Beet Pulp Pellets Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 179 Million |

| Market Size (2030) | USD 235.10 Million |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

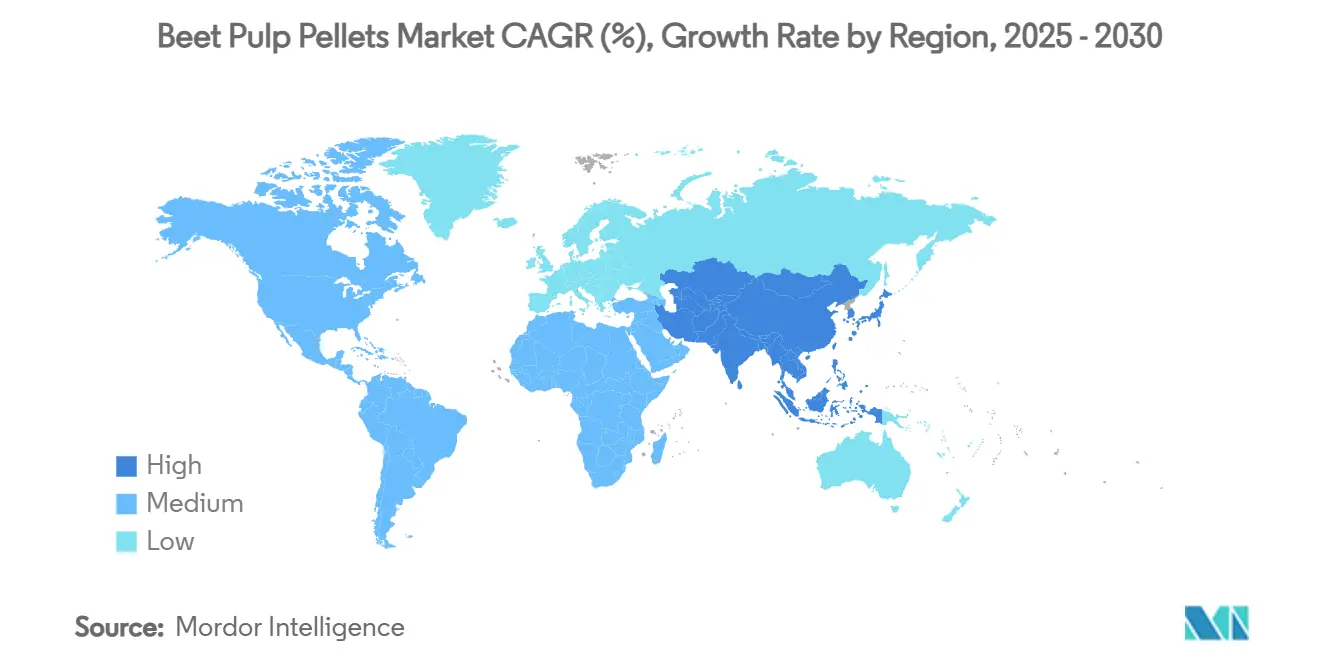

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

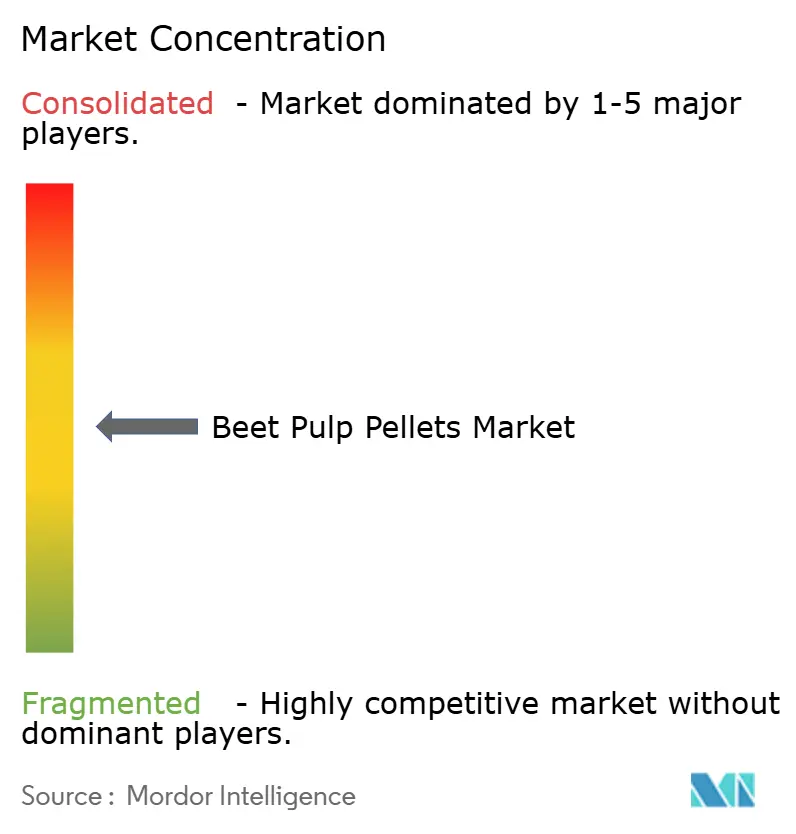

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beet Pulp Pellets Market Analysis by Mordor Intelligence

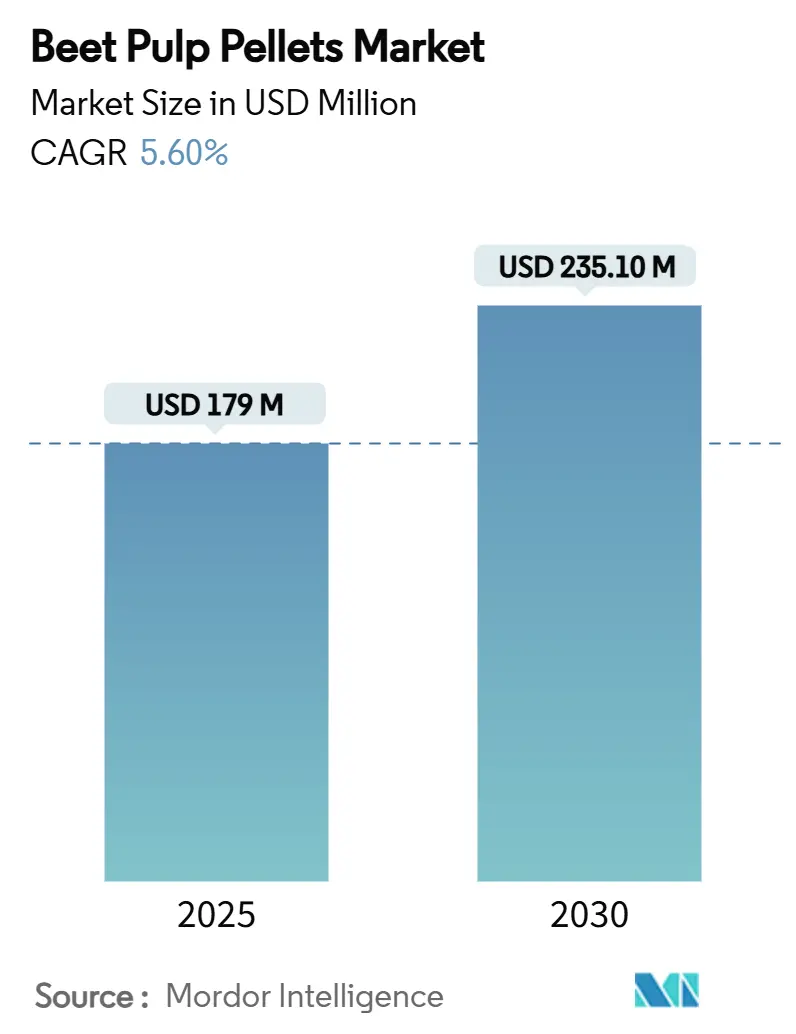

The beet pulp pellets market size is valued at USD 179 million in 2025 and is forecast to reach USD 235.1 million by 2030, expanding at a 5.6% CAGR during the period. Strong demand for consistent, digestible fiber in high-performance livestock diets, rising investments in sugar-beet processing efficiency, and the logistics benefits of dried pellets over wet pulp are central to that growth trajectory. Additionally, the European Union (EU) 27 planted about 1.482 million hectares for the 2024‑25 campaign, a roughly 6% year-on-year increase, supporting a projected production of 15.4 million metric tons of beet sugar [1]Source: United States Department of Agriculture, "Foreign Agricultural Service.2024.Sugar: EU-27 Semi-annual Report," usda.gov. Europe remains the anchor region due to its mature sugar-beet industry, but Asia-Pacific is accelerating on the back of intensive dairy and aquaculture expansion. Processors are upgrading drying and biomethane systems to curb energy costs and comply with tightening sustainability rules, while feed compounders are locking in multi-year supply contracts to shield margins from forage price volatility. Competitive dynamics favor vertically integrated sugar groups that leverage co-product optimization to offset soft sugar prices and widen export reach.

Key Report Takeaways

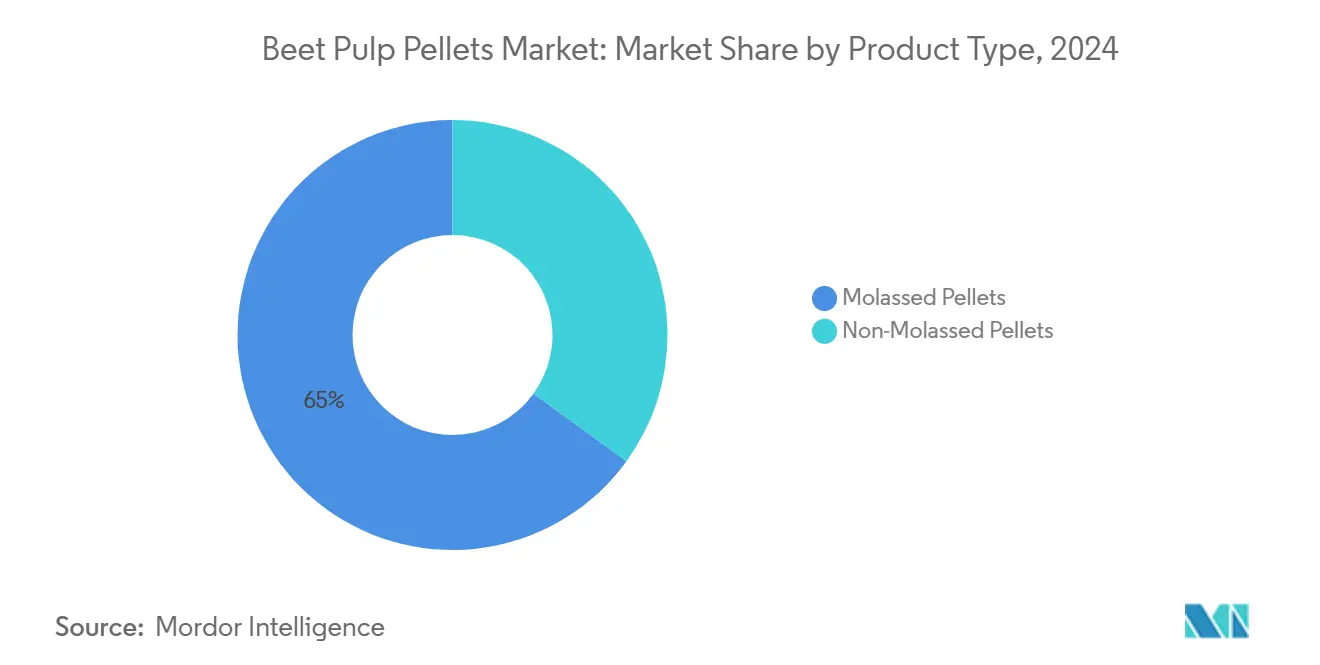

- By product type, molassed pellets accounted for 65% of the beet pulp pellets market share in 2024, and it is projected to lead growth at a 6.9% CAGR through 2030.

- By animal type, dairy cattle diets accounted for a 38% share of the beet pulp pellets market size in 2024, and the equine segment is projected to be the fastest growing at a 7.4% CAGR to 2030.

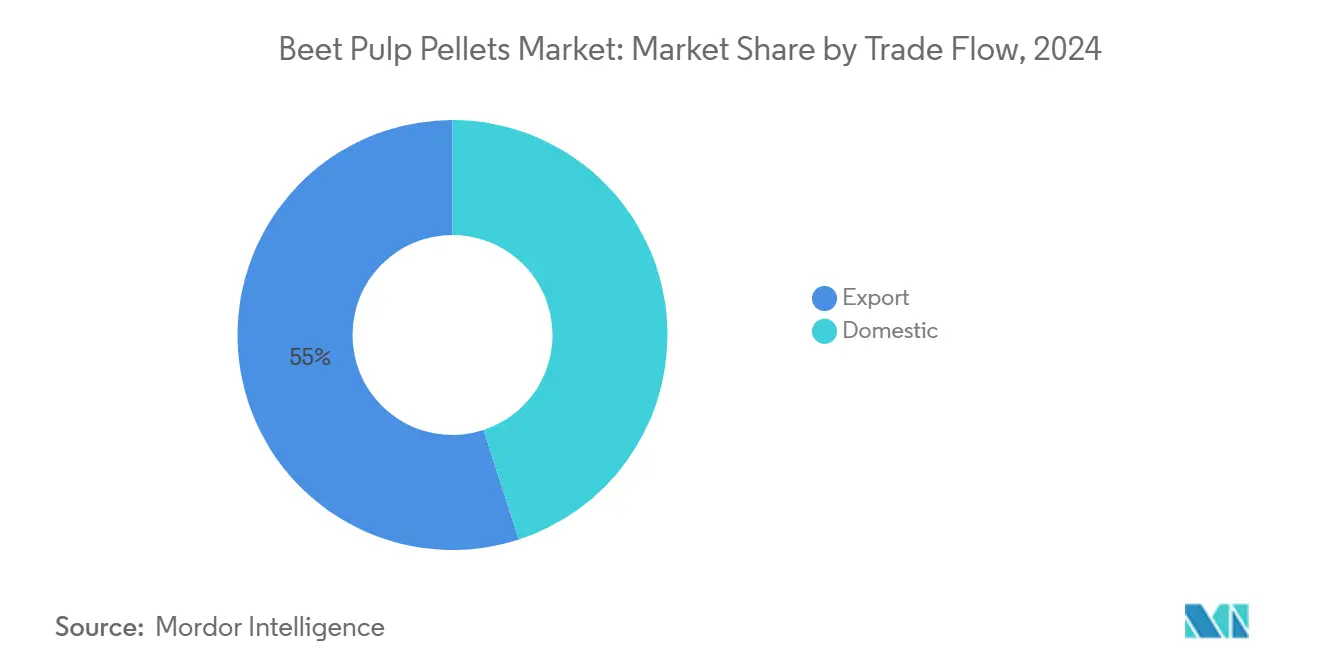

- By trade flow, exports held 55% revenue share of the beet pulp pellets market size in 2024, and it is projected to lead growth at a 6.1% during the forecast period.

- By geography, Europe commanded a 42% market share in 2024, and the Asia-Pacific region is forecast to expand at a 7.1% CAGR through 2030.

Global Beet Pulp Pellets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand for high-fiber dairy feed | +1.2% | North America and Europe | Medium term (2-4 years) |

| Logistics and storage advantages of pelletized fiber | +0.8% | Global export corridors | Long term (≥ 4 years) |

| Expansion of equine low-sugar diet trends | +0.6% | North America and Europe, and emerging Asia-Pacific | Medium term (2-4 years) |

| Rising sugar-beet processing capacity | +0.9% | Europe and the United States | Long term (≥ 4 years) |

| Aquaculture trials showing pre-biotic performance gains | +0.3% | Asia-Pacific core, global spillover | Long term (≥ 4 years) |

| Climate-induced forage shortages driving pellet substitution | +0.7% | Drought-prone regions worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Demand for High-Fiber Dairy Feed

Intensive dairy systems increasingly specify beet pulp pellets to sustain milk-fat synthesis while easing starch loads that raise acidosis risk. Pellets supply 12.5 MJ metabolizable energy per kg of dry matter and 79 g digestible protein, enabling nutritionists to maintain high-energy rations without compromising rumen pH. Ongoing reformulation demands, alongside rising pressure to meet methane-reduction targets, are positioning beet pulp as a climate-smart fiber source that aligns with both productivity and long-term sustainability objectives..

Logistics and Storage Advantages of Pelletized Fiber

Drying and densifying wet beet pulp into pellets reduces moisture content to around 10%, significantly extending shelf life and cutting transportation costs over long distances. Approximately 15% of global beet pulp production is already traded internationally, with European suppliers consistently catering to Asian dairy markets, due to the improved stability of pelletized forms. This processing method enables manufacturers to better manage seasonal production surges, capitalize on off-season price premiums, and avoid spoilage-related losses commonly associated with handling and transporting wet pulp.

Expansion of Equine Low-Sugar Diet Trends

Growing veterinary consensus on limiting non-structural carbohydrates in equine diets is driving increased adoption of beet pulp pellets. Controlled studies have demonstrated that beet pulp can safely substitute up to 50% of forage, particularly when hay quality is poor or availability is limited, helping to reduce the risk of laminitis while maintaining adequate energy intake. Palatable molassed variants further enhance feed acceptance, supporting higher consumption rates. As a result, the equine sector is expanding faster than the broader beet pulp pellets market.

Rising Sugar-Beet Processing Capacity

New investments across the United States Midwest and Eastern Europe are accelerating beet crushing capacity and expanding overall pulp availability. For example, Michigan Sugar Company's USD 109 million molasses desugarization facility processes 650 metric tons per day, channeling the resulting increase in pulp volume directly into pellet production lines. This boost in beet throughput not only stabilizes the raw material supply but also enhances operational efficiency, supports long-term contracting commitments, and bolsters market confidence by reducing supply-side volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from soy hulls and citrus pulp | -0.9% | Regions with strong oilseed or citrus processing | Medium term (2-4 years) |

| Volatile sugar-beet acreage tied to sweetener demand | -0.6% | Europe and North America | Short term (≤ 2 years) |

| High drying-energy costs under carbon pricing | -0.4% | European Union, potential global adoption | Long term (≥ 4 years) |

| On-farm mycotoxin risk during storage | -0.3% | Humid climates worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Soy Hulls and Citrus Pulp

Soy hulls have emerged as the preferred fiber source in regions with concentrated oilseed crushing operations, where backhaul logistics help drive down their effective cost. In subtropical dairy-producing areas, citrus pulp often takes precedence due to its attractive price point and year-round availability. Although beet pulp is valued for its consistent nutrient profile and digestibility, its relatively higher freight costs can be a limiting factor, particularly in markets where cost-effective, locally sourced alternatives like soy hulls and citrus pulp are readily accessible.

Volatile Sugar-Beet Acreage Tied to Sweetener Demand

Processor plantings fluctuate in response to global sugar prices and regulatory changes. Tereos forecasts a 9% contraction in European Union beet area[2]Source: European Commission, "EU agricultural Outlook for Markets and Environment 2023-2035," agriculture.ec.europe.eu for the next campaign, a contraction that is projected to significantly reduce pulp throughput. This potential shortfall is likely to inject notable volatility into forward contracts, increasing price risk and uncertainty. As a result, long-term planning becomes more complex for processors, feed manufacturers, and buyers who rely on stable pulp availability for pellet production, risk mitigation, and cost forecasting. The tightening supply may also prompt a shift toward alternative fiber sources or renegotiation of contract terms, further reshaping market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Molassed Variants Dominated the Market

Molassed pellets held about 65% of the beet pulp pellets market share in 2024, and it is fastest growing segment projected to grow at a CAGR of 6.9% through 2030. This domination is due to heightened equine demand and mixed-species rations where improved palatability lifts intake rates. Product differentiation revolves around uniform coating technology that applies 6-8% molasses without compromising pellet durability, enabling processors to charge premiums while managing inventory integrity during long-haul shipping.

Demand for non-molassed beet pulp pellets continues to grow, largely driven by dairy formulations that restrict soluble sugar content. This trend is further influenced by fluctuations in refined sugar and molasses prices, prompting feed mills to carefully balance energy density with cost-effectiveness to meet nutritional targets. Additionally, ongoing innovations in low-dust pellet design are improving barn air quality, an increasingly important welfare consideration that is shaping procurement decisions among large-scale dairy operations, particularly across North America and Western Europe.

By Animal Type: Dairy Dominance Coupled with Equine Acceleration

Dairy cattle diets generated 38% of the beet pulp pellets market size in 2024, reflecting rumen-fiber optimization strategies that raise milk-fat yields. Ration trials demonstrate up to 15% pellet inclusion without adverse rumen pH shifts, solidifying long-term adoption among milk producers aiming to cut methane while safeguarding production.

Equine nutrition, though smaller in absolute volume, delivers the fastest trajectory at 7.4% CAGR as owners seek low-starch fiber alternatives for insulin-resistant horses. Swine and poultry remain niche outlets because ration-energy priorities lean heavier on cereals, yet gestating sow and broiler breeder segments signal incremental opportunities where bulk fiber supports gut health. Emerging aquaculture demand could reshape the landscape further if pilot studies translate into commercial feed codes [3]Source: Food and Agriculture Organization of the United Nations (FAO), "The State of World Fisheries and Aquaculture 2022," fao.org .

By Trade Flow: Exports Monetize Logistics Advantage

Export consignments comprised 55% of the beet pulp pellets market share in 2024 and continue to outgrow domestic channels at 6.1% CAGR, relying on containerized shipments from European and United States ports into East Asia and the Middle East. Pellets tolerate months of ocean transit without quality loss, an edge wet pulp cannot match. Domestic markets, while stable, contend with local fiber substitutes and price sensitivity. Still, potential growth appears where drought inflates forage costs, prompting feedlots to secure spot pellet deliveries.

Forward contracts increasingly index pellet prices to a basket of sugar, energy, and freight benchmarks, smoothing volatility for both processors and compounders. The model appeals to cash-flow planning in integrated dairy operations, especially under heightened interest-rate environments.

Geography Analysis

Europe held about 42% of the beet pulp pellets market share in 2024. Leading processors, such as Südzucker, reported EUR 9.7 billion (USD 10.5 billion) in turnover for 2024/25, with co-product revenue helping to stabilize margins amid soft sugar prices. Sustainability upgrades, including Nordzucker’s biomethane switch, support compliance with the European Union's Fit-for-55 rules while maintaining pellet output.

The Asia-Pacific region is projected to be the fastest-growing region, expanding at 7.1% through 2030, capitalizing on surging dairy herds in China and India, as well as early aquaculture pilots in Vietnam and Indonesia. Importers prefer pellets over bulky hay because port logistics and quarantine protocols favor compact, heat-treated feedstuffs.

North America is anticipated to hold a significant share of the beet pulp pellets market size in 2024, driven by acreage gains in Minnesota and North Dakota, which are expected to increase pellet volumes. Meanwhile, capacity closures in California highlight regional differences in grower economics. The Middle East and Africa also register above-average growth, with feed buyers mitigating forage imports by adding pellets to dairy and camel rations, bolstered by regional poultry demand.

Competitive Landscape

The beet pulp pellets market is moderately concentrated, with key players including Südzucker AG, Nordzucker AG, Tereos Group, Sucden, and Michigan Sugar Company. These integrated sugar processors leverage shared infrastructure for pulp drying, molasses desugarization, and energy cogeneration to enhance efficiency and reduce operational costs. Their extensive trading and logistics networks enable them to manage regional price differentials and navigate export complexities. However, they continue to face challenges from rising freight rates and increasingly stringent sustainability requirements set by downstream buyers.

Energy transition initiatives are central to the long-term strategy for these companies. Nordzucker AG has achieved carbon-neutral sugar production in Denmark by utilizing biomethane derived from beet residues, significantly lowering energy costs associated with pellet drying. Tereos Group has committed USD 920.7 million (EUR 800 million) toward its 2050 net-zero target, investing in high-efficiency drying systems and waste-heat recovery loops. These sustainability-driven upgrades not only reduce emissions but also enhance cost stability amid energy market volatility.

Export growth remains a priority for these industry leaders. Südzucker AG and Nordzucker AG have established dedicated bulk shipping routes to meet increasing demand from Southeast Asia. Sucden leverages its global trading platform to support cross-regional distribution of beet pulp pellets, while Michigan Sugar Company is expanding its footprint through long-term supply agreements with compound feed producers in Mexico and South Korea. Product innovation efforts are focused on uniform molasses coating, reduced dust formulations, and tailored pellet blends for specific livestock segments such as aquaculture and gestation sows.

Beet Pulp Pellets Industry Leaders

-

Südzucker AG

-

Nordzucker AG

-

Tereos Group

-

Sucden

-

Michigan Sugar Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tereos Group made an investment of USD 927.1 million decarbonization investment program toward net-zero by 2050. These investments support the efficiency of beet pulp pellet lines by implementing high-efficiency dryers and waste-heat recovery systems, reducing production costs and CO₂ emissions.

- September 2024: Nordzucker AG powered Danish operations with beet-residue biomethane, cutting Scope 1 emissions and stabilizing pellet drying costs.

- May 2024: Michigan Sugar Company has launched a molasses desugarization facility in Bay City, doubling processing capacity from 325 to 650 metric tons per day. This boosts sugar recovery and enhances efficiency in beet pulp pellet production by fully utilizing molasses co-products.

Global Beet Pulp Pellets Market Report Scope

| Molassed Pellets |

| Non-Molassed Pellets |

| Dairy Cattle |

| Beef Cattle |

| Equine |

| Swine |

| Poultry |

| Domestic |

| Export |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Molassed Pellets | |

| Non-Molassed Pellets | ||

| By Animal Type | Dairy Cattle | |

| Beef Cattle | ||

| Equine | ||

| Swine | ||

| Poultry | ||

| By Trade Flow | Domestic | |

| Export | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the beet pulp pellets market?

The beet pulp pellets market size stands at USD 179 million in 2025 and is projected to reach USD 235.1 million by 2030.

Which region leads consumption of beet pulp pellets?

Europe holds the largest regional share at 42%, due to its established sugar-beet processing infrastructure and proximity to intensive livestock hubs.

Why are beet pulp pellets favored in dairy rations?

They supply highly digestible fiber and energy that maintain rumen health and support milk-fat synthesis while helping producers meet methane-reduction goals.

What factors are driving the fastest growth segment?

Low-sugar equine diet protocols, combined with the palatability of molassed pellets, push the equine segment ahead at a 7.4% CAGR.

Page last updated on: