Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

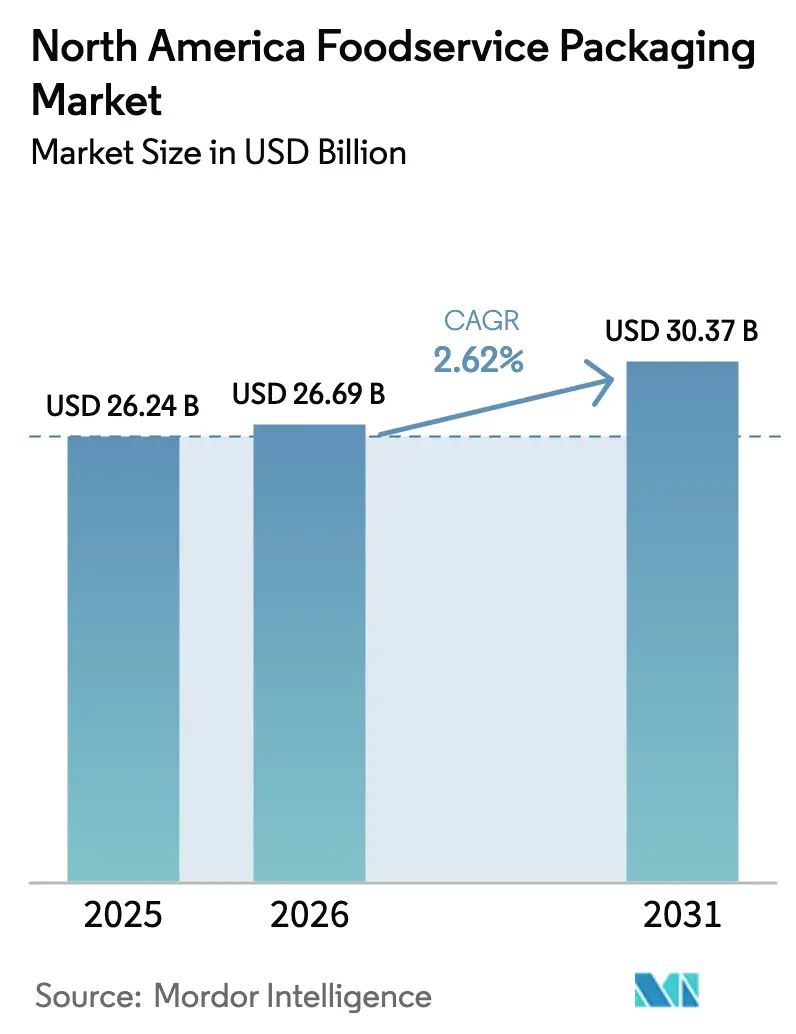

| Base Year Market Size (2025) | USD 26.24 Billion |

| Market Size (2026) | USD 26.69 Billion |

| Market Size (2031) | USD 30.37 Billion |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

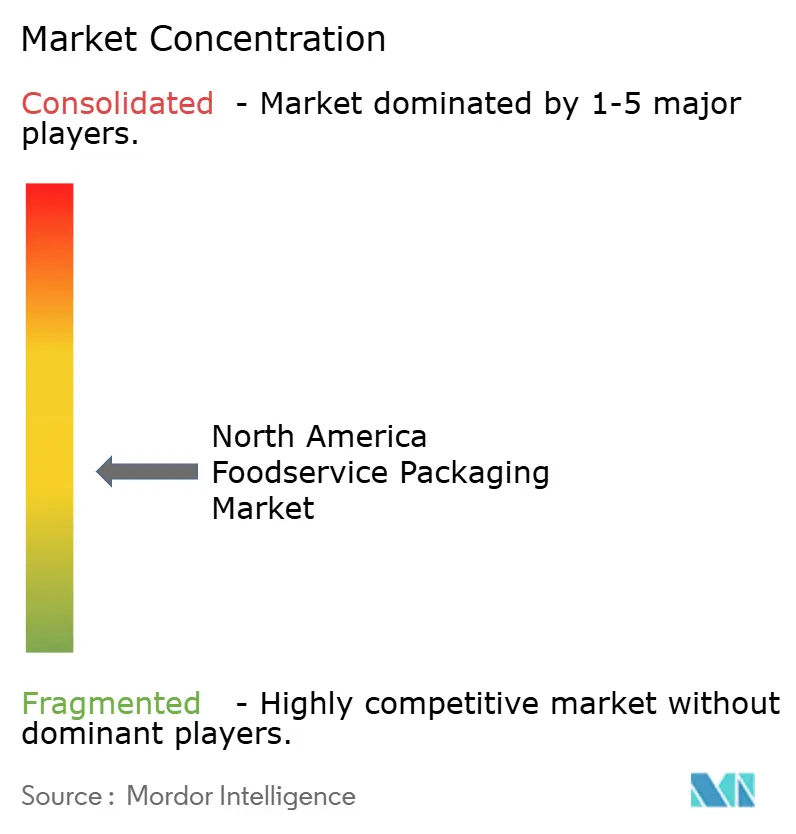

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Foodservice Packaging Market Analysis by Mordor Intelligence

The North America foodservice packaging market size is projected to expand from USD 26.24 billion in 2025 and USD 26.69 billion in 2026 to USD 30.37 billion by 2031, registering a CAGR of 2.62% between 2026 to 2031. A steady headline figure conceals the pivot toward fiber, recycled polymers, and smart labels as ghost kitchens, state-level PFAS bans, and corporate net-zero mandates reshape converter priorities. United States quick-service chains are setting recycled-content thresholds that ripple through resin demand, while California’s SB 54 is forcing multimaterial phase-outs ahead of 2032. Multinational food retailers now evaluate suppliers on Scope 3 metrics and time-temperature tracking, prompting capital flows into molded-fiber lines and digital label platforms. The net effect is a supply chain that is becoming shorter, more regional and more circular, even as it manages volatile polyethylene and polypropylene feedstock costs that spiked 20% through mid-2025.

Key Report Takeaways

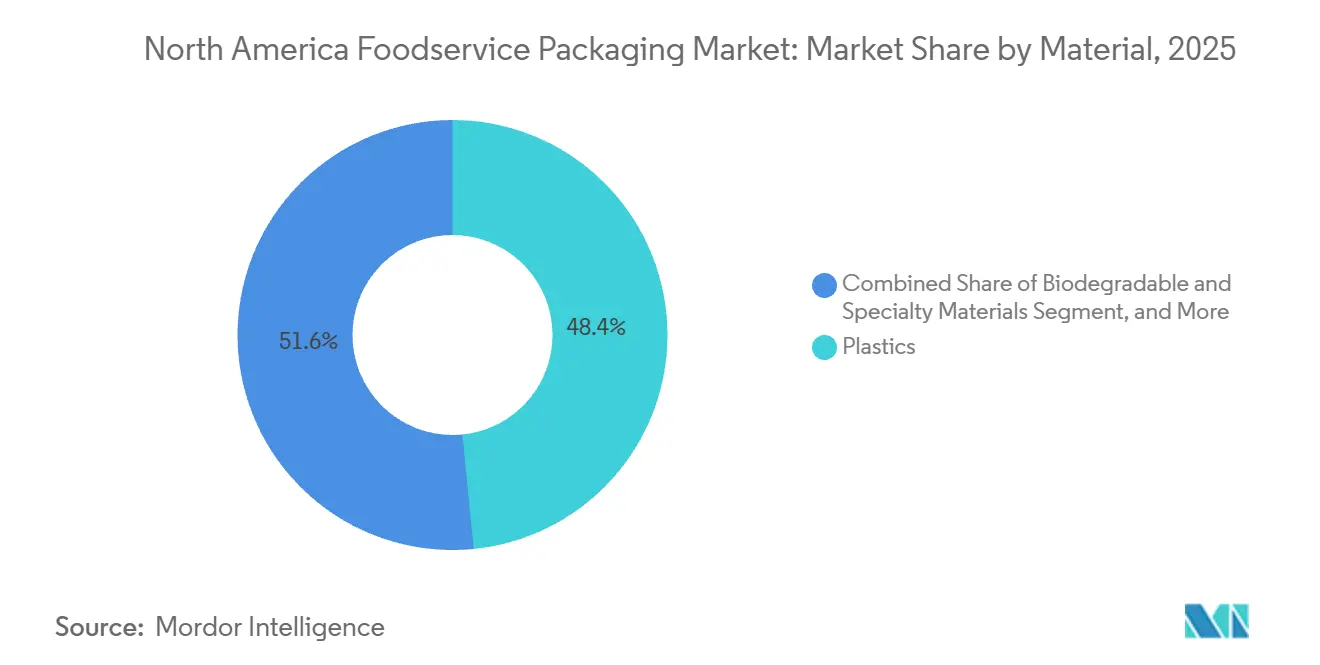

- By material, plastics led with 48.42% of the North America foodservice packaging market share in 2025, while biodegradable and specialty materials are forecast to grow at a 4.32% CAGR through 2031.

- By packaging type, cups and tubs commanded 39.89% revenue share in 2025, whereas trays and containers are projected to expand at a 3.46% CAGR to 2031.

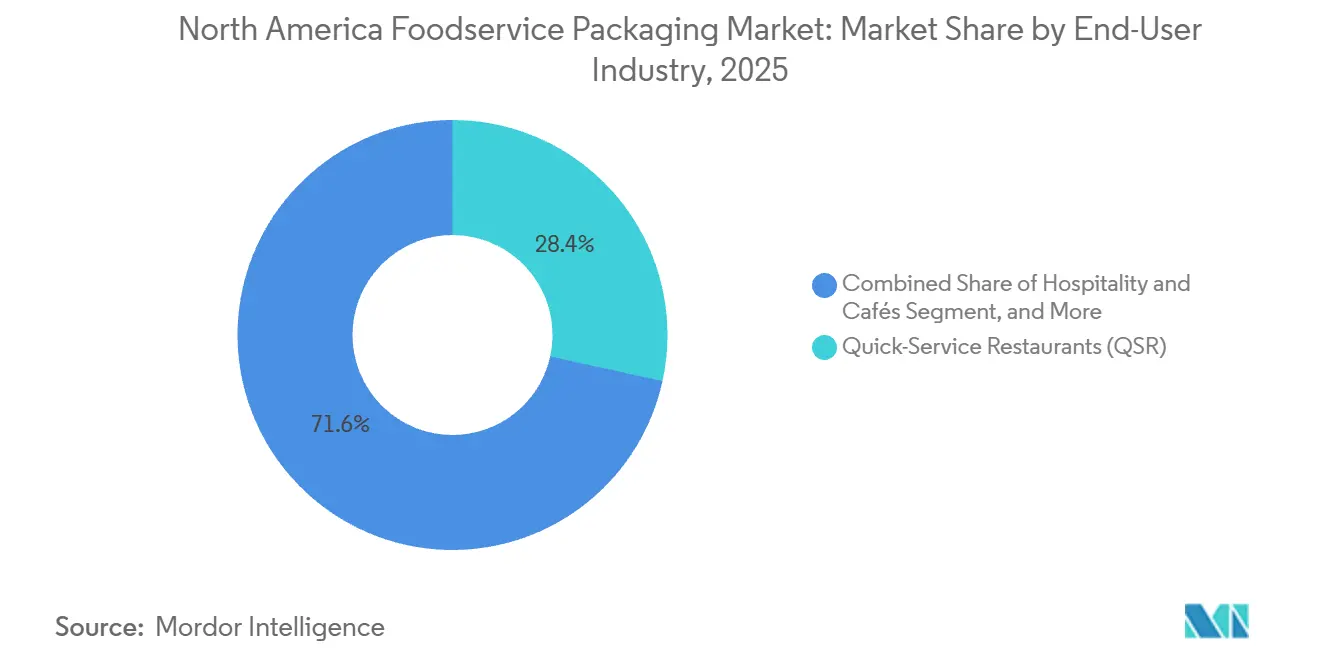

- By end-user, quick-service restaurants held 28.44% of the North America foodservice packaging market share in 2025, yet hospitality and cafés will post the fastest 3.74% CAGR between 2026 and 2031.

- By sustainability profile, conventional formats retained 68.86% share of the North America foodservice packaging market size in 2025, but sustainable alternatives will grow at a 3.61% CAGR through 2031.

- The United States accounted for 72.63% of 2025 revenue, while Mexico is set to log the highest 4.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Foodservice Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Convenience and On-the-Go Meals | +0.8% | United States and Canada, spillover to Mexico urban centers | Short term (≤ 2 years) |

| Rapid Expansion of Food-Delivery and Ghost-Kitchen Models | +0.7% | United States metro areas, Toronto, Vancouver, Mexico City | Medium term (2-4 years) |

| Corporate Net-Zero Mandates Driving Sustainable Packaging Procurement | +0.5% | United States and Canada, early adoption in Mexico by multinationals | Long term (≥ 4 years) |

| Emphasis on Recyclable and Post-Consumer Materials | +0.4% | United States and Canada, limited near-term impact in Mexico | Medium term (2-4 years) |

| Integration of Smart, Connected Packaging for Waste-Tracking | +0.3% | United States and Canada pilot programs, minimal Mexico penetration | Long term (≥ 4 years) |

| Government Incentives for Domestic Compostable Packaging Capacity | +0.2% | United States West Coast, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Convenience and On-the-Go Meals

Food-away-from-home spending climbed to 55% of total United States food expenditures in 2025, underlining a structural move toward portable meal formats.[1]U.S. Bureau of Labor Statistics, “Consumer Expenditures Report 2025,” U.S. Department of Labor, bls.gov Single-serve clamshells and dual-ovenable paperboard trays now dominate breakfast sandwich and entrée offerings because they let commuters reheat food without re-plating.[2]U.S. Food and Drug Administration, “Food Contact Substances: Guidance for Industry,” fda.gov Quick-service chains report that menu simplification lowered fulfillment labor by 12% to 15% and raised average order speed, reinforcing the pull for standardized footprints. Converters, in turn, are scaling up water-based barriers that comply with updated migration rules, reducing dependence on fluorochemicals. The convenience theme also dovetails with ghost-kitchen playbooks where SKU discipline and lightweight packaging lower delivery fees, sustaining volume even when food inflation pressures discretionary spending.

Rapid Expansion of Food-Delivery and Ghost-Kitchen Models

More than two-thirds of DoorDash North America orders in 2025 traveled more than 4 miles, so converters redesigned lids and seals to withstand 30-minute trips without leakage. Ghost kitchens already represent 15% of United States commercial foodservice orders, with penetration rising fastest in secondary metros where rents favor commissary hubs.[3]Graphic Packaging Holding Company, “2025 Annual Report,” graphicpkg.com Delivery-optimized trays made from mono-PP or molded fiber now earn price premiums because they reduce contamination at material recovery facilities. Graphic Packaging recorded a 22% year-over-year jump in tray shipments linked to virtual-brand contracts, confirming that durability and stackability trump dine-in aesthetics. Municipal recycling rules amplify the trend, since single-material walls flow more easily into existing streams, supporting circular-economy scorecards for brand owners.

Corporate Net-Zero Mandates Driving Sustainable Packaging Procurement

Packaging now accounts for 8% of Starbucks’ global greenhouse gas inventory, prompting the chain to mandate 30% recycled content in cups and lids by 2027. McDonald’s has already met its 2025 goal of sourcing guest packaging entirely from renewable, recycled, or certified inputs in the United States and Canada. These brand mandates cascade through tier-two converters, pushing investment into advanced mechanical and chemical recycling that yields food-grade rPET pellets. The Ellen MacArthur Foundation reports that 65% of regional signatories hit 2025 recycled-content goals, yet only 40% achieved reusability targets, showing that infrastructure gaps still hamper circular ambitions. Nonetheless, chain-of-custody certifications such as Forest Stewardship Council are now procurement prerequisites, tilting the share toward vertically integrated suppliers.

Emphasis on Recyclable and Post-Consumer Materials

California’s SB 54 requires 30% recycled content in PET single-use items by 2028, spurring a USD 150 million Amcor investment in molecular recycling assets capable of handling multilayer waste streams. Berry Global reports a 15% price premium for rPET clamshells but still sees robust foodservice uptake because procurement scorecards weigh recycled content at 30%. Feedstock scarcity remains the pinch point, with PET collection rates stuck at 28% in 2025. Converters are responding by signing long-term bale supply contracts and co-investing with material recovery facilities. The regulatory push is slowly narrowing cost gaps, so post-consumer materials are expected to command more than one-quarter of the North America foodservice packaging market by 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Single-Use Plastic Regulations and Bans | -0.6% | United States West and Northeast, federal Canada | Short term (≤ 2 years) |

| Volatility in Polymer and Pulp Input Prices | -0.5% | United States, Canada, import-dependent Mexico | Short term (≤ 2 years) |

| Limited Industrial Composting Infrastructure | -0.3% | United States and Canada, minimal Mexico infrastructure | Medium term (2-4 years) |

| Supplier Consolidation Triggering Contract Renegotiation Risk | -0.2% | United States and Canada | Short term (≤ 2 years) |

| Operational Challenges from State-Level PFAS Restrictions | -0.4% | Twelve United States states with enacted or pending legislation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Single-Use Plastic Regulations and Bans

California, Colorado, Maine, Vermont, and Washington already restrict polystyrene or require source reduction, while Canada’s federal ban took effect in 2023. The overlapping timelines force converters to manage multiple SKUs and create inventory write-down risks; Dart Container booked a USD 42 million impairment on legacy polystyrene tooling in 2024. Compliance costs are asymmetric; vertically integrated suppliers absorb testing and reformulation more easily than regional firms that rely on third-party compounders. Retailers are accelerating phase-outs ahead of statutory deadlines to avoid consumer backlash. As a result, molded-fiber, mono-PET, and coated paperboard alternatives are gaining accelerated certifications, shrinking the addressable volume for traditional foam cups.

Volatility in Polymer and Pulp Input Prices

United States polyethylene spot prices ranged from USD 0.52 to USD 0.71 per pound in 2025, mirroring Gulf Coast cracker outages and global naphtha volatility. Parallel pulp spikes saw northern bleached softwood kraft touch USD 1,450 per metric ton, pressuring coated-paperboard margins. Pactiv Evergreen hedged 60% of its resin purchases, yet still reported a 180-basis-point erosion in gross margin. Smaller converters without forward contracts delayed capital outlays for recycled-content extrusion lines, slowing the rollout of sustainable SKUs. The volatility curbs lenders' risk appetite, making supply chain finance a new battleground for market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Fiber Advances as Polymer Scrutiny Rises

Fiber, biodegradable resin and specialty substrate suppliers are converting regulatory headwinds into share gains. Biodegradable materials are set to register a 4.32% CAGR through 2031 as operators search for SB 54-compliant alternatives. Plastics still account for 48.42% of 2025 revenue, but California and Canada bans have already trimmed polystyrene volumes. Graphic Packaging’s molded-fiber clamshell wins in quick-service salad channels demonstrate how improved grease resistance and stiffness close historical performance gaps. Meanwhile, aluminum and glass stay niche in premium beverage formats because weight, cost and curbside sortation challenges offset their infinitely recyclable value proposition.

NatureWorks’ USD 600 million Nebraska PLA expansion will double capacity by 2027 and raise heat performance to 110 °C, unlocking hot-fill foodservice opportunities. Danimer Scientific secured FDA approval for Nodax PHA grease-barrier coatings, opening new avenues for fiber trays that bypass PFAS fluorochemicals. Still, the North America foodservice packaging market size for certified compostables hinges on end-of-life access; only 185 industrial composters accept foodservice ware in the United States. Operators outside the West Coast often default to landfill, diluting environmental claims. Until curbside organics pickup expands, converters are positioning compostables for coastal metros while pushing rPET and rPP upgrades elsewhere.

By Packaging Type: Delivery Needs Accelerate Tray and Container Demand

Cups and tubs captured 39.89% of the market share in 2025, buoyed by coffee and frozen-dessert chains. Yet the delivery boom is steering incremental growth toward trays and containers, which are expected to outpace the overall North America foodservice packaging market at a 3.46% CAGR through 2031. Inline Plastics’ tamper-evident clamshells meet FDA traceability mandates and now anchor meal-kit SKUs. Sachets and pouches gain in condiment and sauce applications because lighter packages lower freight emissions and unit cost.

Pactiv Evergreen’s EarthChoice dual-ovenable paperboard tray withstands 425 °F for 20 minutes, letting consumers reheat meals without secondary dishes and cutting per-order packaging weight 18% at Chipotle. Sabert’s sugarcane-bagasse Pulp-it line meets ASTM D6868 and rivals polystyrene on insulating performance, winning chain accounts in legislation-heavy states. California’s SB 1335 requirement that public institutions use compostable or recyclable formats by 2028 further tilts the mix to mono-fiber and mono-PP tray designs.

By End-User Industry: Hospitality and Cafés Lead Growth

Quick-service restaurants maintained a 28.44% share in 2025 thanks to their extensive store networks, but incremental momentum is shifting toward hospitality, cafés, and airport concessions, which will log a 3.74% CAGR through 2031. Full-service restaurants are adding off-premise channels, sending plated entrées into clamshells engineered to hold sauces and garnishes intact for 30-minute drives. Institutional catering pivots to single-use trays amid chronic labor shortages in dishwashing, though K-12 sustainable procurement dampens conventional plastic volumes.

Marriott reports that 92% of its North America properties swapped buffet chafers for individually wrapped breakfast items in 2025, boosting unit demand for compostable wraps and lids. Hilton’s contract with Eco-Products standardized compostable cups and cutlery across 1,200 hotels, signaling readiness to absorb an 8% price premium for certified materials. Starbucks’ Seattle reusable-cup pilot achieved a 45% return rate, yet high reverse-logistics costs limit national rollout, keeping single-use cups core to volume over the forecast period.

By Sustainability Profile: Conventional Formats Persist as Transitional Baseline

Conventional packaging retained 68.86% share of the 2025 North America foodservice packaging market size, anchored by virgin-plastic clamshells and polystyrene foam cups that meet low-price thresholds. However, sustainable alternatives are on a steeper 3.61% CAGR trajectory, supported by corporate ESG scorecards and state bans. McDonald’s fulfillment of its 2025 renewable or recycled mandate shows that scale chains can absorb higher material costs when reputational risk is on the line.

California SB 54 and Colorado HB 22-1162 will effectively eliminate unrecyclable polystyrene by 2032, creating stranded assets for lagging converters. The Foodservice Packaging Institute notes that only 38% of municipalities accept fiber clamshells curbside, constraining true circularity. As material recovery facilities retrofit sort lines and chemical recyclers scale, sustainable share is poised to approach one third of market revenue by the end of the decade, but conventional formats will still dominate price-sensitive QSR combo meals in the interior United States.

Geography Analysis

The United States generated 72.63% of the North America foodservice packaging market in 2025, driven by the world’s largest quick-service store base and early delivery-aggregator adoption. State regulations dictate material roadmaps; California SB 54 accelerates fiber migration, while Midwest operators cling to economical polypropylene in the absence of bans. The FDA traceability rule that took effect in January 2026 compels labels with lot codes and QR links, and Novolex now embeds track-and-trace on 60% of its domestic output.

Mexico will be the region’s growth engine, posting a 4.01% CAGR between 2026 and 2031 as rising disposable income lifts dining-out frequency in Monterrey, Guadalajara and Puebla. Starbucks intends to add 150 stores by 2027, each subject to global recycled-content standards that tilt procurement toward fiber lids and rPET cups. McDonald’s Mexico already sources 78% of guest packaging from fiber, double the 2023 level, underscoring how multinational mandates leapfrog local regulation. Yet only 12% of Mexico’s municipal solid waste was recycled in 2024, so most fiber and PLA items still head to landfill.

Canada delivered roughly 15% to 18% of regional sales in 2025. The federal single-use plastics ban removed polystyrene and PVC takeout containers from the market, and British Columbia’s extended producer responsibility rules push converters to shoulder downstream disposal costs, spurring lightweighting. Tim Hortons’ partnership with Huhtamaki will roll fiber hot-drink cups across 4,000 stores by mid-2026, a shift that further reduces polyethylene-lined cup demand and opens incremental molded-fiber capacity. The Canadian Plastics Pact shows 55% of signatories met 2025 recycled-content targets, suggesting gradual but steady progress toward a national circular-economy framework.

Competitive Landscape

The North America foodservice packaging market remains moderately fragmented with players such as Novolex, Huhtamaki, Dart Container, Genpak, Pactiv Evergreen, and others. Consolidation continued as Novolex purchased Flexo Universal and Waddington to deepen its fiber and rigid-plastic range, while the USD 11.2 billion Smurfit WestRock merger created a vertically integrated pulp-to-packaging platform. Buyers such as Compass Group cite 220-basis-point operating margin erosion, partly linked to supplier consolidation, confirming rising procurement leverage for top converters.

Technology capability is emerging as a differentiator. Amcor’s US 11,234,567 patent covers QR-encoded labels that upload carbon data to a blockchain ledger, letting restaurants verify recycled-content claims in real time. Smaller entrants deliver niche value; DeliverZero and Muuse pilot reusable-container deposit loops in New York and San Francisco, but low consumer return rates keep scale uncertain. The FDA updated its bio-based coating guidance in December 2025, removing ambiguities around migration limits and unlocking accelerated R&D for fluorine-free barriers.

Vertical integration into recycling offers insulation from resin volatility. International Paper and Sustana Fiber will open a Michigan plant that processes 100,000 metric tons per year of post-consumer cups into pulp for the EverGreen line, giving the joint venture captive feedstock and a circularity narrative attractive to chain accounts. Sonoco’s USD 75 million pulper upgrade in Connecticut aims for 60% recycled fiber input, signaling that pulp security is just as critical as resin hedging in the decade ahead.

North America Foodservice Packaging Industry Leaders

Novolex Holdings LLC

Huhtamaki Oyj

Dart Container Corporation

Genpak LLC

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Huhtamaki announced a USD 120 million expansion in Waterville, Maine, adding molded-fiber lines that will yield 500 million compostable trays each year upon Q4 2027 completion.

- January 2026: Pactiv Evergreen closed its USD 285 million acquisition of Sabert’s North America foodservice division, gaining sugarcane-bagasse and injection-molded polypropylene capabilities.

- December 2025: Graphic Packaging launched FiberGuard dual-ovenable paperboard trays, engineered for 425 °F reheating to target meal-kit and ghost-kitchen segments.

- November 2025: Amcor formed a supply agreement with Eastman Chemical for 50,000 metric tons of molecularly recycled Cristal polyester annually starting Jan 2026.

North America Foodservice Packaging Market Report Scope

The study on the North American foodservice packaging market showcases demand for significant packaging formats, including corrugated boxes and cartons, plastic bottles, trays, plates, bowls, cups and lids, clamshells, cutlery, and stirrers, as well as the corresponding industry verticals and revenue derived from the sales of packaging products across various geographies.

The North America Foodservice Packaging Market Report is Segmented by Material (Paper and Paperboard, Plastics, Aluminum, Glass, and Biodegradable and Specialty Materials), Packaging Type (Clamshells, Cups and Tubs, Trays and Containers, Sachets and Pouches, and Other Packaging Types), End-User Industry (QSR, FSR, Institutional Catering, Hospitality and Cafés, and Other End-User Industries), Sustainability Profile (Conventional, and Sustainable), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Paper and Paperboard | |

| Plastics | Polyethylene Terephthalate (PET) |

| Polypropylene (PP) | |

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |

| Other Plastics | |

| Aluminum | |

| Glass | |

| Biodegradable and Specialty Materials |

By Packaging Type

| Clamshells |

| Cups and Tubs |

| Trays and Containers |

| Sachets and Pouches |

| Other Packaging Types |

By End-User Industry

| Quick-Service Restaurants (QSR) |

| Full-Service Restaurants (FSR) |

| Institutional Catering |

| Hospitality and Cafés |

| Other End-User Industries |

By Sustainability Profile

| Conventional Type |

| Sustainable Packaging |

By Country

| United States |

| Canada |

| Mexico |

| By Material | Paper and Paperboard | |

| Plastics | Polyethylene Terephthalate (PET) | |

| Polypropylene (PP) | ||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||

| Other Plastics | ||

| Aluminum | ||

| Glass | ||

| Biodegradable and Specialty Materials | ||

| By Packaging Type | Clamshells | |

| Cups and Tubs | ||

| Trays and Containers | ||

| Sachets and Pouches | ||

| Other Packaging Types | ||

| By End-User Industry | Quick-Service Restaurants (QSR) | |

| Full-Service Restaurants (FSR) | ||

| Institutional Catering | ||

| Hospitality and Cafés | ||

| Other End-User Industries | ||

| By Sustainability Profile | Conventional Type | |

| Sustainable Packaging | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current value of the North America foodservice packaging market?

The market stands at USD 26.69 billion in 2026 and is projected to reach USD 30.37 billion by 2031.

Which segment is growing fastest within this market?

Biodegradable and specialty materials lead with a 4.32% CAGR forecast between 2026 and 2031.

How are single-use plastic bans affecting material choices?

State and federal bans are accelerating shifts toward molded fiber, rPET and compostable resins, especially in California and Canada.

Why is Mexico expected to grow faster than the United States and Canada?

Rising middle-class incomes, expanding quick-service chains and urbanization are driving a 4.01% CAGR through 2031 despite limited recycling infrastructure.

What technologies are converters adopting to stay competitive?

Companies are embedding QR-coded smart labels for traceability, installing advanced recycling lines for food-grade PCR and investing in dual-ovenable fiber trays.

Page last updated on: