Parking Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

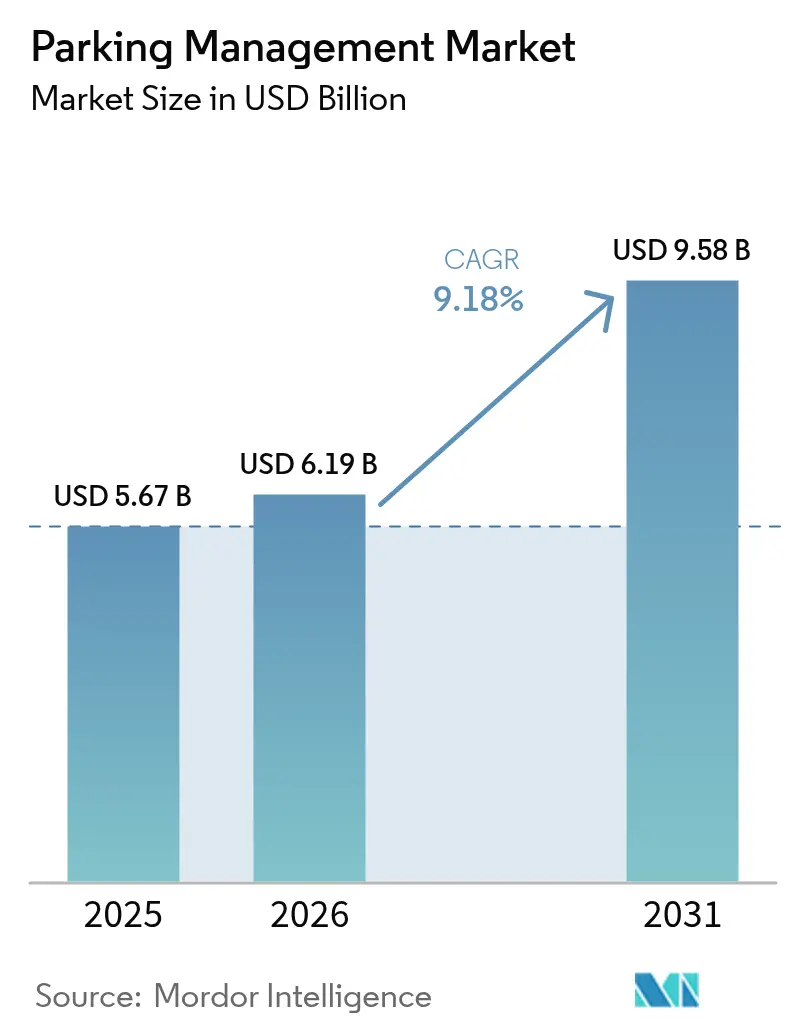

| Market Size (2026) | USD 6.19 Billion |

| Market Size (2031) | USD 9.58 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

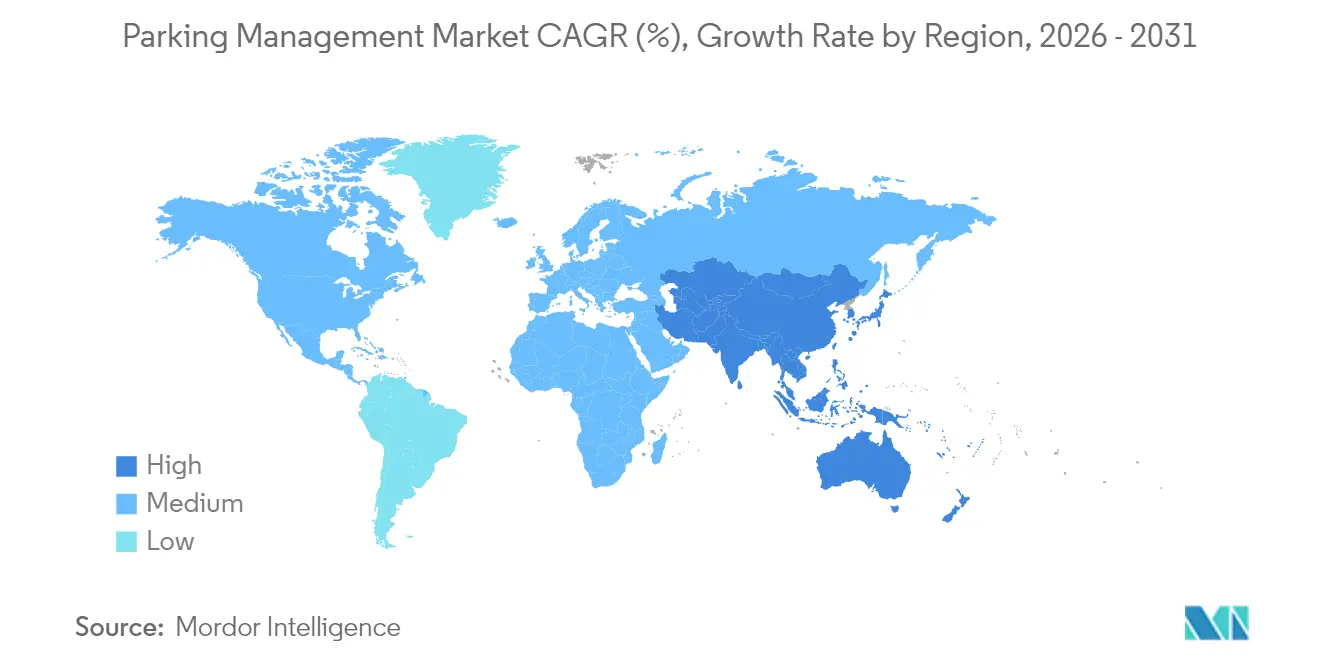

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

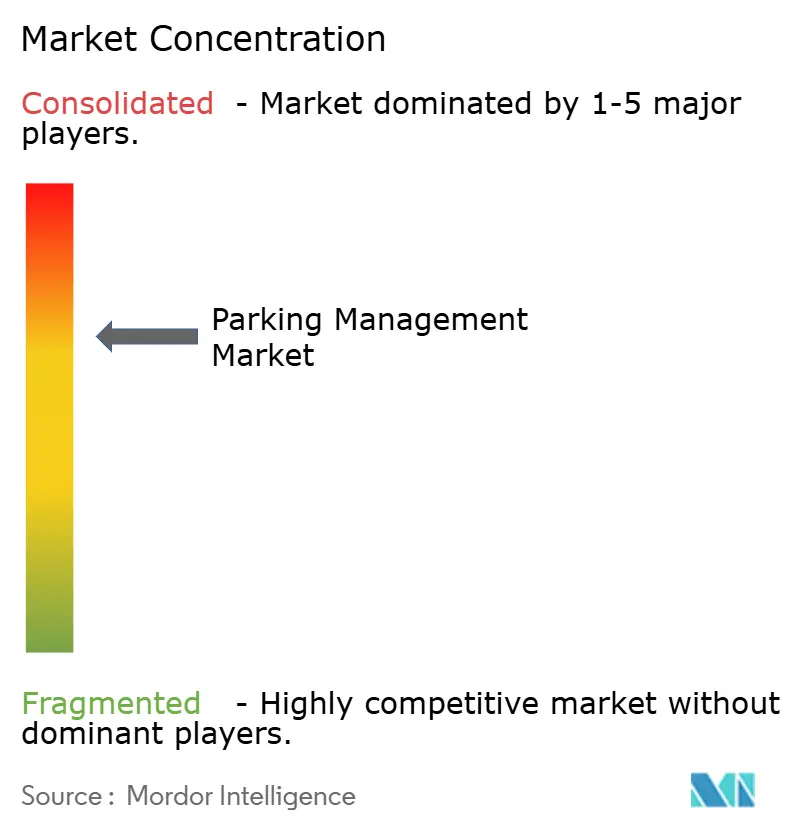

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Parking Management Market Analysis by Mordor Intelligence

The parking management market size was valued at USD 5.67 billion in 2025 and estimated to grow from USD 6.19 billion in 2026 to reach USD 9.58 billion by 2031, at a CAGR of 9.18% during the forecast period (2026-2031). Urban densification, dedicated smart-city funding, and the migration toward data-rich, cloud-based platforms are reshaping how cities, airports, and private operators monetize and regulate curb space.[1]Stephen Goldsmith, “Policy Change, Technology Key to Better Curb Management,” Government Technology, govtech.com Municipal digitization mandates in North America, national smart-city programs in Asia Pacific, and evolving EU sustainability targets collectively fuel demand for integrated solutions that pair license-plate recognition, dynamic pricing, and mobility-as-a-service (MaaS) capabilities. Hardware remains the largest revenue contributor, yet the fastest value creation now comes from analytics and managed services that turn occupancy data into operational intelligence. Competitive dynamics are shifting as infrastructure incumbents defend installed bases while AI-native entrants aggregate multi-site portfolios, often through high-profile acquisitions.

Key Report Takeaways

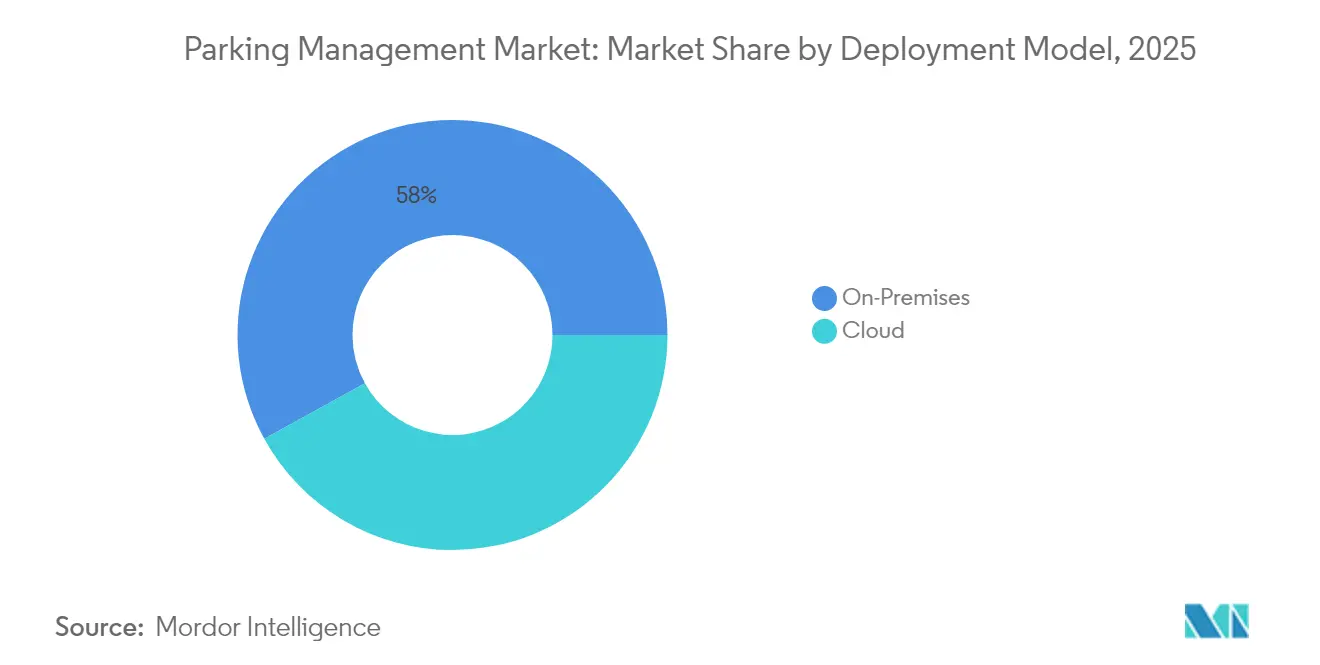

- By deployment model, on-premise systems led with 58.02% of parking management market share in 2025, while cloud platforms are forecast to expand at an 11.12% CAGR through 2031.

- By parking site, off-street facilities accounted for 61.57% of the parking management market size in 2025; on-street is advancing at an 11.28% CAGR to 2031.

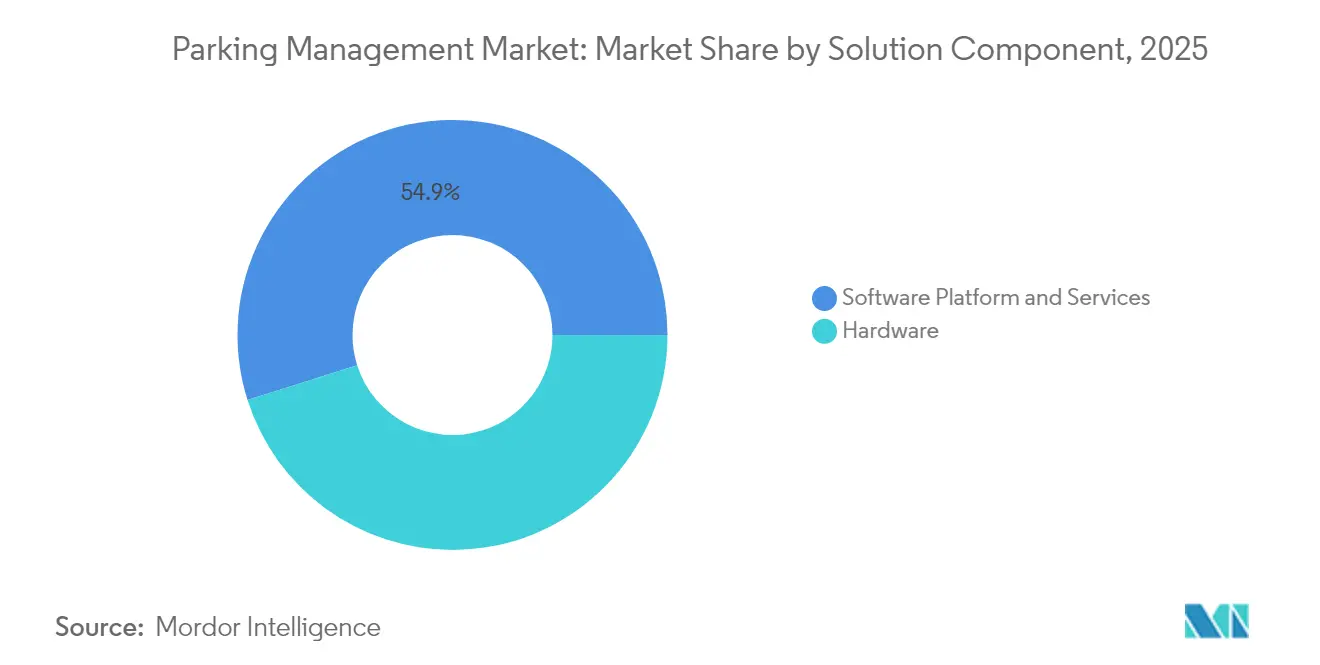

- By solution component, hardware captured 45.12% revenue share in 2025, whereas services represent the fastest-growing stream at a 10.41% CAGR to 2031.

- By end-user vertical, municipal and government operators held 36.31% revenue share in 2025; transit and airports are poised for a 9.66% CAGR through 2031.

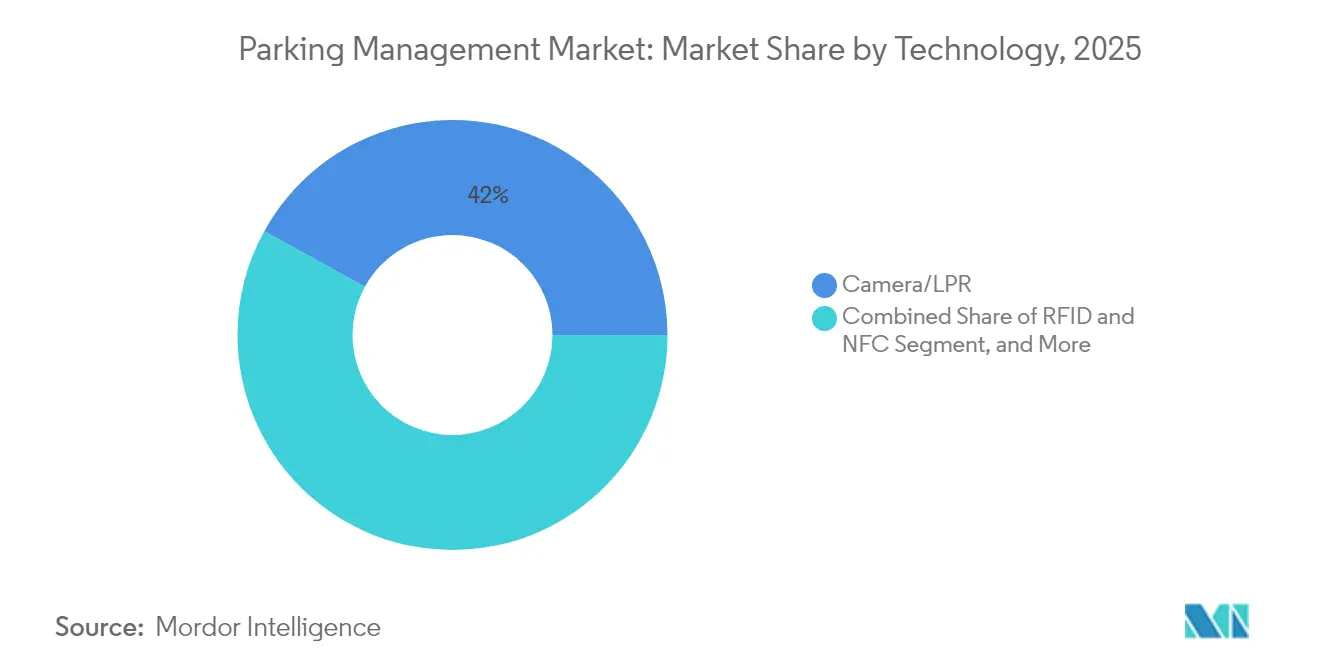

- By technology, camera and license-plate recognition dominated with 41.98% share of parking management market size in 2025, but mobile-app and Bluetooth solutions are rising at a 9.98% CAGR to 2031.

- By geography, North America commanded 38.96% revenue share in 2025, whereas Asia Pacific is projected to record a 9.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Parking Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban traffic congestion mitigation | +2.1% | Global, with peak impact in North America and APAC megacities | Medium term (2-4 years) |

| Smart-city funding for intelligent transport systems | +1.8% | North America and EU leading, APAC core following | Long term (≥ 4 years) |

| Cloud-native parking-as-a-service adoption | +1.6% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Mobile payment and digital ticketing penetration | +1.4% | Global, accelerated in APAC and North America | Short term (≤ 2 years) |

| MaaS-driven dynamic curb-pricing integration | +1.2% | EU and North America core, spill-over to APAC | Medium term (2-4 years) |

| Real-estate REIT monetisation of parking assets | +0.9% | North America and EU, with emerging interest in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Traffic Congestion Mitigation

Dynamic curb management programs demonstrate how parking can reduce vehicle circling and greenhouse-gas emissions. San Francisco’s SF Park recalibrates rates every six weeks to maintain 85% occupancy, producing documented 30% reductions in search traffic within pilot zones. Similar sensor-based deployments in Portland and Hoboken showcase transferable playbooks for mid-sized cities that lack the resources for bespoke research. Municipal agencies now position parking APIs alongside transit feeds, allowing navigation apps to direct drivers to the lowest-cost bay in real time. The approach reframes parking fees from static taxes to behavior-modifying levers that re-balance peak-hour loads. Emerging congestion-pricing proposals in Los Angeles and Singapore further elevate the role of parking data as an enforcement backbone.

Smart-City Funding for Intelligent Transport Systems

Dedicated federal and supra-national grants are lowering adoption risk for cash-strapped municipalities. In the United States, the Federal Highway Administration earmarked USD 2.3 billion through 2026 for 5G-enabled roadway and parking systems, with disbursements contingent on open-architecture and cybersecurity compliance.[2]Jason Carnes, “5G Impacts to Vehicles and Highway Infrastructure,” Federal Highway Administration, dhs.gov European cities tap into Horizon Europe funds to pilot curb-side EV-charging combined with automated parking guidance. Long-cycle capital unlocks multi-agency projects that fuse parking occupancy, traffic-signal timing, and public-transit arrival data into a single urban-mobility dashboard. Because eligibility criteria require interoperability, vendors that support standardized APIs gain a structural advantage when bids are scored.

Cloud-Native Parking-as-a-Service Adoption

Cloud migration compresses deployment windows and slashes upkeep costs by 40-60% relative to on-premise servers, according to operator case studies. Subscription bundles from providers such as SKIDATA include continuous security patches, AI-based fraud detection, and one-click tariff changes across multi-city portfolios. Centralized hosting also eases GDPR and PCI-DSS 4.0 compliance, enabling even small garages to meet enterprise-grade encryption benchmarks. As new mobility modes—from micromobility docks to autonomous-vehicle staging zones, surface, a cloud back end becomes the only practical way to coordinate asset status across thousands of edge devices.

Mobile Payment and Digital Ticketing Penetration

Seamless in-app checkout has shifted from convenience to baseline expectation in the parking management market. The Universal Plug and Charge protocol illustrates the convergence of EV charging, parking access, and payment authentication in a single handshake. Automakers embed parking APIs in infotainment stacks; 77% of Chinese drivers now demand such integration in connected vehicles. Operators report 20% revenue lifts after migrating from cash kiosks to contactless QR and NFC flows, due primarily to lower transaction friction and richer loyalty analytics. Digital receipts facilitate corporate expensing, further broadening the addressable user base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy vulnerabilities | -1.7% | Global, with stricter enforcement in EU and California | Short term (≤ 2 years) |

| High CAPEX and legacy-system integration complexity | -1.3% | North America and EU legacy infrastructure, emerging markets less affected | Medium term (2-4 years) |

| Equity backlash against dynamic pricing | -0.8% | North America and EU urban centers, with spillover to APAC | Medium term (2-4 years) |

| Lack of interoperability standards (vendor lock-in) | -0.6% | Global, with particular impact in fragmented municipal markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Privacy Vulnerabilities

Mandatory migration to PCI-DSS 4.0 after April 2024 exposed security gaps at facilities still running decade-old controllers. Breaches of license-plate databases in California and the Netherlands amplified public scrutiny, prompting regulators to widen audit scopes to include anonymization protocols. Large platforms responded by embedding zero-trust architectures and partnering with specialist security firms, but smaller garages struggle to fund continual penetration testing. EU proposals to classify curb-management data as “high-risk AI processing” may add algorithmic-transparency requirements that further stretch compliance budgets.

High CAPEX and Legacy-System Integration Complexity

Brownfield garages often require demolition of ticket dispensers and loop detectors before optical recognition can be installed, pushing per-facility upgrade costs above USD 50,000 for mid-tier assets. Flash Parking’s USD 85 million special-purpose vehicle offers lease-to-own packages that bundle equipment, software, and servicing fees, yet uptake remains uneven among municipal operators constrained by multiyear procurement cycles. Integration bottlenecks also arise when aligning numerous proprietary firmware versions, delaying rollout schedules and prolonging staff retraining periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Acceleration Despite On-Premises Dominance

The parking management market size for on-premise systems reached USD 3.29 billion in 2025, translating into a 58.02% revenue share. Operators value on-premise control for mission-critical gateways where sub-basement cellular signals remain unreliable. Even so, cloud-native offerings are expanding at an 11.12% CAGR as metropolitan Wi-Fi and private-LTE backbones mature. Cross-site dashboards allow portfolio owners to adjust tariffs globally with a single rule set, and automated disaster-recovery protocols minimize downtime risk.

Cloud adoption strengthens recurring-revenue visibility for vendors and stabilizes cash flows for asset owners via subscription OPEX rather than lumpy CAPEX. Because software patches roll out centrally, vulnerability windows shrink, aligning with PCI-DSS 4.0 audit cycles. Cloud architectures also simplify MaaS integrations, letting third-party apps conduct tokenized reservations without exposing garage networks. As a result, the parking management market sees a progressive blending of hybrid deployments where local gateways cache transactions but sync to cloud analytics.

By Parking Site: Off-Street Leadership with On-Street Growth Momentum

Off-street facilities generated USD 3.49 billion in revenue in 2025, underpinned by stable demand at airports, hospitals, and multi-tenant retail complexes. This accounted for 61.57% of the parking management market share. Yet on-street deployments show superior expansion, rising at an 11.28% CAGR on the back of digital curb-management ordinances in cities such as Birmingham and Guelph.

The on-street advance reflects a policy pivot that treats curb space as a multimodal asset. Real-time dashboards dispatch enforcement patrols only when sensors flag overstays, cutting overtime costs by 18%. Contactless meters and pay-by-plate apps lower cash-handling security risks, while variable rates raise turnover, boosting surrounding retail footfall. Vendors that offer integrated citation workflows and open-data feeds gain mindshare among planners seeking end-to-end transparency.

By Solution Component: Hardware Foundation with Services Acceleration

Hardware commanded USD 2.56 billion of parking management market size in 2025, covering cameras, gateways, and payment kiosks. Although capex-heavy, hardware establishes the data pipeline that software monetizes. Services—implementation, managed operations, and analytics consulting—posted the strongest growth at 10.41% CAGR as operators outsource complexity.

Outcome-based service contracts tie vendor remuneration to KPIs such as occupancy utilization and compliance uplift. Advanced IoT deployments with automated license-plate recognition have yielded 30% fewer billing disputes and 20% incremental revenue, validating the premium on expert configuration. Vendors embed AI models that forecast demand and propose tariff tweaks, nudging garages toward revenue-optimization paradigms long embraced in airline yield management.

By End-User Vertical: Municipal Leadership with Transit Growth

Municipal and government operators held USD 2.06 billion in revenue during 2025, equivalent to 36.31% share. City councils view parking data as a linchpin for emissions mitigation and street-design reform. Conversely, transit hubs and airports, although smaller today, are growing at a 9.66% CAGR as passenger-experience metrics elevate parking convenience to a competitive differentiator.

Airports now bundle curb reservations with flight-status alerts, shrinking average dwell times and freeing curb space for rideshare pick-ups. Some hubs integrate parking loyalty points redeemable for lounge access, creating ancillary revenue synergies. Rail operators retrofit park-and-ride lots with solar canopies and fast chargers, positioning parking assets as renewable micro-grids that offset traction-power needs.

By Technology: Camera/LPR Dominance with Mobile Innovation

Camera and license-plate recognition platforms represented 41.98% of 2025 revenue, anchoring automated entry, audit, and enforcement flows. Edge AI reduces false positives, allowing gateless “free-flow” garages to invoice vehicles post-exit, mirroring tolling paradigms. Mobile-app and Bluetooth credentials, however, are the fastest-rising category at a 9.98% CAGR as users gravitate toward access methods resident in smartphones and in-dash systems.

Sensor fusion is the next milestone: integrating LPR, ultrasonic stall counters, and BLE beacons provides redundant validation layers that enhance fraud detection and accessibility mapping. ISO 15118 vehicle-to-grid standards promise bidirectional authentication between EVs and parking infrastructure, enabling automated valet charging and dynamic energy-pricing participation.

Geography Analysis

North America retained 38.96% of global revenue in 2025, reflecting mature digitization mandates and early adoption of dynamic pricing. Municipalities leverage open-data policies that compel vendors to expose occupancy APIs, spurring third-party innovation in navigation and curb-delivery routing. PCI-DSS 4.0 enforcement and California Consumer Privacy Act amendments drive demand for tamper-resistant architectures. Operators deploy AI vision to remove gates, cutting average ingress times by 40% and elevating user satisfaction scores.

Asia Pacific follows a different trajectory, posting the fastest regional CAGR at 9.78%. Rapid urbanization in China, Japan, and South Korea creates acute land-use pressures, making efficient curb allocation a policy imperative. National smart-city blueprints fund sensor grids and 5G backbones that lower latency for cloud guidance. Automakers integrate Parkopedia feeds into dashboards, and QR payments embedded in super-apps normalize contactless parking even in tier-three cities. The region’s consumer tech literacy accelerates adoption curves, compressing time-to-scale for pilot solutions.

Europe balances data-privacy rigor with sustainability objectives. Revised GDPR cross-border transfer clauses in 2025 require data-localization or approved contractual mechanisms, leading many operators to choose regional cloud zones. EU Green Deal legislation links curb policy to modal-shift targets, incentivizing spaces reserved for micro-mobility docks and EV charging. Dynamic-pricing pilots in Stockholm and Madrid tie tariffs to emission classes, nudging fleets toward cleaner vehicles. While market growth is moderate, regulatory clarity supports vendor investment certainty.

South America and the Middle East and Africa remain emergent but increasingly visible in expansion roadmaps. São Paulo integrates parking sensors with flood-alert networks to reroute traffic during monsoon events, while Dubai positions smart-parking concessions as part of a “paperless government” strategy. Although project counts are lower, greenfield builds allow leapfrogging directly to cloud architectures without legacy constraints.

Competitive Landscape

Competition in the parking management market skews toward mid-level concentration. Infrastructure stalwarts such as SKIDATA, Flowbird, and Scheidt & Bachmann safeguard entrenched hardware footprints, offering modular upgrades to defend share. AI-native disruptors like Metropolis and Peter Park leverage computer vision and cloud orchestration to win greenfield urban-lot contracts. The strategic nature of curb data pushes vendors to ally rather than pursue stand-alone growth: EasyPark’s 2025 acquisition of Flowbird forged a hybrid powerhouse spanning mobile payments and terminal hardware.[4]EasyPark Group, “EasyPark Group Closes Acquisition of Flowbird,” easyparkgroup.com

Value-chain convergence continues. Bosch’s automated valet charging demonstration at CES 2024 marries parking and energy-management domains, opening revenue streams from vehicle-to-grid services. Flash Parking’s integration with Google Maps and Waze injects real-time bay availability into mainstream navigation, amplifying network effects. Vendors differentiate through compliance posture; those meeting PCI-DSS 4.0 and ISO 27001 benchmarks outpace rivals in public-sector tenders.

Capital deployment favors scalability plays: Metropolis used a USD 1.8 billion war chest to acquire SP Plus and instantly double its footprint to 4,000 locations. PE-backed roll-ups accelerate consolidation, yet local integrators retain niches by offering hyper-custom signage and zoning-code expertise. On balance, the top five companies control roughly 55% of revenue, indicating moderate concentration that leaves room for regional specialists.

Parking Management Industry Leaders

Amano McGann Inc.

TIBA Parking Systems (FAAC SpA)

FlashParking Inc.

Passport Labs Inc.

Flowbird Group SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EasyPark Group completed its acquisition of Flowbird Group, creating a global platform spanning 4,000 cities.

- October 2024: Metropolis closed USD 1.8 billion financing and took SP Plus private, expanding AI-powered vision parking across North America.

- October 2024: IEC approved OCPP as International Standard IEC 63584, formalizing EV-charger interoperability adopted by parking operators.

- September 2024: Flash Parking secured USD 85 million to finance EV-ready system upgrades, easing capital hurdles for garage owners.

Global Parking Management Market Report Scope

Parking management refers to the policies and programs that result in improved and efficient use of available parking resources. The parking management system constitutes the access control system, revenue management, security system, boom barrier, and many others.

The Parking Management Market is segmented by Deployment Type (On-premises, Cloud-based), Parking Site (Off-street, On-street), by Geography (North America, Europe, Asia Pacific , Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| On-premises |

| Cloud-based |

| Off-street |

| On-street |

| Hardware (Meters, Sensors, Cameras, LPR, Kiosks) |

| Software Platform |

| Services (Installation, Managed, Consulting) |

| Municipal and Government |

| Commercial Off-street Operators |

| Transit and Airports |

| Hospitality and Retail |

| Healthcare and Universities |

| Other End-User Verticals |

| Sensor-based (ultrasonic, magnetometer) |

| Camera / LPR-based |

| Mobile-app and Bluetooth |

| RFID and NFC |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | On-premises | ||

| Cloud-based | |||

| By Parking Site | Off-street | ||

| On-street | |||

| By Solution Component | Hardware (Meters, Sensors, Cameras, LPR, Kiosks) | ||

| Software Platform | |||

| Services (Installation, Managed, Consulting) | |||

| By End-User Vertical | Municipal and Government | ||

| Commercial Off-street Operators | |||

| Transit and Airports | |||

| Hospitality and Retail | |||

| Healthcare and Universities | |||

| Other End-User Verticals | |||

| By Technology | Sensor-based (ultrasonic, magnetometer) | ||

| Camera / LPR-based | |||

| Mobile-app and Bluetooth | |||

| RFID and NFC | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the parking management market in 2026?

The parking management market size stood at USD 6.19 billion in 2026, backed by smart-city investments and digital payment adoption.

What is the forecast CAGR for parking management solutions through 2031?

Revenue is projected to rise at a 9.18% CAGR, taking the market to USD 9.58 billion by 2031.

Which deployment model is growing fastest?

Cloud-based platforms are expanding at an 11.12% CAGR as operators migrate to scalable, centrally managed solutions.

Which region shows the strongest growth momentum?

Asia Pacific is the fastest-growing region with a 9.78% CAGR, propelled by rapid urbanization and government smart-city programs.

What technology currently dominates parking operations?

Camera and license-plate recognition systems hold 41.98% revenue share, forming the backbone of automated access and billing.

Page last updated on: