North America IT Asset Disposition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

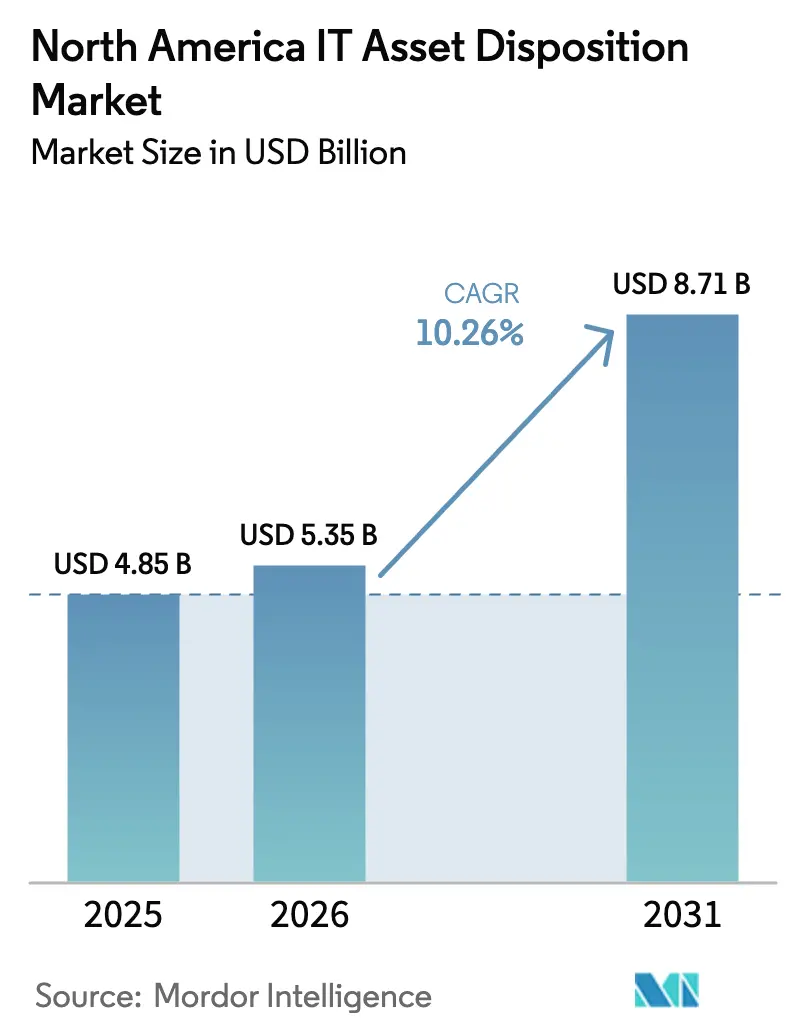

| Base Year Market Size (2025) | USD 4.85 Billion |

| Market Size (2026) | USD 5.35 Billion |

| Market Size (2031) | USD 8.71 Billion |

| Growth Rate (2026 - 2031) | 10.26% CAGR |

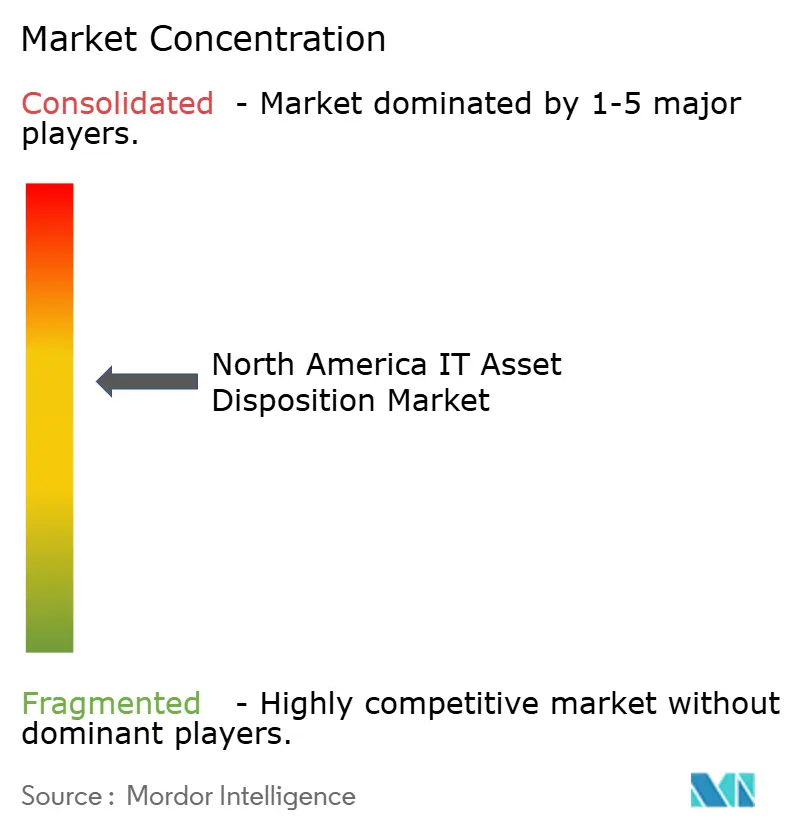

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America IT Asset Disposition Market Analysis by Mordor Intelligence

The North America IT asset disposition market size is expected to grow from USD 4.85 billion in 2025 to USD 5.35 billion in 2026 and is forecast to reach USD 8.71 billion by 2031 at 10.26% CAGR over 2026-2031. Growth reflects the intersection of expanding digital transformation initiatives, stricter e-waste regulation, and corporate moves toward circular-economy models. Enterprises confront higher data-breach liabilities, prompting wider adoption of certified data destruction, while original equipment manufacturers (OEMs) embed “take-back” schemes that recapture residual value and reduce environmental impact. Broader ESG mandates, favorable financing linked to sustainability metrics, and accelerated hardware refresh cycles in hyperscale data centers further widen the addressable base for full-service ITAD providers. However, fragmented reverse-logistics networks and volatile secondary-market pricing for refurbished devices temper the overall growth outlook.

Key Report Takeaways

- By service type, data destruction and sanitization led with 38.20% of the North America IT asset disposition market share in 2025, whereas remarketing and value recovery is projected to expand at a 15.02% CAGR to 2031.

- By end-user enterprise size, small and medium enterprises accounted for 63.90% share of the North America IT asset disposition market size in 2025 and are advancing at an 11.74% CAGR through 2031.

- By asset type, computers and laptops accounted for a 42.60% revenue share in 2025; smartphones and tablets represented the fastest-growing class, growing at 14.13% CAGR.

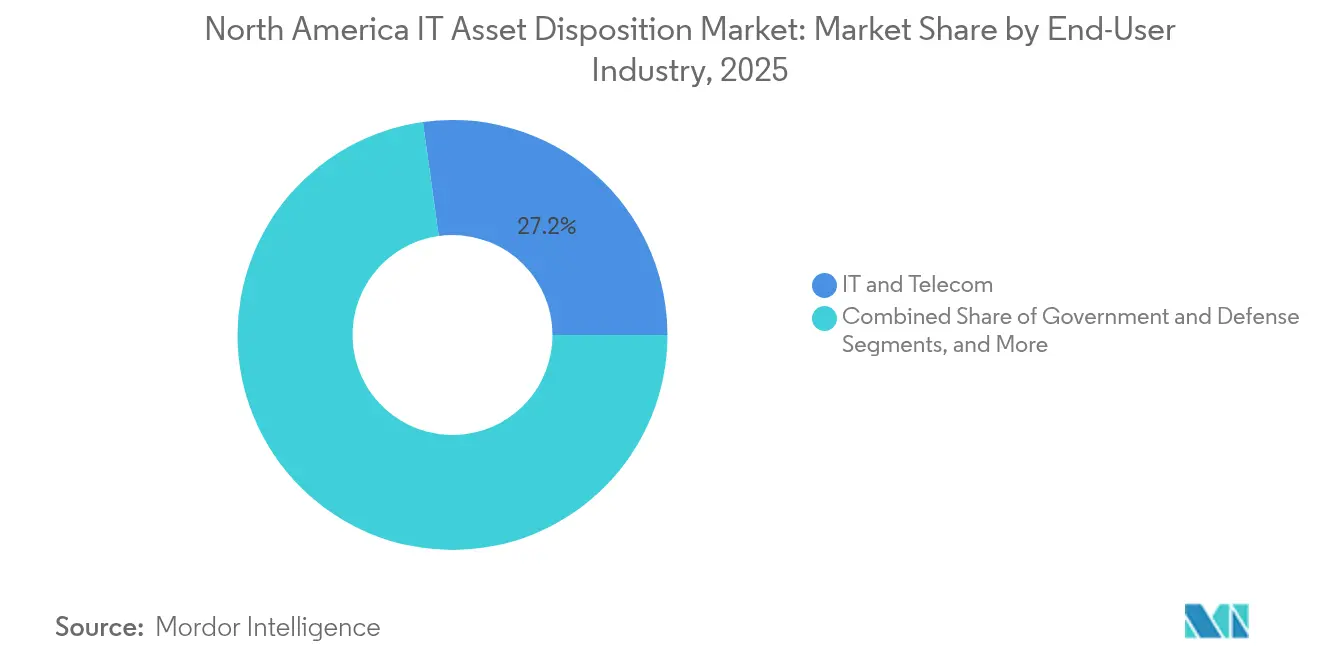

- By end-user industry, healthcare and life sciences are set to grow at 12.61% CAGR, while IT and telecom retained leadership with 27.20% revenue share in 2025.

- By country, the United States held 84.10% share in 2025; Canada is forecast to register the highest regional CAGR of 11.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America IT Asset Disposition Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening state and federal e-waste legislation | +2.8% | United States, Canada | Medium term (2-4 years) |

| Rising corporate liability for data breaches | +2.1% | North America | Short term (≤ 2 years) |

| OEM “take-back” circular-economy programs | +1.9% | United States, Canada | Long term (≥ 4 years) |

| Edge-to-cloud refresh cycles in hyperscale data centers | +1.7% | United States | Medium term (2-4 years) |

| ESG-linked financing lowering cost of capital for ITAD leaders | +1.2% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening State and Federal E-Waste Legislation

Regulatory enforcement intensifies as more jurisdictions broaden e-waste coverage and impose steeper penalties on non-compliant businesses. Arizona’s 2025 framework obliges companies to prove responsible disposal of all electronic assets, while California augments audit powers and fines for violations. The Basel Amendment now curtails cross-border e-waste transfers, compelling firms to develop local processing capacity and bolstering domestic demand for certified ITAD partners. Varying state laws make nationwide compliance complex, so multi-location enterprises enlist providers with unified programs that guarantee consistent data security and environmental stewardship. Extended producer responsibility provisions further transfer disposal costs from municipalities to OEMs, indirectly stimulating enterprise adoption of third-party ITAD services.

Rising Corporate Liability for Data Breaches

Expanding privacy statutes elevate financial exposure when sensitive data is mishandled during asset retirement. The Gramm–Leach–Bliley Act, the FTC Disposal Rule, and HIPAA collectively require the secure destruction of consumer and patient records. Healthcare organizations retiring more than 14 million electronic devices each year now face penalties that can reach multimillion-dollar levels per incident if erasure is incomplete. Because certified data destruction costs represent only a fraction of potential fines, boards of directors increasingly mandate partnerships with auditors who can issue chain-of-custody documentation for every retired unit.[1]Ingram Micro Lifecycle, “Marketplace Price Index for Refurbished IT Equipment,” ingrammicroservices.com

OEM “Take-Back” Circular-Economy Programs

OEMs move from product-centric to lifecycle-centric business models. Dell aims to recover electronics equivalent in weight to its annual product output by 2030 and has already processed 2.5 billion lb since 2007. HP’s Planet Partners adds refurbishment and resale, letting enterprise customers procure and retire assets within a single contract that supports carbon-reduction targets. These integrated offerings relieve smaller firms of upfront logistics planning while enabling OEMs to reclaim valuable materials for new production, thereby lowering virgin-material inputs and aligning with sustainability pledges.

Edge-to-Cloud Refresh Cycles in Hyperscale Data Centers

AI-optimized architectures are shortening refresh intervals from three-to-five years to 18–24 months, producing larger volumes of still-valuable servers, switches, and transceivers. Data-center capital outlays topping USD 20 billion in 2025 translate into rising demand for ITAD specialists capable of decommissioning high-density racks without service disruption. Secondary-market buyers of such hardware gain access to premium equipment that retains high residual value, reinforcing the financial case for remarketing over scrap.[2]4THBIN, “HIPAA Compliance and the High Cost of Data Breaches,” 4thbin.com

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented reverse-logistics infrastructure | -1.8% | North America | Medium term (2-4 years) |

| Residual-value volatility for refurbished hardware | -1.4% | North America | Short term (≤ 2 years) |

| Low ITAD awareness among more than 100-employee firms | -1.1% | United States, Mexico | Medium term (2-4 years) |

| Uncertain downstream recycling capacity for lithium-ion batteries | -0.9% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Reverse-Logistics Infrastructure

Reverse logistics lacks the scale and uniform standards present in forward supply chains. Many rural districts incur high collection costs because low asset density cannot justify dedicated routes. National providers rely on a patchwork of local partners that operate with uneven quality, leading to visibility gaps and inconsistent service levels. Inefficiencies elevate per-asset pricing, particularly for SMEs, and slow market penetration outside major metropolitan areas.

Residual-Value Volatility for Refurbished Hardware

Secondary-market prices swing with rapid technological change, oversupply, and commodity pricing for precious metals. Cloud adoption curbs demand for on-premise servers, while AI hardware upgrades depreciate mainstream architectures more quickly. Providers therefore adopt conservative valuation models, which reduce the trade-in credits they can extend to customers and may dampen uptake among price-sensitive enterprises.[3]CommScope, “Preparing the Network for 1.6T Optics,” commscope.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Type: Mobile Devices Drive Refresh Acceleration

Computers and Laptops held 42.60% of the North America IT Asset Disposition market share in 2025 as hybrid work required consistent refreshes to secure distributed endpoints. Smartphones and Tablets are predicted to expand at a 14.13% CAGR because enterprise mobility programs shorten replacement cycles for security and productivity gains. Servers benefit from hyperscale investments, while Storage Devices ride the shift to high-capacity SSD arrays. Peripherals face shrinking demand amid paperless workflows, although specialized medical and industrial peripherals retain steady disposal volumes.

Enterprises increasingly prioritize mobility-first strategies, retiring traditional desktops in favor of lightweight laptops and tablets that support remote collaboration. University trade-in schemes illustrate this shift, reporting rising mobile-device volumes as students and faculty adopt AI-ready hardware. Meanwhile, data-center operators schedule coordinated decommissions to extract maximum residual values from server and networking units, reinforcing the financial appeal of remarketing programs.

By Service Type: Value Recovery Transforms Industry Economics

Data Destruction and Sanitization dominated 2025 revenue with 38.20%, reflecting firm regulatory oversight of data privacy. Nevertheless, Remarketing and Value Recovery is slated for the highest growth at 15.02% CAGR, underscoring a pivot toward monetizing residual asset value over pure disposal. De-Manufacturing and Recycling gains from stricter e-waste laws, and Logistics Management services become critical for multi-site enterprises needing transparent, cradle-to-grave oversight.

The North America IT Asset Disposition market size linked to remarketing is projected to expand steadily as IEEE 2883-2022 introduces updated wiping standards for emerging storage media. Enterprises view recovered value as a practical hedge against higher new-equipment costs, pressing ITAD providers to refine price-prediction models that manage volatility yet keep client payouts attractive.

By End-User Industry: Healthcare Accelerates Digital Transformation

IT and Telecom retained leadership with 27.20% revenue share in 2025, driven by constant network upgrades and cloud migrations. Healthcare and Life Sciences is forecast to record a 12.61% CAGR as hospitals digitize patient care and meet HIPAA’s strict destruction mandates. Financial institutions remain steady consumers of certified data destruction under Gramm–Leach–Bliley and Sarbanes–Oxley rules, while Government and Defense seek partners with security clearances and specialty protocols.

Healthcare facilities discard medical-grade devices that contain sensitive records and complex materials. As they retire 14 million units annually, specialized handlers assure both data sanitation and compliance with environmental rules. Education and Energy sectors add niche demand segments requiring tailored value-recovery or hazardous-material capabilities, widening the total addressable North America IT Asset Disposition market.

By End-User Enterprise Size: SMEs Drive Market Expansion

SMEs captured 63.90% of the North America IT Asset Disposition market share in 2025 and are tracking an 11.74% CAGR. Many lacked formal retirement policies until high-profile data breaches highlighted the risks of informal disposal. Providers now package turnkey bundles that include pickup, certified wiping, and residual-value credits, removing the need for in-house expertise.

Large Enterprises keep stable demand through multiyear master service agreements that stress system-wide compliance and transparent audit trails. While these buyers often negotiate favorable terms, SMEs constitute the larger growth pool as awareness rises and ESG objectives extend beyond Fortune 1000 ranks. Flexible pricing and national pickup coverage remain decisive for penetrating this fragmented customer base.

Geography Analysis

The United States remains the core of the North America IT Asset Disposition market, benefiting from state-level e-waste mandates that drive standardized disposal across multiple industries. Hyperscale data-center deployments exceeding USD 20 billion in 2025 elevate demand for decommissioning skills tailored to high-density racks and advanced transceivers. Yet rural segments still see sparse pickup coverage, so investments in optimized routing software are under way to contain transportation costs.

Canada’s policy momentum around circular economy accelerates ITAD activity, especially as ESG-linked financing lowers capital costs for service-provider upgrades. Provincial authorities widen product-scope definitions, converting compliance into a competitive imperative for small and mid-sized enterprises. Cross-border flows with the United States allow remarketing channels to exploit scale, but the Basel Amendment curbs outbound e-waste, stimulating domestic processing.

Mexico’s market grows on the back of multinational plant expansions that must mirror global sustainability commitments. Urban centers witness the launch of tech-enabled recycling hubs using automation and blockchain to certify chain-of-custody, while non-metro areas lag due to limited route density. Government incentives and knowledge-sharing initiatives with US and Canadian counterparts aim to standardize protocols and bolster investor confidence.

Competitive Landscape

The sector is moderately fragmented, with global brands, OEMs, and regional specialists contending for share. Iron Mountain, Dell Technologies, and Sims Lifecycle Services exploit extensive logistics networks to service large-enterprise contracts. Regional players differentiate through niche certifications or vertical-specific expertise, such as healthcare or public-sector mandates.

Consolidation is gathering pace. Iron Mountain’s USD 200 million acquisition of Regency Technologies in early 2025 broadened its asset-processing footprint and deepened its U.S. logistics grid, underscoring an industry trend toward end-to-end lifecycle management offerings. Competitors invest heavily in automated sorting lines, AI-driven value-estimation tools, and blockchain-based chain-of-custody systems that heighten transparency and efficiency.

White-space opportunities persist in distributed edge-computing retirements and lithium-ion battery reclamation. Providers capable of closed-loop material recovery for batteries or compliant destruction of solid-state AI accelerators can carve profitable niches. Nonetheless, long-term success hinges on national coverage, regulatory fluency, and integrated service bundles that transform ITAD from a one-off event into a strategic lifecycle function.

North America IT Asset Disposition Industry Leaders

Iron Mountain Incorporated

Dell Technologies

Sims Limited

Hewlett Packard Enterprise Development

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Iron Mountain completed its USD 200 million acquisition of Regency Technologies, adding specialized processing facilities and a wider logistics fleet.

- October 2024: HP Inc. amplified its Planet Partners program by embedding refurbishment and resale, enabling customers to manage procurement and disposal through a single vendor.

- June 2024: Basel Amendment rules took effect, tightening cross-border e-waste movement and motivating North American firms to boost domestic processing.

- April 2024: Dell Technologies set 2030 reuse-or-recycle targets equal to total product shipment tonnage, expanding its packaging policy to 100% recycled or renewable inputs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North American IT Asset Disposition (ITAD) market as paid services that retire, sanitize, remarket, or recycle enterprise-owned computers, peripherals, servers, storage arrays, smartphones, and tablets across the United States, Canada, and Mexico. Revenues merge fees billed by certified ITAD providers with resale value returned to the client, all shown in current-year US dollars.

Scope exclusion: informal scrapyards, pure consumer drop-offs, and standalone data-wiping software are not tracked.

Segmentation Overview

- By Asset Type

- Computers and Laptops

- Peripherals (Printers, Scanners, and More)

- Servers

- Smartphones and Tablets

- Storage Devices (HDD/SSD, Tape, and More)

- By Service Type

- Data Destruction / Sanitization

- De-Manufacturing and Recycling

- Logistics Management and Reverse Logistics

- Remarketing and Value Recovery

- By End-User Industry

- IT and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Healthcare and Life Sciences

- Energy and Utilities

- Education and Others

- By End-User Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Interviews with ITAD executives, corporate sustainability leads, and reverse-logistics partners in all three countries validate pricing tiers, certification uptake, and refresh-cycle length, while targeted surveys confirm residual-value curves and adoption triggers.

Desk Research

We start by matching device-retirement volumes and e-waste weights from the US EPA Facts & Figures, Statistics Canada material-flow accounts, Mexico's SEMARNAT surveys, and the UN Global E-waste Monitor. Annual 10-K filings, investor decks, and certified-recycler audits refine average service fees, resale yields, and recovery rates.

When deeper splits are required, our analysts pull revenue lines from D&B Hoovers, review contract values in Dow Jones Factiva, and probe cross-border shipment flows through Volza customs data. These references illustrate, not exhaust, the desk sources we review.

Market-Sizing & Forecasting

Mordor's model begins top-down by scaling documented decommission counts with service-attachment ratios and average fees, then cross-checks totals with sampled bottom-up roll-ups from large providers. Key variables like enterprise refresh cycles, NAID AAA premiums, metal prices, data-breach penalty trends, and haul distance feed a multivariate regression projecting revenue through 2030. Scenario analysis overlays potential regulatory shocks, and audit-based ratios patch partial disclosures.

Data Validation & Update Cycle

Outputs pass range screens, peer review, and management sign-off before release. We reopen the model each year, or sooner when regulation, mergers, or commodity swings shift volumes or pricing.

Why Mordor's North America IT Asset Disposition Baseline Earns Trust

Published 2024 estimates span roughly USD 4 billion to above USD 7 billion. This range stems from differing asset baskets, treatment of resale proceeds, and refresh-cycle multipliers.

Key gap drivers are that some studies omit Mexico, others fold software and data-center labor into revenues, and refresh assumptions vary from three to six years. Our interviews fix a 4.1-year weighted average for 2024.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.85 B (2025) | Mordor Intelligence | |

| USD 4.00 B (2024) | Regional Consultancy A | Drops Mexico and smartphones; counts provider revenue only |

| USD 7.57 B (2024) | Trade Journal B | Adds software and uses gross resale without netting client share |

These comparisons show that Mordor analysts ground every variable in verifiable data, balance top-down totals with targeted bottom-up checks, and refresh inputs yearly, giving decision-makers a dependable, transparent baseline.

Key Questions Answered in the Report

What is driving the rapid growth of the North America IT Asset Disposition market?

Digital transformation, stricter e-waste and privacy regulations, and the financial appeal of remarketing services underpin the market’s 10.26% CAGR forecast.

How large will the North America IT Asset Disposition market be by 2031?

The market is projected to reach USD 8.71 billion by 2031, up from USD 4.85 billion in 2025.

Which service segment is expanding the fastest?

Remarketing and Value Recovery is set to grow at 15.02% CAGR as enterprises seek to monetize residual asset value.

Why are SMEs adopting ITAD services more quickly than large enterprises?

SMEs now recognize that certified disposition reduces data-breach risk and can supply trade-in credits that offset new hardware costs, driving an 11.74% CAGR for the segment.

What is the most significant restraint facing the market?

Fragmented reverse-logistics infrastructure raises service costs and limits coverage outside major cities, dampening penetration in price-sensitive regions.

Page last updated on: