Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

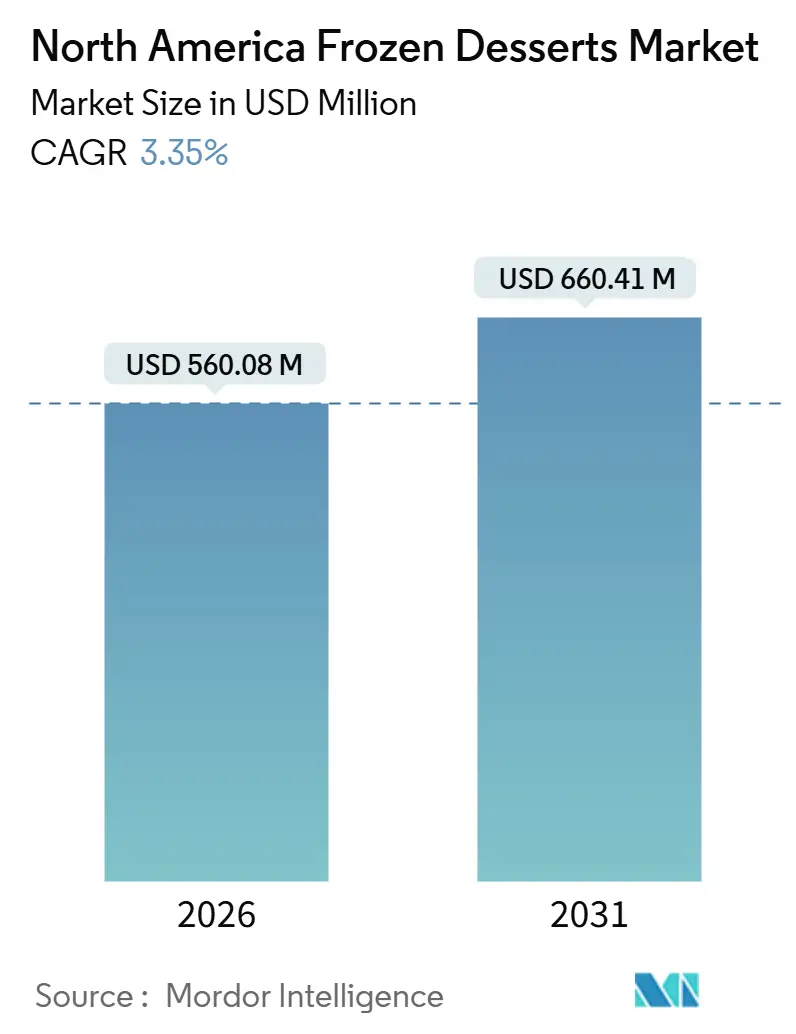

| Market Size (2026) | USD 560.08 Million |

| Market Size (2031) | USD 660.41 Million |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Frozen Desserts Market Analysis by Mordor Intelligence

The North America frozen dessert market size is USD 560.08 million in 2026 and is projected to reach USD 660.41 million in 2031, advancing at a 3.35% CAGR. Factors such as the growing popularity of single-serve options, rapid flavor innovations, and health-focused reformulations are driving demand, surpassing the influence of traditional brand equity. Non-dairy alternatives are outperforming dairy products, fueled by concerns over lactose intolerance and the increasing adoption of flexitarian diets. Additionally, precision-fermented proteins are delivering dairy-like textures while avoiding supply chain disruptions. Social media-driven aesthetics, particularly on Instagram, are reducing product life cycles, encouraging manufacturers to introduce limited-edition SKUs on a quarterly basis. Retailers are adapting to this trend by prioritizing premium pints over standard gallons in freezer-door placements, which helps achieve higher dollar velocities and addresses stagnation in mature U.S. metro markets.

Key Report Takeaways

- By product type, ice cream led with 65.41% of the North America frozen dessert market share in 2025, while gelato posted the fastest 4.25% CAGR through 2031.

- By category, dairy-based products accounted for 78.21% of 2025 revenue, yet non-dairy lines are expanding at a 4.17% CAGR to 2031.

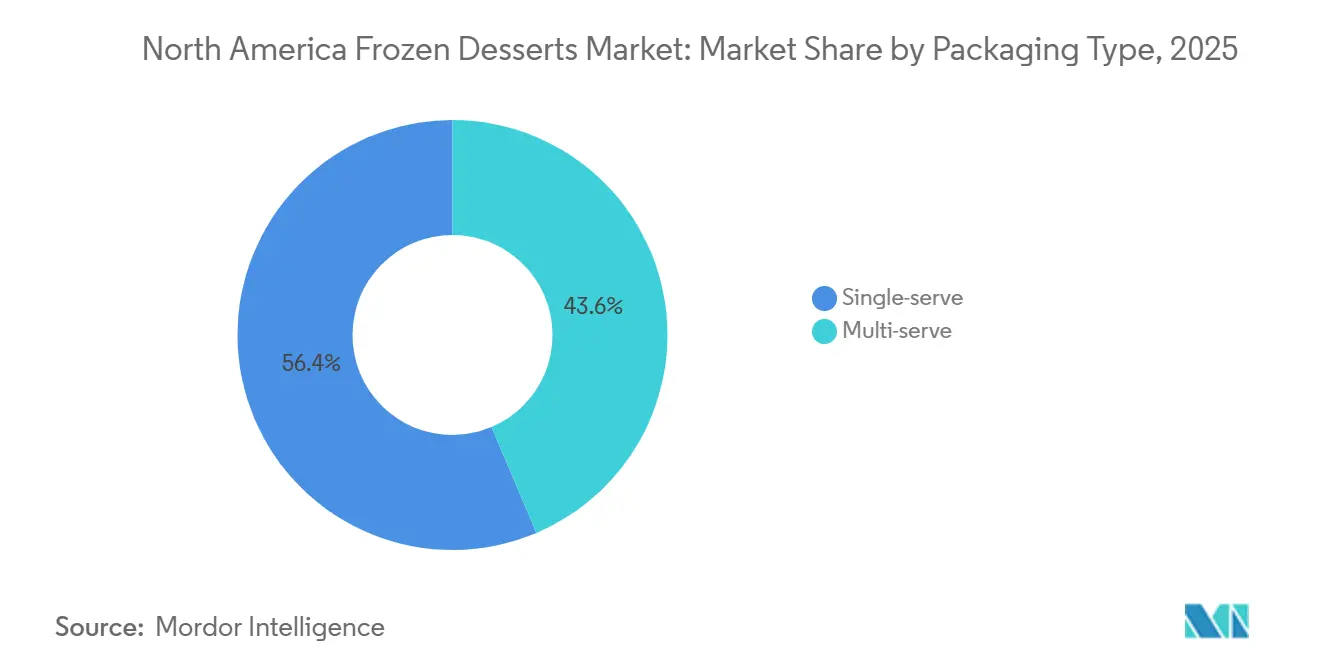

- By packaging type, single-serve formats commanded 56.38% share in 2025 and are growing at a 4.39% CAGR through 2031.

- By distribution channel, off-trade outlets held 97.51% share in 2025, whereas on-trade venues are advancing at a 4.87% CAGR.

- By country, the United States captured 83.76% of the 2025 value, but Mexico is the fastest-rising market with a 4.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Frozen Desserts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of ready-to-eat convenience | +0.6% | United States, Canada, urban Mexico | Short term (≤ 2 years) |

| Growth of premium and artisanal desserts | +0.7% | United States (coastal metros), Canada (Toronto, Vancouver) | Medium term (2-4 years) |

| Rising demand for healthier options (low-sugar, low-fat, plant-based) | +0.8% | North America-wide, strongest in US West Coast and Canada | Medium term (2-4 years) |

| Social media influence promoting visually appealing dessert trends | +0.5% | United States, Canada, Mexico (Gen Z and millennial cohorts) | Short term (≤ 2 years) |

| Premiumization in flavors and textures | +0.4% | United States, Canada | Long term (≥ 4 years) |

| Technological advances in freezing/packaging preserving quality | +0.3% | North America-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing popularity of ready-to-eat convenience

Consumers with busy lifestyles are driving a shift toward single-serve frozen desserts, which now account for over half of unit sales. This change has boosted sales in non-traditional outlets such as gas stations, airport kiosks, and workplace micro-markets, where impulse purchases often carry a 15-20% price premium compared to grocery stores. To meet this demand, manufacturers are introducing portion-controlled options, like mochi-wrapped ice cream, mini gelato cups, and dessert bars, that easily fit into car cupholders and desk drawers, eliminating the need for bowls or spoons. Urban retail is also evolving, with 24-hour convenience chains in cities like New York and Los Angeles now stocking 30-40 frozen dessert SKUs, a notable increase from the 10-15 available a decade ago. This growth enables spontaneous indulgence moments that traditional grocery shopping cannot replicate.

Growth of premium and artisanal desserts

Premiumization extends beyond higher price points to include product origin stories, meticulous small-batch production, and ingredient transparency. These elements often justify a 40-60% price premium over mass-market brands. With increasing disposable incomes, U.S. consumers are showing a preference for premium frozen desserts. According to the U.S. Bureau of Economic Analysis (BEA), the annual disposable personal income in the U.S. was USD 20,749.3 billion in 2023 and rose to USD 21,917.7 billion in 2024[1]Source: U.S. Bureau of Economic Analysis (BEA), "Annual total value of disposable personal income", bea.gov. Artisanal brands like Jeni's Splendid Ice Creams and Salt and Straw have built loyal followings by offering limited-edition flavors, such as brown butter almond brittle and honey lavender, that rotate quarterly, encouraging repeat visits to their scoop shops and online platforms. In 2024, Tillamook entered the super-premium gelato market, leveraging its Oregon dairy cooperative heritage. This move highlights how regional brands can scale their artisanal positioning while preserving their authentic farm-to-freezer identity. The segment has also attracted private equity interest; for example, Blue Bell's recovery after a 2015 recall demonstrated that brands emphasizing craftsmanship and local roots can retain customer loyalty despite operational challenges.

Rising demand for healthier options like low-sugar, low-fat, and plant-based desserts

As the prevalence of diabetes and chronic diseases rises, consumers are increasingly opting for healthier products. In 2024, the International Diabetes Federation reported that 15.7% of adults in the United States had diabetes[2]Source: International Diabetes Federation, "IDF Diabetes Atlas - Eleventh Edition (2025)", idf.org. Health-conscious reformulations are driving rapid growth in non-dairy alternatives, which cater to consumers seeking indulgence without lactose, cholesterol, or animal-derived ingredients. Oat-based ice creams, promoted by brands like Oatly and So Delicious, provide a creaminess similar to dairy while aligning with the environmental and wellness values that appeal to millennials and Gen Z. According to the US Census Bureau, millennials accounted for 21.81% and Gen Z for 20.81% of the U.S. population in 2024[3]Source: US Census Bureau, "Population and Housing Unit Estimates", census.gov. At the same time, precision fermentation is emerging as a transformative innovation. Perfect Day's animal-free whey proteins, developed through precision fermentation and licensed to brands like Coolhaus, replicate the texture and nutritional qualities of dairy without involving cows. This advancement reduces supply-chain uncertainties and methane emissions. In response to the FDA's 2024 updates on "healthy" claims, which limit added sugars to 2.5 grams per serving for front-of-pack endorsements, manufacturers are introducing low-sugar options sweetened with alternatives like allulose or monk fruit. Reflecting the industry's adaptability, Halo Top shifted its focus in 2025 from low-calorie offerings to high-protein positioning. This change highlights the industry's efforts to redefine "better-for-you" products by balancing taste, texture, and label claims while avoiding the health-halo backlash that previously affected diet ice creams.

Social media influence promoting visually appealing dessert trends

Instagram and TikTok now shape product development cycles, prompting manufacturers to release visually striking SKUs, such as swirled colors, edible glitter, and cookie-dough chunks. These products not only attract consumers but also drive user-generated content, equating to millions in organic advertising value. For example, Magnum's 2024 launch of ruby cacao ice cream bars, naturally pink due to cocoa compounds, highlights how visual appeal encourages trial among social-media-savvy consumers who often share dessert moments online before consumption. Retailers are leveraging this trend by designing "Instagrammable" freezer endcaps that showcase limited-edition flavors and seasonal collaborations, transforming foot traffic into digital engagement. This phenomenon is also pressuring legacy brands to update packaging and flavor profiles quarterly, reducing product life cycles and increasing research and development costs as speed-to-market becomes a critical competitive advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in dairy prices | -0.5% | United States, Canada (dairy-dependent manufacturers) | Short term (≤ 2 years) |

| Rising costs of premium/health-focused ingredients | -0.4% | North America-wide, acute in specialty and organic channels | Medium term (2-4 years) |

| Supply-chain risk for specialty plant ingredients | -0.3% | United States, Canada (non-dairy manufacturers) | Medium term (2-4 years) |

| Regulatory pressures on labeling, nutrition claims, and additives | -0.2% | United States (FDA jurisdiction), Canada (Health Canada oversight) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in dairy prices

From Q1 2024 to Q4 2025, Class II milk prices, critical for frozen dessert inputs, experienced an 18% fluctuation. This instability, caused by feed-cost inflation and herd-size adjustments, has created challenges for manufacturers bound by fixed retail pricing. According to data from the USDA Agricultural Marketing Service, dairy product inventories tightened by late 2024, driving up spot prices. Manufacturers responded by either reducing butterfat content in their products or substituting milk solids with less expensive starches. Vertically integrated companies such as Dairy Farmers of America and HP Hood have mitigated these impacts by controlling their upstream supply chains. However, this approach increases their market power, putting independent brands reliant on third-party co-packers at a disadvantage. Additionally, this volatility complicates long-term agreements with retailers. Retailers, unwilling to accommodate mid-year price increases, often delist SKUs that cannot absorb input cost fluctuations, accelerating the rationalization of product categories.

Rising costs of premium/health-focused ingredients

Brands focusing on clean labels and ethical sourcing face tighter margins as specialty inputs, such as organic cane sugar, fair-trade cocoa, grass-fed cream, and prebiotic fibers, carry premiums of 50-100% compared to conventional alternatives. At the same time, FDA-approved allulose, a low-calorie sweetener, is gaining popularity in keto-friendly products. Non-dairy ice creams made with cashew and macadamia bases are encountering supply challenges. With global cashew production concentrated in Vietnam and India, manufacturers are exposed to risks from monsoon variability and export tariffs. Similarly, freight costs for macadamia nuts sourced from Australia and South Africa can double their landed prices compared to domestic almonds. These issues force brands to either maintain ingredient integrity at the expense of margins or opt for cheaper substitutes, risking customer dissatisfaction. This trade-off is reflected in SKU expansions; for example, Halo Top's 2025 portfolio includes over 40 flavors, designed to cater to both price-sensitive and premium-seeking consumers, highlighting how cost pressures drive product diversification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gelato Gains on Texture Premiumization

Ice cream accounted for 65.41% of its projected 2025 value, maintaining its leadership in the North American frozen dessert market despite growth challenges. Gelato, known for its richer texture and premium appeal, is growing at a 4.25% CAGR, attracting consumers who associate lower overrun with artisanal quality. Sherbets and sorbets address the needs of lactose-intolerant consumers, while frozen novelties capitalize on convenience. Emerging options like kulfi and frozen custard are testing their regional popularity through ethnic grocers and food halls. Manufacturers are implementing Italian-style production techniques domestically to scale artisanal methods, improving unit economics while preserving authenticity.

Texture innovation continues to influence repeat purchases. Developments such as mochi-wrapped ice cream combine culturally significant formats with popular flavors, expanding experiential options. Breyers’ Sundae Swirls, which use advanced stabilizers to retain cookie inclusions, demonstrate how technical improvements can enhance mainstream products. Regulatory standards under 21 CFR Part 135 ensure consistent composition while allowing room for flavor innovation, fostering competitive experimentation. If current penetration levels persist, the North American gelato market could reach nearly half the size of the traditional ice cream market by 2031.

By Category: Non-Dairy Alternatives Disrupt Dairy Dominance

In 2025, dairy formulas generated 78.21% of total revenue, driven by ingrained taste preferences and cost efficiencies. Conversely, the non-dairy segment, with a 4.17% CAGR, reflects a shift influenced by environmental concerns and the growing prevalence of lactose intolerance. Oat milk addresses sensory gaps through its beta-glucan viscosity, while animal-free whey supports a carbon-conscious trend in North America's frozen dessert market. Traditional producers are countering with A2 milk and grass-fed claims to appeal to hesitant consumers.

Regarding consumer preferences, Baby Boomers continue to favor traditional dairy, while millennials and Gen Z increasingly adopt flexitarian diets, a trend amplified by social media. Unilever’s Magnum Non-Dairy, utilizing pea protein to maintain bite consistency, demonstrates that mainstream brands can meet plant-based expectations. Regulatory distinctions, such as “frozen dessert” versus “ice cream,” may restrict direct marketing claims but also emphasize product differentiation. If bioreactor costs decline, precision-fermented proteins could achieve price parity, further challenging dairy's market share.

By Packaging Type: Single-Serve Formats Capture On-the-Go Occasions

In 2025, single-serve units accounted for 56.38% of total turnover and are anticipated to grow at a 4.39% CAGR during the forecast period. These units are gaining traction due to their alignment with evolving consumer preferences for snacking, driven by features such as portion control, impulse appeal, and utensil-free convenience. The increasing availability of branded freezers in dollar stores and truck stops further supports this trend, validating Blue Bunny's strategy to expand its distribution routes. On the other hand, multi-serve tubs, traditionally favored for family pantries, are experiencing a decline in market share as household sizes continue to shrink, reducing the demand for larger packaging formats.

Sustainability is playing an increasingly significant role in shaping the packaging format landscape. Eco-conscious options, such as paper tubs and compostable wrappers, are gaining favor among premium buyers who are willing to pay higher prices for environmentally friendly solutions. This shift is further reinforced by regulatory developments, such as California's extended-producer responsibility laws, which are expected to accelerate the adoption of recyclable materials across the frozen dessert market in North America. Consequently, material innovation has emerged as a critical driver of value in packaging, alongside the convenience that consumers continue to prioritize.

By Distribution Channel: On-Trade Recovery Trails Off-Trade Dominance

In 2025, off-trade venues accounted for a significant 97.51% of the total revenue, driven by consistent weekly supermarket promotions and the widespread presence of convenience-store networks. This dominance highlights the strong consumer preference for purchasing frozen desserts through retail channels. On the other hand, the on-trade sector, with a compound annual growth rate (CAGR) of 4.87%, showcases a notable recovery in experiential dining as the market rebounds from the pandemic's impact. Branded scoop shops, such as Tillamook's newly launched locations in Portland and Seattle, play a pivotal role in enhancing brand storytelling while securing the full margin stack. Furthermore, foodservice bundles, like Nestlé's strategic placement of Häagen-Dazs products in Starbucks outlets, capitalize on shared customer traffic to drive increased retail demand.

Although direct-to-consumer (DTC) shipping currently represents less than 5% of the market, it is experiencing remarkable triple-digit growth. This expansion is facilitated by advancements in dry-ice logistics, which enable the delivery of artisanal pints to satisfy consumer cravings across the nation. Retailers are responding to this trend by co-listing popular DTC products, effectively blurring the lines between traditional sales channels and intensifying competition within the North American frozen dessert market.

Geography Analysis

In 2025, the United States leveraged its advanced cold-chain networks and a per-capita intake of 20 pounds to secure 83.76% of the market value. However, future growth is expected to depend on the introduction of premium product lines and health-focused variants. On the West Coast, non-dairy pints have captured a significant 15-18% share in specialty channels, prompting national players to accelerate the development and launch of plant-based product pipelines. Additionally, FDA labeling reforms are driving faster reformulations, which, in turn, are compressing project timelines and increasing research and development budgets to meet regulatory requirements.

Mexico is experiencing a steady growth trajectory with a 4.75% CAGR, supported by rising middle-class incomes and Walmart de México’s strategic expansion of freezer infrastructure across more than 2,500 stores. The extension of cold-chain networks into interior cities like León is enhancing consumer access to frozen desserts beyond the traditional coastal metropolitan areas. Popular domestic flavors such as tamarind, cajeta, and horchata are strengthening local brand loyalty. Simultaneously, U.S. manufacturers are establishing production facilities within Mexico to avoid 10-15% tariffs, ensuring their competitiveness in the North American frozen dessert market.

Canada’s frozen dessert market, which is approximately one-tenth the size of the U.S. market in value, faces pronounced seasonal variations, with 60-65% of sales occurring during the summer months. Compliance costs are rising due to bilingual packaging requirements and Health Canada’s expanded calorie-labeling regulations. In urban centers like Toronto and Vancouver, there is a growing demand for ethnic flavors such as mochi, ube, and kulfi, creating niche opportunities for premium growth. While cross-border sourcing remains a significant aspect of the market, increasing logistics costs could shift purchasing preferences toward domestic production facilities, particularly if renegotiations under the USMCA lead to changes in tariff structures.

Competitive Landscape

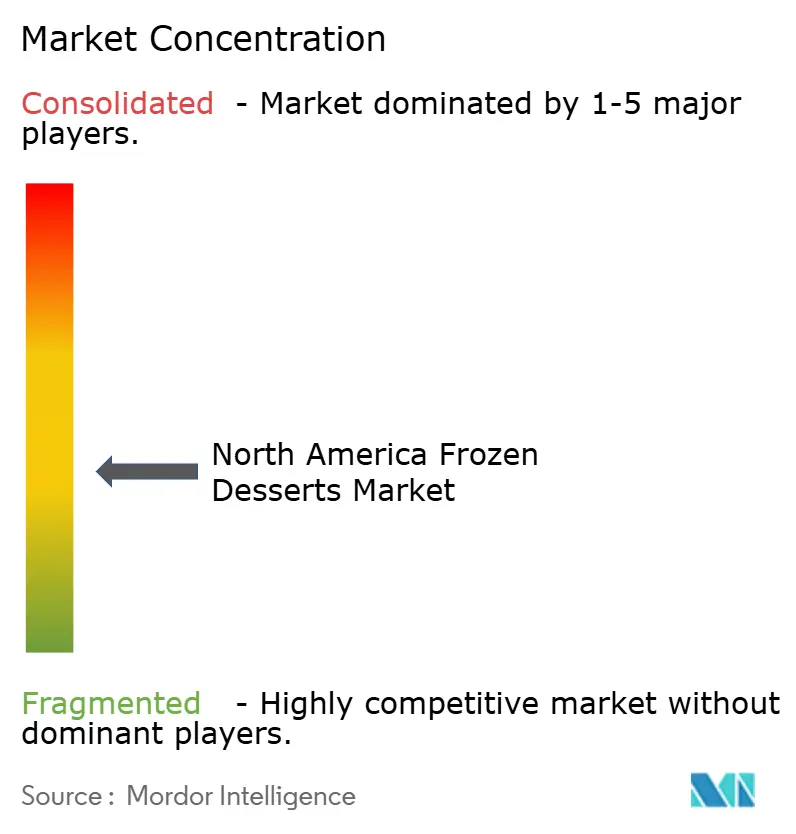

The North America frozen dessert market is moderately fragmented, with leading players such as Unilever Plc, Nestlé SA, General Mills Inc., Dairy Farmers of America Inc., and Froneri holding a significant share. These key companies utilize global research and development capabilities and extensive distribution networks to launch seasonal novelties and premium product lines. Meanwhile, regional cooperatives like Tillamook and Blue Bell focus on farm-origin narratives that appeal to local consumers. Innovation speed is critical; limited-edition releases and TikTok-friendly flavors are tested for digital appeal before broader rollouts.

The frozen dessert market in North America is defined by consistent product innovation and strategic expansion efforts by major players. Companies are prioritizing the development of healthier options, including low-calorie, sugar-free, and clean-label products, to align with evolving consumer demands. Operational flexibility is evident through investments in manufacturing upgrades, with firms enhancing facilities and adopting sustainable practices in production and packaging. Strategic initiatives often involve collaborations with online retailers and foodservice providers to strengthen distribution networks. Market leaders are expanding their footprint through acquisitions of regional companies and the establishment of new production facilities, while also investing in research and development to introduce unique flavors and formulations. Sustainability remains a key focus, with companies adopting eco-friendly packaging and implementing waste reduction strategies.

Disrupters are leveraging precision fermentation to produce dairy-like proteins without relying on cows, mitigating commodity price volatility and enhancing sustainability claims. AI-driven flavor modeling accelerates the transition from concept to shelf, while advanced flash-freezing technology maintains artisanal quality during nationwide shipping. Private-equity activity is on the rise, as demonstrated by Blue Marble's 2024 acquisition, highlighting the importance of scale efficiencies in cold-chain logistics and marketing. In this competitive environment, the North America frozen dessert industry rewards companies that successfully balance indulgence, health, and environmental sustainability while addressing regulatory challenges and ingredient cost pressures.

North America Frozen Desserts Industry Leaders

-

Dairy Farmers of America Inc.

-

Froneri International Limited

-

Unilever PLC

-

Nestlé SA

-

General Mills Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ben and Jerry's announced that it would introduce five new ice bar flavors. The new flavors included Cookie Dough, Chocolate Fudge Brownie, Strawberry Cheesecake, PB Pretzel, and Caramel Blondie, a swirl. The Ben and Jerry's Ice Cream Bars were expected to be available in the freezer aisle starting January 2026, offered in a four 2.5oz-bar multipack, priced between USD 5.99 and USD 7.49. Additionally, a single Cookie Dough Ben and Jerry's Ice Cream Bar was set to launch in convenience stores the following spring, priced at USD 3.99.

- October 2025: Wells Enterprises debuted Nutella Ice Cream and Kinder Bueno Frozen Dessert at the NACS Show in Chicago, held from October 14–17. The two new frozen treats, available in both pints and cones, were scheduled to begin shipping to convenience distributors on December 1, 2025, with broader retail distribution planned for spring 2026. Created to expand the frozen category, these offerings were expected to attract new shoppers, boost overall frozen dessert sales, and reinforce Wells' leadership in frozen innovation.

- August 2025: Frida, the parenting brand recognized for addressing postpartum topics directly, teamed up with OddFellows Ice Cream Co. to create a limited-edition breast milk-inspired flavor. The release coincided with National Breastfeeding Awareness Month and Frida’s launch of its 2-in-1 Manual Breast Pump, aiming to initiate conversations about early motherhood.

North America Frozen Desserts Market Report Scope

Off-Trade, On-Trade are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

Product Type

| Ice Cream |

| Gelato |

| Sherbets and Sorbets |

| Frozen Novelties |

| Others |

Category

| Dairy-based |

| Non-dairy based |

Packaging Type

| Single-serve |

| Multi-serve |

Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Ice Cream | |

| Gelato | ||

| Sherbets and Sorbets | ||

| Frozen Novelties | ||

| Others | ||

| Category | Dairy-based | |

| Non-dairy based | ||

| Packaging Type | Single-serve | |

| Multi-serve | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms