reliance on a single reactor remains a structural risk until cyclotron-based alternatives or LEU-fueled reactors scale commercially. Contingency stockpiling is limited, making consistent isotope access a fragile linchpin for the Australia nuclear imaging market.

Capital-Equipment Budget Constraints

High-spec PET-CT and total-body scanners exceed USD 6 million per unit, testing state budget ceilings amid competing MRI and trauma-care priorities. Smaller hospitals stretch life cycles beyond recommended benchmarks, which may erode image quality and reimbursement eligibility. Private operators confront similar financing hurdles, evidenced by recent consolidation moves to unlock scale economies. The resulting procurement delays could slow the replacement cadence that fuels vendor revenue in the Australia nuclear imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment Dominance Drives Infrastructure Investment

Equipment captured 63.42% of 2025 revenue as hospitals refreshed legacy SPECT cameras and added high-end digital PET-CT units. GE HealthCare’s rollout of total-body scanners at Peter MacCallum Cancer Centre exemplifies migration toward ultra-low-dose platforms. The Australia nuclear imaging market size for radioisotopes, though smaller today, is expanding swiftly on an 8.78% CAGR trajectory through 2031, propelled by theranostic isotopes such as Cu-64 and Ac-225. Domestic suppliers benefit from ANSTO’s GenTech 99mTc generators, while Clarity Pharmaceuticals’ copper-based pipeline adds competitive depth.

Innovation in compact cyclotrons and decentralized generator systems opens new addressable pockets in regional Australia. Foreign OEMs like Siemens Healthineers maintain share through bundled service contracts, yet rising sovereign capability in detector manufacturing is gradually diversifying the supply base. The combination of equipment leadership and isotope growth sustains a balanced revenue mix within the Australia nuclear imaging market.

By Application: Cardiology Leadership Amid Neurology Growth

Cardiology held 38.31% of 2025 revenue owing to entrenched protocols for myocardial perfusion scans reimbursed under MBS item 55146. However, neurology is pacing ahead at an 8.71% CAGR as aging demographics lift dementia assessments. Oncology remains structurally significant, especially after Illuccix gained an expanded TGA indication for therapy selection, reinforcing theranostic uptake.

Emerging applications include endocrine imaging and infection mapping, each leveraging new tracers entering early clinical stages. AI-driven reconstruction tools have improved small-lesion detectability, indirectly enlarging addressable volumes across all specialties. The Australia nuclear imaging market share balance is expected to tilt modestly toward neurology and oncology by 2031 as precision-medicine protocols gain mainstream acceptance.

By End User: Hospital Concentration Supports Diagnostic Center Growth

Hospitals accounted for 68.92% of 2025 expenditure because complex isotope handling and multidisciplinary care favor campus-based settings. Major tertiary centers bundle research, training and clinical delivery, reinforcing purchasing clout with OEMs. Diagnostic imaging centers, though smaller, are the fastest-growing channel at a 8.86% CAGR as health systems redirect low-acuity scans to ambulatory environments for cost efficiency.

Private equity interest—illustrated by Affinity’s AUD 658 million buyout of Lumus Imaging—signals confidence in scalable outpatient models. Academic institutes contribute niche demand tied to early-phase trials, leveraging ANSTO’s Innovation Precinct for isotope access. Collectively, diversified end-user channels fortify resilience in the Australia nuclear imaging market.

Geography Analysis

New South Wales and Victoria dominate activity, anchored by Sydney’s Lucas Heights reactor and Melbourne’s oncology research cluster. Combined, the two states process a majority of national nuclear medicine procedures, reflecting population density and capital-intensive infrastructure. Queensland and Western Australia are closing the gap; Brisbane’s Princess Alexandra Hospital and Perth’s Sir Charles Gairdner Hospital now run full PET-CT suites supported by regional cyclotrons that offset F-18 logistics challenges.

Tasmania and the Northern Territory rely on mainland isotope shipments via temperature-controlled freight and tight scheduling to overcome half-life decay. The rollout of mobile SPECT units is improving rural outreach, aligning with federal equity mandates. Western Australia’s Sandy Ridge disposal site offers sovereign low-level waste capacity, easing compliance risk for facilities nationwide.

Looking ahead, planned theranostic hubs in Adelaide and Canberra are expected to diffuse expertise beyond the eastern seaboard. Telecommunications upgrades underpin tele-nuclear-medicine consults, enabling specialist oversight of remote scans in real time. Together, these initiatives reinforce geographically balanced growth within the Australia nuclear imaging market.

Competitive Landscape

ANSTO’s significant share of isotope supply secures a semi-monopolistic upstream position, while global OEMs such as GE HealthCare and Siemens Healthineers drive equipment innovation. Telix Pharmaceuticals and Clarity Pharmaceuticals illustrate a vibrant domestic biotech cohort, each advancing targeted radiopharmaceuticals with international licensing footprints.

Technology partnerships remain a core competitive lever; GE HealthCare’s total-body PET-CT alliance with Peter MacCallum Cancer Centre is a case in point. AI start-up Harrison.ai, whose software touches half of Australian radiologists, is reshaping diagnostic workflow economics. On the isotope front, strategic pacts—such as Telix and Eckert & Ziegler’s Actinium-225 venture—secure scarce alpha emitters critical for next-wave therapies.

Market entry barriers remain high due to regulatory controls over radiation safety and capital-intensive assets. However, novel generator technologies and decentralized cyclotrons lower threshold footprints for regional operators, broadening competitive participation. Overall, the Australia nuclear imaging market balances concentrated isotope supply with an increasingly dynamic ecosystem of equipment, software and radiopharmaceutical innovators.

Australia Nuclear Imaging Industry Leaders

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

Canon Inc. (Canon Medical Systems Corporation)

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ANSTO began decommissioning the HIFAR reactor after 67 years, marking a milestone in the transition to OPAL-based isotope production

- March 2025: Telix Pharmaceuticals developed breakthrough generator technology for Lead-212 isotope production at its Australian facilities, enabling sufficient yield for up to 60 clinical doses and supporting alpha-emitting radiopharmaceutical commercialization efforts

Australia Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer, cardiac and neurological disorders. Australia Nuclear Imaging Market is segmented by Product (Equipment, and Diagnostic Radioisotope (SPECT Radioisotopes, and PET Radioisotopes), Application (SPECT Application (Cardiology, Neurology, Thyroid, and Other SPECT Applications), and PET Application (Oncology, Cardiology, Neurology, and Other PET Applications). The report offers the value (in USD million) for the above segments.

By Product

| Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) |

| Thallium-201 (TI-201) | ||

| Gallium (Ga-67) | ||

| Iodine (I-123) | ||

| Other SPECT Radioisotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (RB-82) | ||

| Other PET Radioisotopes | ||

By Application

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) | |

| Thallium-201 (TI-201) | |||

| Gallium (Ga-67) | |||

| Iodine (I-123) | |||

| Other SPECT Radioisotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (RB-82) | |||

| Other PET Radioisotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the 2026 value of the Australia nuclear imaging market?

It is valued at USD 201.33 million with a forecast to reach USD 301.78 million by 2031 at an 8.44% CAGR over 2026-2031.

Which segment is growing fastest within the Australia nuclear imaging space?

Radioisotopes are expanding at an 8.78% CAGR, driven by theranostic demand.

Why are neurology procedures gaining traction?

An aging population and rising neurodegenerative disease prevalence are lifting neurology PET and SPECT scan volumes.

How does Australia maintain isotope supply security?

A sovereign production base at Lucas Heights, complemented by regional cyclotrons, underpins domestic availability.

What policy measures support patient access?

The PBS co-payment freeze and updated Medicare Benefits Schedule maintain affordability and reimburse modern equipment.

Page last updated on: