Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 47.39 Billion |

| Market Size (2026) | USD 49.34 Billion |

| Market Size (2031) | USD 60.35 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Hospitality Market Analysis by Mordor Intelligence

The Japan Hospitality market size is expected to grow from USD 47.39 billion in 2025 to USD 49.34 billion in 2026 and is forecast to reach USD 60.35 billion by 2031 at 4.12% CAGR over 2026-2031.

The growth momentum is driven by a mix of inbound demand, technology adoption, and supportive regulation[1]Japan Tourism Agency, “Inbound Tourism Statistics 2024,” mlit.go.jp. . Strong visitor inflows tied to a weaker yen, steady domestic leisure spending, and robust investment in regional tourism assets are strengthening top-line revenue streams for operators. Government stimulus programs that subsidize barrier-free retrofits, together with relaxed visa policies for priority source markets, underpin a medium-term surge in room demand that offsets lingering softness in domestic corporate travel. Operators are also deploying service robots, smart-check-in kiosks, and energy-saving systems to counter labor shortages and rising utilities, which improves operating margins even as wage levels move higher. New supply remains disciplined because construction-material inflation and seismic-retrofit costs raise development hurdles, so existing properties enjoy solid pricing power during the recovery phase.

Key Report Takeaways

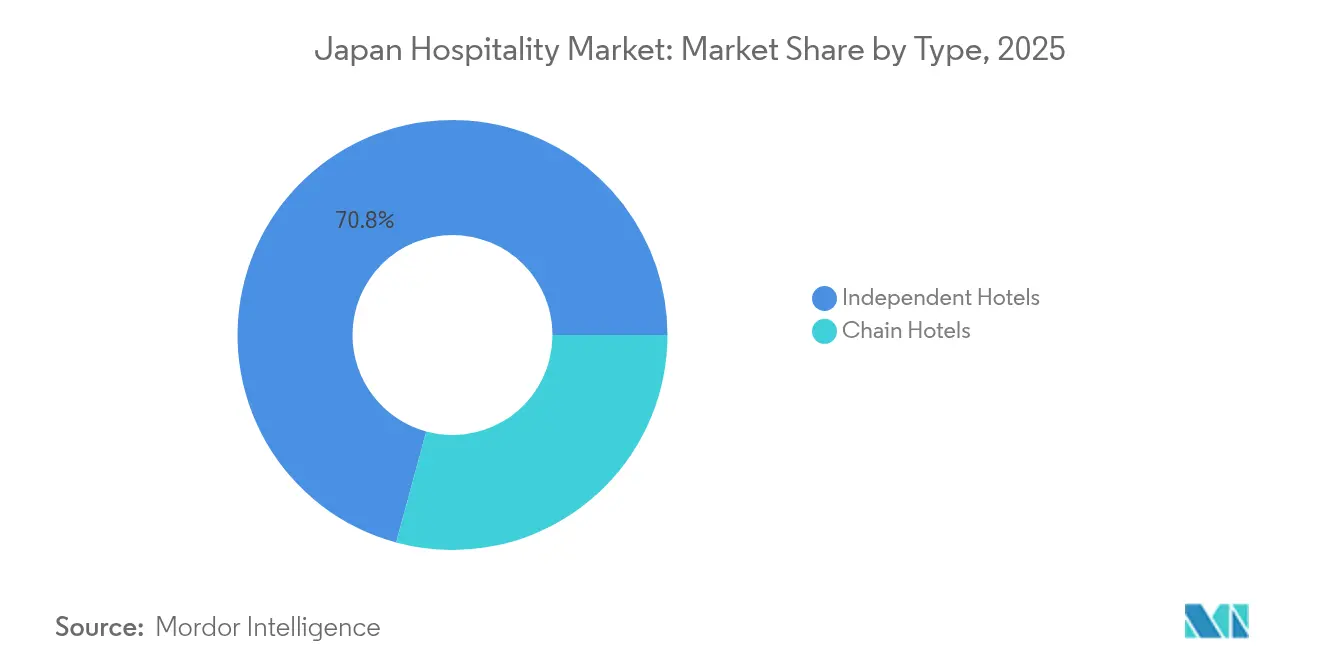

- By type, Independent Hotels led with 70.78% of the Japan hospitality market share in 2025 while Chain Hotels are projected to post a 6.11% CAGR through 2031.

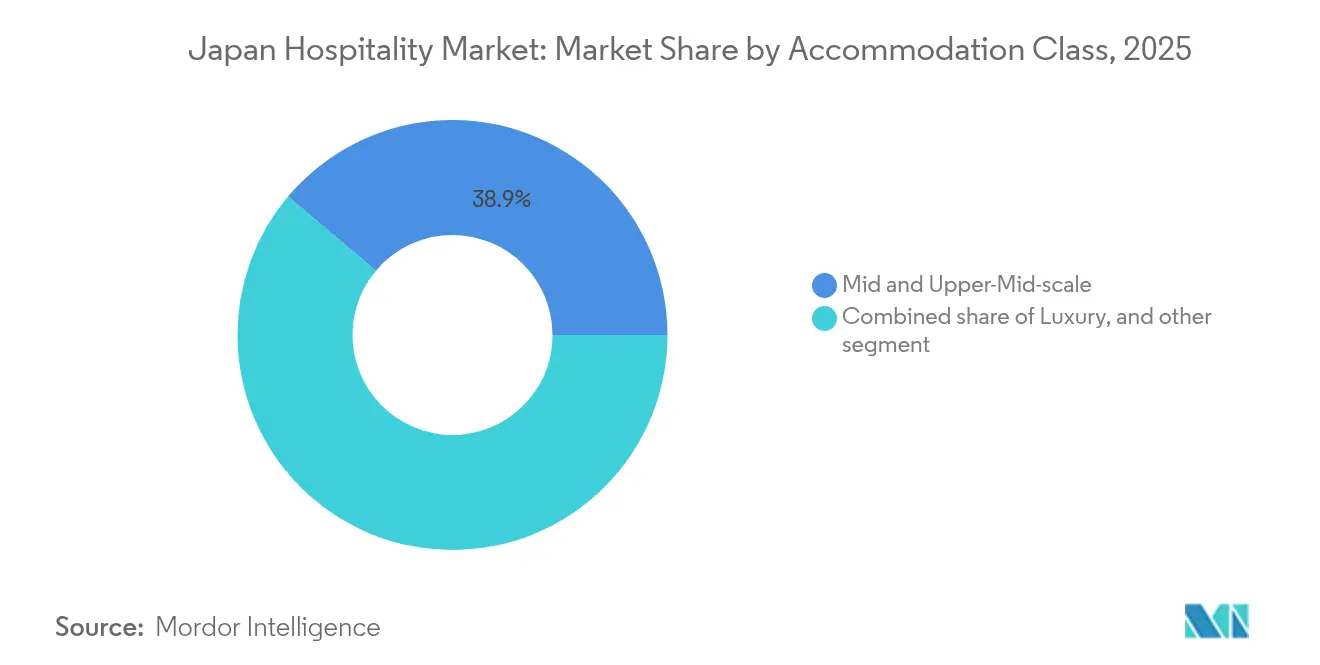

- By accommodation class, Mid & Upper-Mid-scale properties commanded 38.87% of the Japan hospitality market size in 2025; Service Apartments are forecast to grow at a 6.95% CAGR to 2031.

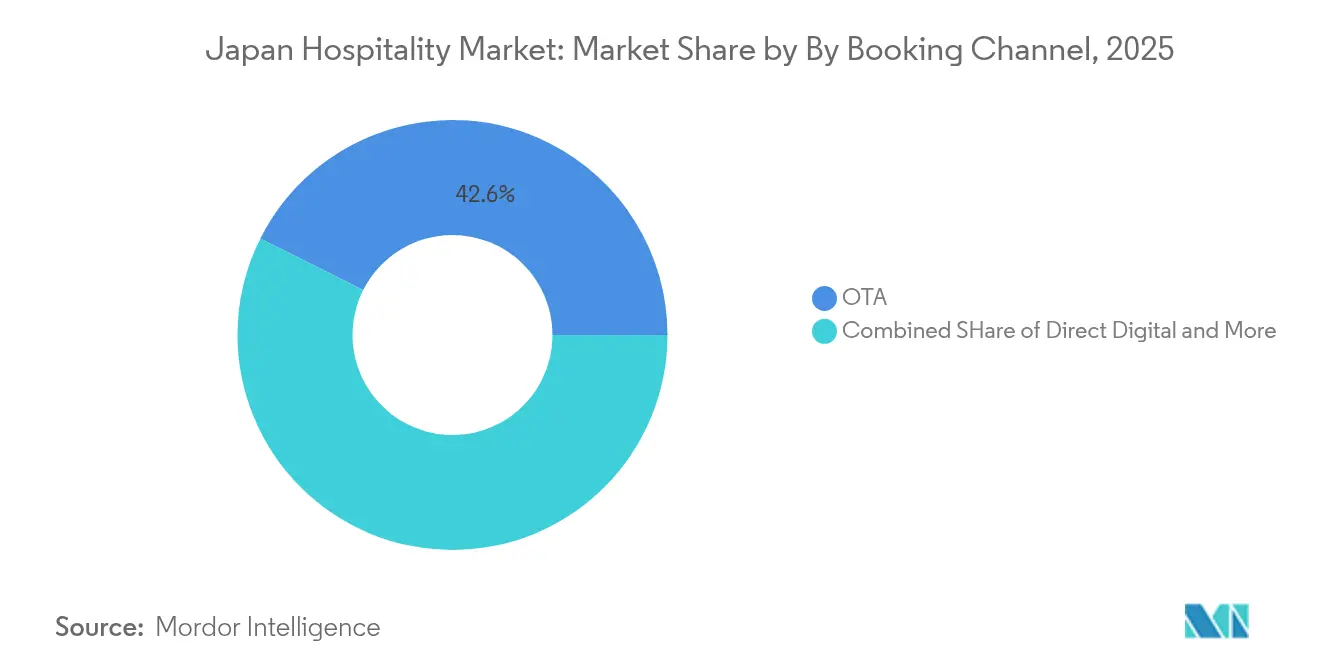

- By booking channel, OTAs controlled 42.59% of the Japan hospitality market size in 2025, whereas Direct Digital platforms are advancing at an 8.55% CAGR through 2031.

- By geography, Kanto accounted for 23.93% of the Japan hospitality industry share in 2025, while Kyushu & Okinawa are expanding at a 5.62% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic inbound tourism surge sustained by weaker Yen | +1.2% | National, with concentration in Tokyo, Osaka, Kyoto | Medium term (2-4 years) |

| Visa-free short-stay agreements expanding to ASEAN & GCC nations | +0.8% | National, with early gains in gateway cities | Long term (≥ 4 years) |

| Government subsidies accelerating hotel refurbishments for barrier-free access | +0.4% | National, with focus on Tokyo, Osaka metropolitan areas | Short term (≤ 2 years) |

| Deployment of service-robotics to curb chronic labour shortages | +0.6% | National, with priority in urban markets | Medium term (2-4 years) |

| 24/7 smart-check-in kiosks boosting ADR & ancillary spend | +0.3% | National, with concentration in business hotels | Short term (≤ 2 years) |

| Decentralised energy solutions lowering OPEX for remote resorts | +0.2% | Regional, focused on Hokkaido, Kyushu resort areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic inbound tourism surge

International arrivals rebounded to 36.87 million in 2024 and visitor spending climbed to JPY 8.14 trillion (USD 57.79 billion), reflecting the potent mix of pent-up demand and currency advantage that positions Japan as a value destination[2]World Travel & Tourism Council, “Japan Travel & Tourism Economic Impact 2024,” wttc.org. . Average length of stay rose to 11.5 days as travelers stretched budgets further under favorable exchange rates. Hotels in Tokyo achieved 91.22% occupancy with average daily rates of JPY 18,965 (USD 134.58), confirming that robust international demand is filling inventory that once relied on domestic corporate guests. The Japan National Tourism Organization is targeting 60 million annual visitors by 2030, a milestone now perceived as attainable given current traction. Dynamic pricing tools have allowed urban hotels to lift rates 60% above 2019 levels without eroding occupancy. Operators that focus on multilingual digital marketing and seamless contactless service are capturing the highest share of incremental spending.

Expansion of visa-free short-stay agreements

The government’s push to ease entry for Southeast Asian and GCC nationals opens large, fast-growing visitor pools, diversifying away from the traditional China–South Korea corridor. Multiple-entry visas for Chinese travelers and pilot e-visa programs for ASEAN nations have already reduced processing backlogs and encouraged repeat visits. These policy steps underpin a structural lift in room nights rather than a temporary spike. Airports in Fukuoka and Naha are tailoring facilities for new feeder routes, accelerating the regional dispersion of inbound traffic. Operators in secondary cities are responding by localizing menus, adding prayer rooms, and expanding foreign-language support. The sustained flow of new markets bolsters year-round occupancy and smooths seasonality that once defined leisure peaks.

Government subsidies for barrier-free retrofits

Tokyo Metropolitan Government covers up to 50% of accessibility upgrade costs, turning compliance into an economic incentive that accelerates property modernization[3]Tokyo Metropolitan Government, “Barrier-free Accommodation Subsidy Program,” sangyo-rodo1.metro.tokyo.lg.jp. . Osaka and several prefectures run similar grants for multilingual signage and digital room controls, allowing older assets to compete with new builds on inclusivity standards. Operators that complete upgrades report higher guest satisfaction and stronger group-tour bookings, particularly from senior and mobility-challenged segments. Accessibility certification is becoming a search filter on major OTAs, so compliant hotels gain superior listing visibility. The subsidy window favors rapid implementation, pushing many independents to undertake renovations earlier than planned. Long term, the barrier-free base lifts Japan’s appeal ahead of the 2030 inbound-visitor target.

Service-robotics deployment to ease labor gaps

Chronic staffing shortages persist as hospitality wages remain below national averages and the working-age population shrinks. Front-desk robots, delivery droids, and smart-check-in kiosks now operate in more than 20% of urban properties, reducing reception labor costs by up to 40%. Case studies at portfolio operators show payback periods under two years, even after accounting for maintenance contracts. Robots also extend service hours, which increases ancillary sales from late-night food and convenience offerings. Guest surveys indicate rising acceptance of automated interaction, especially among younger international travelers. The technology stack generates granular data on guest movement patterns that improve upsell algorithms and energy-management settings. Combined, these gains mitigate margin pressure from mandatory wage increases slated for the next fiscal cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-material inflation squeezing ROI on greenfield projects | -0.9% | National, with acute impact on Tokyo, Osaka development | Short term (≤ 2 years) |

| Shrinking domestic business-travel budgets amid hybrid-work adoption | -0.6% | National, with concentration in metropolitan business districts | Medium term (2-4 years) |

| Tight municipal zoning caps on short-term rentals in Osaka & Kyoto | -0.3% | Regional, focused on Kansai historical districts | Long term (≥ 4 years) |

| Aging building stock facing costly seismic retrofits | -0.4% | National, with priority in pre-1981 construction areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-material inflation

Steel and cement prices rose 30–40% between 2023 and 2025 as raw-material costs and new labor regulations pushed project budgets higher, eroding returns on greenfield hotel developments. Developers now require higher average daily rates or alternative financing to hit hurdle yields, delaying several pipeline projects in central Tokyo. Some investors pivot to conversion of existing office stock or mixed-use towers that spread cost across multiple income streams. Prefectural authorities have responded with limited infrastructure grants, but the gap between replacement cost and achievable room revenue keeps new supply muted. The supply constraint supports pricing for incumbent operators yet limits capacity in high-demand periods. Sustained inflation would lengthen development timelines and further concentrate capital toward premium assets.

Shrinking domestic business-travel budgets

Hybrid work arrangements cut meeting frequency, and corporations have tightened per-diem policies as accommodation rates climb. Business hotels that once filled mid-week now report occupancy dips while weekend leisure traffic surges. Operators are re-configuring room inventory to target couples and families, adding co-working lounges to capture remote workers, and bundling transit passes to attract regional tourists. Dynamic segmentation becomes critical because the corporate share fell to 35% of Tokyo hotel guests in 2024. While inbound leisure demand offsets lost corporate nights, it introduces more pronounced seasonality and currency sensitivity. Properties that diversify into long-stay programs and flexible subscription models hedge against permanent contraction in enterprise travel budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent hotels remain dominant but chains scale rapidly

Independent hotels accounted for 70.78% of the Japan hospitality market share in 2025, reflecting the country’s preference for locally run properties that showcase cultural authenticity. Chain hotels, however, are growing at a 6.11% CAGR, supported by standardized systems and strong loyalty programs that tackle labor shortages with centralized training and technology. Marriott opened its 100th Japanese property in 2024 and has 12 more projects slated, signaling confidence in brand power to attract international guests. Seibu Prince Hotels adopted a cloud reservation platform that strengthens distribution reach and data analytics, improving revenue management across its expanding estate. Independent operators are responding by joining soft-brand collections or investing in property-management systems that integrate with OTAs. Consolidation is expected as family-owned ryokans face succession challenges, creating acquisition opportunities for well-capitalized chains. Over time, the combined room count of top brands will increase even if independents hold numerical property advantage, subtly reshaping competitive intensity across major gateways.

The Japan hospitality market size for Chain Hotels is projected to climb steadily as investors favor scalable models with predictable returns. Franchising frameworks have eased entry for domestic real-estate players who supply land while global brands deliver booking engines and loyalty pipelines. Independent hotels must leverage unique location attributes, bespoke design and high-touch service to stay competitive. Some adopt automation selectively to protect warm service elements while trimming back-office tasks. Others collaborate with regional tourism boards to craft thematic itineraries that highlight local culture, thereby winning group bookings from niche operators. Market share movement will hinge on each segment’s ability to balance authenticity, efficiency and digital reach under tightening labor and cost conditions.

By Accommodation Class: Mid & Upper-Mid-scale holds the bulk while Service Apartments surge

Mid & Upper-Mid-scale properties commanded 38.87% of the Japan hospitality market size in 2025 by offering quality rooms at price points acceptable to both leisure and corporate travelers. The tier’s broad footprint across gateway cities makes it the go-to option for tour packages and loyalty redemption stays. Luxury developments remain active, such as Park Hyatt Sapporo opening in 2029, but their share growth is moderated by high land and construction costs. Budget and economy hotels face margin compression because rising wages offset lean staffing models, prompting some to pivot toward capsule formats or partner with coworking providers for blended revenue. Service Apartments, meanwhile, enjoy a 6.95% CAGR as they cater to digital nomads, relocation clients, and long-vacation guests seeking kitchenettes and extra space.

Japan's hospitality market share gains for Service Apartments stem from regulatory tweaks that clarify licensing under the Hotel and Ryokan Management Law, encouraging institutional capital to fund professionally managed projects. Brands streamline operations through cloud check-in and bundled housekeeping, improving profit per square meter. Mid-scale operators defend share by adding family rooms, contactless vending, and wellness amenities. Luxury hot-spring ryokan concepts such as the ATONA chain aim to blend traditional aesthetics with global service standards, illustrating the creative evolution of the upper tier. Overall, accommodation-class dynamics reward operators that can align guest experience with extended-stay and wellness trends while meeting rigorous environmental standards.

By Booking Channel: OTAs dominate but Direct Digital is rising fast

OTAs controlled 42.59% of bookings in 2025 thanks to large advertising budgets, deep user bases and comprehensive multilingual support that attracts first-time international visitors. Hotels, however, are investing in mobile apps, chatbot engagement, and member-only rates, spurring an 8.55% CAGR for Direct Digital channels. Japan hospitality market size for Direct Digital is thus expected to expand faster than any other channel segment, lowering distribution costs for proactive operators. Corporate and MICE channels face structural weakness as companies trim travel and replace small meetings with virtual sessions. Nonetheless, when meetings occur, hotels with integrated hybrid-event technology and flexible hall configurations capture residual demand. Wholesale and traditional agents still serve pilgrimage groups and educational tours, but continue to lose share as customized online itineraries proliferate.

Rate-parity clauses and loyalty tier perks entice repeat guests to book directly, improving data ownership and upsell potential. Seamless mobile check-in shortens wait times and allows staff redeployment to personalized services. OTAs remain critical for visibility in new markets yet charge commission of 15–20%, so most operators calibrate inventory quotas daily to optimize margin. Meta-search advertising and retargeting campaigns boost direct-channel traffic at manageable cost, though success hinges on continuous website upgrades and localized content. Properties that integrate channel analytics with revenue-management tools will extract the greatest value from the mixed distribution landscape.

Geography Analysis

Kanto held 23.93% of the Japan hospitality market share in 2025, driven by Tokyo’s role as the primary international gateway and corporate hub. The region benefits from year-round flight connectivity, diversified demand and world-class transport, yet land prices and zoning curbs inhibit rapid capacity expansion. Average daily rate growth remains supported by high occupancy, especially during citywide events, though policymakers are experimenting with crowd-dispersion incentives to reduce overtourism. Kansai follows as the cultural heartland with UNESCO sites, but strict caps on short-term rentals in Kyoto temper supply growth and push visitors toward Osaka and nearby prefectures. Hokkaido leverages dual-season appeal, attracting skiers in winter and outdoor enthusiasts in summer, which smooths revenue seasonality for resort operators.

Kyushu & Okinawa log the fastest 5.62% CAGR, aided by infrastructure upgrades, cruise-terminal expansions and the USD 1.12 billion Four Seasons resort scheduled for 2027. Visa-free travel from Taiwan and charter flights from Southeast Asia channel fresh leisure segments into these islands, supporting upscale and eco-resort pipelines. Chubu, Tohoku, Chugoku and Shikoku gain from government programs that promote regional tourism through grants, marketing campaigns and rail-pass discounts. Local authorities emphasize immersive cultural experiences, such as craft tours and agritourism, to differentiate from metropolitan circuits. Japan hospitality market size growth in these regions remains modest but steady, relying on infrastructure rollouts and digital way-finding tools that mitigate language barriers.

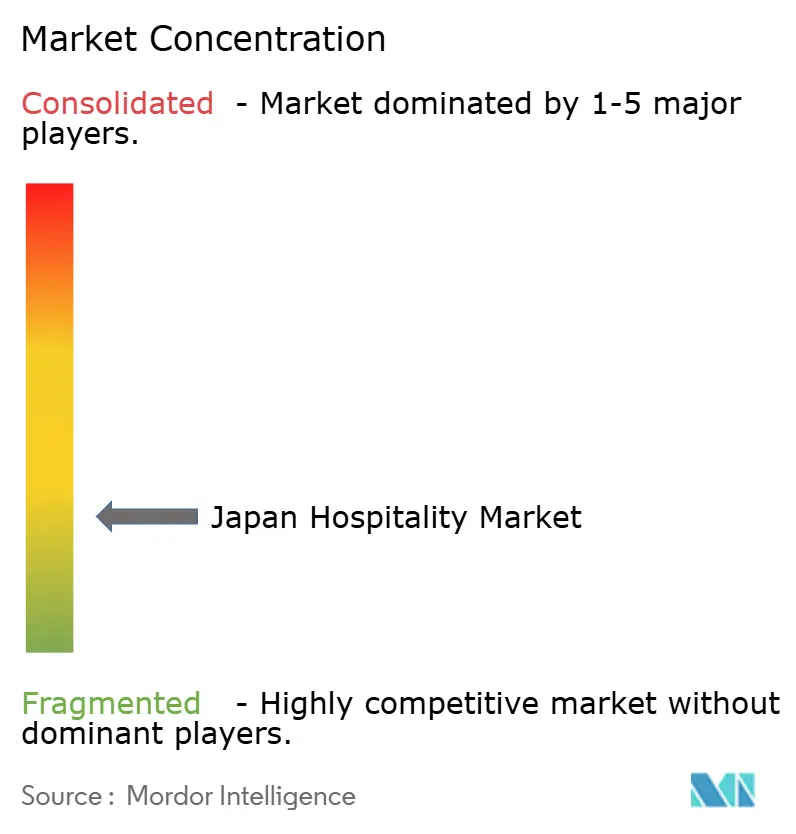

Competitive Landscape

Japan’s hospitality sector is highly fragmented, with the top five operators accounting for a relatively small portion of the total room supply. APA Hotel & Resort holds the leading position, while Toyoko Inn follows closely, maintaining its focus on the budget segment through uniform room designs and eco-friendly cleaning practices. Marriott, Hilton and IHG expand through management contracts, riding loyalty ecosystems to capture premium international travelers. Domestic groups such as Hoshino Resorts differentiate by embedding local culture and sustainability, which appeals to higher-spending guests seeking authentic experiences. Automation strategies give early adopters a cost edge; APA’s nationwide rollout of self-check-in kiosks cut front-desk staffing hours while maintaining guest-satisfaction scores above 85%.

Seibu Prince Hotels’ new cloud-based reservation engine integrates with Sabre SynXis to consolidate inventory and dynamic pricing in real time, helping the chain drive higher direct bookings and cross-brand loyalty redemptions. Fortress Investment Group doubled wages at select assets to stabilize labor, highlighting divergent strategies in a tight human-resource environment. Emerging disruptors include platforms that match traveling gig workers with short-staffed inns, broadening labor solutions beyond pure automation. International brands increasingly partner with domestic developers to navigate zoning and licensing, a model demonstrated by Park Hyatt Sapporo and Four Points Flex Osaka.

Service Apartments represent an acquisition target for real-estate investment trusts that value longer average stay and predictable occupancy. ESG imperatives accelerate retrofits: operators tap government green grants to install solar panels and low-flow fixtures that reduce utilities by up to 20%. Supply discipline stemming from high construction costs strengthens pricing across existing stock, while regional subsidies entice chains into underserved prefectures. Competitive intensity centers on digital distribution and personalized experience rather than raw room count, steering capital toward technology and training that deepen guest engagement and lifetime value.

Japan Hospitality Industry Leaders

APA Hotel & Resort

Prince Hotels, Inc.

Tokyu Hotels & Resorts Co., Ltd.

Fujita Kanko Inc.

Hotel Okura Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hyatt Hotels Corporation signed a management contract for the 157-key Park Hyatt Sapporo, with opening slated for 2029.

- February 2025: Pan Pacific Hotels Group, in partnership with Tokyu Hotels, opened The Hotel Higashiyama Kyoto Tokyu, featuring 143 rooms.

- November 2024: Marriott International unveiled its 100th Japanese hotel, Four Points Flex by Sheraton Osaka Umeda, and outlined 12 additional openings through early 2025.

- November 2024: Mitsui Fudosan announced Hotel The Mitsui Hakone, a 126-room luxury property scheduled for 2026.

- August 2024: Hyatt and Kiraku launched ATONA, a luxury hot-spring ryokan brand with initial funding of JPY 10 billion (USD 71 million).

Japan Hospitality Market Report Scope

The hospitality industry is a broad category of fields within the service industry, including lodging, food, drink service, event planning, theme parks, travel, and tourism. It includes hotels, tourism agencies, restaurants, and bars. The Hospitality Industry in Japan is Segmented by Type (Chain Hotels and Independent Hotels) and by Segment (Service Apartments, Budget and Economy Hotels, Mid and Upper Mid-scale Hotels, and Luxury Hotels). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Hokkaido |

| Tohoku |

| Kanto |

| Chubu |

| Kansai |

| Chugoku |

| Shikoku |

| Kyushu & Okinawa |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Hokkaido |

| Tohoku | |

| Kanto | |

| Chubu | |

| Kansai | |

| Chugoku | |

| Shikoku | |

| Kyushu & Okinawa |

Key Questions Answered in the Report

How large is the Japan hospitality market in 2026 and where is it projected by 2031?

The market is valued at USD 49.34 billion in 2026 and is forecast to reach USD 60.35 billion by 2031, reflecting a 4.12% CAGR during the period.

Which region currently contributes the most revenue?

Kanto region leads with 23.93% of national revenue due to Tokyo’s gateway status and high year-round demand.

What is the fastest-growing region?

Kyushu & Okinawa are expanding at a 5.62% CAGR, supported by infrastructure investments and relaxed visa policies.

Which accommodation class is growing the quickest?

Service Apartments top growth tables with a projected 6.95% CAGR as long-stay and digital-nomad demand rise.

How are hotels tackling the labor shortage?

Operators deploy service robots, automate check-in, and, in some cases, raise wages to secure staff while maintaining service standards.

What is the main factor restraining new hotel construction?

Construction-material inflation coupled with seismic-retrofit costs raises project budgets, making greenfield developments less attractive in the short term.

Page last updated on: