Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

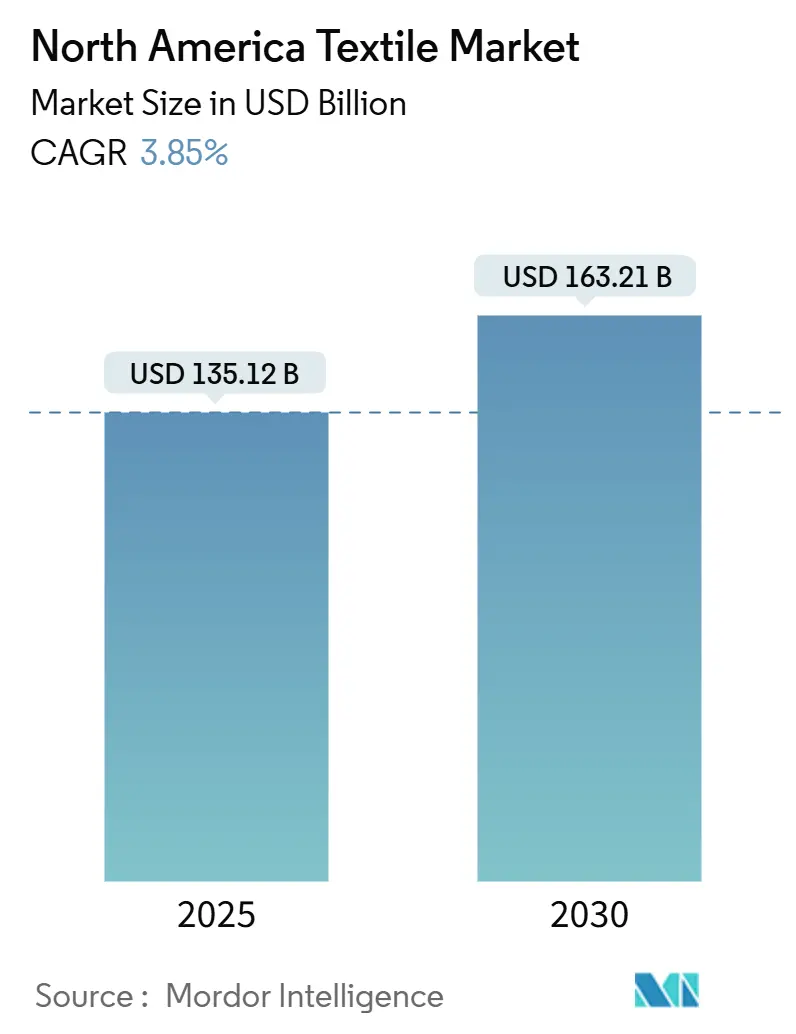

| Market Size (2025) | USD 135.12 Billion |

| Market Size (2030) | USD 163.21 Billion |

| Growth Rate (2025 - 2030) | 3.85% CAGR |

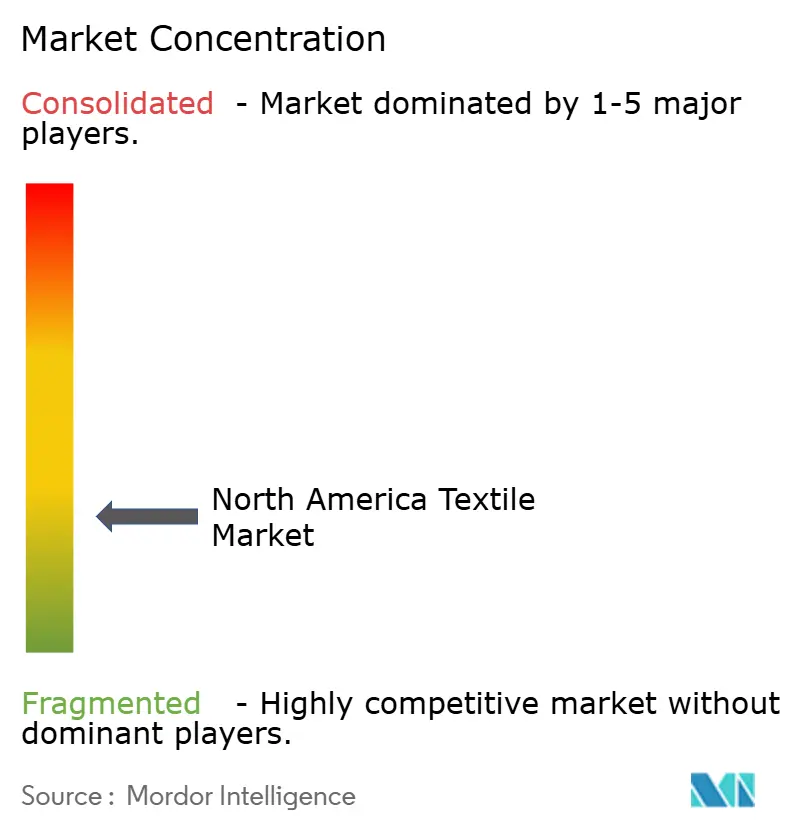

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Textile Market Analysis by Mordor Intelligence

The North America Textile Market size stands at USD 135.12 billion in 2025 and is projected to reach USD 163.21 billion by 2030, reflecting a 3.85% CAGR. Steady expansion is being fueled by nearshoring, the adoption of technical textiles, and regulatory incentives that reward circular business models over sheer production volume. Polyester recycling, PFAS-free finishing chemistries, and AI-enabled inventory planning are lowering waste and compliance costs, widening the performance gap between digitally mature brands and traditional volume players. As sustainability metrics become mandatory in public procurement and private-label requirements, suppliers able to certify traceability and low emissions are commanding price premiums. Intensifying trade friction and raw-material volatility are simultaneously spurring demand for regional supply resilience. In this context, the North American textiles market is transitioning from a commodity-driven competition to one centered on value creation, anchored in functional innovation and transparent operations.

Key Report Takeaways

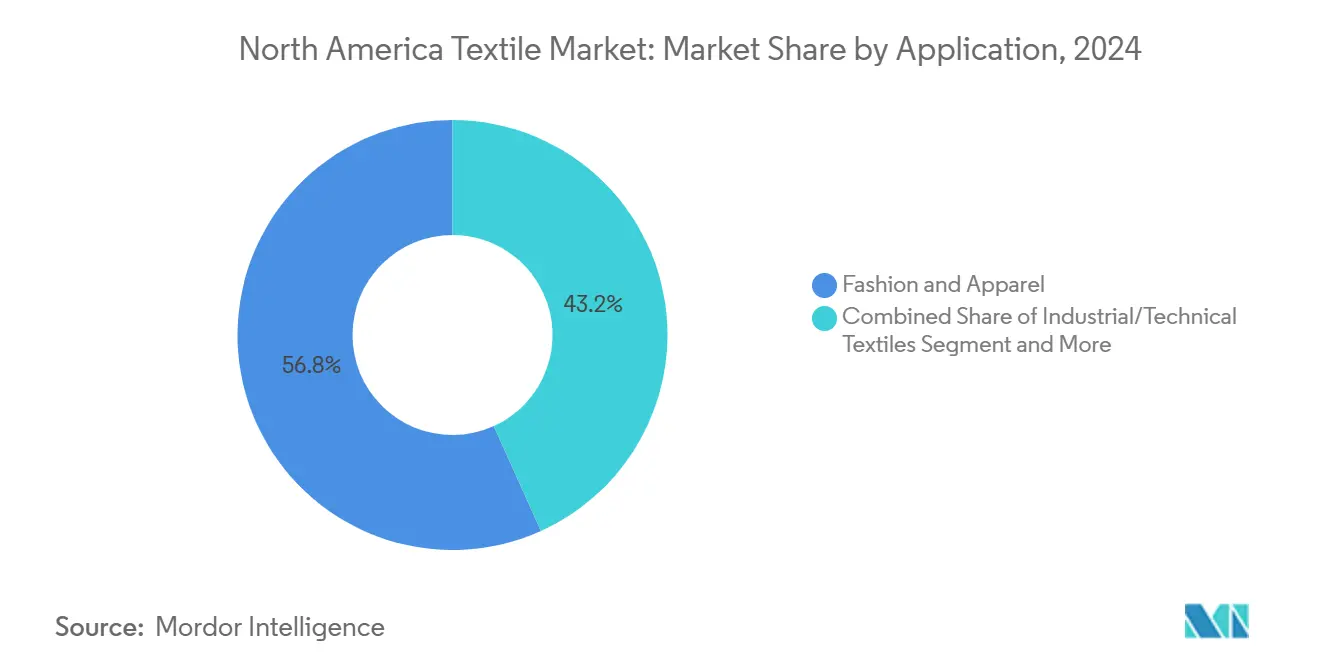

- By application, Fashion and apparel led with 56.76% of the North American textiles market share in 2024, while industrial and technical textiles are tracking a 5.47% CAGR through 2030.

- By raw material, Synthetic fibers captured 38.98% share of the North American textiles market size in 2024, and recycled or bio-polyester, is forecast to expand at a 5.88% CAGR between 2025-2030.

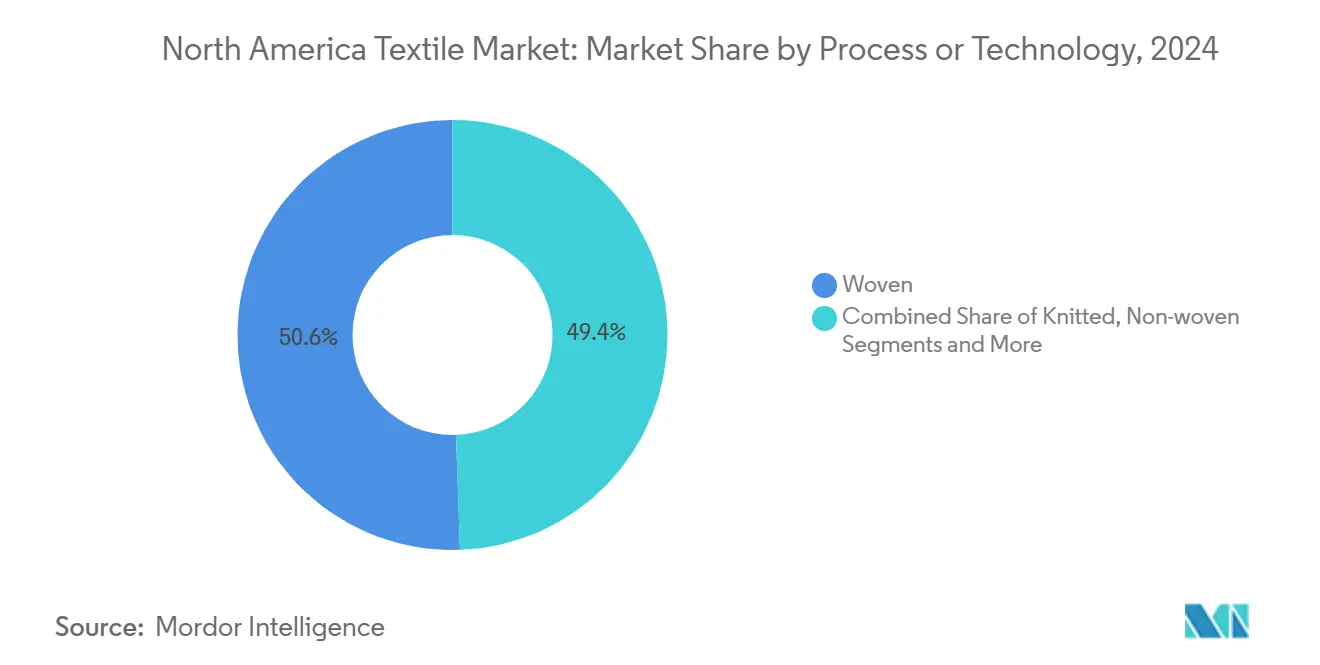

- By process/technology, Woven processes accounted for 50.56% of the North American textiles market in 2024, yet non-wovens are advancing at a 5.37% CAGR through 2030.

- By geography, the United States held 52.97% of regional revenue in 2024, whereas Mexico is expected to post the fastest 5.12% CAGR to 2030.

North America Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable apparel demand | +1.1% | U.S., Canada, Mexico | Medium term (2-4 years) |

| Technical textiles in automotive & healthcare | +0.9% | U.S., Mexico | Long term (≥4 years) |

| AI-driven demand forecasting | +0.7% | Region-wide | Medium term (2-4 years) |

| Reshoring and nearshoring | +0.6% | U.S., Mexico | Short to medium (≤4 years) |

| Expansion of bio-based fibers | +0.5% | U.S., Canada | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Apparel

Retailers, regulators, and consumers have redefined sustainability as a non-negotiable purchase criterion rather than a premium add-on. Carbon-footprint labeling and mandatory extended-producer-responsibility laws in several U.S. states now reward suppliers that can document recycled content and traceable cotton provenance. HanesBrands cut Scope 1 and 2 emissions by 53% between 2019-2024 and shifted 75% of its cotton to certified sustainable sources, using those milestones to secure preferred shelf space at mass merchants. Amazon’s Climate Pledge Friendly tags and emerging EU digital-product passports are accelerating similar commitments among regional mid-tier brands. As cost-parity between recycled and virgin polyester narrows, volume orders for mechanically and chemically recycled resin are locking in multi-year contracts. Firms that align early with life-cycle-assessment metrics are capturing price premiums and mitigating the reputational risk of greenwash litigation.

Growth of Technical Textiles in Automotive & Healthcare

Automakers and hospitals are turning to lightweight composites, conductive fabrics, and high-filtration non-wovens to meet fuel-efficiency norms and infection-control protocols. Melt-blown and spunbond capacity added during the pandemic has been redirected into cabin-air filters, wound dressings, and battery separators, raising domestic demand for specialty polypropylene and PET chips. Recycled carbon-fiber mat is gaining traction in structural components for electric vehicles because it combines weight savings with circular-sourcing narratives attractive to ESG investors. In healthcare, antimicrobial silver-ion coatings and copper-infused linens have moved from trials to scaled procurement by U.S. hospital networks. The sector’s ability to qualify new materials under FDA and NHTSA performance standards will determine its share of next-generation mobility and medical budgets.

Adoption of AI-Driven Demand Forecasting Reducing Inventory Waste

Inventory misalignment has long eroded margins in the North American textiles market, but cloud-based analytics platforms are closing the gap. Levi Strauss & Co. reports double-digit improvements in inventory turns after embedding machine-learning algorithms that integrate point-of-sale data with raw-material lead times. Vision-inspection systems on knitting and dyeing lines now detect defects in real time, cutting rework rates and dye over-use. Smaller contract mills are subscribing to software-as-a-service modules that simulate demand scenarios and automate fabric allocation, enabling them to meet fast-fashion replenishment windows previously monopolized by Asian giants. Early adopters attribute 20-30 basis-point gross-margin expansion to these digital controls, making AI integration a hygiene factor rather than a differentiator by 2028.

Reshoring and Nearshoring of Production Post-Pandemic

U.S. fashion brands that struggled with container shortages and tariff spikes during 2021-2023 have formalized Mexico- and Central America-plus-one sourcing strategies. Under USMCA rules of origin, yarn-forward provisions grant duty-free access for garments knit and sewn within the bloc, incentivizing investment in regional spinning and dyeing capacity. Mexican apparel exports to the U.S. climbed 8% in 2024, bolstered by strategic alliances between U.S. retailers and maquiladora clusters in Coahuila and Nuevo León. Automation investments such as digital print lines and robotic sewing units are mitigating regional labor-cost differentials, making nearshore capacity competitive on total-landed-cost metrics. Brands cite lead-time reductions of four to six weeks and markdown savings as key benefits.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cotton & synthetic price volatility | -0.8% | U.S. and global supply | Short term (≤2 years) |

| Stringent dyeing & finishing rules | -0.6% | U.S., Canada, Mexico | Medium term (2-4 years) |

| Skilled-labor shortages | -0.5% | U.S., Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cotton & Synthetic Raw-Material Prices

Cotton futures dipped in early 2025 as global stocks swelled, yet polyester staple prices jumped when crude rebounded above USD 90 per barrel, exposing mills to erratic input curves. The North American textiles market relies on Asia for more than 65% of virgin PET, so freight-rate spikes and currency swings can erode margins within a single quarter. Brands that hedge with recycled feedstock contracts or dual-source across continents are partially insulated, but commodity segments with slim spreads face pass-through difficulties at retail. Financialization of fiber markets via exchange-traded derivatives adds speculative swings that can detach prices from fundamentals, complicating procurement budgeting for medium-sized mills. Inventory buffering offers temporary relief but ties up working capital and heightens obsolescence risk when design cycles shorten.

Stringent Environmental Rules on Dyeing & Finishing

The U.S. Environmental Protection Agency tightened effluent standards for azo dyes and heavy-metal mordants in 2025, requiring zero-liquid-discharge or advanced oxidation for new permits. California and New York ban PFAS in textiles sold after January 2025, prompting rapid reformulation of water-repellent treatments and new lab-testing protocols at customs. Canadian regulators are following with tougher wastewater guidelines that may harmonize across the region by 2027. Mills that invested early in membrane-bioreactor systems and digital color-management software report water savings of up to 50%, offsetting cap-ex with lower chemical spend and sewer surcharges. Late adopters, especially in small-lot piece dyeing, risk customer attrition when private-label buyers impose compliance scorecards[1]U.S. Customs and Border Protection, “USMCA Textile Provisions,” cbp.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Technical Textiles Drive Diversification

Fashion and apparel retained 56.8% of the North American textiles market share in 2024, underscoring the enduring dominance of consumer-driven categories. Industrial and technical textiles, however, are forecast to grow at a 5.47% CAGR through 2030, the fastest among all applications. Non-woven medical masks, wound dressings, and filtration media now occupy permanent production capacity that once served disposable hygiene exports. Automotive OEMs are specifying lightweight woven composites and noise-dampening felts to hit stringent fuel-economy rules, lifting contract volumes for aramid, glass, and recycled carbon-fiber fabrics. In household furnishings, stain-resistant upholstery is migrating to PFAS-free chemistries, opening opportunities for silicone- and wax-based repellents compliant with state bans. Department of Defense solicitations for flame-retardant uniforms and high-tenacity parachute fabrics further accelerate technical-textile penetration. These shifts illustrate how the North American textiles market is recasting its growth narrative around performance and regulation-driven demand clusters[2]U.S. International Trade Commission, “Textile and Apparel Imports,” usitc.gov.

Medical and industrial buyers demand rigorous supply-chain transparency, steering contracts toward mills that operate ISO-certified cleanrooms and offer real-time lot-traceability portals. Early movers that combine antimicrobial finishes with recycled fiber content are already carving out margin-rich niches. As healthcare systems lock in multi-year PPE reserve contracts, domestic capacity committed to ASTM Level 3 surgical masks is forecast to run at sustained high utilization. Conversely, the fashion segment is tempering unit growth with greater emphasis on made-to-order models that align with sustainability pledges. Over the forecast horizon, the technical-textile segment’s superior pricing power is expected to pull the North American textiles market toward a more balanced revenue mix, reducing its historical over-reliance on retail fashion cycles.

By Raw Material: Synthetics Retain Primacy, Recycled Polyester Gains Speed

Synthetic fibers held a 38.9% revenue share in 2024, far ahead of cotton, wool, and specialty natural fibers. Within synthetics, recycled and bio-based polyester is projected to grow at a 5.88% CAGR to 2030, eclipsing virgin PET growth by nearly twofold. Brand commitments such as Nike’s 50% recycled-material target for footwear uppers and Adidas’ pledge to phase out virgin polyester by 2027 are translating into multiyear offtake agreements. Depolymerization technologies commercialized in 2024 enable bottle-to-filament production with 90% energy savings over virgin resin, enticing mill adoption. Meanwhile, bio-PET derived from sugarcane ethanol is gaining pilot-scale traction, offering a lower carbon footprint without sacrificing dye uptake or tensile strength.

Cotton remains strategically significant but faces agronomic risks from extreme weather that trimmed U.S. yields in 2023 and 2024. To hedge volatility, several vertically integrated mills are blending recycled polyester with Better Cotton Initiative lint, balancing sustainability claims with moisture-management performance. Specialty high-performance fibers like aramid, UHMWPE, and PBO are winning defense and aerospace contracts, yet their aggregate volume remains niche. Regulatory scrutiny of microplastic shedding from synthetic apparel is spurring R&D into plasma and enzymatic surface treatments that promise fiber integrity without legislative backlash. Over the forecast period, synthetics will stay dominant, but their composition will tilt sharply toward recycled and bio-based inputs as the North American textiles market aligns with circular-economy mandates.

By Process/Technology: Non-Wovens and 3D Weaving Reshape Production

Woven textiles accounted for 50.6% of 2024 revenues, reflecting the entrenched role of shuttle- and rapier-loom fabrics in denim, workwear, and home furnishings. Non-wovens, however, are poised to clock a 5.37% CAGR through 2030, driven by melt-blown filtration media, spunbond hygiene substrates, and increasingly by needle-punched automotive insulators. Pandemic-era capital deployed to produce face-mask melt-blown lines has pivoted toward high-efficiency particulate-air (HEPA) filters and battery-separator membranes. Meanwhile, 3D weaving and spacer-fabric technologies are enabling one-piece composite preforms that cut scrap and labor, winning traction in aerospace interior panels and sports equipment.

Computer-aided design linked directly to jacquard looms now permits mass customization without compromising throughput, a capability embraced by DTC mattress and upholstery brands. Digital twin simulations of dye-house thermal loads and airflow patterns have shaved 15% off steam consumption at early-adopter mills, supporting decarbonization commitments. Regulatory water-use caps are accelerating the switch from batch to continuous dyeing, further favoring larger mills able to amortize automation investments. As smart sensors populate knitting and non-woven lines, predictive-maintenance algorithms are curbing unplanned downtime and extending asset life. Collectively, these process upgrades make the North American textiles market more resilient and responsive, traits critical to capturing near-shore reorder cycles.

Geography Analysis

The United States anchored 52.9% of regional revenue in 2024, a position secured through deep consumer demand, advanced manufacturing clusters, and a concentration of technical-textile innovators. Yet U.S. mills wrestle with tightening EPA regulations on dye effluents and PFAS, as well as skilled-labor shortages that complicate expansion plans. Investment in AI scheduling, cobot sewing cells, and renewably powered dye houses is helping offset labor and compliance costs while protecting gross margins. American brands are also pushing for yarn-forward sourcing under USMCA, thereby boosting domestic spinning orders and supporting regional supply-chain resilience[3]U.S. International Trade Commission, “North American Textile Trade,” usitc.gov.

Mexico is on track for the fastest 5.12% CAGR between 2025-2030 as it transitions from a cut-and-sew outpost to an integrated hub with ring-spinning, dyeing, and finishing capacity oriented toward rapid replenishment orders. The peso’s stability, favorable wage differentials, and government grants for technical-textile parks in Nuevo León are reinforcing its allure. Automotive investment in the Bajío region is catalyzing demand for laminated interior fabrics and air-bag yarns, pulling in foreign direct investment from European composite weavers. Nearshore lead-times shortened to 20 days in 2024, versus 60-plus days for trans-Pacific shipments, a delta that retailers cite as critical to markdown avoidance.

Canada remains a smaller but strategically differentiated market, focusing on specialty, sustainable, and high-performance textiles sourced from its ample biomass and hydroelectric resources. Canadian mills leverage provincial incentives for clean technology, enabling closed-loop water systems and on-site biomass boilers that lower Scope 1 emissions. Brands producing PFAS-free outerwear and technical knits for cold-weather sports are clustering around Quebec’s textile innovation ecosystem. While growth is slower than Mexico’s, Canada’s alignment with stringent eco-labels positions it well for premium export segments. Across the tri-nation landscape, regulatory convergence on chemical safety, recycling, and digital traceability is likely to define competitive positioning through 2030.

Competitive Landscape

Competitive intensity in the North America textile market is rising as legacy apparel giants and specialist technical-textile players pursue divergent yet overlapping strategies. Nike, VF Corporation, Levi Strauss & Co., and HanesBrands have funneled cap-ex into AI-driven demand planning, direct-to-consumer (DTC) channels, and automation that cuts waste and shortens product-development cycles. Each has declared science-based emissions targets and publishes supplier-audit data, positioning sustainability as a core brand promise. Consolidation is accelerating: HanesBrands divested the Champion label to focus on innerwear and debt reduction while bolstering proprietary supply chains, and VF Corporation is streamlining its portfolio under Project “Reinvent” to free cash for innovation in The North Face and Vans.

White-space opportunities are attracting venture-backed startups and mid-size innovators specializing in bio-based fibers, PFAS-free chemistries, and smart fabrics. Firms such as MycoWorks and Bolt Threads are scaling lab-grown materials, scoring pilot agreements with luxury houses seeking novel aesthetics and low carbon footprints. Non-woven specialists that pivoted from pandemic PPE to filtration and battery components are diversifying revenue streams, challenging incumbents through proprietary melt-blown dies and bicomponent fiber patents. Patent data show a 28% year-over-year rise in U.S. filings for digital weaving and composite-reinforcement textiles, underscoring the technology race for differentiation.

Regulatory shifts serve as both a barrier and a catalyst. EPA and state PFAS bans have elevated compliance to a decisive competitive factor, effectively disqualifying laggards from major retail assortments and public procurement lists. Brands with established chemical-management frameworks and third-party certifications (e.g., Bluesign, ZDHC) are penetrating premium markets previously gated by price sensitivity. Simultaneously, raw-material volatility is prompting vertical integration: Levi Strauss & Co. expanded a strategic alliance with a recycled-polyester spinner in Tennessee, and Nike invested in an Indonesian depolymerization plant to secure feedstock. As top players continue to hold slightly above 55% of regional revenue, the North American textiles market remains moderately concentrated yet open to disruptive entrants that align with sustainability and digital-efficiency imperatives.

North America Textile Industry Leaders

Nike Inc.

VF Corporation

PVH Corp.

Hanesbrands Inc.

Levi Strauss & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Gildan Activewear reached a definitive agreement to purchase HanesBrands for USD 2.2 billion in cash and stock, combining Gildan’s annual output of roughly 1.2 billion basic T-shirts with Hanes, Bonds, Maidenform, and other inner-wear names.

- June 2025: Swedish recycler Syre signed multiyear supply deals with Gap and Target; Gap will use 10,000 t per year of Syre polyester chips, while Target will integrate the material into select lines and co-develop circular-polyester solutions.

- May 2025: Soho Apparel Group announced a U.S. capacity build-out, citing “Made-in-America” incentives and pledging new or expanded cut-and-sew sites that add domestic headcount.

- February 2025: Kontoor Brands agreed to acquire outdoor and workwear label Helly Hansen from Canadian Tire for about USD 900 million, fast-tracking Kontoor’s push into technical outerwear.

North America Textile Market Report Scope

By Application

| Fashion & Apparel |

| Industrial/Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports Textiles, etc.) |

By Raw Material

| Natural Fibers | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibers | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibers | |

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) |

By Process / Technology

| Woven | |

| Knitted | |

| Non-woven | Spunlaid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-Laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

By Geography

| United States |

| Canada |

| Mexico |

| By Application | Fashion & Apparel | |

| Industrial/Technical Textiles | ||

| Household & Home Textiles | ||

| Medical & Healthcare Textiles | ||

| Automotive & Transport Textiles | ||

| Others (Protective, Sports Textiles, etc.) | ||

| By Raw Material | Natural Fibers | Cotton |

| Wool | ||

| Silk | ||

| Synthetic Fibers | Polyester | |

| Nylon | ||

| Rayon / Viscose | ||

| Acrylic | ||

| Polypropylene | ||

| Recycled Fibers | ||

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) | ||

| By Process / Technology | Woven | |

| Knitted | ||

| Non-woven | Spunlaid (Spunbond / Melt-blown) | |

| Dry-laid Hydro-entangled | ||

| Wet-Laid | ||

| Needle-punched | ||

| 3-D Weaving & Spacer Fabrics | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current revenue value for North American textiles?

The sector stands at USD 135.12 billion in 2025 and is forecast to reach USD 163.21 billion by 2030.

Which application segment leads regional revenue?

Fashion and apparel holds the largest share at 56.76% of 2024 sales.

Which fiber type is showing the fastest growth?

Recycled and bio-based polyester is projected to grow at a 5.88% CAGR through 2030.

Which country is expanding production the quickest?

Mexico is tracking the fastest 5.12% CAGR between 2025-2030, buoyed by nearshoring and USMCA incentives.

How are PFAS regulations affecting textile supply chains?

State-level bans in California and New York plus federal proposals are driving rapid reformulation of water-repellent finishes and stricter supplier audits.

What technologies are brands adopting to reduce inventory waste?

AI-driven demand forecasting and real-time defect detection are improving inventory turns and shaving 20-30 basis points off gross margins.

Page last updated on: