Air Handling Units (AHU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

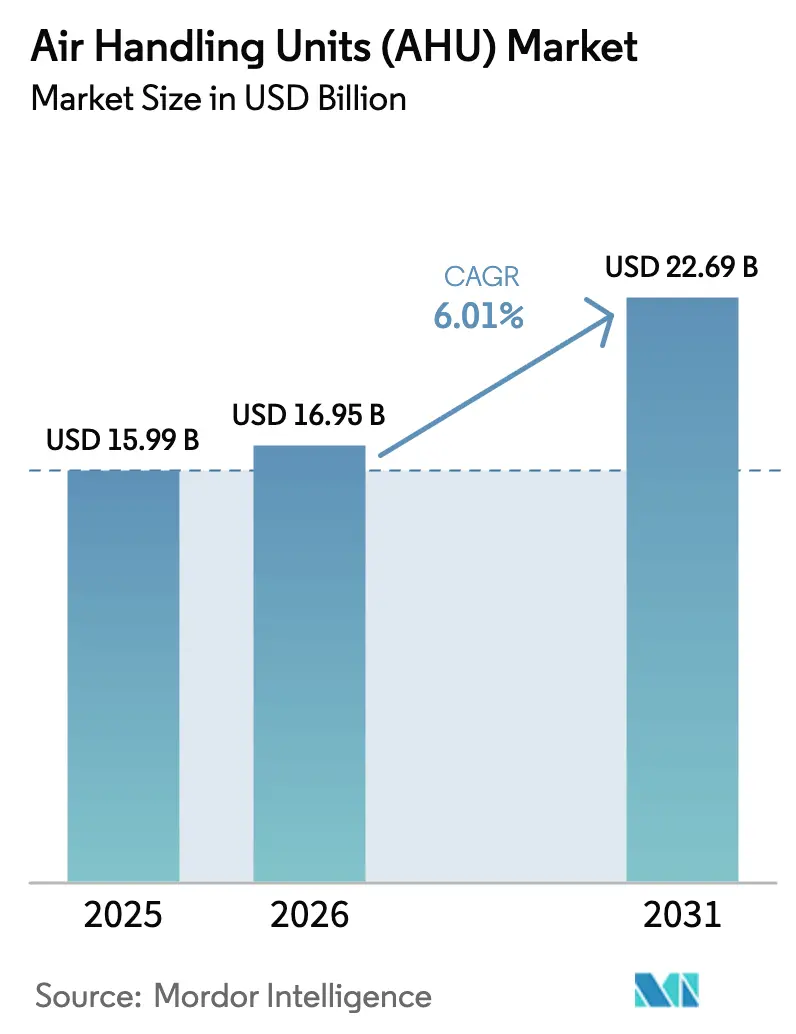

| Market Size (2026) | USD 16.95 Billion |

| Market Size (2031) | USD 22.69 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Air Handling Units (AHU) Market Analysis by Mordor Intelligence

The air handling units market size in 2026 is estimated at USD 16.95 billion, growing from 2025 value of USD 15.99 billion with 2031 projections showing USD 22.69 billion, growing at 6.01% CAGR over 2026-2031. This expansion follows rising energy-efficiency mandates, the shift to low-GWP refrigerants and stronger demand from data-center and pharmaceutical clean-room operators. The 2024 EU Ecodesign Regulation is already steering equipment designs toward lower specific fan power and ≥73% heat-recovery effectiveness. Asia-Pacific leads today’s air handling units market with 32% revenue share, supported by China’s 185 million-unit air-conditioner output and robust export growth. The Middle East shows the fastest trajectory at 9.4% CAGR through 2030 as district-cooling schemes specify custom rooftop units for 50 °C ambient conditions. Data-center build-outs in North America and Europe are accelerating modular AHU demand, while material cost inflation and skilled-labor shortages temper near-term project execution.

Key Report Takeaways

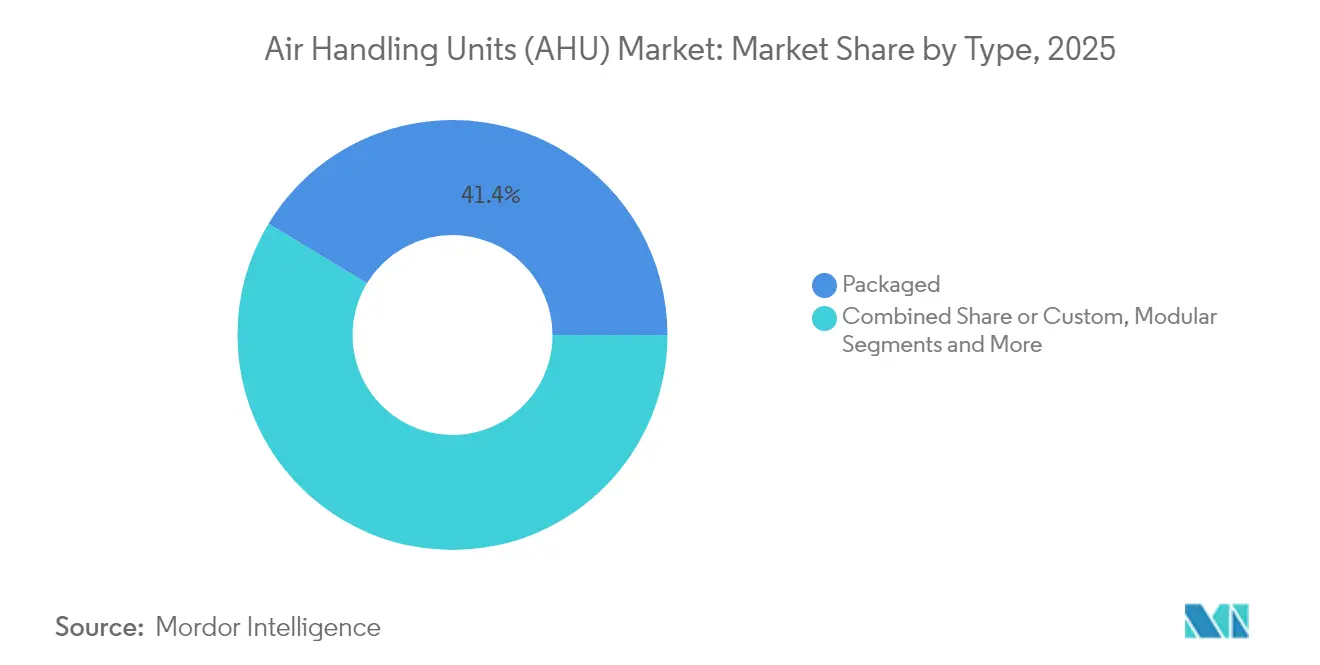

- By type, packaged units held 41.35% of the air handling units market share in 2025, whereas modular systems post the quickest 8.52% CAGR to 2031.

- By capacity, 5,001-15,000 m³/h systems accounted for 47.40% of the air handling units market size in 2025; units above 15,000 m³/h expand at 9.25% CAGR.

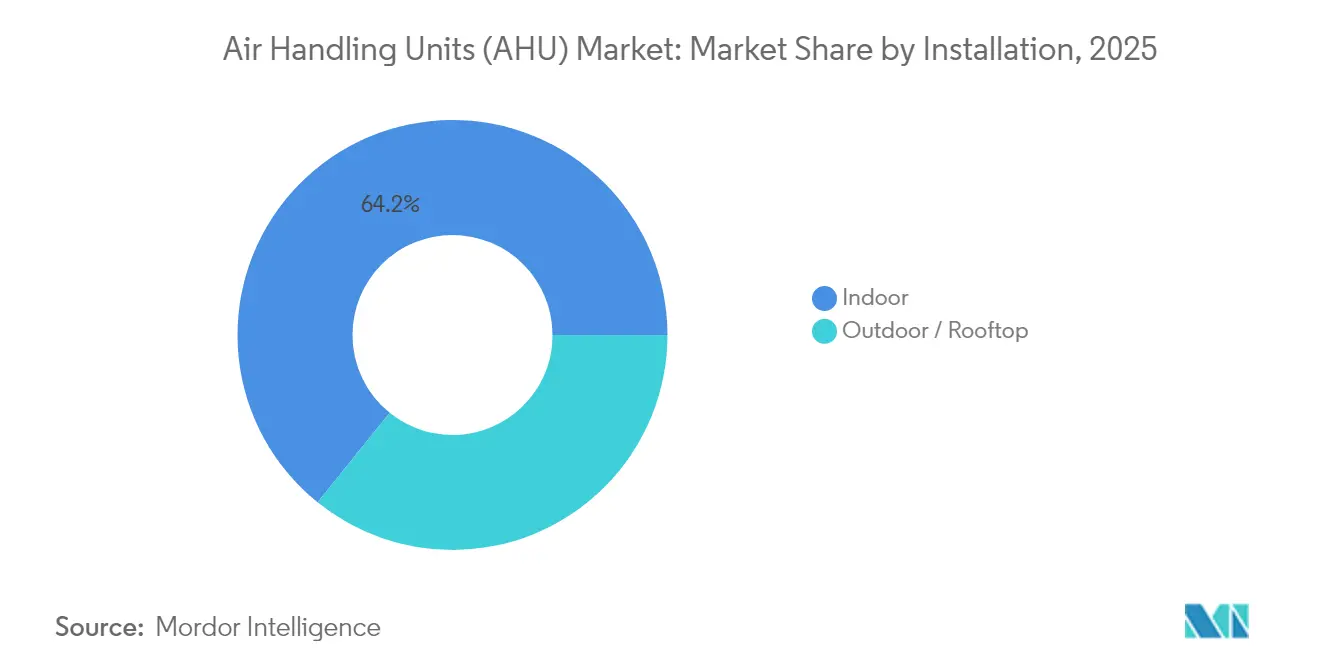

- By installation, indoor units retained 64.20% share in 2025 while outdoor/rooftop installations advance at an 7.95% CAGR.

- By component, fans and blowers dominated with 29.60% 2025 revenue, yet energy-recovery wheels rise at a 9.60% CAGR.

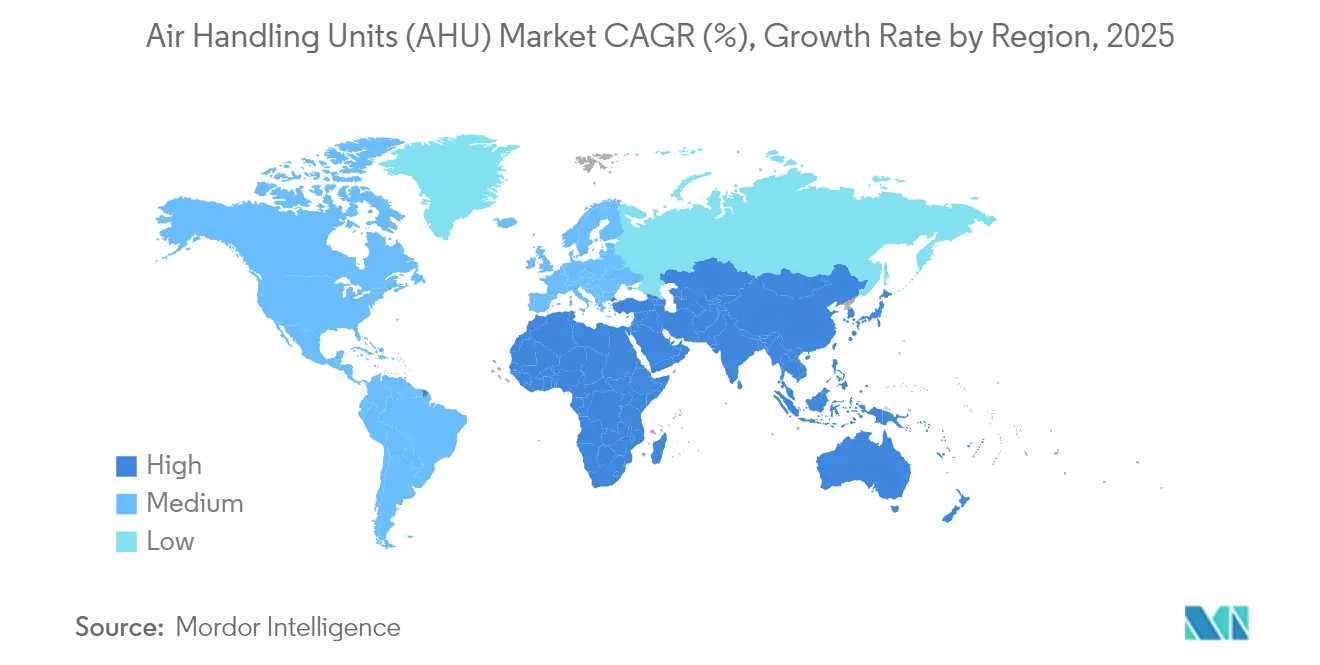

- Regionally, Asia-Pacific commanded 31.55% revenue in 2025; the Middle East is forecast to post a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Handling Units (AHU) Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Healthcare & pharma clean-room filtration uptick in Asia | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| EU Ecodesign 2023/813 mandating lower SFP & higher heat-recovery | +0.8% | Europe with adoption in North America | Long term (≥ 4 years) |

| Hyperscale data-centre build-outs requiring modular indirect adiabatic AHUs | +1.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Retrofit demand for energy-recovery ventilation in Japan & South Korea | +0.6% | APAC core, demonstration effect globally | Medium term (2-4 years) |

| GCC district-cooling projects spurring custom high-ambient rooftop AHUs | +0.7% | Middle East core, hot-climate transfer | Medium term (2-4 years) |

| Electrification of industrial heat loads driving heat-pump AHUs > 15,000 m³/h | +0.9% | Europe core, North America accelerating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Healthcare & Pharma Clean-room Filtration Uptick in Asia

Asia’s pharmaceutical build-out is boosting demand for AHUs that maintain ISO 14644-1 Class 5-to-8 spaces while balancing energy use. Manufacturers tailor units to divergent FDA and EU GMP Annex 1 velocity criteria to serve cross-border production requirements. China and India now specify HEPA-filtered air systems for biotech and semiconductor fabs, integrating real-time particle monitoring with building controls for compliance and efficiency.[1]International Organization for Standardization, “ISO 14644-1:2015 Cleanrooms and Associated Controlled Environments,” iso.org

EU Ecodesign 2023/813 Mandating Lower SFP & Higher Heat-Recovery

Regulation 2024/1781 requires AHUs to curb fan power and exceed 73% heat-recovery effectiveness, pushing energy wheels from option to baseline. Industrial fans from 125 W to 500 kW must also meet tighter efficiency rules, a change forecast to save 31 TWh by 2030. Lifecycle digital passports extend compliance beyond first sale and create after-sales differentiation.

Hyperscale Data-Centre Build-outs Requiring Modular Indirect Adiabatic AHUs

AI compute growth lifts orders for modular adiabatic units that combine air and emerging liquid-cooling loops. AAON secured USD 174.5 million in data-center thermal-management contracts for 2025 deliveries. Investments such as Daikin’s USD 121 million Mexico plant improve North American supply of purpose-built modules

Retrofit Demand for Energy-Recovery Ventilation in Japan & South Korea

Building-code revisions in Japan and Korea elevate retrofit activity. Seoul’s underground shopping-mall project cut CO₂ 33% and TVOCs 74% with energy-recovery ventilation. Payback spans 6-36 months, supporting rapid adoption of wheels and plate exchangers delivering 40-80% effectiveness.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile aluminium & copper prices inflating coil/fan costs | -0.9% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Skilled-labour shortages delaying on-site assembly of large custom AHUs | -0.7% | North America core, emerging Europe | Medium term (2-4 years) |

| Decentralised DOAS adoption as substitute in small commercial spaces | -0.5% | North America & Europe | Long term (≥ 4 years) |

| Lengthy EU approvals for low-GWP refrigerant equipment | -0.4% | Europe core, global spill-over | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminium & Copper Prices Inflating Coil/Fan Costs

Tariffs drove 25% spikes in aluminum and steel costs, compressing AHU margins and deferring projects in 2025. Copper volatility adds risk to heat-exchanger budgets that can represent 30% of unit material value. Manufacturers hedge purchases, redesign for reduced material intensity and renegotiate supply contracts, but engineering cycles lengthen.[2]ACHR News, “Solving the Refrigeration Technician Shortage,” achrnews.com

Skilled-Labour Shortages Delaying On-site Assembly of Large Custom AHUs

The HVAC sector faces 42,500 unfilled technician roles and 500,000 construction-trade vacancies, slowing installation of multi-section rooftop units. A2L refrigerant training adds complexity, prompting firms to expand apprenticeships while integrating factory-pre-assembled modules to curb field labor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular Systems Drive Innovation

Packaged units held 41.35% 2025 revenue as standard offices favored predictable selection. Modular systems, however, show 8.52% CAGR as data-center developers demand capacity blocks that install quickly and expand without downtime. Custom configurations thrive in pharmaceuticals and electronics manufacturing where bespoke filtration and humidity targets preclude catalog solutions. The air handling units market sees suppliers shifting to configurable frames that shorten lead times while preserving customization. Modular construction also limits skilled-labor exposure by transferring more assembly to the factory, a key advantage in tight labor markets.

Growth momentum stems from hyperscale data processing, where indirect adiabatic modules and liquid-cooling ready coils dominate. Flexible footprints permit phasing that aligns capital spending with rack deployment. As a result, the air handling units market integrates skid-mounted fans, coils and controls into plug-and-play packages validated in-house before shipment.

By Capacity: Large Systems Capture Industrial Growth

The 5,001-15,000 m³/h tier accounts for 47.40% 2025 revenues, serving hospitals, higher-education and mixed-use developments. Yet units exceeding 15,000 m³/h expand at 9.25% CAGR driven by electrified process heat and district networks. The air handling units market size for >15,000 m³/h installations is supported by European industrial heat-pump projects totaling 23 GW potential, worth EUR 4.6-11.5 billion. MAN’s 20-33 MW CO₂ heat-pump illustrates momentum toward mega-scale AHUs integrated with thermal loops.

Smaller capacity units (<5,000 m³/h) stay relevant in premium residential towers where central treatment improves indoor air quality. Variable-speed EC fans and compact heat-recovery wheels help meet tight acoustical and spatial constraints, though market growth lags larger systems.

By Installation Type: Outdoor Systems Gain Momentum

Indoor mechanical-room placement dominates with 64.20% 2025 share, but rooftops grow 7.95% CAGR as developers seek rentable floor area. High-ambient designs for the GCC employ UV-resistant panels and 3 000-Pa static fans to cope with desert dust and long duct runs. Weatherized enclosures and service corridors allow maintenance without disrupting occupants. This shift reduces building-core complexity and aligns with fast-track construction schedules.

Outdoor preference also supports retrofit projects where interior space is limited. Pre-assembled penthouse units crane-lifted to the roof minimize business interruption and compress project timelines, enhancing the air handling units market appeal for commercial renovations.

By Technology: Heat Recovery Drives Efficiency

Heat-pipe wraps lower reheat loads by 32% against conventional coils heatpipe.com. Run-around coils achieve up to 80% recovery when air streams are segregated, as documented in TROX tests trox.de. Plate exchangers offer no-moving-parts reliability for public facilities with limited maintenance budgets. Desiccant wheels paired with heat pumps secure supply-air dewpoints below -15 °C and deliver paybacks under three years in food-processing plants.

Thermodynamic heat-pump AHUs exhibit the quickest adoption, especially in Europe’s electrification programs where units provide simultaneous cooling and 140 °F process water. Vendors integrate variable-speed compressors and microchannel condensers to elevate seasonal COPs beyond 4.0.

Geography Analysis

Asia-Pacific leads the air handling units market with 31.55% 2025 revenue. China’s 185 million-unit air-conditioner production base anchors the regional supply chain, while India’s HVAC spending trajectory toward USD 30 billion by 2030 at 15.8% CAGR boosts domestic AHU demand. Japan and South Korea advance retrofit activity through stringent IAQ revisions and successful underground-facility demonstrations that cut radon 98%. Local players collaborate with global OEMs to supply modular systems that satisfy diverse project timelines.

Europe’s mature regulatory environment accelerates technology turnover. The Ecodesign framework pushes heat-recovery effectiveness and digital product passports, enlarging the air handling units market share of high-efficiency models. Industrial heat-pump deployment from Scandinavia to Germany drives >15,000 m³/h unit demand. Suppliers navigate extended conformity assessments for A2L refrigerants, but eventual approvals unlock a replacement cycle across aging installations.

The Middle East records the fastest 9.02% CAGR thanks to mega-projects in Saudi Arabia, Qatar and the UAE. District-cooling networks specify desert-ready rooftop AHUs that thrive at 50 °C. Government visions prioritize sustainability, rewarding equipment that reduces peak electricity loads. Meanwhile North America faces raw-material surcharges and technician shortages, yet hyperscale data centers are ordering modular thermal-management systems in volumes unprecedented for the region. The air handling units market size linked to data-center build-outs is projected to expand at double-digit rates through 2031.

Competitive Landscape

The air handling units industry remains moderately fragmented. Global leaders such as Daikin, Carrier, Trane Technologies and Johnson Controls combine broad portfolios with geographic reach. Acquisition activity is high: Rheem’s parent bought Fujitsu’s HVAC arm for USD 1.6 billion, signaling consolidation toward integrated solutions. CSW Industrials acquired Aspen Manufacturing for USD 313.5 million to strengthen coil and AHU capabilities.

Technology competition centers on heat-pump integration, modular scalability and digital diagnostics. Daikin’s Trailblazer® heat-pump chiller and AAON’s low-ambient Alpha Class heat pumps illustrate differentiation through extreme-temperature performance. Partnerships with controls specialists enable predictive maintenance, minimizing downtime for mission-critical sites.

Niche manufacturers thrive by focusing on clean-room, high-ambient or deep-dehumidification niches. Barriers include certification costs for A2L refrigerants and the engineering heft needed to meet EU digital-passport requirements. Nonetheless, specialized expertise commands premium margins in pharma and semiconductor segments, influencing overall air handling units market dynamics.

Air Handling Units (AHU) Industry Leaders

-

Daikin Industries Ltd

-

Carrier Corporation

-

TRANE Inc. (Trane Technologies PLC)

-

Johnson Controls International PLC

-

Systemair AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Daikin Applied launched the Trailblazer® HP air-cooled scroll chiller utilizing heat pump technology for efficient heating and cooling in commercial and industrial settings, achieving up to 300% efficiency while reducing energy consumption and greenhouse gas emissions compared to traditional systems.

- June 2025: AAON introduced significant advancements to its Alpha Class line of commercial air-source heat pumps, featuring EXTREME Series with ultra-low-ambient performance down to -20°F while maintaining 100% heating capacity at 5°F, leveraging Copeland's variable-speed compressors and refrigerant injection technology.

- March 2025: CSW Industrials announced acquisition of Aspen Manufacturing for USD 313.5 million, enhancing its HVAC/R product portfolio with a leading manufacturer of evaporator coils and air handling units positioned to support the refrigerant transition with products compatible with both legacy and new refrigerants.

- March 2025: Trane Technologies introduced the Fan Coil Wall platform for data centers, offering tailored cooling solutions with 400 kW or greater cooling capacity, utilizing chilled water for cooling to promote lower operational costs and reduced carbon emissions.

Global Air Handling Units (AHU) Market Report Scope

An air handling unit (AHU), also called an air handler, is a piece of equipment used to condition and circulate air as a component of a heating, ventilating, and air conditioning system. It is usually a large metal box that comprises a blower, heating and cooling elements, filter chambers, sound attenuators, and dampers.

The air handling units (AHU) market is segmented by type (packaged, modular, custom), end user (residential, commercial, industrial), and geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Custom |

| Packaged |

| Modular |

| DX Integrated |

| Heat-Recovery Units |

| Less than 5,000 |

| 5,001 - 15,000 |

| Greater than 15,000 |

| Indoor |

| Outdoor / Rooftop |

| Heat-Pipe |

| Run-Around Coil |

| Plate Heat Exchanger |

| Desiccant-Based |

| Thermodynamic Heat Pump AHU |

| Comfort Ventilation |

| Process Ventilation and Dehumidification |

| Residential | |

| Commercial | Offices |

| Hospitality and Leisure | |

| Healthcare Facilities | |

| Educational Institutions | |

| Retail and Shopping Malls | |

| Industrial | Food and Beverage |

| Pharmaceuticals and Biotech | |

| Oil and Gas / Petrochemicals | |

| Automotive and Machinery | |

| Other Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Custom | |

| Packaged | ||

| Modular | ||

| DX Integrated | ||

| Heat-Recovery Units | ||

| By Capacity | Less than 5,000 | |

| 5,001 - 15,000 | ||

| Greater than 15,000 | ||

| By Installation Type | Indoor | |

| Outdoor / Rooftop | ||

| By Technology | Heat-Pipe | |

| Run-Around Coil | ||

| Plate Heat Exchanger | ||

| Desiccant-Based | ||

| Thermodynamic Heat Pump AHU | ||

| By Application | Comfort Ventilation | |

| Process Ventilation and Dehumidification | ||

| By End-user | Residential | |

| Commercial | Offices | |

| Hospitality and Leisure | ||

| Healthcare Facilities | ||

| Educational Institutions | ||

| Retail and Shopping Malls | ||

| Industrial | Food and Beverage | |

| Pharmaceuticals and Biotech | ||

| Oil and Gas / Petrochemicals | ||

| Automotive and Machinery | ||

| Other Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the air handling units market?

The air handling units market stands at USD 16.95 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to post a 6.01% CAGR, reaching USD 22.69 billion by 2031.

Which region leads global demand?

Asia-Pacific leads with 31.55% 2025 revenue, driven by China’s large HVAC manufacturing base.

Why are modular AHUs gaining popularity?

Hyperscale data centers require scalable, pre-engineered cooling blocks that modular designs provide, resulting in an 8.52% segment CAGR.

What are the main challenges facing manufacturers?

Volatile raw-material prices, skilled-labor shortages and lengthy refrigerant approval processes are key restraints.

How are regulations shaping future AHU designs?

The EU Ecodesign Regulation mandates lower fan power and ≥73% heat-recovery, pushing adoption of energy-recovery wheels and digital lifecycle passports.

Page last updated on: