Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

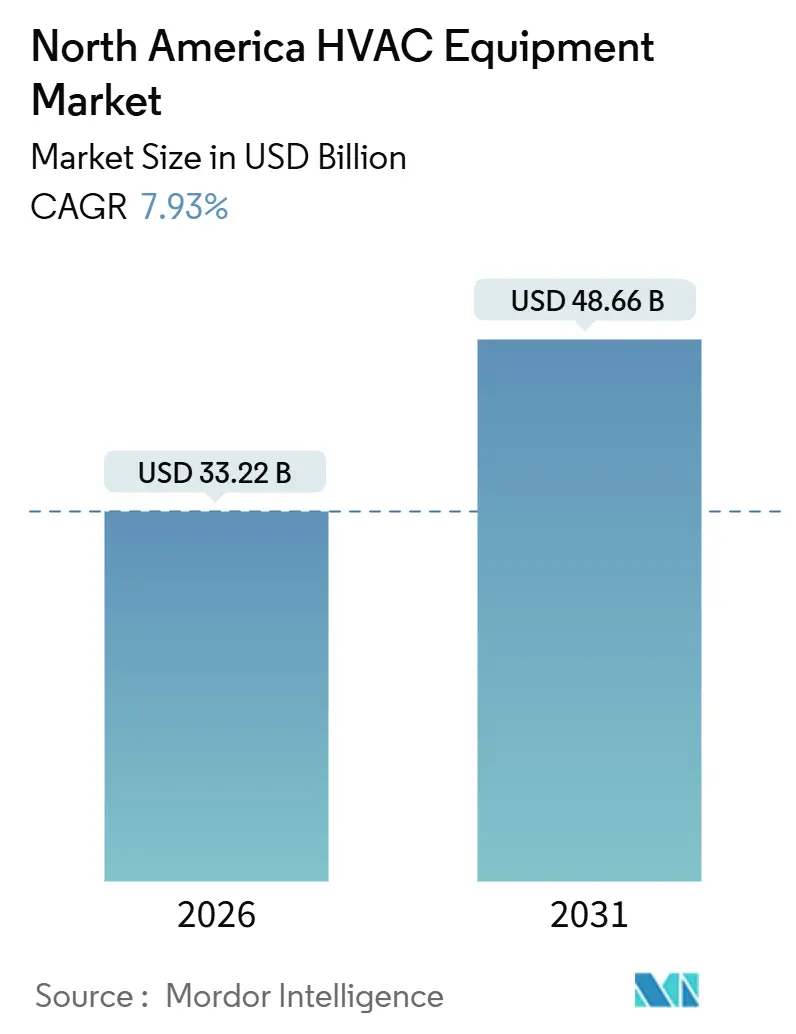

| Market Size (2026) | USD 33.22 Billion |

| Market Size (2031) | USD 48.66 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America HVAC Equipment Market Analysis by Mordor Intelligence

The North America HVAC equipment market size reached USD 33.22 billion in 2026 and is projected to climb to USD 48.66 billion by 2031, translating into a robust 7.93% CAGR over the period. Replacement cycles tied to new A2L-refrigerant mandates, accelerating heat-pump adoption, and a shift toward connected, demand-response-ready systems are sustaining momentum despite supply-chain volatility. Retrofit activity accounts for a dominant share of spending, as building owners move quickly to lock in federal tax credits before they phase down, while commercial buyers upgrade ventilation and controls to meet stricter indoor-air-quality codes. Competitive intensity remains high; incumbents are protecting installed-base service revenues through predictive-maintenance contracts, while Asian brands erode price points in the fast-growing ductless segment. Near-term tailwinds from U.S. semiconductor re-shoring and Mexican nearshoring offset headwinds from installer labor shortages and higher liability premiums for A2L systems.

Key Report Takeaways

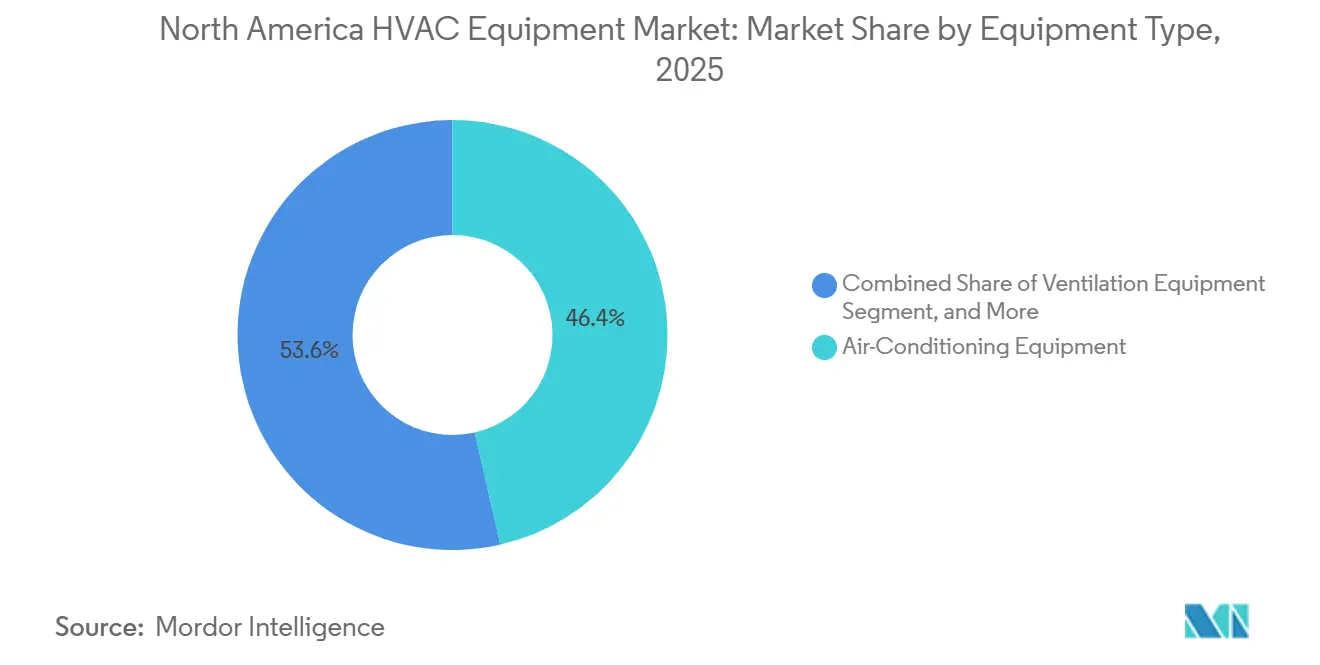

- By equipment type, air-conditioning systems led with 46.43% revenue share in 2025, and the subsegment is expanding at an 8.64% CAGR through 2031.

- By installation type, retrofit and replacement accounted for 60.84% of demand in 2025, while new construction is projected to grow at an 8.29% CAGR through 2031.

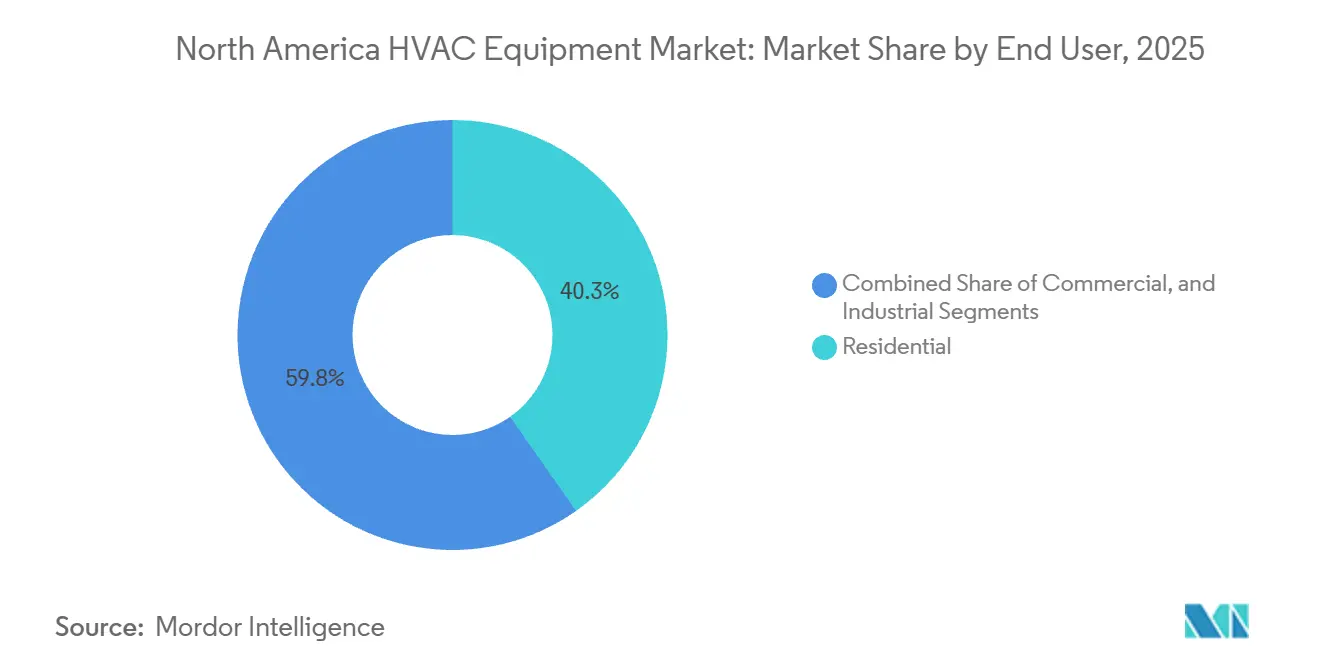

- By end user, the commercial segment accounted for 59.75% of spend in 2025 and is growing at an 8.81% CAGR through 2031.

- By building type, office buildings commanded a 32.62% share of commercial HVAC demand in 2025, whereas data centers are forecast to post the fastest 9.12% CAGR through 2031.

- By country, the United States maintained a dominant 79.82% share in 2025, while Mexico is projected to register the fastest 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America HVAC Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Heat Pumps and Electrification of Heating | +1.80% | United States and Canada (Pacific Northwest, Northeast) | Medium term (2-4 years) |

| Accelerating Adoption of Low-GWP A2L Refrigerants Creating Replacement Wave | +1.50% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Growing Demand for Smart and Connected HVAC Systems | +1.20% | U.S. commercial and high-end residential, Canadian urban centers | Medium term (2-4 years) |

| Stringent Energy-Efficiency Regulations and Incentives | +1.10% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Rising Residential and Non-residential Construction Activity | +0.90% | Mexico nearshoring corridors, U.S. Sunbelt, Canadian infill | Medium term (2-4 years) |

| Emergence of Prefabricated Modular HVAC Units for Quick Retrofits | +0.60% | U.S. commercial retrofits, Canadian healthcare pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rapid Adoption of Heat Pumps and Electrification of Heating

Federal tax credits of up to USD 2,000 per unit, combined with state bans on new natural-gas hookups, have propelled heat-pump shipments beyond gas furnaces for the first time in U.S. history.[1]U.S. Department of Energy, “Heat Pump Shipments Surpass Gas Furnaces for First Time,” Energy.gov Cold-climate units capable of delivering full capacity at −15 °F, backed by CAD 5,000 (USD 3,950) in utility rebates, are taking hold in Canada. Variable-speed compressors now routinely achieve seasonal COPs of 3.5, reducing payback periods to fewer than 6 years in many Northeast markets. As regional gas utilities pivot toward electrification incentives, dual-fuel systems pairing heat pumps with backup resistance heaters are gaining traction in retrofit projects. This structural shift is expected to re-weight the North America HVAC equipment market toward electrically driven heating across the forecast horizon.

Accelerating Adoption of Low-GWP A2L Refrigerants Creating Replacement Wave

The American Innovation and Manufacturing Act triggered a 40% cut in hydrofluorocarbon quotas by 2024, lifting R-410A prices 60% and pushing OEMs to R-454B and R-32 formulations.[2]U.S. Environmental Protection Agency, “Phasedown of Hydrofluorocarbons Under the AIM Act,” Epa.gov Revised ASHRAE 15 and NFPA 1 codes now require integrated leak detection and enhanced ventilation, encouraging factory-charged equipment that minimizes field refrigerant handling. Building owners are pre-emptively retiring 10- to 12-year-old systems ahead of further quota cuts, accelerating a replacement wave that benefits brands with deep distributor networks. Shorter product life cycles increase aftermarket parts revenue and favor manufacturers able to quickly pivot design platforms.

Growing Demand for Smart and Connected HVAC Systems

FERC Order 2222 opened wholesale markets to distributed energy resources, allowing networked rooftop units to earn USD 50-150 per kW of peak load curtailed. Wi-Fi thermostats surpassed 40% penetration in new U.S. homes in 2025, fueled by voice-assistant integration and utility demand-response rebates. OEMs are converting raw equipment data into subscription-based predictive-maintenance offers, diversifying cash flows away from hardware margins. Convergence with BACnet and Modbus allows lighting, shading, and ventilation to coordinate, lowering total energy use while maintaining ASHRAE 62.1 indoor-air-quality thresholds.[3]ASHRAE, “Standard 62.1 Ventilation for Acceptable Indoor Air Quality,” Ashrae.org

Stringent Energy-Efficiency Regulations and Incentives

New SEER2 baselines of 14.3 in the North and 15.0 in the South eliminated the lowest-cost tiers in 2023, steering buyers toward variable-speed compressors and electronically commutated motors. The Inflation Reduction Act’s Section 179D offers up to USD 5 per ft² for 50% reductions in energy use, jump-starting large-scale rooftop and chiller retrofits. Canada’s paused Greener Homes Grant previously rebated up to CAD 5,600 (USD 4,100), creating pipeline uncertainty but signaling long-term policy support. Together, these measures lock in a higher baseline of efficiency across the North America HVAC equipment market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Transition to A2L Refrigerants Increasing Liability Insurance Costs | -0.70% | United States contractor networks (California, Northeast) | Short term (≤ 2 years) | |

| Supply-Chain Vulnerability Due to Critical Electronics and Sensor Shortages | -0.60% | United States and Canada | Short term (≤ 2 years) | |

| High Initial Capital Cost of High-Efficiency Systems | -0.50% | U.S. residential retrofits, Canadian provinces with limited rebates | Medium term (2-4 years) | |

| Skilled Labor Shortage for Installation and Maintenance | -0.40% | United States and Canada rural markets | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Transition to A2L Refrigerants Increasing Liability Insurance Costs

Contractor insurance premiums rose 15-25% in 2025 as underwriters priced in leak-related fire risk, with compliance upgrades adding USD 500-1,500 per mechanical room. Smaller installers unable to fund training and detection equipment are exiting, consolidating channels, and raising labor costs. Multifamily property managers face insurer scrutiny, slowing approvals for heat-pump retrofits that would displace legacy furnaces. In the near term, elevated liability costs suppress penetration of A2L systems among price-sensitive residential buyers.

Supply-Chain Vulnerability Due to Critical Electronics and Sensor Shortages

Microcontroller lead times hit 26 weeks in early 2025, delaying variable-speed product launches and prompting costly redesigns. Spot prices for pressure and humidity sensors climbed 40-60%, slashing margins on fixed-price distributor contracts. While new U.S. fab capacity is slated to open by late 2026, the timing gap keeps OEMs exposed to chip shortages, tempering shipment forecasts for connected equipment across the North America HVAC equipment market.

Segment Analysis

By Equipment Type: Air-Conditioning Leads as Heat Pumps Surge

Air-conditioning equipment represented 46.43% of the overall North America HVAC equipment market revenue in 2025 and is scaling at an 8.64% CAGR, supported by rising cooling-degree days and the retirement of R-410A systems. The subsegment’s share of the North America HVAC equipment market in 2026 was almost USD 15.4 billion, reflecting its entrenched role in both residential and light-commercial buildings. Ductless mini-splits stand out by capturing retrofit demand where duct installation is impractical, while variable refrigerant flow platforms enable simultaneous heating and cooling across large commercial footprints.

Heat pumps, classified within heating equipment, are closing the gap fast. Electrification mandates and rebate stacks narrow the installed-cost delta versus gas furnaces, redirecting share within the North America HVAC equipment market toward electrically driven solutions. Ventilation gear such as energy-recovery ventilators and humidifiers rides the wave of IAQ compliance, while packaged terminal units return to multifamily design specs due to simplified billing and space savings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Installation Type: Retrofit Dominates as Builders Embrace Factory Packages

Retrofit and replacement installations accounted for 60.84% of the North America HVAC equipment market share in 2025 and continue to drive near-term sales as owners accelerate system retirements ahead of tighter refrigerant caps. Financing promotions and seasonal replacement campaigns encourage homeowners to act before costly midsummer failures. Meanwhile, the North America HVAC equipment market size attached to new construction grows at 8.29% CAGR, propelled by industrial plants in Mexico and multifamily projects across the U.S. Sunbelt.

Builders increasingly specify pre-packaged mechanical rooms that arrive fully wired and charged, trimming onsite labor by up to 50%. Electrification simplifies floor plans by eliminating gas piping but pushes panel upgrades that add USD 2,000-4,000 per dwelling. The balance between retrofit and new construction will narrow only modestly through 2031, keeping replacement spend a dominant thread in the overall growth story.

By End User: Commercial Upgrades Outpace Residential Upkeep

Commercial accounts commanded 59.75% of the North America HVAC equipment market revenue in 2025 and are expanding at an 8.81% CAGR, thanks to IAQ retrofits, energy-cost-reduction mandates, and monetization of demand response. Office portfolios are installing energy-recovery ventilators to comply with ASHRAE 62.1, while malls are swapping fixed-speed rooftop units for variable-speed models that modulate load in response to real-time occupancy.

Residential spend holds 40.25%, but adoption hurdles persist because heat-pump premiums and A2L insurance costs can deter budget-constrained homeowners. Integration with rooftop solar and home batteries is emerging as a selling point, signaling how the North America HVAC equipment market will intertwine with distributed energy investments. Industrial users remain a niche, focusing on process chillers and high-tonnage handlers where uptime is mission-critical.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Building Type (Commercial): Data Centers Dominate Growth Pipeline

Among commercial end users, data centers posted the fastest 9.12% CAGR, as hyperscalers race to cool AI-accelerator racks with densities exceeding 100 kW. This niche represents a rapidly expanding slice of the North America HVAC equipment market, with operators pivoting to liquid cooling and modular deployments that compress project timelines from 18 months to 6 months.

Office buildings still account for 32.62% of the 2025 spend but battle hybrid-work-induced underutilization. Healthcare facilities invest in HEPA filtration and UV germicidal add-ons, boosting per-square-foot HVAC spend. Hospitality conversions to ductless mini-splits favor granular room control, and retail shifts toward sensor-driven conditioning that aligns energy use with foot traffic.

Geography Analysis

The United States held 79.82% of 2025 revenues, giving it the lion’s share of the North America HVAC equipment market. Population inflows and higher cooling-degree days fuel sunbelt demand, while Northern states pivot to cold-climate heat pumps backed by state electrification credits. Fragmented state codes complicate national product rollouts but reward agile regional players. Federal Section 25C and 179D incentives remain pivotal, although their scheduled phase-downs pull some demand forward into the 2026-2028 window.

Mexico is the fastest-growing geography, with an 8.78% CAGR through 2031, as nearshoring sparks industrial construction. Automotive and electronics plants in Nuevo León and Guanajuato specify large-tonnage handlers and process chillers, inflating the North America HVAC equipment market size attributable to the country. Residential demand concentrates in Mexico City and Monterrey, skewing toward ductless units due to price sensitivity and smaller living spaces. Gradually tightening CONUEE efficiency labels are raising minimum specification levels, albeit unevenly.

Canada, though the smallest contributor, is quickly electrifying heating due to carbon pricing in British Columbia, Quebec, and Nova Scotia. Cold-climate heat pumps qualify for CAD 5,600 (USD 4,100) in rebates, though program pauses inject volatility into contractor pipelines. Urban density in Toronto and Vancouver encourages district energy, tempering unitary equipment sales but opening service opportunities around central-plant optimization.

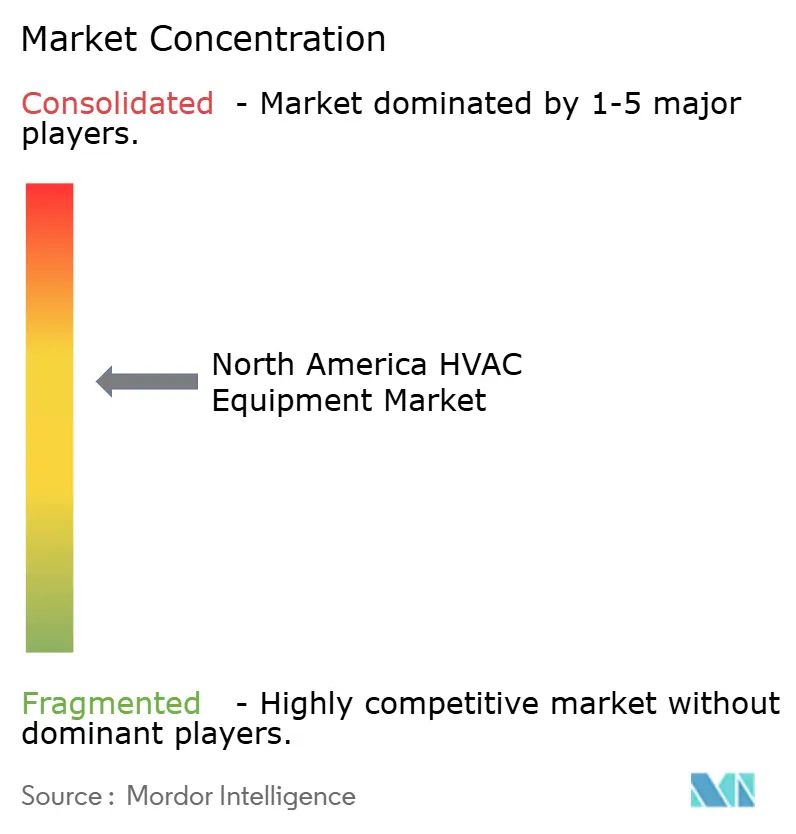

Competitive Landscape

Competition in the North America HVAC equipment market remains moderately fragmented. Carrier, Trane Technologies, and Daikin monetize massive installed bases through IoT-driven service contracts that predict failures and proactively schedule parts, turning lumpy hardware revenue into steady cash flows. Johnson Controls and Lennox follow suit, layering cloud analytics onto legacy controls to differentiate service offerings.

Asian brands such as Gree, Midea, and LG undercut prices in the ductless mini-split category and leverage variable refrigerant flow expertise to win light-commercial bids. The incumbent response centers on warranty extensions, rapid-ship programs, and tighter integration with building-automation protocols. Emerging white space includes prefabricated modular HVAC units for quick retrofits, and AAON’s customizable rooftop line offers 8- to 12-week delivery, beating larger competitors’ 16-plus-week timelines.

The A2L transition rewards OEMs that can pivot quickly, distributors that must clear legacy R-410A stock, and service organizations that capture refrigerant conversion work, locking in recurring revenue. Data-center cooling shifts toward liquid loops present opportunities for industrial cooling specialists to gain footholds, challenging traditional HVAC incumbents to add complementary technologies or form partnerships.

North America HVAC Equipment Industry Leaders

Johnson Controls International PLC

Daikin Industries Ltd

Lennox International Inc.

Electrolux AB

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Carrier Global Corporation committed USD 150 million to expand its Monterrey, Mexico plant, adding 200,000 rooftop and ductless units of annual capacity, with completion targeted for mid-2027.

- December 2025: Trane Technologies closed an acquisition of a commercial HVAC controls software platform, integrating cloud analytics and demand-response into its Tracer suite.

- November 2025: Daikin Industries secured a multiyear semiconductor supply agreement with a U.S. chipmaker, guaranteeing priority allocation for variable-speed compressor drives.

- October 2025: Johnson Controls introduced A2L-ready rooftop units using R-454B and embedded leak-detection sensors that satisfy updated ASHRAE 15 and NFPA 1 codes.

- September 2025: Lennox International opened a USD 120 million heat-pump facility in South Carolina, adding 300,000 units of annual cold-climate capacity.

North America HVAC Equipment Market Report Scope

Heating, ventilation, and air conditioning (HVAC) refers to the use of technologies to control the temperature, humidity, and air quality in enclosed spaces. HVAC equipment provides thermal comfort and acceptable indoor air quality in both the indoor and vehicular environments. It is an important part of residential structures, such as single-family homes, apartment buildings, hotels, and senior living facilities, as well as medium-to-large industrial and office buildings, such as hospitals, where safe and healthy building conditions are regulated with respect to temperature and humidity, using outdoor air.

The North America HVAC Equipment Market Report is Segmented by Equipment Type (Heating Equipment, Ventilation Equipment, and Air-Conditioning Equipment), Installation Type (New Construction, and Retrofit and Replacement), End User (Residential, Commercial, and Industrial), Building Type for Commercial (Office Buildings, Healthcare Facilities, Hospitality and Leisure, Retail Stores and Malls, Educational Institutions, and Data Centers), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Equipment Type

| Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | ||

| Unitary Heaters | ||

| Ventilation Equipment | Air Handling Units (AHUs) | |

| Air Filters | ||

| Fan Coil Units | ||

| Humidifiers and Dehumidifiers | ||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits |

| Ductless Mini-Splits | ||

| Packaged Rooftops | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

By Installation Type

| New Construction |

| Retrofit / Replacement |

By End User

| Residential |

| Commercial |

| Industrial |

By Building Type (Commercial)

| Office Buildings |

| Healthcare Facilities |

| Hospitality and Leisure |

| Retail Stores and Malls |

| Educational Institutions |

| Data Centers |

By Country

| United States |

| Canada |

| Mexico |

| By Equipment Type | Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | |||

| Unitary Heaters | |||

| Ventilation Equipment | Air Handling Units (AHUs) | ||

| Air Filters | |||

| Fan Coil Units | |||

| Humidifiers and Dehumidifiers | |||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits | |

| Ductless Mini-Splits | |||

| Packaged Rooftops | |||

| Variable Refrigerant Flow (VRF) Systems | |||

| Room Air Conditioners | |||

| Packaged Terminal Air Conditioners | |||

| Chillers | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Building Type (Commercial) | Office Buildings | ||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Retail Stores and Malls | |||

| Educational Institutions | |||

| Data Centers | |||

| By Country | United States | ||

| Canada | |||

| Mexico | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will North American HVAC equipment spending be by 2031?

It is projected that total outlays will reach USD 48.66 billion, up from USD 33.22 billion in 2026, equating to a 7.93% CAGR.

Which product group is expanding the fastest?

Air-conditioning systems, particularly ductless mini-splits and variable refrigerant flow platforms, are advancing at an 8.64% CAGR through 2031.

Why is the commercial buyer segment outpacing residential demand?

Commercial owners seek indoor-air-quality compliance and utility demand-response revenue, pushing the segment to an 8.81% CAGR versus slower residential growth.

What role does Mexico play in regional growth?

Nearshoring of manufacturing is propelling Mexico to an 8.78% CAGR, the fastest among the three countries, with strong demand for industrial chillers and handlers.

How are A2L refrigerants changing replacement cycles?

Rising R-410A prices and new safety codes shorten equipment life cycles from 15 years to roughly 12 years, accelerating replacement sales.

Which companies command the largest share?

Carrier, Trane Technologies, Daikin, Johnson Controls, and Lennox together hold about 55–60% of regional revenue, indicating a moderately concentrated landscape.