North America Stand-Up Pouch Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

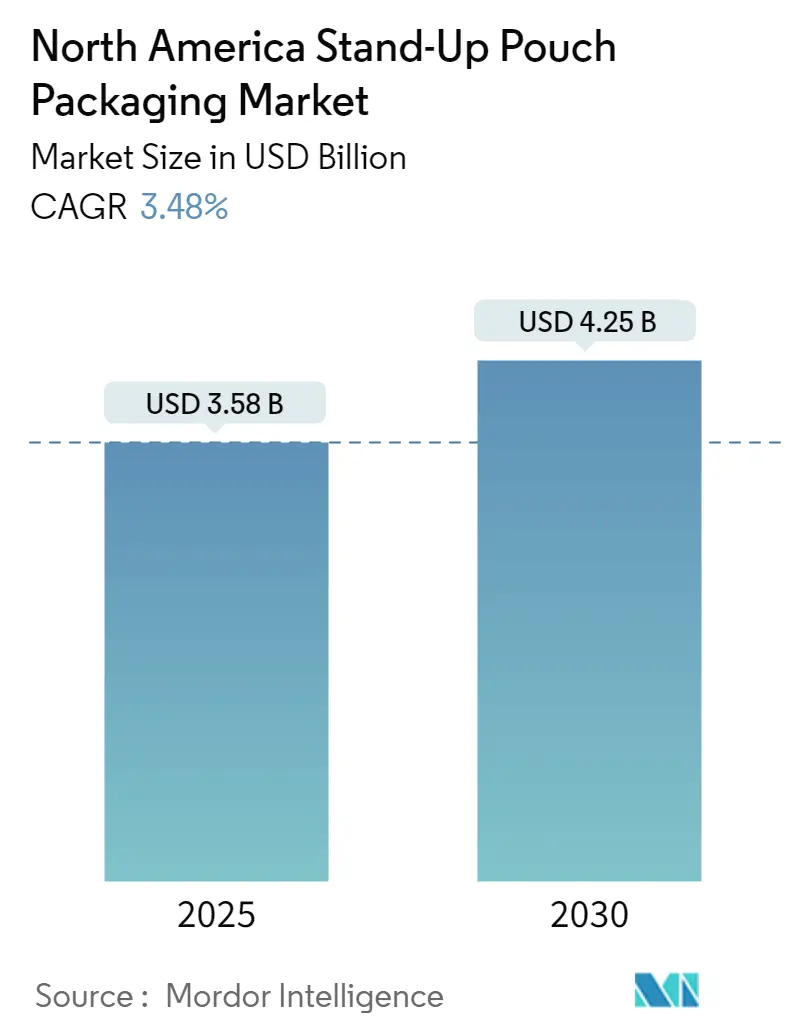

| Market Size (2025) | USD 3.58 Billion |

| Market Size (2030) | USD 4.25 Billion |

| Growth Rate (2025 - 2030) | 3.48% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Stand-Up Pouch Packaging Market Analysis by Mordor Intelligence

The North America Stand-Up Pouch Packaging Market size is worth USD 3.58 Billion in 2025, growing at an 3.48% CAGR and is forecast to hit USD 4.25 Billion by 2030.

The North American packaging industry is experiencing significant transformation driven by changing consumer preferences and technological advancements. According to the United States Census Bureau, the industry revenue of plastic bag and pouch manufacturing in New York alone generated USD 474.63 million in 2023, indicating robust regional manufacturing capabilities. The integration of advanced technologies in flexible packaging machinery and materials has become crucial for manufacturers to maintain competitiveness. Companies are increasingly investing in automation and smart consumer packaging solutions to improve efficiency and meet evolving market demands. The shift towards digital printing technologies has enabled manufacturers to offer more customized and visually appealing retail packaging solutions while reducing production time and costs.

The industry is witnessing a notable shift towards sustainable pouch packaging solutions, with manufacturers actively developing eco-friendly alternatives. In August 2023, Ahlstrom Oyj and Paper People LLC collaborated to launch an innovative fiber-based, recyclability-certified packaging solution for frozen food, demonstrating the industry's commitment to sustainability. Major players are forming strategic partnerships to accelerate sustainable innovation, as evidenced by PPC Flexible Packaging's partnership with Israel-based compostable packaging specialist Tipa in June 2023. These developments reflect the industry's response to increasing consumer awareness and regulatory pressure regarding environmental impact.

Consumer behavior patterns are significantly influencing packaging design and functionality requirements. According to Agriculture and Agri-Food Canada, retail sales of savory snacks in the United States reached USD 55.28 billion in 2022, driving demand for convenient and resealable flexible packaging solutions. The rise of e-commerce has necessitated the development of more durable and protective packaging designs. Manufacturers are responding by incorporating features such as enhanced barrier properties, tamper-evidence, and smart packaging elements that can monitor product freshness and authenticity.

The pet care industry has emerged as a significant driver of packaging innovation, with the American Pet Products Association reporting that pet industry expenditure in the United States exceeded USD 136 billion in 2022. This has led to increased demand for specialized flexible packaging solutions that ensure product freshness and convenience. Manufacturers are developing new pouch designs with features like easy-pour spouts, resealable closures, and enhanced barrier properties to meet the specific requirements of pet food and treats. The industry is also witnessing innovation in material science, with companies developing new polymer blends and barrier materials that extend shelf life while maintaining product quality.

North America Stand-Up Pouch Packaging Market Trends and Insights

Demand for Food and Beverage Expected to Grow in North America, Thereby Contributing to the Market Growth

The robust growth in food pouch packaging and beverage pouch packaging consumption across North America is creating substantial opportunities for the stand-up pouch packaging market. This is particularly evident in the coffee sector, where the United States consumption reached 26.3 million 60-kilogram bags in the 2022/2023 fiscal year, showing an increase from 25.94 million bags in 2020/2021. The rising coffee consumption has prompted manufacturers to invest in innovative packaging solutions that preserve product freshness and aroma, with stand-up pouches emerging as a preferred choice due to their ability to maintain product integrity and provide convenient storage options. Additionally, the shift in consumer preferences towards ready-to-eat meals and processed foods is reshaping the packaging landscape, with approximately 75% of Canada's food supply now coming from processed foods according to the University of Toronto's report.

The market is further strengthened by evolving consumer dietary preferences and health consciousness, particularly evident in the growing demand for plant-based products. In Canada, the retail sales of plant-based ready meals reached 22.1 million USD in 2022, up from 19.1 million USD in 2021, demonstrating the expanding market opportunity for specialized packaging solutions. The pet food sector is another significant driver, with Agriculture and Agri-Food Canada (AAFC) projecting retail sales to grow at a CAGR of 4.9%, reaching CAD 5.3 billion by 2025. This growth in various food and beverage segments is compelling manufacturers to develop specialized packaging solutions that cater to specific product requirements while ensuring extended shelf life and maintaining product quality.

Standard Pouches Offer a High Level of Convenience and Require Less Material Volume Compared to Alternatives

Stand-up pouches are revolutionizing the packaging industry through their innovative features that enhance consumer convenience while optimizing material usage. These pouches incorporate advanced closure systems such as zipper pouch packaging, sliders, and spout packs, providing consumers with easy-access options and reliable resealability. The integration of tear notches and easy-open features has made these pouches particularly popular in various applications, from pet food packaging to ready-to-eat meals. Furthermore, the lightweight nature of these pouches, combined with their high-barrier properties, offers superior protection against external elements such as moisture, oxygen, and light, ensuring product freshness while using significantly less material compared to traditional packaging alternatives.

The material efficiency of stand-up pouches extends beyond just reduced volume, as manufacturers are increasingly incorporating sustainable and eco-friendly materials in response to growing environmental concerns. Major packaging companies are reconsidering their packaging decisions, focusing on developing recyclable and sustainable solutions that maintain the convenience features consumers expect. The pouches' design flexibility allows for ample branding space and custom shapes, enabling brands to differentiate themselves on retail shelves while maintaining functional benefits. This combination of convenience packaging features and material efficiency has made stand-up pouches particularly attractive to businesses looking to optimize their packaging solutions while meeting consumer demands for user-friendly, sustainable packaging options. The rise of flexible plastic packaging further underscores the industry's shift towards innovative, sustainable solutions.

Segment Analysis: By Pack Type

Standard Segment in North America Stand-Up Pouch Packaging Market

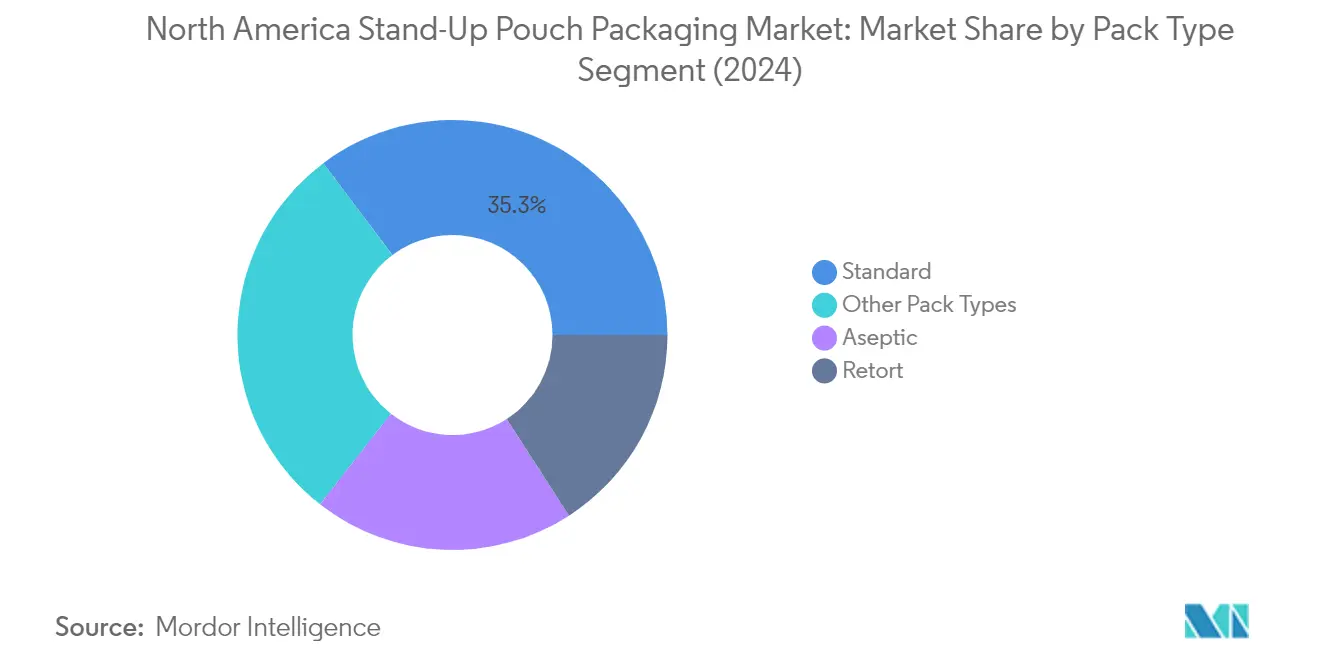

The standard segment maintains its dominant position in the North American stand-up pouch packaging market, commanding approximately 35% market share in 2024. Standard pouches have gained significant traction across various industries, particularly in food and beverage applications, due to their versatility and consumer-friendly features. These pouches offer excellent protection for products while providing convenient features like resealable pouch packaging and easy-opening mechanisms. The segment's growth is primarily driven by the increasing demand for processed and convenient packaged foods in the retail market, especially for products such as baby food, coffee, and juices, as these pouches help retain flavor and aroma while withstanding environmental effects. The adoption of standard pouches has been particularly strong in the organic food sector, where manufacturers value the pouches' ability to preserve product freshness and display attractive branding elements.

Retort Segment in North America Stand-Up Pouch Packaging Market

The retort pouch packaging segment is emerging as the fastest-growing category in the North American stand-up pouch packaging market, with a projected growth rate of approximately 4% from 2024 to 2029. This impressive growth is attributed to the increasing demand for packaging options that can extend the shelf life of various food products, particularly meat, seafood, poultry, and ready-to-eat meals. Retort pouch packaging is gaining popularity due to its ability to withstand high-temperature sterilization processes while maintaining product integrity and freshness. The segment's growth is further supported by technological advancements in material science, leading to the development of more durable and sustainable retort packaging solutions. Manufacturers are increasingly investing in recyclable retort pouch technologies, responding to both consumer demands for sustainability and regulatory requirements for environmentally friendly packaging solutions.

Remaining Segments in Pack Type

The aseptic and other pack types segments continue to play vital roles in the North American stand-up pouch packaging market. The aseptic segment is particularly significant in the pharmaceutical and food and beverage industries, where sterile packaging conditions are essential for product safety and longevity. This segment benefits from the growing demand for extended shelf-life products and ambient shipping solutions. Meanwhile, the other pack types segment, which includes specialized formats like gusseted pouch packaging and spouted pouches, serves unique market needs across various industries. These specialized formats are particularly popular in the beverage industry and for products requiring precise dispensing mechanisms, offering manufacturers flexibility in design and functionality to meet specific product requirements and consumer preferences.

Segment Analysis: By Material Type

Plastic Segment in North America Stand-Up Pouch Packaging Market

The plastic segment dominates the North America stand-up pouch packaging market, commanding approximately 84% market share in 2024. This substantial market presence is primarily attributed to plastic's versatility, cost-effectiveness, and superior barrier properties. The segment's dominance is further strengthened by technological improvements in lightweight packaging and the extensive use of materials like polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET). The plastic material's ability to provide strong resistance to UV light, oxygen, dust, and moisture makes it particularly attractive for food and beverage applications. Major manufacturers are increasingly focusing on developing sustainable solutions, with many introducing recyclable and bio-based alternatives to address environmental concerns while maintaining the material's performance benefits.

Paper Segment in North America Stand-Up Pouch Packaging Market

The paper segment is emerging as the fastest-growing category in the North America stand-up pouch packaging market, projected to grow at approximately 5% from 2024 to 2029. This growth is driven by increasing consumer awareness and regulatory pressure for sustainable packaging solutions. Paper pouches are gaining significant traction due to their 100% reusable, recyclable, and biodegradable properties, making them an environmentally friendly alternative to traditional packaging materials. The segment's growth is further supported by innovations in kraft paper pouches, which offer enhanced strength and durability while maintaining eco-friendly characteristics. Major brands are actively transitioning to paper-based solutions, particularly in the food and beverage industry, where consumer demand for sustainable packaging continues to rise.

Remaining Segments in Material Type

The metal/foil segment plays a crucial role in the North America stand-up pouch packaging market, particularly in applications requiring superior barrier properties and extended shelf life. Metal/foil pouches, often referred to as metallized pouches, offer exceptional protection against external elements and are particularly valued in the packaging of sensitive products such as coffee, tea, and pharmaceutical items. The segment's importance is emphasized by its ability to provide maximum oxygen, aroma, and water vapor barrier properties, making it indispensable for certain high-performance packaging applications where product preservation is paramount.

Segment Analysis: By End-User

Food Segment in North America Stand-Up Pouch Packaging Market

The food segment continues to dominate the North America stand-up pouch packaging market, commanding approximately 47% market share in 2024. This significant market position is driven by the increasing adoption of stand-up pouches in various food applications, including snacks, candy-based products, processed foods, meat, poultry, seafood, and dairy products. The segment's growth is primarily attributed to the rising demand for convenient packaging solutions that can preserve food freshness, extend shelf life, and offer easy storage and transportation options. Stand-up pouches have become particularly popular in the food sector due to their ability to provide excellent barrier properties against moisture, odors, and external contaminants, while also offering features like resealable zippers and clear windows for product visibility. The segment's strong performance is further supported by the growing consumer preference for portable, lightweight packaging solutions that align with modern lifestyle needs and the increasing demand for ready-to-eat and processed food products.

Beverages Segment in North America Stand-Up Pouch Packaging Market

The beverages segment is emerging as the fastest-growing category in the North America stand-up pouch packaging market, with a projected growth rate of approximately 4% from 2024 to 2029. This accelerated growth is primarily driven by the increasing adoption of spouted pouch packaging in various beverage applications, including fruit juices, energy drinks, and other liquid pouch packaging products. The segment's rapid expansion is attributed to the superior convenience offered by stand-up pouches, particularly those equipped with spouts and innovative dispensing systems. These packaging solutions are gaining popularity among beverage manufacturers due to their cost-effectiveness compared to rigid packaging alternatives and their ability to provide enhanced shelf presence. The growth is further supported by the rising demand for on-the-go beverage consumption and the increasing preference for lightweight, portable packaging solutions that offer better handling and storage capabilities while maintaining product freshness and quality.

Remaining Segments in End-User Segmentation

The other segments in the North America stand-up pouch packaging market include pet food, medical and pharmaceutical, home and personal care, and other end-users, each serving distinct market needs. The pet food segment has established a strong presence due to the growing pet ownership trends and the increasing demand for premium pet food products with convenient packaging solutions. The medical and pharmaceutical segment focuses on providing sterile, secure packaging options with features like child-resistant closures and tamper-evident seals. The home and personal care segment caters to products such as detergents, cosmetics, and personal hygiene items, emphasizing the need for moisture-resistant and user-friendly packaging. These segments collectively contribute to the market's diversity and demonstrate the versatility of stand-up pouch packaging across various applications, each driven by specific industry requirements and consumer preferences.

North America Stand-Up Pouch Packaging Market Geography Segment Analysis

Stand-Up Pouch Packaging Market in the United States

The United States dominates the North American stand-up pouch packaging market, commanding approximately 86% of the total market share in 2024. The market's robust performance is driven by the high consumption of processed food and evolving consumer preferences towards sustainable flexible packaging solutions. Manufacturing companies in the United States are strategically positioned to capitalize on the growing demand for stand-up pouches, particularly in ready-to-use and on-the-go food packaging segments. The exceptional barrier properties of these pouches ensure product freshness and protection from external factors, contributing significantly to their widespread adoption. Beyond food and beverage applications, the market has witnessed substantial growth in home care product categories, where pouches with spouts and dispensing features provide convenience and minimize product wastage. The country's emphasis on recyclable films and pouches, driven by consumer demand for eco-friendly options, has further accelerated market growth. Stand-up pouch manufacturers in the region are actively pursuing strategic partnerships to leverage shared expertise and foster innovations, resulting in more robust and diversified product offerings.

Stand-Up Pouch Packaging Market in Canada

The Canadian stand-up pouch packaging market has demonstrated remarkable resilience and growth, recording an impressive growth rate of approximately 5% during the period 2019-2024. The market's expansion is primarily attributed to the prevalent reliance on packaged and processed foods, with reports indicating that approximately 75% of the nation's food supply comes from processed foods. The food industry's rapid evolution and changing packaging alternatives have attracted numerous businesses to reconsider their packaging decisions as more eco-friendly and sustainable solutions become available. Local manufacturers like Logos Pack, Omniplast, Canada Brown, Rootree, and Grauman Packaging have played pivotal roles in market development. The pet food industry has emerged as a significant growth driver, with stand-up pouches becoming increasingly popular for both dry and wet pet food packaging. The healthcare sector has also contributed substantially to market growth, with spouted stand-up pouches gaining traction for medical products due to their precision in dispensing and enhanced safety features. The market has witnessed significant corporate expansions and strategic acquisitions, reflecting the growing demand across various end-user segments. Additionally, the adoption of doypack packaging in retail has further bolstered the market's appeal, offering versatile and user-friendly retail packaging solutions.

Competitive Landscape

Top Companies in North America Stand-Up Pouch Packaging Market

The market features established players like Amcor, Mondi, Sealed Air, Sonoco Products, and Smurfit Kappa Group leading the innovation landscape through sustainable pouch packaging solutions and advanced manufacturing capabilities. Companies are increasingly focusing on developing recyclable pouch packaging and mono-material pouches to align with environmental regulations and changing consumer preferences. Strategic partnerships and collaborations with technology providers are enabling enhanced product features like smart packaging solutions and improved barrier properties. Operational excellence is being achieved through investments in automated manufacturing processes and digital transformation initiatives. Geographic expansion strategies are primarily centered around acquisitions of regional players to strengthen market presence and distribution networks. The emphasis on research and development has accelerated the introduction of novel closure systems, spouted variants, and customized solutions for specific end-user applications.

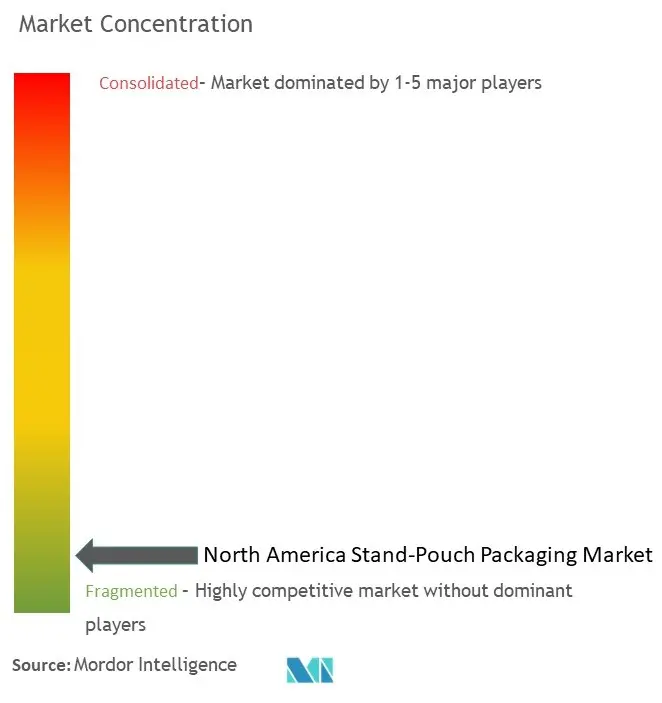

Fragmented Market with Strong Regional Players

The North American stand-up pouch packaging market exhibits a fragmented structure characterized by the presence of both global conglomerates and specialized regional manufacturers. Global players leverage their extensive research capabilities, established distribution networks, and economies of scale to maintain a competitive advantage, while regional players compete through customization capabilities and quick turnaround times. The market demonstrates moderate consolidation levels, with larger companies actively pursuing strategic acquisitions to expand their product portfolio and geographic reach. The competitive dynamics are further shaped by the presence of vertically integrated manufacturers who control various aspects of the value chain, from material production to end-product manufacturing.

Merger and acquisition activities in the market are primarily driven by the need to acquire technological capabilities, expand manufacturing capacity, and gain access to new customer segments. Companies are increasingly focusing on acquiring specialized manufacturers with expertise in sustainable pouch packaging solutions and advanced manufacturing processes. The trend of consolidation is particularly evident in regions with high growth potential, where larger players are acquiring local manufacturers to strengthen their market position. Strategic partnerships and joint ventures are becoming common as companies seek to combine complementary strengths and share technological expertise.

Innovation and Sustainability Drive Market Success

For established players to maintain and increase their market share, a multi-faceted approach combining technological innovation, sustainability initiatives, and customer-centric solutions is essential. Companies need to invest in advanced manufacturing capabilities while simultaneously developing eco-friendly packaging solutions that meet stringent regulatory requirements. Building strong relationships with key end-users through customized solutions and value-added services is becoming increasingly important. The ability to offer comprehensive packaging solutions, including design support, technical assistance, and after-sales service, helps in creating differentiation in a competitive market.

New entrants and emerging players can gain ground by focusing on niche market segments and developing specialized solutions for specific applications. Success factors include establishing strong relationships with raw material suppliers, investing in flexible manufacturing capabilities, and developing innovative solutions that address unmet market needs. The threat of substitution from alternative packaging formats necessitates continuous innovation in product design and functionality. Regulatory compliance, particularly regarding environmental sustainability and food safety, remains a critical factor for success. Companies need to stay ahead of evolving regulations and consumer preferences while maintaining cost competitiveness through operational efficiency and strategic sourcing. The role of flexible packaging in this context cannot be understated, as it offers adaptability and efficiency in meeting diverse consumer demands.

North America Stand-Up Pouch Packaging Industry Leaders

Amcor PLC

Mondi Group

Sealed Air Corporation

Sonoco Products Company

Smurfit Kappa Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023 - ProAmpac launched its ProActive PCR retort pouches, a sustainable alternative to conventional retort options. ProActive PCR Retort pouches are designed to reduce virgin plastics usage and contain up to 30% post-consumer recycled (PCR) material by mass. ProActive PCR Retort pouches are specifically designed for products such as shelf-stable ready-to-eat proteins, which demand ultra-high barrier and high-heat resistance.

- February 2023 - PPC Flexible Packaging acquired Israel-based StePac, MAPfresh Holdings (StePac). By combining PPT’s existing portfolio, this acquisition is expected to bring mutual customers a much more diverse selection of options, ultimately delivering industry-leading sustainable solutions. PPC Flexible’s growth strategy through acquisition is a multifaceted approach aimed at expanding market presence, diversifying product offerings, optimizing operations, and staying ahead in a competitive industry. Each acquisition plays a strategic role in reinforcing the company’s position and contributing to its overall growth. In

North America Stand-Up Pouch Packaging Market Report Scope

The study covers the North American stand-up pouch market tracked in terms of volume (consumption demand) and revenue generated from different types of stand-up pouches. The stand-up pouch is a type of flexible packaging that can stand erect on its bottom for display, storage, and convenience and is generally made up of raw materials, such as plastic, paper, and metal/foil used across industries, such as food, beverages, medical & pharmaceutical, pet food, and others. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the stand-up pouch market in terms of drivers and restraints.

The North America stand-up pouch packaging market is segmented by pack type (standard, aseptic, retort, other pack types), by material type (plastic [PE, PP, PVC, EVOH, bio-plastics], metal/foil, paper), by end-user (food, beverages, medical & pharmaceutical, pet food, home and personal care, other end-users), by country (United States, Canada). The market sizes and forecasts are provided in terms of value in USD and volume in units for all the above segments.

| Standard |

| Aseptic |

| Retort |

| Other Pack Types |

| Plastic (PE, PP, PVC, EVOH, Bio-Plastics) |

| Metal/Foil |

| Paper |

| Food |

| Beverages |

| Medical and Pharmaceutical |

| Pet Food |

| Home and Personal Care |

| Other End Users |

| United States |

| Canada |

| By Pack Type | Standard |

| Aseptic | |

| Retort | |

| Other Pack Types | |

| By Material Type | Plastic (PE, PP, PVC, EVOH, Bio-Plastics) |

| Metal/Foil | |

| Paper | |

| By End User | Food |

| Beverages | |

| Medical and Pharmaceutical | |

| Pet Food | |

| Home and Personal Care | |

| Other End Users | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

How big is the North America Stand-Up Pouch Packaging Market?

The North America Stand-Up Pouch Packaging Market size is worth USD 3.58 billion in 2025, growing at an 3.48% CAGR and is forecast to hit USD 4.25 billion by 2030.

What is the current North America Stand-Up Pouch Packaging Market size?

In 2025, the North America Stand-Up Pouch Packaging Market size is expected to reach USD 3.58 billion.

What years does this North America Stand-Up Pouch Packaging Market cover, and what was the market size in 2024?

In 2024, the North America Stand-Up Pouch Packaging Market size was estimated at USD 3.46 billion. The report covers the North America Stand-Up Pouch Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Stand-Up Pouch Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: