Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

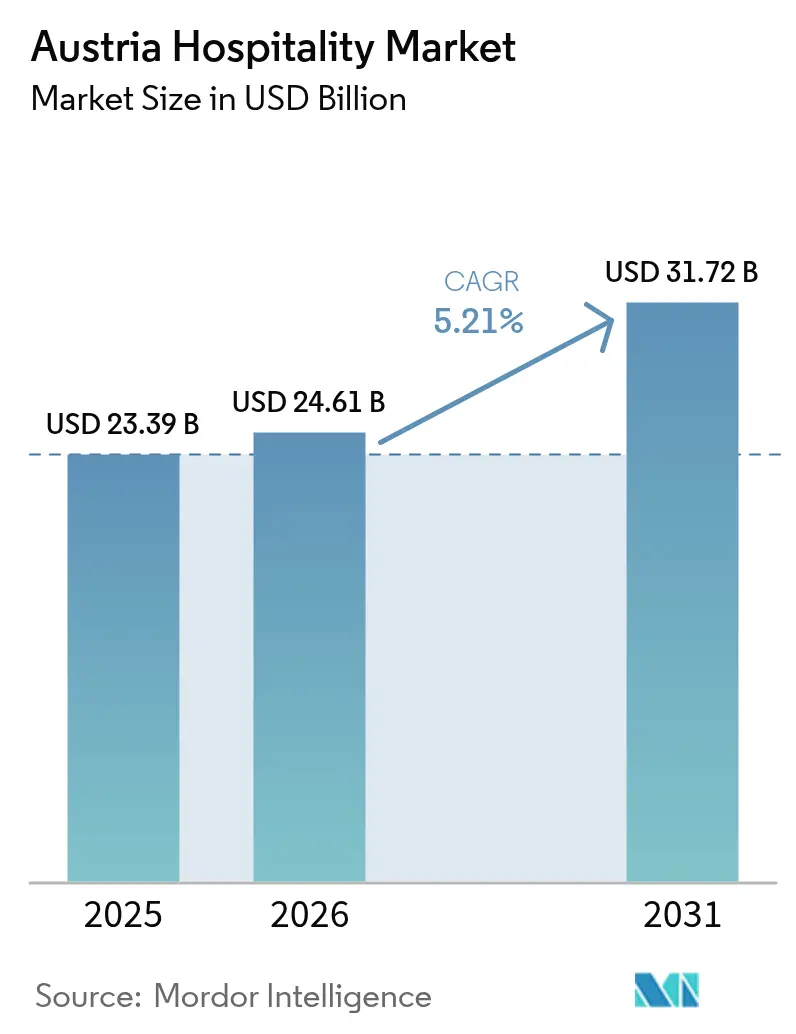

| Base Year Market Size (2025) | USD 23.39 Billion |

| Market Size (2026) | USD 24.61 Billion |

| Market Size (2031) | USD 31.72 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

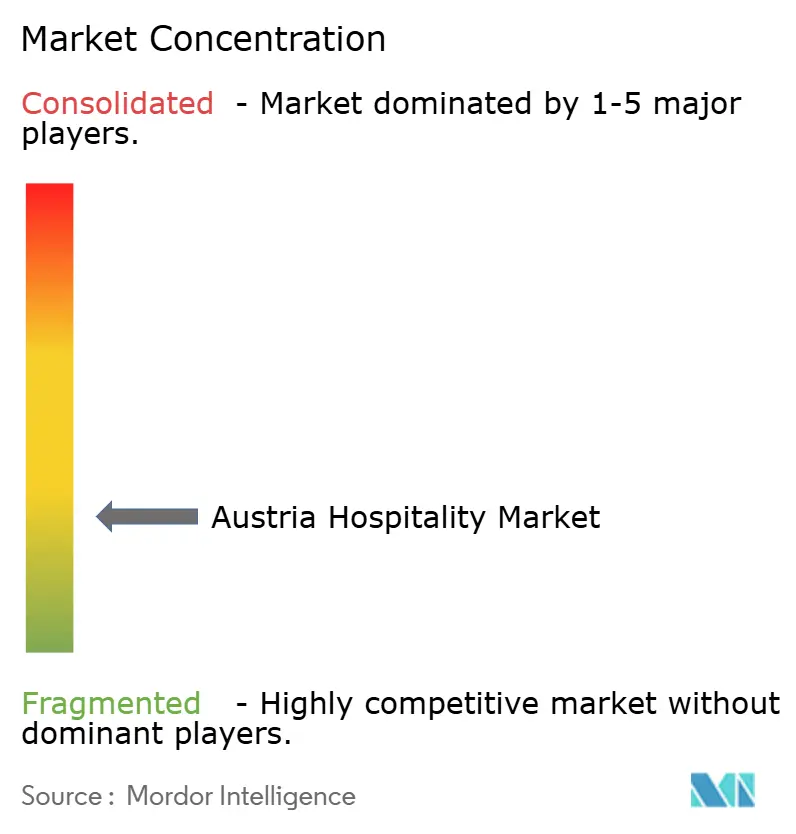

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Hospitality Market Analysis by Mordor Intelligence

The Austria Hospitality Market size is expected to grow from USD 23.39 billion in 2025 to USD 24.61 billion in 2026 and is forecast to reach USD 31.72 billion by 2031 at a 5.21% CAGR over 2026–2031. Vienna leads the ICCA global ranking for 2024 with 154 international congresses, driving consistent room demand. Streamlined eVisa protocols and expanded transatlantic and Asian connections increase long-haul visitors' stays by 1.7 nights and daily spending by 22%. Direct digital channels grow faster than intermediated bookings, enhancing margins for operators prioritizing loyalty and dynamic pricing. Labor shortages and rising sustainability compliance costs influence Austria's hospitality market, while regulatory measures on short-term rentals shift demand toward traditional lodging.

Key Report Takeaways

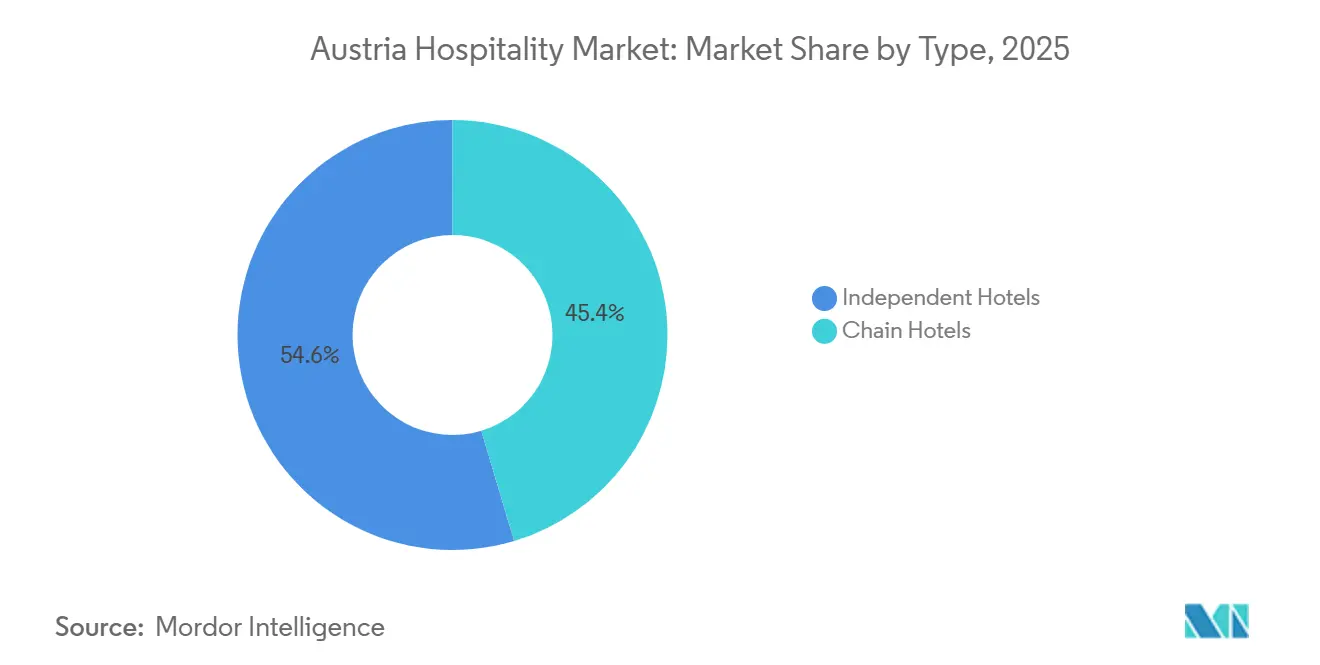

- By type, independent hotels led with 54.63% in the Austria Hospitality Market in 2025, while chain hotels are projected to expand at a 7.25% CAGR through 2031.

- By accommodation class, mid and upper-mid-scale held 43.78% in the Austria Hospitality Market in 2025, while luxury is forecast to record the fastest growth at a 7.45% CAGR to 2031.

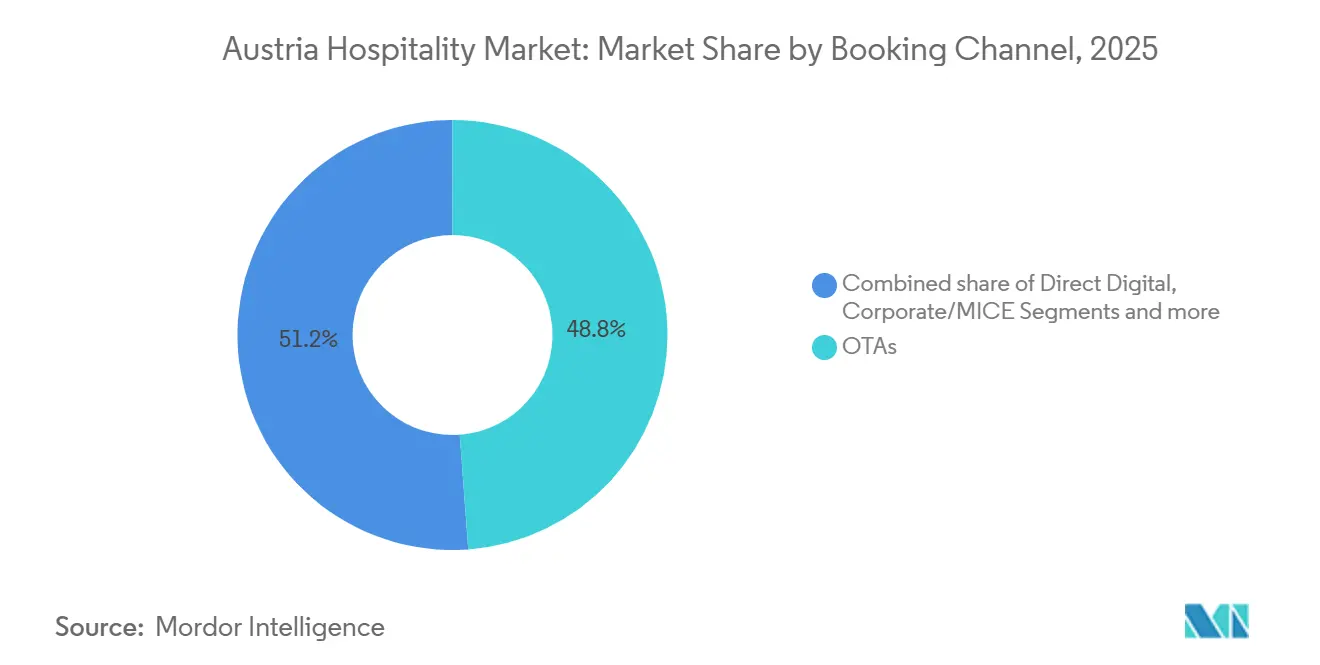

- By booking channel, OTAs accounted for 48.84% in the Austria Hospitality Market in 2025, while direct digital is set to grow at an 8.24% CAGR through 2031.

- By geography, Vienna contributed 30.12% in the Austria Hospitality Market in 2025, and Tyrol is projected to post the fastest regional expansion at a 5.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inbound tourism from the United States and Asia is surging, strengthening Austria’s hospitality demand | +1.2% | Vienna, Tyrol, Salzburg | Medium term (2-4 years) |

| Government-backed incentives are driving sustainable hotel renovation projects | +0.8% | Global | Long term (≥ 4 years) |

| Vienna’s expanding conference infrastructure is boosting the MICE segment | +1.0% | Vienna, spill-over to Lower Austria | Short term (≤ 2 years) |

| Domestic staycations are gaining traction, supporting local hospitality growth | +0.6% | Lower Austria, Upper Austria, Styria | Medium term (2-4 years) |

| Alpine wellness retreats are emerging as hubs for corporate resilience training | +0.7% | Tyrol, Salzburg, Upper Austria | Long term (≥ 4 years) |

| Rail-based night-train packages are stimulating tourism in Austria’s secondary cities | +0.5% | Asia-Pacific core, spill-over to Salzburg, Innsbruck, Graz | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inbound tourism from the United States and Asia is surging, strengthening Austria’s hospitality demand

Austria recorded 157.27 million overnight stays in 2025, a 1.9% increase from 2024, with a shift toward higher-spending long-haul guests. The United States' overnight stays rose 10% from January to May 2025, reaching 519,000, while Chinese travelers increased throughout the year, boosting demand during shoulder months. These visitors stay 1.7 nights longer and spend 22% more daily than regional guests due to improved air connectivity and simplified eVisa protocols. Their bookings in October and April help reduce seasonality without affecting peak-period gains during summer and Christmas markets. The hospitality market benefits as operators adjust mid-week and off-peak pricing to reflect higher spending by transatlantic and Asian travelers, particularly in Vienna and Tyrol[1]TravelMole, “Austria Tourism Appeal 2025,” TravelMole, travelmole.com.

Government-backed incentives are driving sustainable hotel renovation projects

Federal sustainability bonuses cover up to 14% of eligible eco-retrofit costs, while the Austrian Hotel and Tourism Bank offers loans from EUR 350,000 (USD 411,71) to EUR 5 million (USD 5.88 million) with 2% interest subsidies. This reduces upgrade costs. Properties with the Austrian Ecolabel report 6-8% higher ADR and 15-20% utility savings, improving cash flow during off-peak months. Early adopters align with the EU Buildings Directive, which requires zero-emission new buildings by 2030 and EPC C for older properties by 2032. Completing retrofits now secures subsidized financing, while delays may lead to higher costs as supply chains tighten. Sustainability credentials also influence corporate procurement and event selection in MICE programs, enhancing returns on green investments[2]USP.gv.at, “Tourism Investment Promotion by the Federal Government,” USP.gv.at, usp.gv.at.

Vienna’s expanding conference infrastructure is boosting the MICE segment

Vienna is investing EUR 230 million (USD 270.6 million) in the VIECON transformation of Messe Wien to increase overnight demand and strengthen its congress capabilities. Conference attendees spend EUR 550 (USD 646.97) daily, compared to EUR 170 (USD 199.97) by leisure tourists, boosting revenue and supporting higher mid-week hotel rates. In 2024, Vienna hosted 154 international congresses, 6,619 events, and generated 1,999,000 overnight stays, contributing EUR 1.32 billion (USD 1.55 billion) in value. This demand, less cyclical than leisure travel, fills mid-week hotel gaps without requiring discounts. Austria’s hospitality sector benefits as venues meet sustainability standards, now critical in multi-year congress bid evaluations.

Domestic staycations are gaining traction, supporting local hospitality growth

Domestic overnight stays are projected to reach 40.46 million in 2025, a 0.5% increase from 2024, supporting off-peak revenue stability outside main tourist corridors. Lower Austria experienced 4.3% growth in domestic guests during the 2024-2025 winter season, boosting regional properties focused on wellness and wine-based itineraries. Hotels offering thermal-spa access with vineyard tours or cycling routes extended stays to 2.8 nights, increasing total spending by 18% and improving margins without relying solely on rate adjustments. The Austrian hospitality market can expand personalized packages integrating local experiences and flexible check-in options, converting short weekend trips into longer stays. Direct digital engagement with nearby regions enhances these efforts, encouraging repeat visits and sustained growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages combined with wage inflation are pressuring Austria’s hospitality sector | -0.9% | Global | Short term (≤ 2 years) |

| Stricter energy-efficiency renovation requirements are raising compliance costs for hotels | -0.6% | European Union-wide, concentrated in legacy city hotels | Long term (≥ 4 years) |

| Uncertainty around short-term rental regulations is creating market instability | -0.4% | Vienna, Salzburg | Short term (≤ 2 years) |

| Over-tourism concerns in Salzburg are fueling local backlash and regulatory scrutiny | -0.3% | Salzburg Old Town | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor shortages combined with wage inflation are pressuring Austria’s hospitality sector

A tight labor supply in Austria's accommodation and food-service sectors increased wage costs in 2024, with 90.7% of employers struggling to fill positions in 2025. Elevated vacancy rates led operators to test automation in front-of-house and housekeeping roles to maintain service standards. Cooking remained the hardest profession to staff, with 133 companies unable to recruit, affecting independent kitchens and chain hotels. Austria's Talent Accord aims to hire 15,000 non-European Union workers by 2027, but visa and housing delays prolong hybrid staffing models. The hospitality market is piloting four-day work rosters and self-service options for basic requests, reducing turnover and enabling staff to focus on higher-value guest interactions[3]The International, “Austria Faces Staff Shortages in Hospitality Sector,” The International, theinternational.at.

Stricter energy-efficiency renovation requirements are raising compliance costs for hotels

The EU Buildings Directive requires new buildings to achieve zero emissions by 2030 and older assets to meet EPC C standards by 2032, increasing capital needs for hotels. Renovating a 120-room legacy property costs EUR 0.7-1.2 million (USD 0.8-1.4 million). Subsidies for stand-alone fossil-fuel boilers ended on January 1, 2025. Early adopters can access federal sustainability bonuses covering up to 14% of capital expenditures, reducing payback periods for HVAC and insulation upgrades. In Austria, renovation waves are expected to align with funding windows and contractor availability, potentially accelerating timelines before 2030-2032 deadlines. Scheduling renovations during off-peak months helps operators maintain occupancy and pricing during peak periods[4]Ecochain, “Energy Performance of Buildings Directive,” Ecochain, ecochain.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Conversion Wave Reshapes Ownership Landscape

Chain hotels are expected to grow at a 7.25% CAGR from 2026 to 2031. Independent hotels held 54.63% of Austria's hospitality market share in 2025. Brand-affiliation strategies have grown through conversions and soft-brand deals, offering distribution and loyalty benefits without full corporate control changes. IHG acquired Ruby Hotels for EUR 110.5 million (USD 130.0 million), establishing a lean-luxury brand in Vienna, with integration into its reservation system planned for 2026. Marriott’s partnership with VERKEHRSBUERO added over 1,100 rooms under Four Points Flex by Sheraton and Tribute Portfolio, streamlining global sales support for legacy assets. Independent operators attract repeat domestic guests valuing personalized service, but face higher compliance and technology costs per property. Owner-operators in Austria weigh franchise fees against direct demand and brand-level revenue management.

Chain hotels manage GDPR and reporting obligations through centralized teams, while independents rely on external advisors. Strong first-party programs reduce commission outflows by 4 to 7 percentage points, improving property-level margins through direct digital reservations and loyalty initiatives. Conversions with minimal downtime preserve cash flows and lower construction risks in cities with strict zoning rules. Asset-light partnerships enable faster adjustments to changing guest preferences in Austria's hospitality market.

By Accommodation Class: Luxury Surge Reflects Wealth Migration and Ultra-Premium Positioning

Luxury properties are expected to grow at a 7.45% CAGR through 2031. Mid and upper-mid-scale hotels accounted for 43.78% of the Austria hospitality market's value in 2025. The Mandarin Oriental Vienna, featuring 138 rooms and 52 suites, enhanced the ultra-luxury segment in the capital. Asset transactions, such as the Ritz-Carlton Vienna's acquisition by a Middle Eastern investor, reflect confidence in sustained demand. Mid and upper-mid-scale hotels address corporate and leisure demand, while budget properties face wage pressures that reduce margins at lower ADRs. Service apartments support extended stays for relocating executives and production crews, driving demand beyond peak seasons without extensive amenities.

Falkensteiner is investing EUR 40 million (USD 47.1 million) to transform Alpine Palace into a 127-room luxury resort, focusing on wellness and corporate retreat needs. Sustainability certifications enable higher ADRs and attract high-spending guests, while energy-efficient systems help manage rising utility costs. The Austria hospitality market is shifting toward quality in upper tiers, with curated experiences replacing room-only offerings. Mid-scale properties benefit when corporate travel budgets push guests to lower tiers. Budget and economy operators are reassessing formats and labor models to maintain profitability as wages rise faster than room rates.

By Booking Channel: Direct Digital Gains Challenge OTA Dominance Through AI and Loyalty Engineering

OTAs accounted for 48.84% of bookings in 2025. Direct digital reservations, supported by loyalty platforms and integrated apps, are projected to grow at an 8.24% CAGR through 2031. Expanding direct channels allows hotels to reclaim 4 to 7 percentage points of commission margins and use CRM data to create targeted offers, increasing repeat stays. Austria's hospitality market is adopting AI chatbots for pre-arrival and in-stay support, reducing service friction and enabling lean teams to handle higher volumes. Revenue-management systems are being deployed for precise pricing and package designs that include transport or wellness access, boosting ADRs. Corporate and MICE bookings remain relationship-driven, favoring properties with dedicated sales teams and loyalty programs.

Traditional agents and wholesalers retain importance in specific source markets where group itineraries and language support are critical. Independent hotels face higher fixed costs to develop GDPR-compliant data platforms, while global chains spread these investments across larger portfolios. As direct booking tools improve, metasearch and brand.com pages are converting more visitors into buyers, reducing reliance on commission-sensitive third-party platforms. OTA visibility remains vital for acquiring new customers, but retention is shifting to brand ecosystems that reward repeat stays and referrals. Channel-mix optimization is expected to continue as operators balance scale benefits with commission and data considerations.

Geography Analysis

Austria recorded 157.27 million overnight stays in 2025, a 1.9% increase from 2024, with stable growth across key provinces. Vienna accounted for 30.12% of Austria's hospitality market share with 20.09 million overnight stays, supported by international meetings and exhibitions. In 2024, the city hosted 6,619 events, generating 1,999,000 overnight stays, and expanded capacity to 81,800 beds to accommodate larger conferences and seasonal demand. Tyrol reported 50.02 million overnight stays in 2025, maintaining its position in alpine leisure while diversifying into wellness for summer months. Salzburg recorded 30.90 million overnight stays in 2025, driven by cultural and event-related demand.

Tyrol is projected to grow at a 5.32% CAGR through 2031, supported by wellness retreats and improved long-haul access, increasing average spending. The United States overnight stays rose 10% in the first five months of 2025, while China showed positive momentum, extending booking windows and stabilizing mid-week occupancy. Vienna’s occupancy averaged 70.8% in 2025, aided by expanded venue capacity and bed availability for concurrent events. Lower and Upper Austria attracted domestic travelers with accessible locations and bundled spa or wine experiences, spreading demand beyond Vienna. Regional market growth is supported by infrastructure, diverse offerings, and evolving traveler preferences.

Policy and supply changes also influenced regional performance. Vienna’s 90-day cap on short-term rentals outside residential zones reduced alternative supply, redirecting leisure demand to hotels. Private holiday dwelling overnight stays in Vienna dropped 13.9% between May and September 2024, raising hotel occupancy in core districts. Carinthia saw a 0.7% decline in 2025 overnight stays, while Lower Austria eased 0.4%, reflecting aging assets and product gaps being addressed in new plans. Regional investments in wellness, culture, and rail connectivity are expected to drive multi-stop itineraries anchored by Vienna’s congress appeal.

Competitive Landscape

The Austria hospitality market is moderately concentrated, with many independent operators and increasing conversions to global brand systems. Chain groups favor asset-light growth, adding managed and franchised rooms through soft-brand frameworks that maintain owner autonomy. Marriott’s partnership with VERKEHRSBUERO converted over 1,100 rooms into Four Points Flex by Sheraton and Tribute Portfolio, expanding its presence in key cities. IHG acquired Ruby Hotels for EUR 110.5 million (USD 130.0 million), enhancing lean-luxury offerings in Vienna and integrating the brand into a global distribution network. Family-owned groups, such as Falkensteiner, focus on wellness and experience differentiation through targeted investments. Investor interest in Vienna remains strong, as seen in the Vienna Marriott Hotel's sale to an international consortium.

Technology and channel strategies are critical for competitive advantage. Strengthening loyalty programs and app-based services increases contribution margins by 4 to 7 percentage points. Revenue-management platforms enable dynamic pricing and bundled offers, such as combining rooms with rail access or wellness amenities, boosting average daily rates (ADR). AI chatbots and self-service tools reduce front-desk staffing pressures and allow employees to focus on guest satisfaction. The Austrian Ecolabel supports ADR growth and influences procurement for MICE events. Operators aligning sustainability with guest experience and digital convenience achieve higher repeat rates and referrals.

Human capital challenges persist. In 2025, 90.7% of employers reported hiring difficulties, with cooks being the hardest to recruit. New scheduling models and expanded training aim to reduce attrition. Hilton’s recognition as Austria’s No. 1 Best Workplace in 2024 highlights the importance of employer practices in recruitment. Companies integrating retention strategies, technology, and flexible staffing improve productivity amid wage pressures and renovation needs. Conversions and selective asset sales reflect confidence in Vienna’s MICE capabilities and growing accommodation capacity, supporting larger events without rate dilution.

Austria Hospitality Industry Leaders

Austria Trend Hotels

ARCOTEL Hotels

Falkensteiner Hotels & Residences

Accor (Ibis, Mercure, Novotel)

Marriott International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Accor rebranded the 102-room Hotel Rathauspark Wien, previously part of Radisson, into its Handwritten Collection. Located near Vienna City Hall, the 4-star hotel features a 24-hour lobby bar, fitness center, and Austrian Ecolabel certification. This partnership with Verkehrsbuero Hospitality strengthens Accor's presence in the DACH market, focusing on mid-scale, independent hotels with unique identities.

- January 2026: The Austrian government adopted "Vision T," a tourism strategy allocating EUR 1 million (USD 1.2 million) for Milan/Cortina Winter Olympics marketing and simplifying licensing for hospitality ventures. It includes "talent visas" for seasonal workers and aligns with the EUR 1.8 billion (EUR 2.1 billion) Sanierungsoffensive 2026 program (EUR 360 million (USD 423.5 million) annually, 2026-2030) for energy-efficient hotel renovations, addressing labor shortages and rising costs.

- December 2025: Mandarin Oriental opened its first Austrian property, a 138-room luxury hotel (86 rooms, 52 suites) in a restored 1908 Art Nouveau courthouse in Vienna's First District. The 5-star hotel includes four dining venues led by Chef Thomas Seifried, a spa with seven treatment rooms, an indoor pool, and a 140-sqm ballroom.

- November 2025: Motel One expanded its presence in Vienna by opening the 198-room Vienna-Donau City. This addition strengthens its standardized, technology-driven model designed for urban environments.

Austria Hospitality Market Report Scope

The Austria Hospitality Market report analyzes the hotel and accommodation sector, covering demand trends, supply dynamics, and regional performance. It segments the market by type, accommodation class, booking channels, and geography (Vienna, Lower Austria, Upper Austria, Salzburg, Tyrol, and others). Key drivers include increased inbound tourism from the United States and Asia, government incentives for sustainable renovations, Vienna’s expanding conference infrastructure, domestic staycations, alpine wellness retreats, and rail-based night-train packages. Challenges include labor shortages, wage inflation, stricter energy-efficiency standards, regulatory uncertainty, and over-tourism in Salzburg. The report uses Porter’s Five Forces to assess regulations, technology, supply chains, and competition. It provides market size, forecasts, company profiles, and market share analysis for players like Austria Trend Hotels, ARCOTEL Hotels, and others. The report provides market size and forecasts for the Austria Hospitality Market, in value (USD), across all segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geography

| Vienna |

| Lower Austria |

| Upper Austria |

| Salzburg |

| Tyrol |

| Rest of Austria |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geography | Vienna |

| Lower Austria | |

| Upper Austria | |

| Salzburg | |

| Tyrol | |

| Rest of Austria |

Key Questions Answered in the Report

What is the current size and growth outlook for the Austria hospitality market?

The Austria hospitality market size is USD 23.39 billion in 2025 and is projected to reach USD 31.72 billion by 2031 at a 5.21% CAGR, reflecting resilient demand across city and alpine destinations.

Which accommodation types are growing fastest in Austria’s hospitality sector?

Chain hotels are set to expand at a 7.25% CAGR from 2026 to 2031, while independent hotels remain important with a 54.63% base in 2025 that anchors regional diversity.

How is Vienna influencing national performance in the Austria hospitality market?

Vienna contributed 30.12% of value in 2025, hosted 6,619 meetings in 2024, and continues to drive mid week demand with top ranked international congress activity.

What booking channels will gain share in Austria over the forecast period?

Direct digital reservations are forecast to grow at 8.24% CAGR through 2031 as hotels invest in loyalty platforms and revenue management to reduce commission outflows.

Which regions in Austria are poised for the fastest growth through 2031?

Tyrol is projected to lead with a 5.32% CAGR, supported by wellness oriented product development and stronger inbound flows that extend beyond ski season.

What policy and compliance themes matter most for operators in Austria?

Energy efficiency mandates under the European Union Buildings Directive and local short term rental rules shape capital plans and supply dynamics, while labor shortages continue to raise operating complexity.

Page last updated on: