Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

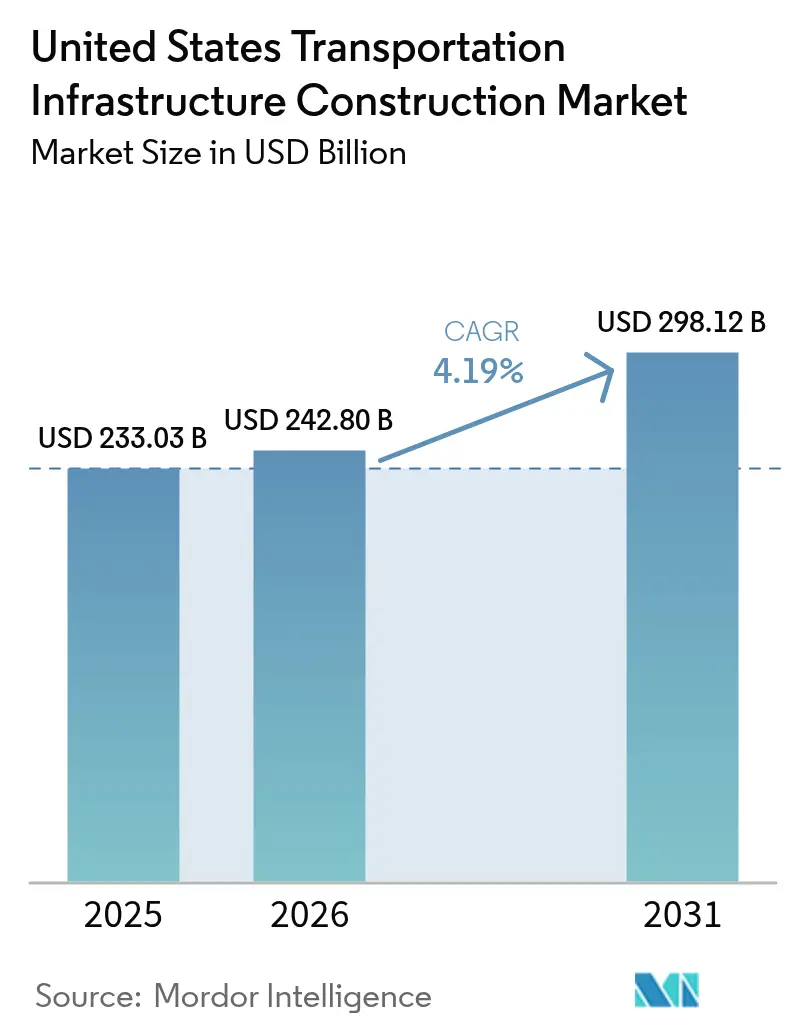

| Base Year Market Size (2025) | USD 233.03 Billion |

| Market Size (2026) | USD 242.8 Billion |

| Market Size (2031) | USD 298.12 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The United States Transportation Infrastructure Construction Market size is expected to grow from USD 233.03 billion in 2025 to USD 242.8 billion in 2026 and is forecast to reach USD 298.12 billion by 2031 at 4.19% CAGR over 2026-2031. Robust federal appropriations under the Infrastructure Investment and Jobs Act (IIJA), rising state‐level allocations, and growing private capital participation are sustaining this growth momentum. Public dollars remain the market’s financial anchor, but public-private partnerships are accelerating complex megaproject delivery timelines. Rail, aviation, and electric-vehicle (EV) charging corridors are emerging as complementary focal points to the country’s vast highway network. Contractors are countering skilled-labor shortages and material-price swings by investing in digital workflows and modular methods, fostering productivity gains that partially offset cost inflation. Even so, execution risks tied to funding-match gaps and volatile input prices persist, particularly in rural counties and small metropolitan areas.

Key Report Takeaways

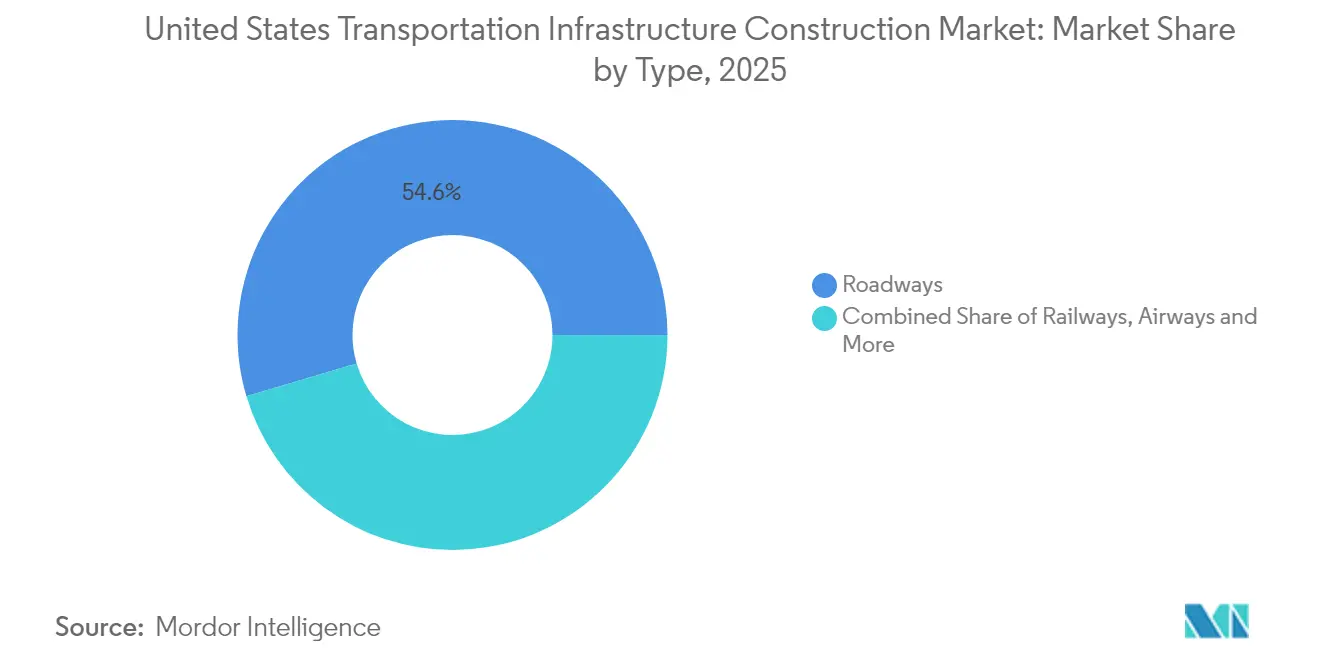

- By type, roadways led with 54.60% revenue share of the US transportation infrastructure construction market in 2025, while railways are forecast to post the fastest 5.18% CAGR to 2031.

- By construction type, new construction accounted for 60.30% of the US transportation infrastructure construction market size in 2025 and is projected to grow at a 4.95% CAGR through 2031.

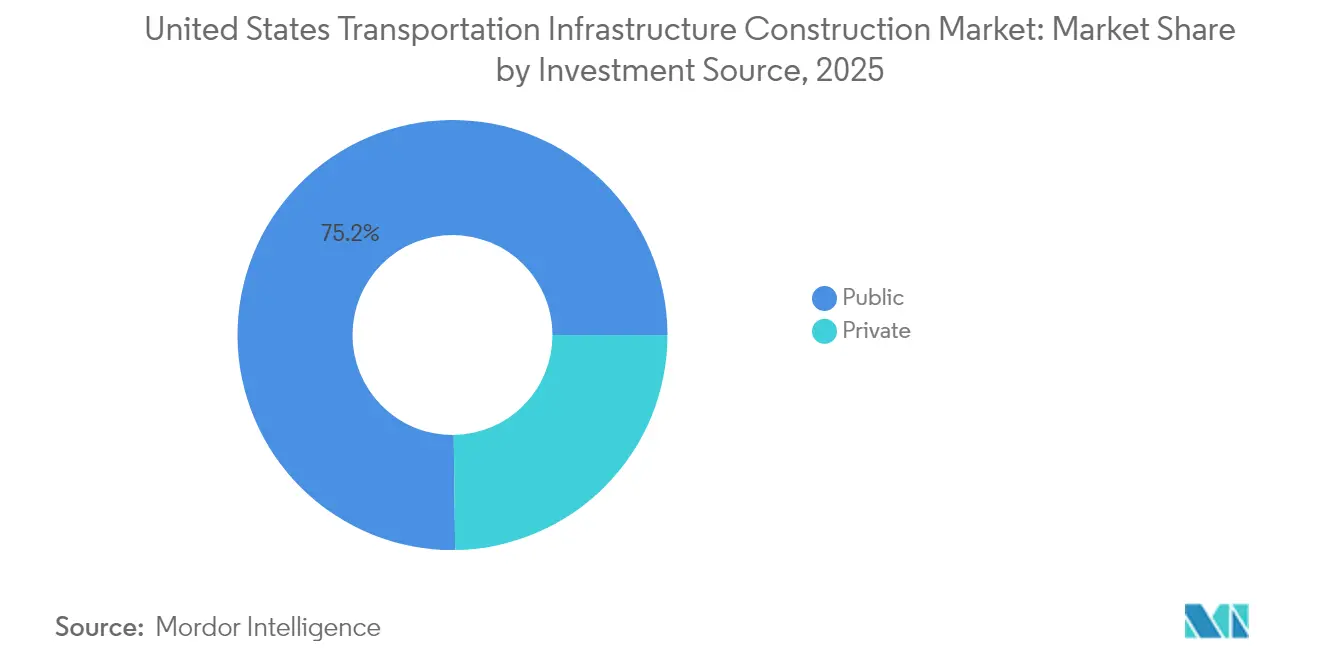

- By investment source, public funds represented 75.20% of spending in 2025; the private-capital segment is advancing at a 5.32% CAGR, reflecting deeper public-private-partnership pipelines.

- By geography, Texas commanded 10.85% of 2025 spending and is expected to register a 4.86% CAGR between 2026 and 2031, the highest among all states.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Federal & State Rail Initiatives | +1.2% | Northeast Corridor, California, Texas | Medium term (2-4 years) |

| E-commerce Freight Connectivity | +0.9% | Urban logistics hubs & port regions | Long term (≥ 4 years) |

| Airport Revitalization Programs | +0.8% | Major metropolitan airports | Medium term (2-4 years) |

| Nationwide EV Charging Roll-out | +0.7% | CA, NY, FL, TX, national corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ongoing Federal and State Rail Initiatives Supporting Long-Distance and Regional Corridor Upgrades

The USD 66 billion rail allocation embedded in the IIJA is triggering a wave of projects aimed at capacity, safety, and passenger-service improvements. Since January 2025, the Railroad Crossing Elimination Grant Program has awarded USD 1.1 billion across 123 projects, removing chokepoints that slow both freight and passenger services. Amtrak’s goal of 64 million riders by 2040, up from 33 million pre-pandemic, is sharpening the focus on double-tracking, signaling upgrades, and station overhauls. Private rail operators are complementing federal outlays; Norfolk Southern’s USD 200 million freight-corridor upgrade in Alabama exemplifies this synergy.

E-Commerce Expansion Driving Nationwide Demand for Freight Terminals, Warehousing, and Intermodal Connectivity

E-commerce sales volumes are heightening the need for freight-terminal capacity, short-haul rail spurs, and last-mile delivery depots. Colorado’s 2024 Freight Plan cites rising parcel traffic as a catalyst for intermodal yard redesigns. Warehouse construction costs climbed 38% between 2020 and 2023 before stabilizing in 2024, underscoring the capital intensity of logistics real estate. Containerized freight movements reached record highs in 2024, further stretching terminal throughput.

Airport Revitalization Programs Advancing Terminal Expansions, Runway Upgrades, and Safety Enhancements

Ongoing airport revitalization programs across the United States are significantly transforming aviation infrastructure, with a strong push toward modernizing terminal facilities, enhancing runway capacity, and integrating multimodal connectivity. Backed by the Airport Terminal Program, which allocates approximately USD 1 billion annually, airports are upgrading critical components such as gates, baggage handling systems, and passenger access points.

Major capital programs like Sacramento International Airport’s USD 1.3 billion SMForward initiative and Miami International Airport’s USD 7 billion expansion plan exemplify the scale of investment aimed at accommodating future demand. According to the Federal Aviation Administration, passenger enplanements are expected to increase by 38% by 2033, further driving the need for extended runways, advanced safety systems, and seamless intermodal transfer facilities. These programs underscore a broader federal and regional commitment to enhancing the resilience, efficiency, and passenger experience across the U.S. airport network.

Nationwide EV Infrastructure Deployment Integrating Charging Stations Across Highway Networks and Urban Centers

The rapid rollout of electric vehicle (EV) infrastructure is emerging as a key growth driver for the U.S. transportation infrastructure construction market. By late 2024, over 183,000 public charging ports, including 43,152 DC fast chargers, had been deployed, reflecting accelerating demand for EV-ready transport corridors. Under the NEVI formula program, the federal government aims to install 500,000 public chargers by 2030, supported by USD 7.5 billion in IIJA funding.

Recent allocations, including USD 635 million announced in January 2025 to add 11,500 ports across 27 states, are fueling construction activity, particularly in underserved areas, where two-thirds of the funding is directed. In parallel, utilities plan to invest USD 5.3 billion in grid modernization to support a projected 78.5 million EVs on U.S. roads by 2035. These investments are stimulating demand for civil works, electrical infrastructure, and roadside facilities, reinforcing EV infrastructure as a transformative force in U.S. transport development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gaps in Federal–State Matching Funds | -0.6% | Rural & economically disadvantaged areas | Medium term (2-4 years) |

| Skilled-Labor Deficits | -0.8% | High-growth states, national | Short term (≤ 2 years) |

| Construction Input Price Volatility | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gaps in Federal–State Matching Requirements Creating Bottlenecks for Transportation Projects in Underserved Regions

The Congressional Research Service projects a USD 40 billion annual shortfall in the Highway Trust Fund by decade-end if current outflows persist. Rural counties often lack fiscal headroom to supply matching dollars, delaying bridge reconstructions, road widenings, and rural transit hubs. Proposed cuts in the House continuing-resolution draft would remove USD 2 billion earmarked for local safety projects, aggravating already thin capital pipelines.

Widespread Skilled Labor Deficits Driving Higher Construction Costs and Project Delays

The U.S. transportation infrastructure market is under strain from a persistent skilled labor shortage, despite a recent decline in construction job openings to 248,000 in April 2025. Wage pressures remain acute, with the average hourly pay climbing to USD 36.05[2]Engineering News-Record, “BLS: Construction Job Openings Are Down in April” , reflecting intense competition for qualified workers. This labor gap continues to drive up construction costs and contributes to delays in major infrastructure projects, particularly those requiring specialized skills in transit, electrical, and bridge systems. Compounding the issue, existing training pipelines are misaligned with market needs, limiting the industry’s ability to meet rising demand despite robust federal funding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Roadways Dominate Infrastructure Investment

The roadways segment kept its lead in 2025, accounting for 54.60% of total spending. Highways remain the backbone of U.S. mobility, and investors took notice: contract awards for highways and bridges hit a record USD 121 billion in 2024. Federal backing is equally strong. The Infrastructure Investment and Jobs Act set aside about USD 350 billion for highway programs through 2026, while the Biden-Harris Administration sent USD 62 billion to states for FY 2025, USD 18.8 billion more than in FY 2021. Industry leaders such as Bechtel, AECOM, and Skanska are vying for new interstate widenings and bridge replacements that upgrade aging assets.

Railways are growing fastest, with a 5.18% CAGR projected for 2026-2031. A USD 66 billion federal infusion under the IIJA is the main catalyst. In January 2025, the Federal Railroad Administration awarded USD 1.1 billion across 123 projects to remove grade crossings and improve safety. The airways segment benefits from an annual USD 1 billion Airport Terminal Program that funds terminal upgrades. Ports and inland waterways receive another USD 450 million through the FY 2025 Port Infrastructure Development Program. Better links among these modes are now essential: Colorado’s 2024 Freight Plan highlights intermodal projects that align highways, rail spurs, and distribution hubs to meet e-commerce demand freight.colorado.gov.

By Construction Type: New Construction Addresses Capacity Constraints

New builds represented 60.30% of the US transportation infrastructure construction market size in 2025 and are expected to expand at a 4.95% CAGR through 2031, supported by an 8.5% predicted rise in 2025 construction starts. Megaproject pipelines feature USD 49 billion in upcoming terminal works and USD 33 billion in highway increments. Capacity-driven projects in fast-growing Sun Belt metros emphasize additional lanes, flyovers, and managed toll lanes—each requiring extensive right-of-way acquisition and complex staging schedules, thereby favoring large, vertically integrated contractors.

Renovation activity, though slower growing, remains critical for legacy asset upkeep. The 2025 American Society of Civil Engineers Report Card raised overall infrastructure scores, yet highlighted a USD 3.7 trillion repair backlog. Asset owners are blending repair scopes into larger corridor upgrades to limit user disruption. Digital twin models and reality-capture scans are now standard in design packages, enhancing precision in rehabilitation plans—a practice increasingly embedded across the US transportation infrastructure construction industry.

By Investment Source: Private Capital Accelerates Growth

Public funds still anchor 75.20% of spending, but private capital’s 5.32% CAGR through 2031 signals shifting financing dynamics. The Build America Bureau’s May 2025 pipeline lists USD 12.7 billion in credit-assistance requests, including the Midtown Bus Terminal replacement and multiple intercity railcars procurements. Electric utilities are channeling USD 5.3 billion into EV charging grids, further boosting privately financed workloads. Capital-stack innovation—blending TIFIA loans, private-activity bonds, and equity tranches—is unlocking schedules otherwise hampered by public-budget constraints, strengthening value creation across the US transportation infrastructure construction market.

Geography Analysis

Texas captured 10.85% of the 2025 expenditure and is projected to expand at a 4.86% CAGR through 2031, the highest growth trajectory in the US transportation infrastructure construction market. The USD 148 billion Unified Transportation Program earmarks USD 43 billion for roadway development and maintenance, anticipating a 34% population surge by 2050. Over 3,181 publicly accessible charging locations position Texas for accelerated EV uptake. Freight corridor upgrades plus border-crossing enhancements amplify the state’s logistics competitiveness.

California remains a heavyweight, despite the governor’s USD 4.3 billion in transportation budget shifts for FY 2024-25. The state leads with 15,673 charging locations and is deploying 1,100+ new EV ports across two funding solicitations under its NEVI plan. Senate Bill 1 continues to stimulate county-level economic output, bolstering construction demand. Sustainable-transport planning grants prioritize climate resilience, multimodal access, and zero-emission freight corridors.

New York, Florida, and Illinois comprise the remaining top-five spenders. New York’s proposed USD 68.4 billion MTA capital plan elevates subway accessibility and railcar procurement. Florida tracks input costs closely; asphalt dropped 8.1% to USD 167 per ton in early 2025, slightly easing highway budget pressures. Illinois leverages IIJA dollars to modernize inland waterways critical for Midwest grain exports. Regions lacking fiscal capacity continue to struggle with matching-fund gaps, widening service disparities across the broader US transportation infrastructure construction market.

Competitive Landscape

The U.S. transportation infrastructure construction market is moderately concentrated, with major firms such as Bechtel Corporation, Fluor Corporation, AECOM, Skanska, Kiewit, and Turner Construction leading the execution of large-scale projects. These companies play a significant role in shaping national infrastructure development, particularly in complex, high-value undertakings. Increasingly, digital capabilities and strong ESG credentials are becoming key differentiators in securing project bids and maintaining long-term competitiveness.

Fluor posted USD 15.5 billion in 2023 revenue, with 76% of its backlog now reimbursable, signaling a preference for lower-risk contract structures. Skanska is piloting AI-enabled equipment tracking to mitigate idle time and reduce carbon footprints.

Merger and acquisition activity remains brisk: Home Depot’s USD 18.3 billion purchase of SRS Distribution and Quikrete’s USD 6 billion Summit Materials acquisition exemplify upstream consolidation aimed at securing material supplies. Specialty contractors are carving niches in EV-charging installations and climate-resilient retrofits, expanding the competitive field while keeping the US transportation infrastructure construction market dynamic.

United States Transportation Infrastructure Construction Industry Leaders

Bechtel Corporation

Fluor Corporation

Kiewit Corporation

AECOM

Skanska USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Port Authority of NY & NJ advanced a USD 9.4 billion 2025 budget with USD 3.6 billion slated for capital investments.

- March 2025: MTA released its proposed USD 68.4 billion 2025-2029 capital plan, prioritizing accessibility and rolling-stock renewal.

- January 2025: The Biden-Harris Administration awarded USD 635 million for 11,500 additional public EV charging ports across 27 states, with 67% targeting disadvantaged communities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States transportation infrastructure construction market as all value of work put in place for new build or major renovation of publicly accessible roadways, railways, airports, and ports or inland waterways, measured in constant 2024 dollars from contract award through substantial completion. This definition follows the asset-based view used by federal agencies and includes publicly funded design-build projects that are delivered through public-private partnerships.

Scope exclusion: minor routine maintenance jobs and purely building-related work inside terminals are left outside the sizing.

Segmentation Overview

- By Type

- Roadways

- Railways

- Airways

- Ports and Inland Waterways

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By States

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with state transportation budget officers, Class-I freight rail planners, tier-one civil contractors, and airport program managers across the South, Midwest, and Pacific regions. Their insights clarified bid price escalation, typical lead times, and the share of design-build contracts, allowing us to fine-tune cost curves and validate our assumed project pipelines.

Desk Research

We began with government sources that track hard spending, such as the United States Department of Transportation, the Bureau of Transportation Statistics, the Federal Transit Administration, and the Federal Aviation Administration. State DOT capital plans, the American Road & Transportation Builders Association outlook, and U.S. Census 'Value of Construction Put in Place' tables gave timely contract values that anchor our base year. Additional context came from trade associations like the American Association of Port Authorities and open customs data that show maritime cargo flows.

Company 10-Ks retrieved via D&B Hoovers, news archives on Dow Jones Factiva, and patent trends (Questel) helped us size private participation and emerging technologies (for example, advanced bridge materials). These examples illustrate our secondary inputs; numerous other public and subscription datasets were reviewed to cross-check figures and fill gaps.

Market-Sizing & Forecasting

A top-down model starts with federal and state capital outlays, which are adjusted for the share that flows to the four asset classes before being further filtered through historical payout schedules. We then corroborate these totals with bottom-up indicators, sampled highway lane-mile additions, rail track extensions, terminal gate counts, and sampled average construction cost indices to ensure internal consistency. Key variables feeding the model include IIJA annual authorizations, state fuel-tax receipts, passenger enplanements, port TEU throughput, and Bureau of Economic Analysis price deflators. Multivariate regression, confirmed by expert consensus, projects each driver to 2030 and produces the CAGR used in our forecast horizon. Where individual state data were missing, interpolation relied on nearby states' spending ratios that share similar population density and asset age profiles.

Data Validation & Update Cycle

Outputs pass three tiers of review: automated variance checks against historical ranges, peer review within the construction vertical, and a final sign-off by a senior analyst. Our team refreshes every report annually and re-contacts sources if federal appropriations, major contract awards, or material cost swings exceed preset thresholds.

Why Mordor's US Transportation Infrastructure Construction Baseline Earns Trust

Published estimates often diverge because firms mix spending, asset value, and operations in different ways and apply varying refresh cadences.

Key gap drivers include scope breadth, treatment of repair spending, and forecast discipline. Other publishers may roll maintenance and operational outlays into capital totals or count full life-cycle costs, which inflates the headline figure, whereas Mordor Intelligence focuses strictly on construction value put in place during the build or major rehabilitation phase.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 233.0 B (2025) | Mordor Intelligence | |

| USD 380.4 B (2024) | Regional Consultancy A | Blends minor maintenance and rolling stock purchases into construction totals |

| USD 214 B (2024) | Trade Journal B | Tracks contractor billings only, omits multiyear megaproject accruals |

| USD 1.89 T (2024) | Global Consultancy C | Counts entire life-cycle capex plus opex and includes telecom and energy corridors |

The comparison shows that when scope is tightened to construction activity, our 2025 baseline sits between narrower spend-flow tallies and vastly broadened capex plus opex views. According to Mordor Intelligence, this disciplined middle ground delivers a transparent, repeatable baseline that decision-makers can rely on for budgeting and strategy.

Key Questions Answered in the Report

What is the projected value of the US transportation infrastructure construction market by 2031?

The market is forecast to reach USD 298.12 billion by 2031, growing at 4.19% CAGR.

Which segment is growing fastest within the US transportation infrastructure construction market?

Railways are expected to expand at 5.18% CAGR from 2026 to 2031, the highest among all transportation modes.

How dominant is public funding in the US transportation infrastructure construction market?

Public sources accounted for 75.20% of investments in 2025, though private capital is advancing faster at 5.32% CAGR.

Why is Texas critical to nationwide infrastructure growth?

Texas holds 10.85% of 2025 spending and has committed USD 148 billion over ten years, targeting congestion relief and multimodal freight corridors.

What impact do skilled-labor shortages have on project delivery?

Persistent labor gaps are inflating wages and elongating schedules, prompting contractors to adopt automation and prefabrication to maintain productivity.

Page last updated on: