Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

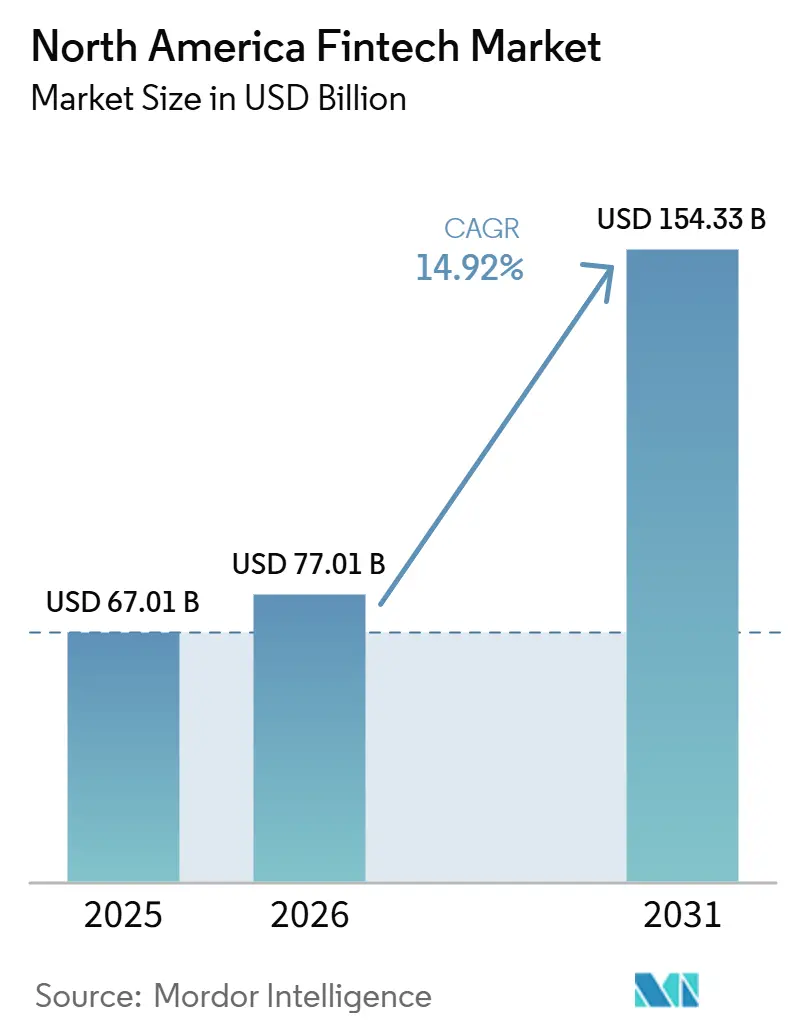

| Base Year Market Size (2025) | USD 67.01 Billion |

| Market Size (2026) | USD 77.01 Billion |

| Market Size (2031) | USD 154.33 Billion |

| Growth Rate (2026 - 2031) | 14.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fintech Market Analysis by Mordor Intelligence

The North America Fintech Market size is projected to be USD 67.01 billion in 2025, USD 77.01 billion in 2026, and reach USD 154.33 billion by 2031, growing at a CAGR of 14.92% from 2026 to 2031.

Real-time payment rails, consolidation around regulatory compliance, and broad deployment of generative AI are simultaneously expanding addressable revenue pools and compressing cost structures. FedNow’s connection to more than 900 U.S. financial institutions has accelerated instant settlement adoption, while Consumer Financial Protection Bureau (CFPB) rulemaking is encouraging scale-driven mergers among nonbank operators able to amortize supervision costs. Digital wallets anchored to card funding remain the channel of choice for everyday payments, and neobanks are capturing a growing share of younger households by keeping customer acquisition costs below USD 25 per account. Small-business demand for software-embedded payments, gains in fraud-orchestration accuracy, and early pilots of tokenized deposits are further propelling the North America fintech market toward double-digit growth through the decade.

Key Report Takeaways

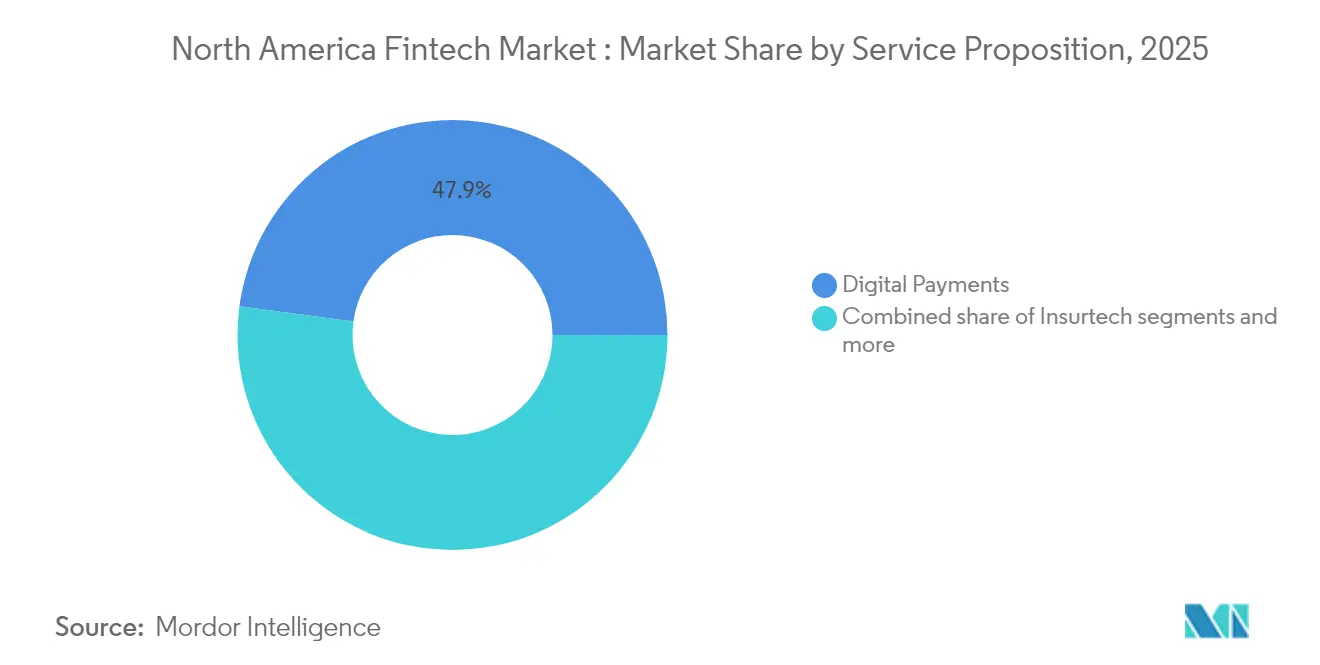

- By service proposition, digital payments captured 47.86% of the North America fintech market share in 2025, while neobanking is forecast to grow fastest at a CAGR of 21.95% between 2026 and 2031.

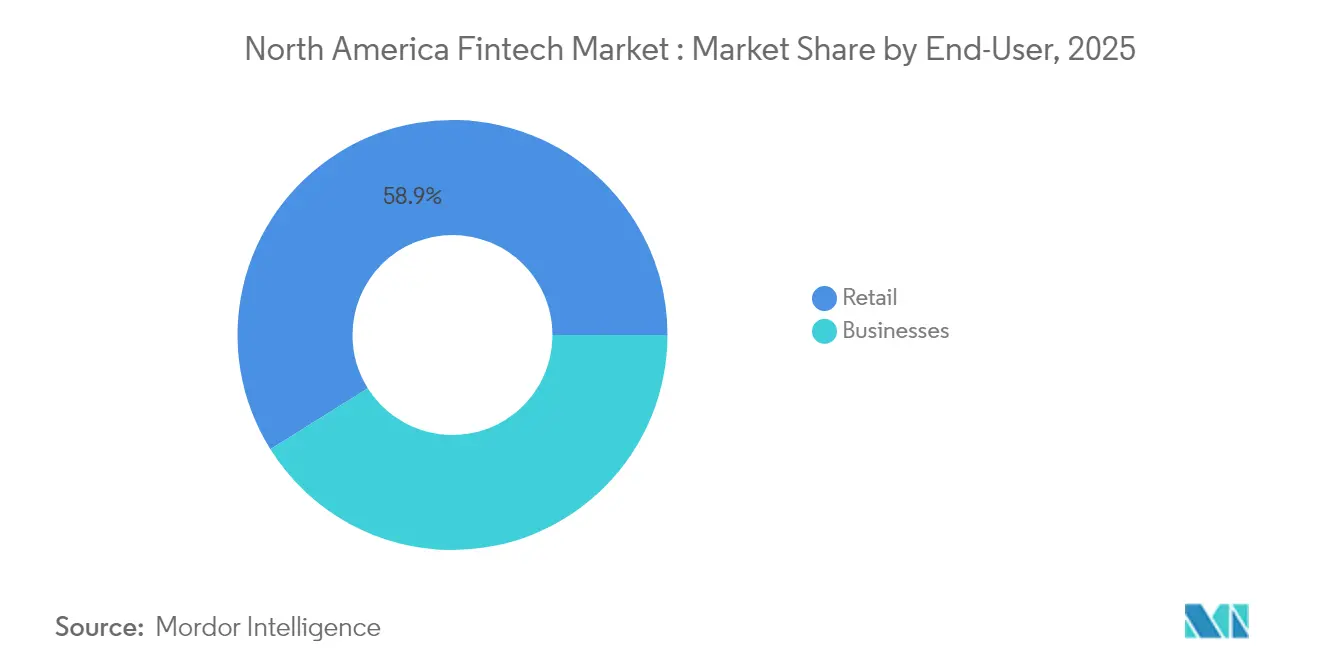

- By end-user, retail accounted for 58.92% of the North America fintech market share in 2025, with business users expected to expand at a growth rate of 17.74% CAGR during 2026–2031.

- By user interface, mobile apps represented 63.61% of the North America fintech market share in 2025, while POS/IoT devices are projected to rise at a 19.6% CAGR through 2031.

- By geography, the United States led with 72.05% of the North American fintech market share in 2025, while Mexico is anticipated to grow at the fastest rate of 16.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| P2P and card-funded digital-wallet dominance | +3.2% | United States, Canada | Medium term (2-4 years) |

| SME uptake of integrated POS/ISV suites | +2.8% | United States, Canada | Short term (≤ 2 years) |

| Bank–fintech BaaS/API partnerships | +2.5% | Region-wide | Medium term (2-4 years) |

| FedNow and other real-time rail monetization | +1.9% | United States, Canada | Long term (≥ 4 years) |

| AI-based fraud-orchestration savings | +2.1% | Region-wide | Short term (≤ 2 years) |

| Tokenized deposits and programmable money pilots | +1.4% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

P2P and Card-Funded Digital-Wallet Dominance

Card-backed wallets such as Apple Pay, PayPal, and Cash App processed more than USD 1.7 trillion in combined volume during 2024, illustrating the scale advantage gained by remaining inside established card networks. Consumers continue to prefer wallets that keep existing credit lines intact, and Venmo’s quarterly throughput climbed 10% to USD 75.6 billion, reinforcing the stickiness of P2P ecosystems. FedNow’s request-to-pay functionality is expected to open complementary revenue streams for wallet providers that overlay value-added messaging and invoice services. At the same time, a January 2025 CFPB rule brings nonbank payment apps handling more than 50 million annual transactions under direct federal examination, raising the fixed-cost bar for smaller entrants.

SME Uptake of Integrated POS/ISV Suites

Small merchants are turning to software-embedded payments that consolidate ordering, loyalty, payroll, and lending. Toast derived 87% of its 2024 top line from payments, hardware, and ancillary financial services rather than license fees, revealing the monetization power of bundled offerings. Community banks acknowledge that losing the merchant cash-management relationship threatens low-cost core deposits, and several have begun white-labeling point-of-sale fintech products to defend share. Market observers expect the embedded-finance revenue pool to grow from USD 185 billion in 2024 to USD 228 billion in 2028, implying a North America fintech market expansion path that rewards vertically integrated players.

Bank–Fintech BaaS/API Partnerships

The Banking-as-a-Service revenue opportunity is moving from proofs of concept toward scaled production, with the regional BaaS market anticipated to reach USD 66 billion by 2030[1]Cole Gottlieb, “PayPal Partners With Fiserv; C&R Acquires SpringFour,” Cross River, crossriver.com. . Fintechs gain speed to market, while chartered institutions unlock fee income from excess compliance capacity. The 2024 failure of middleware provider Synapse exposed operational gaps and accelerated FDIC plans to require daily reconciliation of for-benefit-of accounts, putting a premium on robust data pipelines. PayPal’s program with Fiserv to embed “Fastlane” guest checkout inside bank merchant portals demonstrates how BaaS can extend distribution without direct consumer acquisition costs.

AI-Based Fraud-Orchestration Savings

Deploying machine learning across transaction monitoring has cut fraud write-offs by 50% for early adopters while trimming manual reviews 60%. The Federal Trade Commission tallied USD 8.8 billion in U.S. consumer scam losses in 2024, underscoring the addressable problem set[2]Federal Trade Commission, “Consumer Sentinel Network Data Book 2024,” ftc.gov.. PayPal reports that its AI models now score 1,000 transactions per second and save more than 1 million annual customer hours previously spent resolving false positives. The growing wage premium for GenAI engineers, however, could drag implementation timelines for smaller wallets and processors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying CFPB and state compliance costs | −2.3% | United States | Short term (≤ 2 years) |

| Rising cyber-insurance premiums post-ransomware | −1.8% | Region-wide | Medium term (2-4 years) |

| Cloud-compute price inflation | −1.5% | Global | Medium term (2-4 years) |

| Talent gap in GenAI and zero-trust security | −1.2% | U.S., Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying CFPB and State Compliance Costs

Direct CFPB supervision now applies to about seven large nonbank payment providers, expanding examination scope to data privacy, fraud-refund timing, and account closures[3]Consumer Financial Protection Bureau, “Final Rule: Large Nonbank Payment Providers,” cfpb.gov. . California and New York regulators initiated 37% of fintech enforcement actions in 2024, collecting USD 30 million in consumer restitution. Although an April 2025 CFPB memo signals fewer federal sweeps, the requirement to publicly file all settlement orders under the nonbank registry rule raises reputational stakes for compliance lapses.

Rising Cyber-Insurance Premiums Post-Ransomware

Cyber insurance premiums surge following high-profile ransomware incidents affecting financial services, with 72% of companies exceeding cloud budgets and up to one-third of cloud spending wasted on unused resources. These cost pressures particularly impact API-heavy fintechs that rely on cloud infrastructure for scalability and real-time processing capabilities. Treasury and Financial Services Sector Coordinating Council resources for secure cloud adoption highlight regulatory focus on concentration risk in large cloud providers. FinOps implementations can reduce cloud spending by 20-30%, but require specialized expertise that competes with cybersecurity talent in tight labor markets. The cloud computing market's 16.8% CAGR through 2030 indicates continued cost inflation pressures that may force fintech consolidation or pricing adjustments to maintain unit economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Digital Payments Continue to Dominate

Digital payments controlled 47.86% of the North America fintech market share in 2025, translating to roughly USD 32.1 billion in segment revenue. Card-funded wallets ride the installed card-network rails, providing instant scale and merchant acceptance. PayPal alone processed USD 1.7 trillion in total payment volume, while Cash App’s monthly active users surpassed 55 million. Digital lending gained ground as AI underwriting models cut approval times to under 10 seconds, and digital investment portals grew assets by waiving commissions.

Neobanking, although smaller today, is forecast to race ahead at a 21.95% CAGR and could command more than one-fifth of the North America fintech market by 2031. Chime’s eight-million-plus account base illustrates the low-cost viral growth economics; its customer acquisition cost averages USD 20, versus nearly USD 925 for traditional banks. Insurtech startups using telematics and behavioral data are shaving loss ratios for auto and home policies. Across propositions, incumbents are embedding financing, insurance, and wealth modules directly inside consumer wallets, expanding average revenue per user without raising switching friction.

By End-User: Retail Leads but Business Adoption Is Accelerating

Retail use accounted for 58.92% of the North America fintech market size in 2025, reflecting widespread wallet penetration among smartphone owners. Consumers gravitate toward fee-free checking, automated budgeting, and cash-back rewards that outclass legacy bank accounts. P2P volumes surpassed USD 400 billion in 2024 as Venmo, Zelle, and Cash App became default money-movement channels for younger demographics.

Business-oriented fintech services, however, are on track for the faster 17.74% CAGR through 2031. SMEs increasingly prefer all-in-one point-of-sale packages bundling inventory, payroll, and lending. Toast’s USD 1.1 billion of 2024 gross profit, 87% of which came from payments and hardware, shows how payments-led platforms are monetizing operational data. Spend-management providers such as Brex, Ramp, and Airbase are issuing physical and virtual cards that route real-time expense data back into ERP systems, reducing manual reconciliation costs by 60–70%. Compliance badges such as SOC 2 and ISO 27001 have become table stakes for vendors selling into mid-market and enterprise tiers.

By User Interface: Mobile Apps Hold the Lion’s Share

Mobile applications captured 63.61% of all front-end interactions in 2025, cementing smartphones as the primary gateway to financial services. Push-notification rails enable context-aware offers, and biometric logins have reduced abandoned sessions. PayPal reports that more than 70% of its transactions now originate on mobile screens.

POS and IoT devices are the fastest-rising interface category, set to expand at a 19.6% CAGR. Square’s evolution from dongles to full cloud-based registers underscores the shift toward hardware-software-payments convergence. Connected vending machines, parking meters, and mobility turnstiles are embedding NFC readers that authorize payments without phones or cards, creating ambient commerce. Browser-based portals remain vital for back-office workflows such as reconciliation, lending dashboards, and investment analysis, but their share of total user minutes is declining each year.

Geography Analysis

The North American fintech market remains anchored in the United States, which generated 72.05% of the 2025 transaction value on the back of mature banking infrastructure, deep venture funding, and regulatory clarity. FedNow has introduced instant settlement across all 50 states, and more than 900 institutions have connected to the service, positioning banks to monetize request-to-pay overlays. While CFPB oversight raises compliance outlays, it also standardizes rules of the road, lowering macro legal uncertainty for scaled players.

Canada contributes a modest but stable share, buoyed by open-banking consultations and strong capital-market pipelines. Fintech investment hit USD 9.5 billion in 2024 after high-profile deals involving Nuvei and Neo Financial. Cross-border e-commerce flows with the United States encourage product localization more than new regulatory approval, allowing Canadian providers to adapt U.S. codebases with limited rewrites.

Mexico is the breakout growth story, projected to deliver a 16.9% CAGR and lift its share of the North America fintech market beyond 10% by 2031. Internet penetration has reached 81.2%, and the country now hosts more than 1,000 active fintech firms serving 70 million users. Mercado Libre’s fintech arm grew its 2024 revenue by 37%, underscoring the headroom in payments and credit among underbanked populations. The Comisión Nacional Bancaria y de Valores continues to refine sandbox regimes that foster innovation while monitoring systemic risk.

Competitive Landscape

The North American fintech market exhibits moderate concentration with the top five players commanding significant market share, indicating significant fragmentation and competitive intensity across multiple service categories. PayPal leads the market peer segment revenue share in Q1 2025, leveraging its USD 1.7 trillion annual payment volume and 400 million active accounts to maintain its market position despite intensifying competition. However, organic growth disruption increasingly drives market consolidation more than merger and acquisition activity, with digital-native providers like Stripe, Square, and Adyen collectively gaining significant market share between 2016-2021 through superior technology and customer experience rather than acquisitions[4]Joel Van Arsdale and Sameer Verma, “M&A No Longer the Key Driver of Consolidation in U.S. Merchant Payments,” Flagship Advisory Partners, flagshipadvisorypartners.com..

Strategic differentiation emerges through vertical specialization and integrated service offerings that create switching costs and customer stickiness. Toast's success in restaurant point-of-sale systems, generating 87% of gross revenues from payments and adjacent services rather than software subscriptions, exemplifies how vertical focus enables premium pricing and comprehensive customer relationships. Incumbent processors retain wholesale payment volume but lose merchant margin as integrated software vendors capture pricing power through bundled solutions that combine payments with business management tools. Banking-as-a-Service partnerships create new competitive dynamics as traditional banks monetize regulatory charters and infrastructure while fintechs focus on customer experience and product innovation, though recent operational failures like Synapse highlight execution risks in these arrangements.

White-space opportunities emerge in cross-border B2B payment orchestration for mid-market exporters and GenAI-driven hyper-personalized wealth management micro-pods that leverage artificial intelligence to provide customized investment advice and portfolio management services. The Federal Deposit Insurance Corporation's enhanced recordkeeping requirements for Banking-as-a-Service relationships create compliance frameworks that may consolidate the market toward established players with robust operational infrastructure while raising barriers for new entrants.

North America Fintech Industry Leaders

PayPal

Fiserv

Stripe

Block (Square & Cash App)

FIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Juspay partnered with Recurly to integrate its open-source payment orchestration platform, Hyperswitch, into Recurly's subscription billing ecosystem, enabling merchants to access over 300 payment service providers (PSPs), improve payment success rates, and accelerate expansion into global markets.

- June 2026: Juspay joined the Mastercard Engage partner network as a certified partner for Click to Pay, strengthening secure, tokenized checkout capabilities for enterprise merchants worldwide.

- March 2025: PayPal unveiled its “PayPal 2.0” roadmap targeting high-single-digit gross-profit growth and low-teens EPS growth by 2027 through AI-driven checkout optimization and a USD 50 billion debit-card TPV goal.

- January 2025: CFPB finalized direct federal supervision of nonbank payment providers processing more than 50 million transactions per year, affecting the seven largest wallet and P2P platforms.

North America Fintech Market Report Scope

The fintech market is defined as the sector encompassing technology-driven financial services and solutions within the region. This market includes various innovations and services such as digital payments, online banking, blockchain technology, robo-advisors, peer-to-peer lending, and financial management platforms.

The North American Fintech Market is segmented by service proposition and country. By service proposition, the market is segmented into money transfer and payments, savings and investments, digital lending and lending marketplaces, online insurance and insurance marketplaces, and other service propositions (digital banking). By country, the market is segmented into the United States, Canada, and the Rest of North America. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending & Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| Canada |

| United States |

| Mexico |

| By Service Proposition | Digital Payments |

| Digital Lending & Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Geography | Canada |

| United States | |

| Mexico |

Key Questions Answered in the Report

How large is the North America fintech market in 2026?

It stands at USD 77.01 billion and is projected to reach USD 154.33 billion by 2031.

Which service proposition leads regional revenue?

Digital payments hold 47.86% of 2025 revenue and remain the core growth engine.

What is driving the rapid rise of neobanks?

Customer acquisition costs under USD 25 per account and mobile-first design fuel a 21.95% CAGR outlook.

Why are SMEs adopting integrated POS platforms?

Bundled software and payments cut operational complexity and unlock lending and analytics features.

How will FedNow influence the competitive landscape?

Instant settlement enables request-to-pay overlays that can lift non-interest income at banks and wallets alike.

Which geography is expected to grow fastest through 2031?

Mexico, with a 16.9% CAGR, driven by high internet penetration and an underbanked population.

Page last updated on: