VRF Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

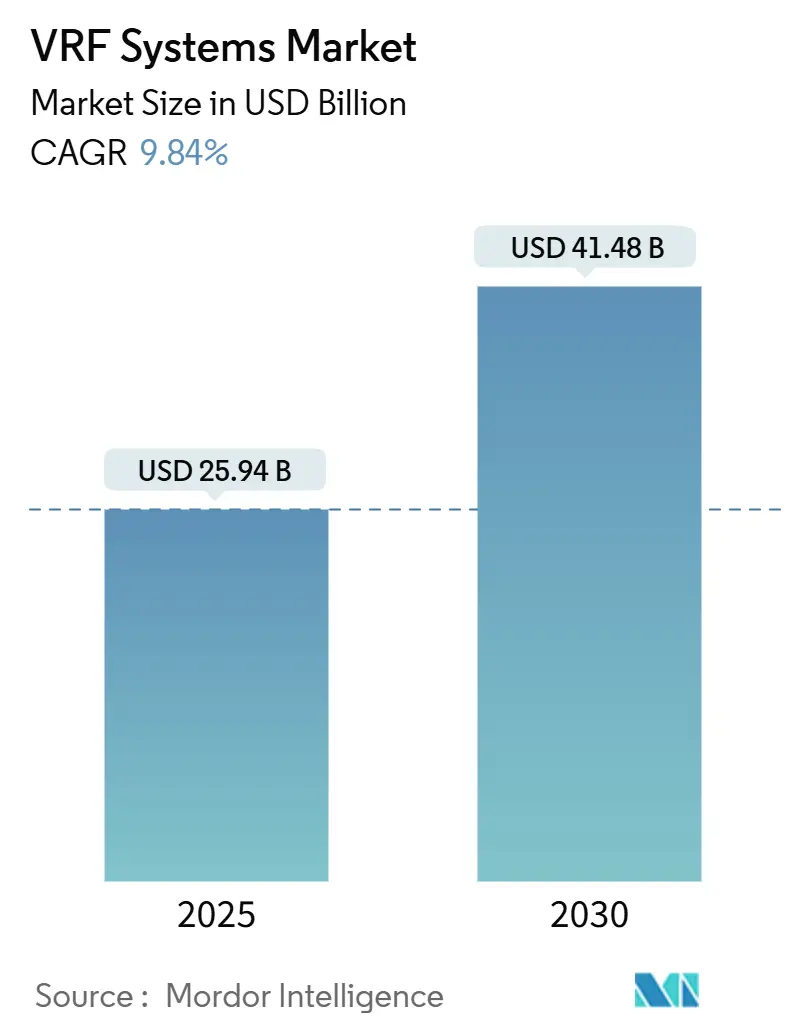

| Market Size (2025) | USD 25.94 Billion |

| Market Size (2030) | USD 41.48 Billion |

| Growth Rate (2025 - 2030) | 9.84% CAGR |

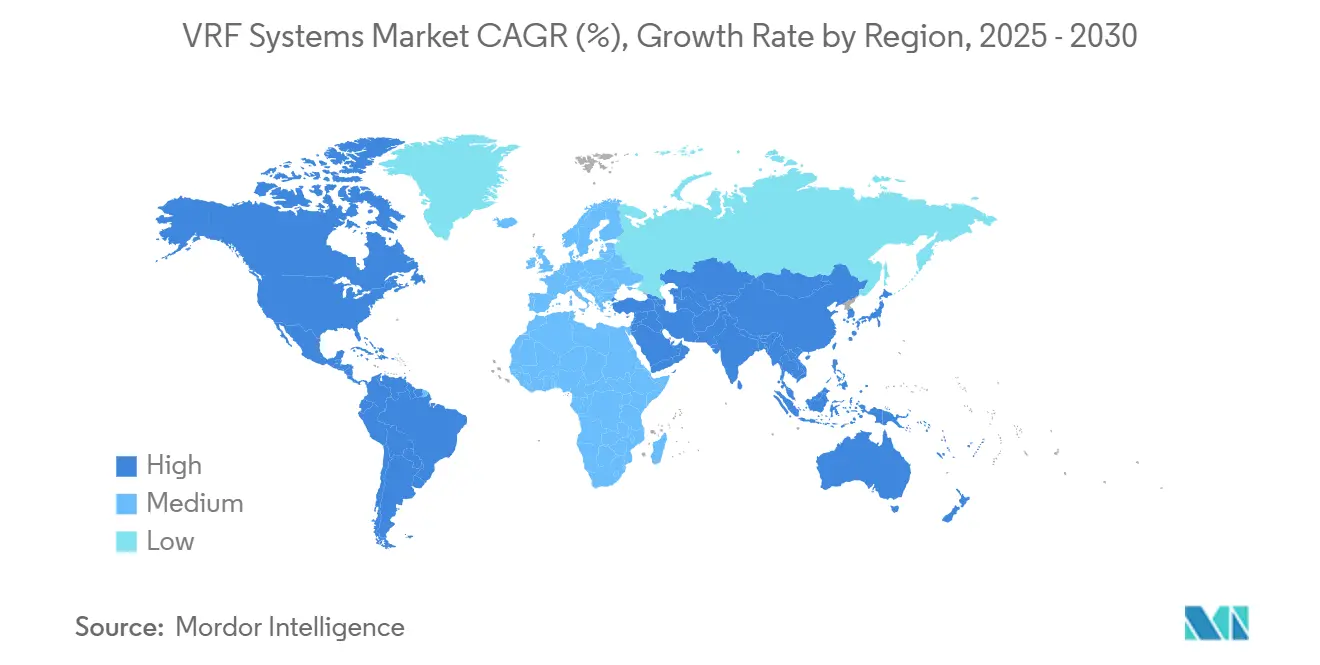

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

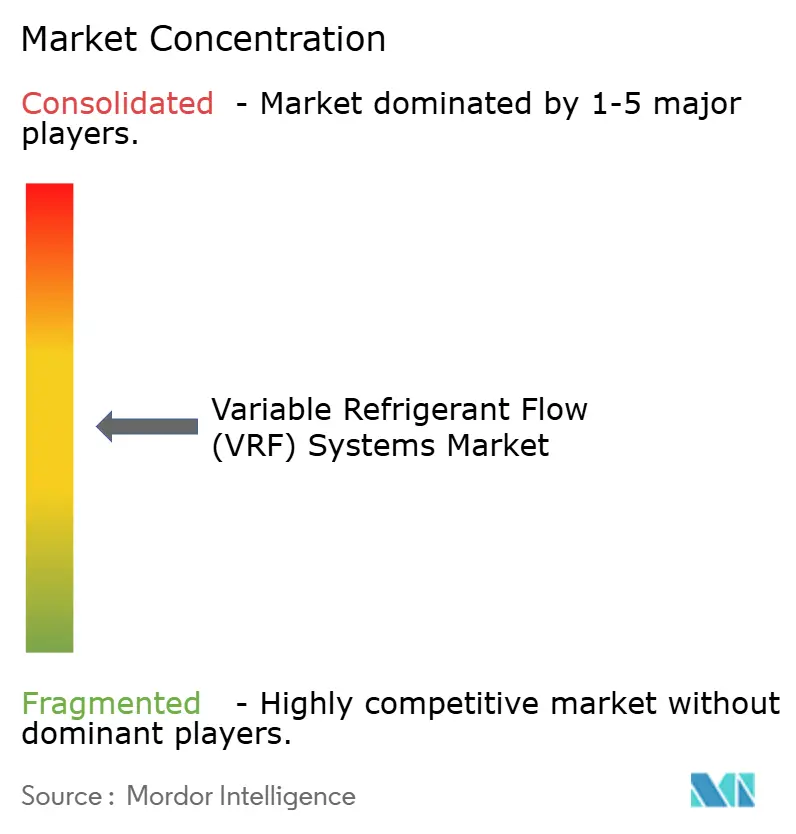

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

VRF Systems Market Analysis by Mordor Intelligence

The variable refrigerant flow (vrf) systems market size is valued at USD 25.94 billion in 2025 and is forecast to reach USD 41.48 billion by 2030, advancing at a 9.84% CAGR. Demand momentum reflects tighter refrigerant rules, breakthroughs in cold climates that extend heat-pump performance to –22 °F, and electrification mandates embedded in the American Innovation and Manufacturing (AIM) Act.[1]Environmental Protection Agency, “Phasedown of Hydrofluorocarbons,” federalregister.gov Supply-chain volatility in R-454B and R-32 pricing is reshaping sourcing strategies, while AI-native control platforms are turning VRF units into grid-interactive resources that support renewable integration. South America leads growth at 11.8% CAGR thanks to Brazil’s 38% jump in air-conditioner output to 5.9 million units in 2024.

Key Report Takeaways

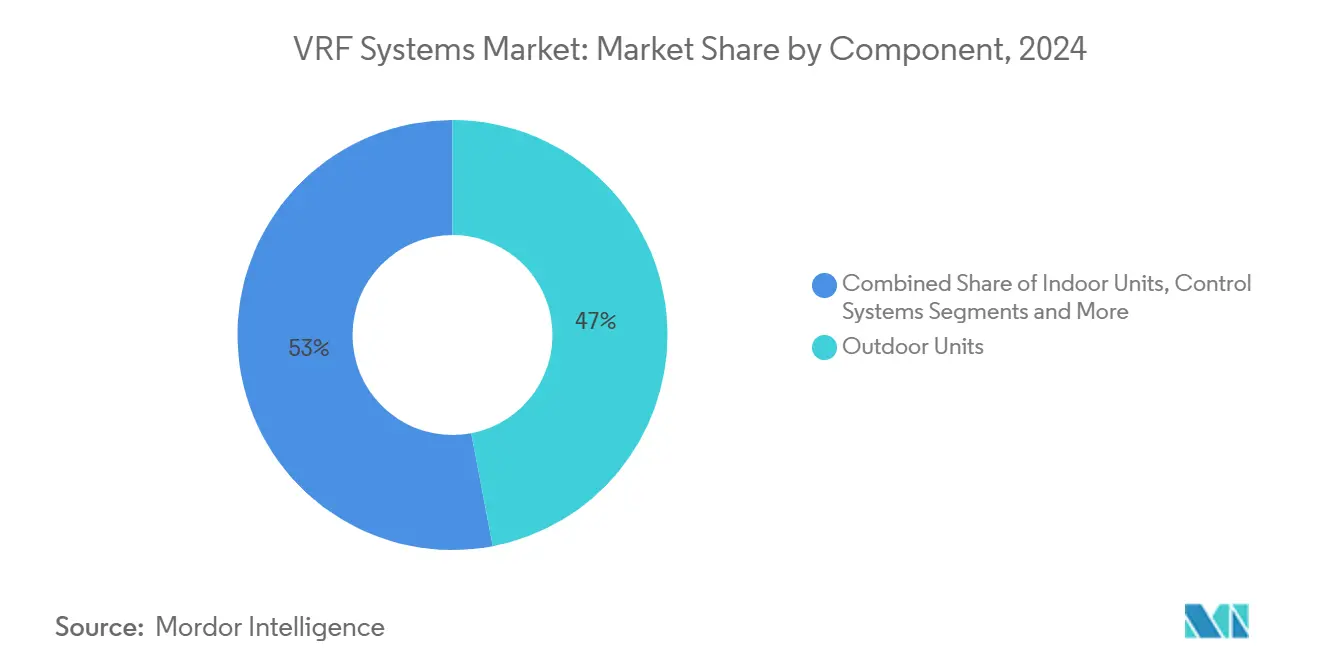

- By component, outdoor units held a 47% share of the variable refrigerant flow (vrf) systems market size in 2024, while control systems are projected to expand at a 10.9% CAGR to 2030.

- By system type, heat-pump configurations commanded 54.2% share of the variable refrigerant flow (vrf) systems market size in 2024; heat-recovery variants are forecast to grow at a 10.8% CAGR.

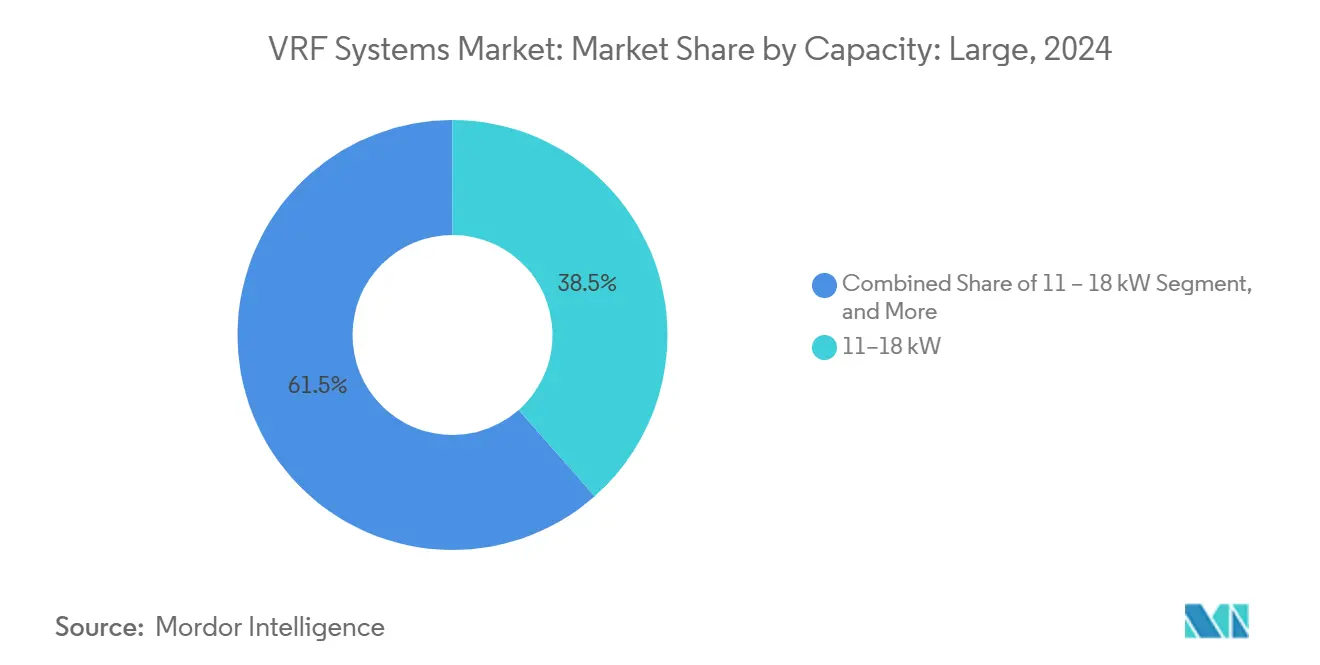

- By capacity, the 11–18 kW class captured 38.5% share of the variable refrigerant flow (vrf) systems market size in 2024; systems above 24 kW show the highest 11.1% CAGR through 2030.

- By end user, commercial facilities led with 49.1% share of the variable refrigerant flow (vrf) systems market size in 2024, whereas residential applications registered the fastest 10.5% CAGR.

- By geography, Asia-Pacific maintained a 52.7% share of the variable refrigerant flow (vrf) systems market size in 2024; South America advances at an 11.8% CAGR to 2030.

Global VRF Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retrofit demand in historical and high-rise buildings | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Stringent refrigerant-phase-down regulations (AIM Act, F-Gas) | +2.1% | North America and EU, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Rapid heat-pump electrification agendas in Europe and Japan | +1.6% | Europe and Japan, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Demand for HVAC load-flexibility to balance renewable grids | +1.3% | Global, early adoption in Germany, California | Medium term (2-4 years) |

| Smart building integration and BMS-driven optimisation | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Cold-climate VRF breakthroughs (<-22 °F operation) | +1.4% | North America, Northern Europe, parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Retrofit Demand in Historical and High-Rise Buildings

Preservation rules in Europe and North America favour VRF adoption because slim refrigerant piping minimises structural disturbance. The Hotel Saint Louis retrofit used Samsung DVM S heat-recovery units to protect heritage interiors while freeing revenue-generating floor space. Comparable logic guided St. Patrick Catholic Church in Illinois, where Mitsubishi equipment met local heritage criteria and reduced noise levels.[2]Mitsubishi Electric Trane HVAC US, “St. Patrick Catholic Church,” mitsubishicomfort.com In New York, Local Law 97 compliance is driving co-op boards to switch from fossil steam to VRF heat pumps, cutting projected winter bills by 80%. Europe's strict conservation statutes and high-rise constraints accelerate similar demand because traditional ducts cannot fit narrow shafts. This retrofit surge enlarges the addressable variable refrigerant flow (vrf) systems market more than new-build projects because stock of older buildings far exceeds annual construction additions.

Stringent Refrigerant-Phase-Down Regulations (AIM Act, F-Gas)

The EPA’s decision to extend the installation deadline for high-GWP VRF equipment to 1 January 2027 prevents stranded inventory yet keeps pressure on manufacturers to pivot toward R-454B and R-32 lines.[3]Environmental Protection Agency, “Phasedown of Hydrofluorocarbons,” federalregister.gov Mitsubishi Electric Trane HVAC US responded by unveiling an R-454B portfolio with 78% lower GWP, equipped with embedded leak-detection logic to satisfy A2L safety codes. Worthington Enterprises ramped cylinder production to ease container shortages, illustrating how regulation cascades through component supply chains. Europe’s F-Gas proposals and Japan’s April 2025 mandate for low-GWP multy splits mirror the U.S. path, prompting Mitsubishi Heavy Industries to debut 31 R-32 residential models with AI comfort modes. The regulatory timetable thus accelerates innovation while favouring brands with secure refrigerant pipelines.

Rapid Heat-Pump Electrification Agendas in Europe and Japan

EU modelling shows that residential-heating decarbonisation needs EUR 13 billion (USD 14.3 billion) annual subsidies, with current policy only closing 60% of the gap. Targeted grants stimulate demand in Eastern Europe, where gas boilers still dominate. Japan’s long-term carbon neutrality plan mainstreams cold-climate VRF; Hitachi’s air365 Max heats to –22 °F, meeting Hokkaido specifications. LG built a global R&D triangle linking Alaska, Oslo and Seoul to refine algorithms for extreme temperatures. These policy-driven volumes enlarge manufacturing scale, reduce per-unit cost and fortify the variable refrigerant flow (vrf) systems market against cyclical swings in commercial construction.

Demand for HVAC Load-Flexibility to Balance Renewable Grids

Utilities with high solar and wind penetration pay building owners to modulate HVAC loads. Rheem patented a heat-pump interface that receives dispatch signals and throttles compressors accordingly. Academic trials using model-predictive control realised 15–25% emission cuts versus conventional logic, proving the grid value of variable capacity drives.[4]Environmental Protection Agency, “Phasedown of Hydrofluorocarbons,” federalregister.gov VRF units further operate as short-term thermal batteries, pre-cooling or pre-heating during low-price hours. As demand-response tariffs spread in Germany and California, grid-interactive capability becomes a purchase criterion, enlarging premium segments within the variable refrigerant flow (vrf) systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High first-cost vs. RTU and chilled-water systems | -1.4% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Shortage of VRF-trained installers and service technicians | -1.1% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Supply-chain exposure to R-32 / R-454B refrigerant price swings | -0.9% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Installation-complexity in existing labs / data-centres | -0.7% | Global, specialized applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High First-Cost vs. RTU and Chilled-Water Systems

Installed VRF budgets of USD 16.50–33 per sq ft can exceed rooftop-unit alternatives, dampening uptake in capital-constrained markets. U.S. tax credits now cover 30% of project cost or USD 2,000, and Inflation Reduction Act rebates reach 100% for low-income households up to USD 8,000. Financing models such as Hardware-as-a-Service convert large upfront checks into operating leases, but long paybacks of 8–15 years still impede wider diffusion.

Shortage of VRF-Trained Installers and Service Technicians

Thirty percent of HVAC contractors curtailed workloads in 2024 because they lacked A2L-qualified labour. Carrier’s TechVantage pledge to train 100,000 technicians and hire 1,000 new staff addresses the skills gap. The North American Sustainable Refrigeration Council’s R-TRADE programme has upskilled 1,200 personnel since 2023. Yet community-college curricula and tooling must still evolve to handle A2L leak-detection protocols, delaying installation throughput and restraining variable refrigerant flow (vrf) systems market velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Control Systems Drive Smart Integration

The component landscape generated the largest revenue from outdoor units that captured 47% of the variable refrigerant flow (vrf) systems market share in 2024 because they house compressors, heat exchangers and refrigerant routing assemblies. Control systems, however, are expanding at a 10.9% CAGR, making them the fastest value-accretion node across the supply chain.

Next-generation controllers integrate AI chips, cloud connectivity and built-in leak-detection sensors, transforming a once-ancillary board into a revenue-rich software platform. Samsung’s DVM S2 architecture embodies this pivot by embedding auto-commissioning logic that cuts start-up time from days to hours. As safety codes demand mandatory refrigerant-monitoring in A2L systems, every new installation requires smarter panels, sustaining double-digit growth in the control slice of the variable refrigerant flow (vrf) systems market.

By System Type: Heat Recovery Gains Momentum

Heat-pump variable refrigerant flow (vrf) systems market held 54.2% share in 2024 on account of single-package heating and cooling versatility. Heat-recovery variants are expected to register a 10.8% CAGR because they transfer waste heat from cooling zones to spaces needing heating, eliminating redundant boilers.

Field research from PSOklahoma shows 30% energy reduction when heat-recovery VRF replaces split-DX units in office settings. Universities and hospitals value lower peak-demand charges and qualify for utility incentives tied to load-shifting. Consequently, specification engineers increasingly list heat-recovery in bid documents, reinforcing its outsized contribution to incremental variable refrigerant flow (vrf) systems market size growth over the forecast horizon.

By Capacity: Large Systems Accelerate Growth

Systems in the 11–18 kW band contributed 38.5% to 2024 revenue, remaining the sweet spot for mid-rise offices and retail. Equipment above 24 kW records the highest 11.1% CAGR because data centres, electric-vehicle plants and institutional complexes seek electrified alternatives to chilled-water loops.

U.S. DOE guidance positions VRF as a boiler-replacement pathway in large commercial electrification strategies, citing modular scalability and phased installation advantages. MAN Energy Solutions’ delivery of dual 12.5 MW heat pumps to Scout Motors validates up-scaling capability beyond traditional comfort cooling. As building footprints intensify, large-capacity shipments will represent a disproportionate slice of new variable refrigerant flow (vrf) systems market billings.

By End User: Residential Segment Accelerates

Commercial buildings dominated revenue with 49.1% share in 2024, reflecting established zoning and energy-cost imperatives. The residential sub-market advances at a 10.5% CAGR, benefiting from 30% tax credits and rebate structures that cut first cost for single-family owners.

Heritage homes in dense urban centres often lack duct runs; VRF’s small-diameter piping solves that constraint while offering room-by-room comfort. Hotels also accelerate orders because occupancy-based control schemes raise guest satisfaction and trim utility expense. Taken together, these dynamics lift residential contribution from a previously niche base, strengthening demand diversification inside the variable refrigerant flow (vrf) systems market.

Geography Analysis

Asia-Pacific commanded 52.7% of global revenue in 2024, anchored by China's export-oriented manufacturing clusters and Japan's upcoming April 2025 low-GWP mandate that pushes R-32 adoption. India's data-centre boom further enlarges regional volumes, while Australia's stricter NatHERS codes bolster retrofit demand. Government subsidies and robust supply chains underpin price competitiveness, ensuring Asia-Pacific remains the production and consumption fulcrum of the variable refrigerant flow (vrf) systems market.

South America is the fastest-growing theatre, projected at 11.8% CAGR to 2030. Brazil's 5.9 million-unit output in 2024 elevated the nation to the world's second-largest producer, supporting both domestic consumption and regional exports. Macroeconomic expansion and hotter summers are accelerating adoption in Chile and Argentina, although currency volatility remains a downside risk.

North America and Europe are mature yet opportunity-rich markets, with U.S. Inflation Reduction Act incentives improving residential affordability and DOE cold-climate challenge results opening northern states previously considered uneconomic for heat pumps. Europe's EUR 13 billion (USD 14.3 billion) annual subsidy requirement underscores sustained policy support. The Middle East and Africa trail on absolute volume but register rising tender activity for mixed-use towers seeking high-efficiency cooling amid soaring temperatures.

Competitive Landscape

The industry shows moderate concentration, with Japanese, Korean and U.S. multinationals sharing leadership positions. Bosch’s USD 8 billion acquisition of Johnson Controls–Hitachi’s light-commercial portfolio nearly doubles Bosch HVAC revenue to EUR 9 billion (USD 9.8 billion) and signals a scale-seeking strategy that tightens competitive intensity. Samsung and Lennox formed a 50.1/49.9 joint venture to access North America’s ductless segment forecast to grow from USD 32 billion in 2024 to USD 48.8 billion by 2034.

Competitive advantage is migrating from hardware cost curves to differentiated cold-weather performance, AI optimisation and secure refrigerant supply. Honeywell’s 42% tariff surcharge on R-454B reshaped procurement economics, favouring brands with vertical refrigerant integration. Patent filings by Rheem on demand-response interfaces highlight how grid-interactive capability becomes a new battleground.

Workforce initiatives create soft-cap barriers; Carrier’s plan to train 100,000 technicians positions the brand as a turnkey partner for dealers lacking A2L credentials. Meanwhile, Mitsubishi Electric is investing USD 143.5 million to localise compressor production in Kentucky, mitigating currency risk and serving Buy-American preferences

VRF Systems Industry Leaders

-

Daikin Industries, Ltd.

-

Mitsubishi Electric Corporation

-

Carrier Global Corporation

-

Midea Group Co., Ltd.

-

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mitsubishi Heavy Industries rolled out 31 residential VRF models with AI comfort modes and cold climate defrost functionality.

- March 2025: Daikin reported EUR 28 billion (USD 30.9 billion) FY 2023 sales and reinforced its pan-European heat-pump push at ISH 2025.

- February 2025: Lennox and Samsung launched Varix VRF lines compatible with SmartThings connectivity, deepening their North American joint venture.

- January 2025: Mitsubishi Electric Trane HVAC US introduced an R-454B VRF range with integrated leak sensors for residential and light commercial deployment.

Global VRF Systems Market Report Scope

The Variable Refrigerant Flow (VRF) Systems Market Report is Segmented by Component (Outdoor Units, Indoor Units, Control Systems, Accessories and Piping), System Type (Heat Pump, Heat Recovery, Hybrid / Water-Cooled, All-Electric VRF), Capacity (less than or equal to 10 kW, 11 – 18 kW, 19 – 24 kW, Above 24 kW), End User (Commercial, Residential, Industrial, Public and Institutional), and by Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Outdoor Units |

| Indoor Units |

| Control Systems |

| Accessories and Piping |

| Heat Pump |

| Heat Recovery |

| Hybrid / Water-Cooled |

| All-Electric VRF |

| less than or equal to 10 kW |

| 11 – 18 kW |

| 19 – 24 kW |

| Above 24 kW |

| Commercial |

| Residential |

| Industrial |

| Public and Institutional |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Component | Outdoor Units | ||

| Indoor Units | |||

| Control Systems | |||

| Accessories and Piping | |||

| By System Type | Heat Pump | ||

| Heat Recovery | |||

| Hybrid / Water-Cooled | |||

| All-Electric VRF | |||

| By Capacity | less than or equal to 10 kW | ||

| 11 – 18 kW | |||

| 19 – 24 kW | |||

| Above 24 kW | |||

| By End User | Commercial | ||

| Residential | |||

| Industrial | |||

| Public and Institutional | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the VRF systems market growing through 2030?

The global VRF systems market is projected to expand at a 9.84% CAGR, rising from USD 25.94 billion in 2025 to USD 41.48 billion by 2030.

Which region is the largest contributor to VRF sales today?

Asia-Pacific holds 52.7% of 2024 revenue, supported by manufacturing scale in China and progressive heat-pump policies in Japan.

What is driving the shift toward low-GWP refrigerants in VRF?

AIM Act and F-Gas timelines mandate phasedown of high-GWP blends, prompting manufacturers to pivot to R-454B and R-32 products with 70–80% lower climate impact.

Why are control systems the fastest-growing component segment?

AI-enabled controllers provide predictive maintenance, leak detection and grid-interactive functions, delivering tangible energy savings that justify premium pricing.

How do heat-recovery VRF systems differ from standard heat-pump models?

Heat-recovery units can simultaneously cool and heat different zones by transferring waste heat internally, reducing building energy use by up to 30% in mixed-load facilities.

What incentives exist for residential VRF adoption in the United States?

Owners can claim 30% federal tax credits up to USD 2,000 and may qualify for Inflation Reduction Act rebates covering 100% of costs for qualifying low-income households.

Page last updated on: