Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.68 Billion |

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Trash Bags Market Analysis by Mordor Intelligence

The North America trash bags market size is projected to expand from USD 3.68 billion in 2025 and USD 3.92 billion in 2026 to USD 5.17 billion by 2031, registering a CAGR of 5.69% between 2026 to 2031. Strong state landfill-diversion mandates, Fortune 500 zero-waste commitments, and rising parcel volumes from e-commerce operations are lifting liner consumption across households, offices, fulfillment centers, and construction sites. Color-coded and ASTM D6400-certified bags are moving quickly through retail shelves as California, New York, and Massachusetts enforce 50% diversion thresholds that favor premium compostable SKUs. Corporate facilities are shifting toward high-clarity, recycled-content liners that withstand rigorous sorting protocols, while pay-as-you-throw programs in more than 7,000 U.S. municipalities spur steady demand for municipally branded bags. Together, these trends position converters that can balance performance, sustainability, and cost to win long-term supply contracts in the North America trash bags market.

Key Report Takeaways

- By end user, residential captured 45.67% of the North America trash bags market share in 2025, while the industrial segment is advancing at a 6.03% CAGR through 2031.

- By product type, low-density polyethylene led with 41.23% share in 2025, whereas biodegradable and compostable variants are growing at a 7.12% CAGR to 2031.

- By capacity, 8-30 gallon kitchen bags held 37.55% share in 2025, and 30-55 gallon contractor bags are projected to expand at a 5.87% CAGR over 2026-2031.

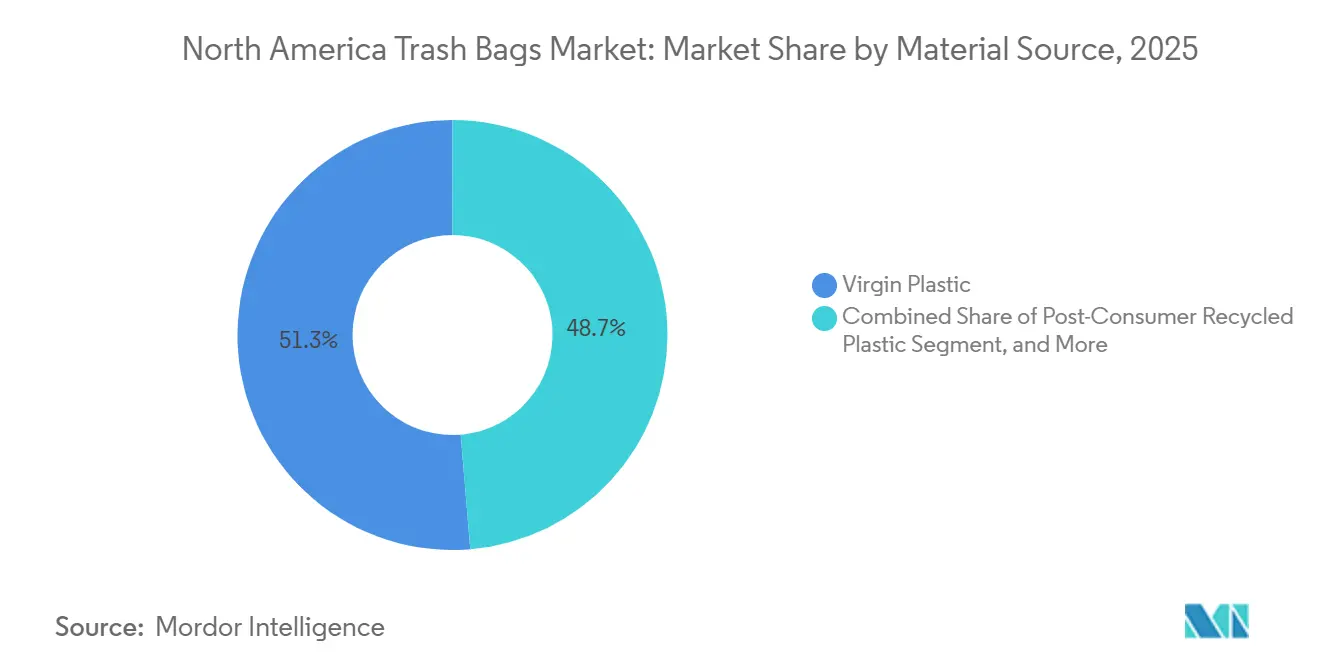

- By material source, virgin plastic accounted for 51.32% share in 2025, yet bio-based resins are on track for a 7.07% CAGR through 2031.

- By sales channel, offline retail secured 70.29% share in 2025, while online platforms are pacing ahead with a 6.43% CAGR to 2031.

- By geography, the United States dominated with 63.84% share in 2025, whereas Mexico is the fastest-growing country at a 6.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Trash Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential waste-stream expansion and state landfill-diversion targets | +1.8% | United States, Canada | Long term (≥ 4 years) |

| Corporate zero-waste pledges from Fortune 500 facilities | +1.4% | United States, Canada, Mexico | Medium term (2-4 years) |

| Rapid e-commerce packaging turnover elevating commercial trash volume | +1.2% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Municipal pay-as-you-throw programs accelerating bag consumption | +1.0% | United States, Canada | Medium term (2-4 years) |

| High-clarity recycled-content resins enabling premium pricing | +0.7% | United States, Canada | Long term (≥ 4 years) |

| Adoption of antimicrobial liners in healthcare and foodservice | +0.5% | United States, Canada, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Residential Waste-Stream Expansion and State Landfill-Diversion Targets

Household waste in the United States reached 292 million tons in 2024, and population inflows into metropolitan areas are pushing per-capita disposal rates higher. California SB 1383 and comparable rules in New York and Massachusetts now obligate municipalities to collect organics separately, creating locked-in demand for ASTM D6400-compliant compostable liners.[1]California Department of Resources Recycling and Recovery, “SB 1383 Regulations,” calrecycle.ca.gov Municipal purchasing departments increasingly specify multi-layer bags with color cues that prevent cross-contamination during curbside pickup. Converters are answering with new coextrusion lines that embed pigment bands without compromising recyclability, a capital shift that favors incumbents already spending more than USD 5 million each year on R&D. As similar diversion targets propagate to Canadian provinces, the North America trash bags market gains a durable growth runway anchored in regulatory certainty.

Corporate Zero-Waste Pledges from Fortune 500 Facilities

More than 180 Fortune 500 companies now target TRUE or UL zero-waste certification, which requires diversion rates above 90% and segregation into at least five material streams.[2]U.S. Zero Waste Business Council, “Zero Waste Certification,” uszwbc.org To streamline audits, plants are shifting to clear liners that let sorters verify contents without opening bags, cutting contamination and labor time at Procter and Gamble’s Lima, Ohio, site by 12% in 2025. General Motors embedded RFID tags in 60-gallon translucent bags to trace waste back to production cells, enabling targeted operator training and fewer mis-sorted loads. Jan-san distributors report 20-30% price premiums for these feature-rich SKUs, creating margin headroom for converters that master additive dosing and inline printing. The expanding corporate pledge universe therefore secures a durable premium tier within the North America trash bags market.

Rapid E-Commerce Packaging Turnover Elevating Commercial Trash Volume

North American fulfillment centers processed 18.3 billion parcels in 2025, generating roughly 4.2 million tons of cardboard, stretch film, and void-fill that require daily clearance to meet fire codes.[3]National Fire Protection Association, “Fire Code Compliance,” nfpa.org Amazon’s Bessemer, Alabama, hub alone consumes about 22,000 contractor-grade bags per week to handle packaging waste from same-day and next-day orders. Walmart mandates at least 30% post-consumer content in bags used across its e-commerce network under the Project Gigaton initiative. To secure recycled feedstock, Inteplast commissioned a USD 75 million wash line capable of turning 150 million lb of post-consumer film into pellet feed for trash-bag extrusion. High parcel velocity thus translates directly into sustained contractor-bag demand and underpins recycled-content investment in the North America trash bags market.

Municipal Pay-As-You-Throw Programs Accelerating Bag Consumption

Pay-as-you-throw (PAYT) ordinances operated in 7,142 U.S. municipalities at the close of 2025, up from 6,890 a year earlier, and each program requires households to buy branded liners that embed disposal fees. Worcester, Massachusetts, logged a 34% rise in certified-bag sales and a 19% drop in landfill tonnage within 12 months of launching PAYT, proving that price signals nudge consumer behavior. Portland, Maine, pairs 15- and 30-gallon bags at differential price points, steering residents toward right-sized disposal and boosting small-capacity unit volumes. Bid documents often insist on domestic production, recycled-content floors, and ISO-verified tear strength, raising barriers for low-grade imports. As more towns adopt PAYT to defer landfill costs, dependable baseline demand accrues to regional converters in the North America trash bags market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyethylene and bioplastic feedstock prices | -1.1% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Single-use-plastic bans and extended producer responsibility laws | -0.9% | Canada, United States | Medium term (2-4 years) |

| Retail SKU cannibalization from reusable tote initiatives | -0.4% | United States, Canada | Long term (≥ 4 years) |

| Logistics emissions scrutiny curbing import of low-grade liners | -0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyethylene and Bioplastic Feedstock Prices

LDPE spot prices swung between USD 0.52 and USD 0.68 per lb in 2025 after hurricane disruptions and cracker outages on the Gulf Coast.[4]Berry Global, “Manufacturing Innovation,” berryglobal.com Without pass-through clauses, private-label converters absorb those spikes, eroding margins that typically run below 12%. Bioplastic inputs proved even choppier, with polylactic-acid resin climbing from USD 1.85 to USD 2.31 per lb as Midwest drought cut dextrose yields. Mid-tier firms now carry 60-90 days of inventory to hedge volatility, tying up working capital that could fund coextrusion upgrades or lab testing. Sudden cost jumps therefore sap near-term profitability across the North America trash bags market.

Single-Use-Plastic Bans and Extended Producer Responsibility Laws

Canada’s Single-Use Plastics Prohibition Regulations bar checkout bags under 75 microns unless they contain at least 20% post-consumer resin, removing a source of repurposed liners for household trash.[5]Environment and Climate Change Canada, “Single-Use Plastics Prohibition Regulations,” canada.ca New York’s statewide plastic-bag ban curtailed grocery checkout supply by roughly 90%, driving a 14% drop in store-bought trash-bag units as consumers reused thicker totes. British Columbia and Ontario now require producers to pay 100% of municipal recycling costs, adding up to CAD 0.06 (USD 0.05) per bag in eco-fees that spur lightweighting. Compliance teams must track dozens of local exemptions, increasing SKU proliferation and inventory risk. Collectively, these measures crimp volume growth and squeeze margins in the North America trash bags market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Industrial Momentum Outpaces Household Demand

The residential segment captured 45.67% of the North America trash bags market share in 2025, benefiting from widespread curbside programs that keep weekly kitchen-bag purchases steady. Industrial users are forecast to expand at a 6.03% CAGR through 2031, lifting their portion of the North America trash bags market size as federally funded bridge, road, and water-system upgrades create debris streams that require heavy-duty liners. Contractors specify 30-55 gallon bags engineered to resist puncture forces above 400 psi, and procurement teams pay premiums of 25-35% for products verified to ASTM performance standards. Commercial offices, retail locations, and hospitality venues accounted for roughly 32% of 2025 volume, with occupancy rebounding to 68% and supporting demand for janitorial liners that often feature antimicrobial additives.

Foodservice operators within the commercial bracket favor bags certified to NSF antimicrobial protocols, a niche that drew USD 18 million in venture funding during 2025. Industrial facilities also turn to transparent liners embedded with RFID tags so zero-waste auditors can trace contamination to specific workcells, an innovation that secures long-term contracts despite price premiums. Residential demand remains stable yet faces gradual substitution from reusable containers distributed under city give-away schemes. Overall, the industrial end user is set to contribute the largest incremental revenue to the North America trash bags market size over the forecast horizon.

By Product Type: Compostable Lines Lead Growth Curve

Low-density polyethylene (LDPE) retained 41.23% of 2025 sales, sustained by tooling familiarity and the ability to incorporate up to 40% post-consumer resin without gauge drift. High-density polyethylene (HDPE) maintains relevance in warehouse and contractor settings where stiffness and moisture barriers are prized, but its advance lags LDPE and compostables. Biodegradable and compostable liners are projected to grow at a 7.12% CAGR, the fastest among product types, as California SB 1383 and similar rules legally obligate organics-collection bags to meet ASTM D6400 or EN 13432 standards.

Polylactic acid and starch-blend formulations cost 50-80% more than LDPE yet enjoy captive purchasing in regulated jurisdictions, steadily enlarging their slice of the North America trash bags market share. Conventional HDPE faces incremental erosion where retailers and municipalities forge plastic-reduction agreements with environmental groups. Still, LDPE’s flexibility, seal strength, and cost advantage preserve its leadership in household and light-commercial channels, ensuring a balanced but shifting product-type mix through 2031.

By Capacity: Contractor Bags Capture Infrastructure Upswing

Kitchen-sized 8-30 gallon liners held 37.55% of the North America trash bags market share in 2025, reflecting their ubiquity in routine household disposal cycles. These bags typically feature drawstring closures, odor-neutralizing additives, and two- or three-layer structures that balance performance with price. Contractor-grade 30-55 gallon liners are on track for a 5.87% CAGR, riding a non-residential construction spend that climbed to USD 1.03 trillion in 2025.

Warehouses and renovation crews prefer 3.0-mil bags with reinforced gussets, a specification that drove a 14% uptick in 45-55 gallon sales at industrial distributors during the first half of 2025. Drum liners above 55 gallons support manufacturing clean-outs and bulk waste transfers, while bathroom bag sizes under 8 gallons grow slowly in hospitality and healthcare. The capacity mix is therefore tilting toward contractor and drum sizes, underscoring how infrastructure funding and fulfillment-center expansion add volume to the North America trash bags market size.

By Material Source: Recycled And Bio-Based Content Gains Traction

Virgin LDPE and HDPE together commanded 51.32% of shipments in 2025 thanks to consistent melt-flow rates that ensure clarity and seal integrity. Post-consumer recycled (PCR) pellets accounted for 28% of supply, a share buoyed by the commissioning of a USD 75 million wash line that feeds 150 million pounds of PCR into extrusion each year. Hybrid blends pairing virgin and recycled resin serve private-label buyers who need tight gauge tolerance without paying full virgin premiums.

Bio-based resins are forecast to post a 7.07% CAGR as corporate Science Based Targets initiative commitments spur brand owners to specify polylactic-acid or polyhydroxyalkanoate liners. NatureWorks added 150 million pounds of PLA capacity in 2025 to support ASTM-certified compostable bags, signaling confidence in the segment’s upside. Cost remains a hurdle, PLA trades above USD 2 per pound, but municipalities with mandatory organics programs create price-insensitive demand that gradually diversifies feedstock sourcing across the North America trash bags market share.

By Sales Channel: Digital Subscriptions Win Steady Household Replenishment

Offline retail, covering grocery, mass merchandise, and hardware, retained 70.29% of 2025 sales as shoppers dropped liners into carts during weekly trips, often choosing private-label multipacks priced up to 25% below national brands End-cap displays and instant-redeem coupons keep unit velocity high, and in-store sample stations educate consumers on drawstring and odor-control upgrades.

Online platforms are climbing at a 6.43% CAGR, leveraging Subscribe and Save models that shave 5-15% off list prices and guarantee doorstep replenishment every four to eight weeks. Direct-to-consumer compostable brands bypass slotting fees and reinvest savings in social-media advertising, while jan-san portals service bulk purchasers with technical data sheets and pallet pricing. Offline will remain dominant through 2031, yet incremental channel share continues to migrate online, reflecting the convenience premium that households and small businesses place on automated ordering within the North America trash bags market size.

Geography Analysis

The United States generated 63.84% of the North America trash bags market size in 2025, powered by 7,000-plus pay-as-you-throw programs that require residents to buy municipally branded liners. State landfill-diversion rules in California, New York, and Massachusetts mandate compostable or color-coded bags, giving converters with ASTM certifications a pricing edge. Infrastructure Investment and Jobs Act funds pour into bridge and rail projects, lifting contractor-bag demand, while Amazon’s 1,100-site fulfillment grid drives commercial volume. Single-use-plastic bans create SKU complexity yet open margin room for premium compostables that meet local thresholds.

Mexico is projected to post a 6.07% CAGR to 2031, the fastest among regional peers. The 2024 General Law for the Prevention and Integral Management of Waste requires municipalities over 500,000 residents to implement color-coded source separation by 2027, instantly enlarging the addressable base for certified bags. Mexico City already obliges commercial kitchens to use compostable liners for organics, and foreign direct investment in waste-management infrastructure reached USD 1.8 billion in 2025. Informal recycling networks temper penetration in lower-income districts, but rapid urbanization in Monterrey and Guadalajara offsets that drag.

Canada supplied roughly 12% of 2025 revenue, anchored by extended producer responsibility frameworks that push compliance costs onto manufacturers and require recycled-content minimums. British Columbia mandates 35% post-consumer content by 2026, while Ontario’s full-producer-pay model adds CAD 0.04 (USD 0.03) per bag in fees, motivating lightweighting and larger gauge precision. Cold winters complicate compostable logistics, yet Toronto and Vancouver pilots show early success with BPI-certified liners, positioning bio-based suppliers for gradual gains. These divergent provincial rules diversify the regulatory landscape but collectively reinforce the sustainability theme guiding the North America trash bags market share outlook.

Competitive Landscape

Reynolds Consumer Products and The Clorox Company together control about 35% of regional revenue via the Hefty and Glad franchises, securing premium shelf space and consistent brand recall. Both groups leverage national advertising budgets to defend price premiums while incrementally raising recycled-content targets.

Novolex tilts the field through vertical integration: eight resin-extrusion plants, 14 film-blowing sites, and 22 converting lines enable private-label bids that undercut national brands by 20-30% yet still deliver gross margins above 18%. Inteplast Group combines cracker capacity with a USD 75 million mechanical recycling plant that feeds 150 million lb of PCR pellets into trash-bag lines, letting it offer fixed-price contracts insulated from LDPE spot swings.

Niche players Aluf Plastics and Heritage Bag Company differentiate with antimicrobial and odor-control chemistries carrying NSF certifications, winning healthcare and foodservice accounts worth tens of millions annually. Berry Global introduced AI-guided thickness monitors that trimmed off-spec scrap by 14%, illustrating how process controls can lift returns even in commodity segments. Patent filings in multi-layer films, bio-based additives, and RFID-embedded liners climbed 22% from 2024-2025, signaling that technology innovation, not just resin cost, will shape competitive edges in the North America trash bags market.

North America Trash Bags Industry Leaders

Reynolds Consumer Products Inc. (Hefty)

Novolex Holdings LLC

Inteplast Group Corporation

Cosmoplast Industrial Company LLC

International Plastics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Reynolds Consumer Products committed USD 45 million to add a fourth blown-film line in Wisconsin, boosting contractor-bag capacity by 180 million units and raising recycled content to 40%.

- January 2026: The Clorox Company introduced Glad ForceFlexPlus with Antimicrobial Protection, a 13-gallon kitchen bag expected to lift household hygiene standards and already posting USD 6.2 million in first-month sales.

- April 2025: Reynolds reported Q1 2025 Hefty revenue of USD 240 million, up 3% year-on-year on volume gains for scented bags.

- December 2025: Novolex acquired Boulder Bag Company for USD 28 million, gaining ASTM D6400 expertise and a foothold in 140 western U.S. municipal contracts.

North America Trash Bags Market Report Scope

Trash bags are disposable garbage bags used to handle and dispose of trash. Trash bags are typically made of plastic material that comes in various sizes and options. The market includes revenue accrued from the sales of trash bags offered by various vendors operating in the market.

The North America Trash Bags Market Report is Segmented by End User (Residential, Commercial, and Industrial), Product Type (Low-Density Polyethylene Bags, High-Density Polyethylene Bags, and Biodegradable and Compostable Bags), Capacity (Less than 8 Gal, 8-30 Gal, 30-55 Gal, and Above 55 Gal), Material Source (Virgin Plastic, Post-Consumer Recycled Plastic, Hybrid, and Bio-Based Resins), Sales Channel (Offline Retail, Online Retail, Jan-San Distribution), and Geography (United States, Canada, and Mexico). TMarket Forecasts are Provided in Terms of Value (USD).

By End User

| Residential |

| Commercial |

| Industrial |

By Product Type

| Low-Density Polyethylene (LDPE) Bags |

| High-Density Polyethylene (HDPE) Bags |

| Biodegradable and Compostable Bags |

By Capacity (Gallons)

| Less than 8 Gal (Bathroom) |

| 8 - 30 Gal (Kitchen) |

| 30 - 55 Gal (Contractor) |

| Above 55 Gal (Industrial Drum Liners) |

By Material Source

| Virgin Plastic |

| Post-Consumer Recycled Plastic |

| Hybrid (Recycled + Virgin) |

| Bio-Based Resins |

By Sales Channel

| Offline Retail (Grocery, Mass Merchandiser) |

| Online Retail |

| Jan-San and Institutional Distribution |

By Country

| United States |

| Canada |

| Mexico |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Product Type | Low-Density Polyethylene (LDPE) Bags |

| High-Density Polyethylene (HDPE) Bags | |

| Biodegradable and Compostable Bags | |

| By Capacity (Gallons) | Less than 8 Gal (Bathroom) |

| 8 - 30 Gal (Kitchen) | |

| 30 - 55 Gal (Contractor) | |

| Above 55 Gal (Industrial Drum Liners) | |

| By Material Source | Virgin Plastic |

| Post-Consumer Recycled Plastic | |

| Hybrid (Recycled + Virgin) | |

| Bio-Based Resins | |

| By Sales Channel | Offline Retail (Grocery, Mass Merchandiser) |

| Online Retail | |

| Jan-San and Institutional Distribution | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How fast is the North America trash bags market expected to grow between 2026 and 2031?

The market is forecast to expand at a 5.69% CAGR from 2026 to 2031 as landfill-diversion mandates, zero-waste pledges, and e-commerce activity raise liner consumption.

Which capacity segment is advancing the quickest?

Contractor-grade 30-55 gallon bags are projected to record a 5.87% CAGR through 2031 on the back of robust non-residential construction activity.

Why are compostable trash bags gaining share in the region?

State and municipal organics programs require ASTM D6400-certified liners, prompting a 7.12% CAGR for biodegradable and compostable bags through the forecast period.

What role do online channels play in category growth?

Subscription services and same-day delivery partnerships are pushing online sales ahead at a 6.43% CAGR, although offline stores still control most volume.

How are producers addressing resin price volatility?

Vertically integrated players like Inteplast secure supply with in-house cracking and recycling, while others carry extra inventory or negotiate blended-resin formulas to stabilize costs.

Which country will contribute the highest incremental revenue after the United States?

Mexico, projected at a 6.07% CAGR, will generate the largest incremental gains due to new source-separation mandates and expanding municipal collection networks.

Page last updated on: